|

시장보고서

상품코드

1833628

보청기 시장 : 시장 기회 및 촉진요인, 업계 동향 분석, 예측(2025-2034년)Hearing Amplifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

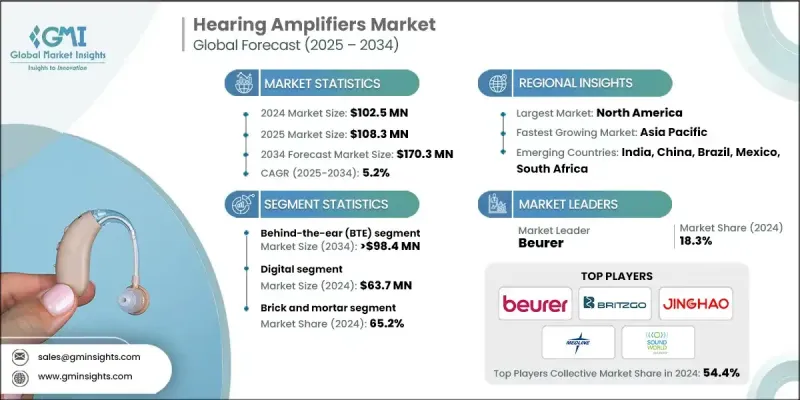

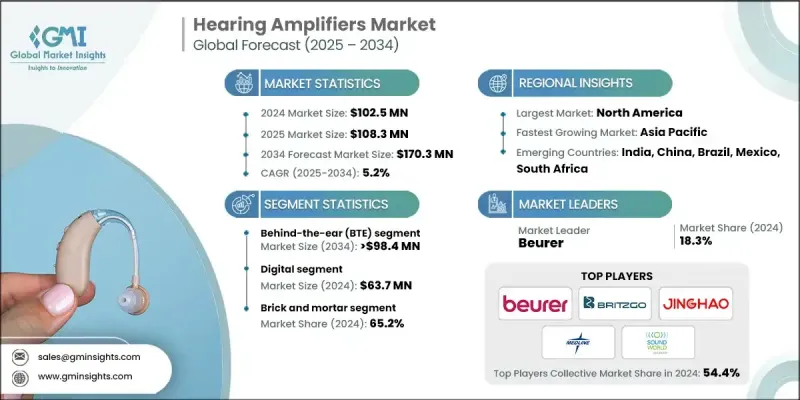

세계의 보청기 시장은 2024년에는 1억 250만 달러로 평가되었고, CAGR 5.2%로 성장할 전망이며, 2034년에는 1억 7,030만 달러에 이를 것으로 예측됩니다.

이 성장에는 난청 경험자 증가, 세계 인구의 급속한 노화, 음향 증폭 기술의 지속적인 혁신, 인지도 및 소비자 수용 증가 등 몇 가지 중요한 요인이 있습니다. 개인 음향 증폭기(PSAP)라고 불리는 이 제품은 경도에서 중등도 난청자를 위해 주변 소리의 볼륨을 높이도록 설계되었습니다. 전통적인 보청기와 달리 PSAP는 의료기기로 분류되지 않으므로 청각 전문의가 필요 없으며 매장에서 쉽게 얻을 수 있습니다. 합리적인 가격과 편의성으로 많은 사람들, 특히 고가의 보청기에 대한 투자를 주저하는 노인들에게 매력적인 선택이 되고 있습니다. 주요 기업은 전략적 지리적 포지셔닝, 제품 혁신에 대한 강한 고집, 연구개발에 대한 엄청난 투자를 통해 경쟁력을 유지하고 보청기 제품을 연마하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 1억 250만 달러 |

| 예측 금액 | 1억 7,030만 달러 |

| CAGR | 5.2% |

2024년에는 귀걸이형(BTE) 분야가 59%의 점유율을 차지했습니다. 이 분야는 사용자 친화적인 기능, 강력한 증폭 능력 및 다양한 정도의 청각 장애에 대한 적합성으로 인기를 얻고 있습니다. BTE 모델은 귀걸이형에 비해 조정이 쉽고 편안하며 인체공학적으로 뛰어나 고령 소비자, 특히 손이 불편한 소비자에게 지지됩니다. 이와 같은 품질로 BTE 보청기는 광범위한 층에 선호되는 솔루션이 되어 시장에서의 우위성을 더욱 확고하게 하고 있습니다.

