|

시장보고서

상품코드

1801910

수용성 비료 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Water Soluble Fertilizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

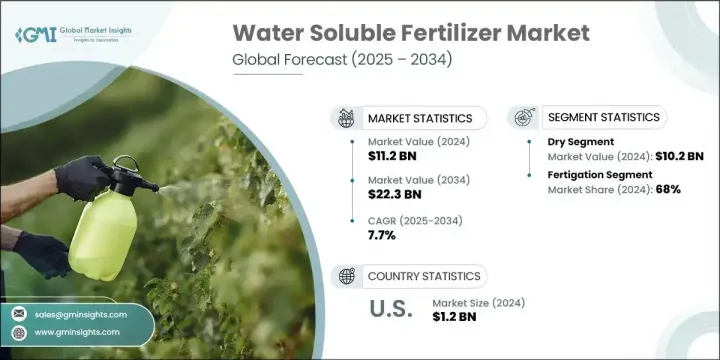

세계의 수용성 비료 시장은 2024년에는 112억 달러로 평가되었고, CAGR 7.7%로 성장하여 2034년에는 223억 달러에 이를 것으로 예측되고 있습니다.

이 성장이 예상되는 배경에는 정밀 농업을 지원하고 증가하는 식량 수요를 충족시키는 효율적이고 즉각적인 비료에 대한 수요가 증가하고 있습니다. 수용성 처방의 장점, 특히 최신 관개 시스템과의 적합성에 대한 인식이 높아짐에 따라 생산자는 기존의 비료에서 꾸준히 전환하고 있습니다. 수용성 비료는 흡수가 빠르고 영양소 공급 목표가 명확하고 지속 가능한 농법에 적합하기 때문에 선호됩니다. 또, 온실 재배나 특수 작물에도 널리 사용되고 있는 것도, 수요의 일인이 되고 있습니다. 고부가가치 작물과 한정된 농지에서의 생산성 향상에 대한 요구가 시장 도입을 가속화하고 있습니다.

이러한 기회에도 불구하고 시장은 여러 장애물에 직면하고 있습니다. 제품 가격이 높고 신흥국 시장에서는 정교한 관개에 대한 액세스가 제한되어 있고 일부 지역에서는 낮은 인지도가 있어 시장 확대를 제한할 수 있습니다. 수용성 비료는 적용하기 쉽고 식물을 사용할 수 있기 때문에 생산자에게 매력적입니다. 수용성 비료는 관개 시스템에 통합되거나 토양에 직접 적용될 수 있으므로 적용량과 타이밍을 보다 자유롭게 제어할 수 있습니다. 전통적인 작물과 고가치 작물의 생산자들 사이에서 관심이 높아짐에 따라 지속 가능하고 환경 친화적인 선택이 선호되고 시장 상황은 계속 변화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 112억 달러 |

| 예측 금액 | 223억 달러 |

| CAGR | 7.7% |

2024년 점유율은 관개 분야가 68%를 차지합니다. 영양소 적용과 절수방법의 개선이 진행되고 있는 가운데 관개를 통해 양분을 공급하는 시비가 가장 효율적인 접근법으로 부상해 왔습니다. 이것은 노력을 최소화하고 양분의 이용을 극대화합니다. 엽면 먹이는 또한 성장하는 기술이며 식물의 부족을 치료하는 빠른 양분 공급 방법을 제공합니다. 게다가, 방출 제어형 비료가 일반적으로 되고 있어, 안정된 양분 공급을 확보해, 반복 시용할 필요성을 줄임으로써, 자원 절약을 지지하고 있습니다.