아날로그 부문은 2034년까지 연평균 복합 성장률(CAGR) 5.5%를 보일 것으로 예측됩니다. 비용 효과를 선호하는 소비자는 아날로그 모델에 계속 끌려가고 있습니다. 그 매력은 저렴한 가격뿐만 아니라 사운드 설정을 사용자 정의할 수 있는 간단하고 사용하기 쉬운 조작성에도 있습니다. 이러한 특징은 선진국, 개발도상국을 불문하고, 퍼스널 사운드 앰프에 기능적이고 예산 중시의 선택지를 요구하는 구매층을 끌어안고 있습니다.

북미의 보청기 시장은 2024년에 38.5%의 점유율을 차지했습니다. 이 지역의 성장의 주요 원동력이 되고 있는 것은 규제 상황의 변화, 특히 시판(OTC) 보청기의 인가입니다. 이러한 정책 전환은 기존 진입 장벽을 제거하고 소매 채널을 확대하며 소비자가 의사의 진찰을 받지 않고 이용하기 쉬운 청각 솔루션을 검토할 수 있게 함으로써 새로운 성장 기회를 창출하고 있습니다. 이러한 변화로 인해 보청기의 인지도와 관심이 지역 전체에서 크게 높아지고 있습니다.

보청기 산업을 적극적으로 형성하는 주요 기업으로는 MEDCA HEARING, JINGHAO, Sound World Solutions, Diglo, NUHEARA, Beurer, Alango, Medline, Britzgo, Kinetik Medical, Innerscope Hearing Technologies, Conversor, Foshan Vohom Technology 등이 있습니다. 보청기 시장에서 발판을 굳히기 위해 각 회사는 제품 혁신에 중점을 두고 노인 소비자에게 맞는 인체 공학적이고 고성능 디자인에 중점을 둡니다. 많은 기업들은 기능성, 음질, 사용자 제어를 강화하기 위해 연구 개발에 많은 투자를 하고 있습니다. 무선 기술과 소형화의 진보를 활용함으로써, 각사는 사용하기 쉽고, 겸손하며 강력한 기기를 제공하는 것을 목표로 하고 있습니다. OTC 및 온라인 소매 채널을 통한 유통 확대는 접근성을 높이는 데 도움이 됩니다. 게다가, 의료 제공자와의 제휴나 인지도 향상을 목표로 한 프로모션 활동에 의해 기업은 보다 폭넓은 층을 받아들여, 성숙 시장과 신흥 시장 모두에서 브랜드의 존재감을 확고하게 하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 노화에 따른 난청 증가

- 고령화 인구 증가

- 증폭 및 노이즈 저감의 기술적 개선

- 업계의 잠재적 위험 및 과제

- 처방전 보청기 및 인공 내이와의 경쟁

- 한정된 환불 및 보험 적용 범위

- 시장 기회

- 온라인 판매 및 원격 청각 검사 플랫폼의 성장

- 제품의 소형화 및 인체공학의 개선

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- 소비자 경로

- 가격 분석(2024년)

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 귀걸이형(BTE)

- 귀에 장착하는 유형(ITE)

- 기타 제품

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 디지털

- 아날로그

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 점포

- 전자상거래

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Alango

- Beurer

- Britzgo

- Conversor

- Diglo

- Foshan Vohom Technology

- Innerscope Hearing Technologies

- JINGHAO

- Kinetik Medical

- MEDCA HEARING

- Medline

- NUHEARA

- Sound World Solutions

The Global Hearing Amplifiers Market was valued at USD 102.5 million in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 170.3 million by 2034.

This growth is fueled by several key factors, including the rising number of individuals experiencing hearing loss, a rapidly aging global population, continued innovation in sound amplification technologies, and increasing awareness and consumer acceptance. Hearing amplifiers, often referred to as personal sound amplification products (PSAPs), are designed to boost the volume of ambient sounds for people with mild to moderate hearing difficulties. Unlike traditional hearing aids, PSAPs are not classified as medical devices, making them easily accessible over the counter without the need for an audiologist. The affordability and convenience of these devices make them an appealing choice for many, especially older adults who are hesitant to invest in more expensive hearing aids. Leading companies are maintaining their competitive edge through strategic geographic positioning, a strong focus on product innovation, and significant investment in research and development to refine their hearing amplifier offerings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $102.5 Million |

| Forecast Value | $170.3 Million |

| CAGR | 5.2% |

In 2024, the behind-the-ear (BTE) segment held 59% share. This segment has gained popularity because of its user-friendly features, strong amplification capabilities, and compatibility with various degrees of hearing impairment. BTE models are favored by older consumers, especially those with limited hand dexterity, due to their ease of adjustment, comfort, and ergonomic benefits compared to in-ear devices. These qualities make BTE hearing amplifiers a preferred solution across a wide demographic, further solidifying their dominance in the market.

The analog segment is forecasted to grow at a CAGR of 5.5% through 2034. Consumers who prioritize cost-effectiveness continue to gravitate toward analog models. Their appeal lies not only in affordability but also in their simple, user-friendly controls that offer customizable sound settings. These features attract buyers in both developed and developing regions who want functional and budget-conscious options for personal sound amplification.

North America Hearing Amplifiers Market held 38.5% share in 2024. A significant driver of regional growth is the evolving regulatory landscape, particularly the authorization of over-the-counter (OTC) hearing devices. Such policy shifts have created new growth opportunities by removing traditional barriers to entry, expanding retail channels, and empowering consumers to explore accessible hearing solutions without medical consultations. These changes have significantly increased visibility and interest in hearing amplifiers across the region.

Key players actively shaping the Hearing Amplifiers Industry include MEDCA HEARING, JINGHAO, Sound World Solutions, Diglo, NUHEARA, Beurer, Alango, Medline, Britzgo, Kinetik Medical, Innerscope Hearing Technologies, Conversor, and Foshan Vohom Technology. To strengthen their foothold in the hearing amplifiers market, companies are emphasizing product innovation, focusing on ergonomic and high-performance designs tailored to older consumers. Many firms are investing heavily in R&D to enhance functionality, sound quality, and user control. By leveraging advances in wireless technology and miniaturization, companies aim to deliver discreet, powerful devices that are easy to use. Expanding distribution through OTC and online retail channels helps boost accessibility. In addition, partnerships with healthcare providers and promotional efforts aimed at raising awareness are enabling firms to tap into wider demographics and solidify brand presence in both mature and emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Technology trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of age-related hearing loss

- 3.2.1.2 Rising geriatric population base

- 3.2.1.3 Technological improvements in amplification and noise reduction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from prescription hearing aids and cochlear implants

- 3.2.2.2 Limited reimbursement/insurance coverage

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of online sales and tele-audiology platforms

- 3.2.3.2 Product miniaturization and improved ergonomics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Consumer pathway

- 3.7 Pricing analysis, 2024

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Behind-the-ear (BTE)

- 5.3 In-the-ear (ITE)

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Digital

- 6.3 Analog

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Brick and mortar

- 7.3 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alango

- 9.2 Beurer

- 9.3 Britzgo

- 9.4 Conversor

- 9.5 Diglo

- 9.6 Foshan Vohom Technology

- 9.7 Innerscope Hearing Technologies

- 9.8 JINGHAO

- 9.9 Kinetik Medical

- 9.10 MEDCA HEARING

- 9.11 Medline

- 9.12 NUHEARA

- 9.13 Sound World Solutions