제품 유형 중 보존 기간이 길고 보관이 용이하며 계량이 쉬운 분말 제제가 인기입니다. 그러나 분진이 나기 쉽고 취급이 어렵다는 단점도 있습니다. 액체 비료는 영양분의 흡수가 뛰어나 다른 액체와의 혼합성도 좋지만, 보존 기간이 짧기 때문에 수송이나 보관에 과제가 있습니다. 입상 비료는 사용의 용이성과 보존 기간의 길이가 균형을 이루고 있지만 가격이 높아지는 경향이 있습니다. 생산자는 비용, 살포 편의성, 특정 작물의 요구에 따라 이러한 제형 중에서 선택합니다.

미국 수용성 비료 2024년 시장 규모는 12억 달러. 정밀농업으로의 전환과 양분이용효율의 향상이 진행되어 수용성 비료 수요가 증가하고 있습니다. 농부는 관개에 적합한 드립 관개와 피벗 관개 시스템을 빠르게 채택하고 있습니다. 이 기술은 식물의 뿌리 지역으로의 양분 공급을 보장하고 흡수를 향상시키고 유출로 인한 손실을 최소화하여 비용 절감과 보다 효율적인 비료 사용을 초래합니다.

세계의 수용성 비료 시장에서 활약하는 주요 기업으로는 Sinochem Hong Kong(Group) Co., Ltd., Yara International ASA, Nutrien Ltd., Haifa Group, Israel Chemicals Ltd.(ICL) 등이 있습니다. 수용성 비료 시장의 주요 기업은 세계의 지위를 강화하기 위해 제품 혁신, 지리적 확대, 전략적 파트너십의 조합을 추구하고 있습니다. 연구개발은 계속해서 최우선 과제이며, 각 사는 작물별로 커스터마이즈한 솔루션, 최신의 관개 시스템에 대응한 배합을 개발하고 있습니다. 각 회사는 또한 정밀 시비를 지원하고 생산자가 데이터 주도로 의사 결정할 수 있도록 하는 디지털 플랫폼에 투자하고 있습니다. 농업의 현대화가 기세를 늘리는 신흥 시장에 진출하면 새로운 수요를 끌어들이는데 도움이 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적 인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 규모와 예측 : 형태별, 2021년-2034년

- 주요 동향

- 건조

- 분말

- 과립

- 액체

제6장 시장 규모와 예측 : 제품별, 2021년-2034년

- 주요 동향

- 질소

- 우레아

- 질산암모늄

- 질산칼슘

- 기타

- 미량 영양소

- 철

- 망간

- 기타

- 인산

- 인산1암모늄

- 인산

- 기타

- 칼륨

- 염화칼륨

- 황산칼륨

- 질산칼륨

제7장 시장 규모와 예측 : 신청 방법별, 2021년-2034년

- 주요 동향

- 잎면 살포

- 시비 관수

제8장 시장 규모와 예측 : 작물별, 2021년-2034년

- 주요 동향

- 곡물

- 야채

- 과일

- 농장

- 잔디 및 관상용 식물

- 온실작물

제9장 시장 규모와 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Yara International

- Israel Chemicals

- Nutrien

- Everris

- Sinochem Hong Kong

- Haifa Group

- AGAFERT

- KS Aktiengesellschaft

- COMPO EXPERT

- The Mosaic Company

- Coromandel International

- VAKI-CHIM

The Global Water Soluble Fertilizer Market was valued at USD 11.2 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 22.3 billion by 2034. This anticipated growth stems from rising demand for efficient, fast-acting fertilizers that support precision farming and meet growing food requirements. As awareness around the advantages of water-soluble formulations increases-especially their compatibility with modern irrigation systems-growers are steadily shifting away from conventional fertilizers. These fertilizers are favored for their rapid absorption, targeted nutrient delivery, and compatibility with sustainable practices. Their widespread use in greenhouse farming and specialty crops also contributes to demand. High-value crops and the need for increased productivity from limited farmland are accelerating market adoption.

Despite these opportunities, the market faces some hurdles. High product prices, limited access to advanced irrigation in developing nations, and low awareness in some areas may restrict market expansion. Water-soluble fertilizers appeal to growers due to their simplicity in application and plant availability. These fertilizers can be integrated into irrigation systems or applied directly to the soil, offering greater control over dosage and timing. As interest grows among traditional and high-value crop growers, the preference for sustainable, eco-conscious options continues to reshape the market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.2 Billion |

| Forecast Value | $22.3 Billion |

| CAGR | 7.7% |

The fertigation segment accounted for a 68% share in 2024. With ongoing improvements in nutrient application and water conservation methods, fertigation-delivering nutrients through irrigation-has emerged as the most efficient approach. It minimizes labor and maximizes nutrient use. Foliar feeding is another growing technique, offering a fast nutrient delivery method to treat plant deficiencies. Additionally, controlled-release fertilizers are becoming more common, ensuring a steady nutrient supply and reducing the need for repeated applications, thus supporting resource conservation.

Among product types, the powdered formulations are popular due to their long shelf life, ease of storage, and simple measurement. However, they can be dusty and difficult to handle. Liquid fertilizers offer superior nutrient uptake and mix well with other liquids but face challenges in transport and storage due to shorter shelf life. Granules offer a balance of ease of use and long shelf life, though they tend to be pricier. Growers select among these forms based on cost, application convenience, and specific crop needs.

U.S. Water Soluble Fertilizer Market generated USD 1.2 billion in 2024. The nation's increasing shift toward precision agriculture and enhanced nutrient use efficiency has pushed demand for water-soluble fertilizers. Farmers are rapidly adopting drip and pivot irrigation systems, which are well-suited for fertigation. This technique ensures nutrient delivery to plant root zones, improves uptake, and minimizes losses through runoff, leading to cost savings and more efficient fertilizer use.

Key players active in the Global Water Soluble Fertilizer Market include Sinochem Hong Kong (Group) Co., Ltd., Yara International ASA, Nutrien Ltd., Haifa Group, and Israel Chemicals Ltd. (ICL). To strengthen their global position, leading companies in the water-soluble fertilizer market are pursuing a combination of product innovation, geographic expansion, and strategic partnerships. R&D remains a top priority, with firms developing customized, crop-specific solutions and formulations compatible with modern irrigation systems. Companies are also investing in digital platforms that support precision application and enable growers to make data-driven decisions. Expanding into emerging markets where agricultural modernization is gaining momentum helps capture new demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Form

- 2.2.2 Product

- 2.2.3 Crop

- 2.2.4 Application

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dry

- 5.2.1 Powder

- 5.2.2 Granules

- 5.3 Liquid

Chapter 6 Market Size and Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Nitrogenous

- 6.2.1 Urea

- 6.2.2 Ammonium nitrate

- 6.2.3 Calcium nitrate

- 6.2.4 Others

- 6.3 Micronutrient

- 6.3.1 Iron

- 6.3.2 Manganese

- 6.3.3 Others

- 6.4 Phosphatic

- 6.4.1 Mono-ammonium phosphate

- 6.4.2 Phosphoric acid

- 6.4.3 Others

- 6.5 Potassium

- 6.5.1 Potassium chloride

- 6.5.2 Potassium sulfate

- 6.5.3 Potassium nitrate

Chapter 7 Market Size and Forecast, By Mode of Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Foliar

- 7.3 Fertigation

Chapter 8 Market Size and Forecast, By Crop, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Cereals

- 8.3 Vegetables

- 8.4 Fruits

- 8.5 Plantation

- 8.6 Turf & ornamentals

- 8.7 Greenhouse crops

Chapter 9 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Yara International

- 10.2 Israel Chemicals

- 10.3 Nutrien

- 10.4 Everris

- 10.5 Sinochem Hong Kong

- 10.6 Haifa Group

- 10.7 AGAFERT

- 10.8 K+S Aktiengesellschaft

- 10.9 COMPO EXPERT

- 10.10 The Mosaic Company

- 10.11 Coromandel International

- 10.12 VAKI-CHIM