|

시장보고서

상품코드

1876578

자동차 신경망 처리 장치(NPU) 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Automotive Neural Processing Unit (NPU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

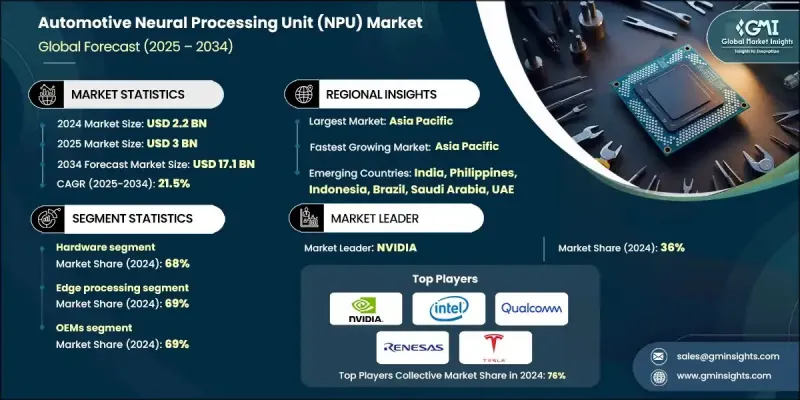

세계의 자동차 신경망 처리 장치(NPU) 시장은 2024년 22억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 21.5%를 나타내 171억 달러에 이를 것으로 예측됩니다.

차량의 NPU 활용 확대는 자동차가 방대한 센서 데이터를 실시간으로 처리하고 주변 환경을 해석하고 신속한 데이터 구동식 의사결정을 수행할 수 있게 함으로써 지능형 이동성에 혁명을 일으키고 있습니다. 이러한 전용 칩은 ADAS(첨단 운전자 보조 시스템), 자율주행 차량, 차량 내 인텔리전스를 위한 심층 학습 용도를 지원하여 안전성, 에너지 최적화, 운전 쾌적성을 대폭 향상시키고 있습니다. 자동차 제조업체 및 Tier 1 공급업체는 예측 분석, 저지연 데이터 융합 및 실시간 차량 의사결정을 지원하는 차세대 컴퓨팅 아키텍처를 설계 중입니다. 전동화와 커넥티드 모빌리티로의 전환이 진행되는 가운데 예측 에너지 제어, 고급 배터리 관리, V2G(차량에서 그리드로의 전력 공급) 연계를 위한 NPU 채용이 더욱 가속화되고 있습니다. 이러한 프로세서는 환경 조건 및 운전자 행동을 통해 학습함으로써 전기자동차의 경로 최적화 및 항속 거리 예측을 향상시킵니다. 엣지 컴퓨팅 및 클라우드 컴퓨팅과의 NPU 통합은 무선 업데이트(OTA), 지능형 진단 및 원격 최적화를 가능하게 하며 지속가능성에 대한 노력을 강화합니다. COVID-19 팬데믹은 자동차 밸류체인에서 디지털 변환을 가속화했습니다. 제조업체는 생산의 회복력을 확보하고, 엣지에 있어서 AI를 활용한 자기 복구형 자동차 시스템을 개발하기 위해, AI, 시뮬레이션, 원격 진단에의 의존도를 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 22억 달러 |

| 예측 금액 | 171억 달러 |

| CAGR | 21.5% |

하드웨어 부문은 2024년에 68%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 20.5%를 나타낼 것으로 예측됩니다. 하드웨어가 시장을 계속 독점하고 있는 이유는 NPU(Newral Processing Unit)가 AI 기반 차량 컴퓨팅의 핵심을 이루고 있기 때문입니다. 고급 프로세서와 System-on-Chip(SoC)에 통합된 NPU는 ADAS(첨단 운전자 보조 시스템), 자동 운전, 인포테인먼트 시스템에 필수적인 고속, 저지연, 병렬 데이터 처리를 실현합니다. 자동차 제조업체는 차량 생태계 내에서 직접 효율적인 실시간 의사 결정을 지원하고 클라우드 연결에 대한 의존도를 최소화하고 에지에서의 처리 효율성을 향상시키기 위해 하드웨어 혁신에 엄청난 투자를 하고 있습니다.

에지 처리 부문은 2024년에 69%의 점유율을 차지했고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 20.6%를 나타낼 것으로 예측됩니다. 에지 기반의 AI 처리가 중요성을 높이고 있는 배경에는 차량이 대량의 데이터를 직접 탑재 기기상에서 처리할 수 있기 때문에 지연을 줄이고 운전자 감시, 물체 감지, 네비게이션 등 중요한 안전 용도에서의 의사결정의 신속화를 도모할 수 있다는 점이 있습니다. 외부 네트워크에 대한 의존도를 줄임으로써 에지 NPU는 다양한 연결 환경에서 성능, 신뢰성 및 응답성을 향상시키고 지능형 차량 설계의 핵심 구성 요소 역할을 강화하고 있습니다.

중국의 자동차 신경망 처리 장치(NPU) 시장은 2024년 37%의 점유율을 차지하며 4억 2,390만 달러 규모에 이르렀습니다. 이 나라에서의 지능화·자동운전기술의 발전은 급속히 진행되고 있으며, 주요 성장거점으로서의 지위를 확립하고 있습니다. 정부의 지원책과 국가정책에 의해 국내 반도체 기술 혁신과 AI 하드웨어의 국산화가 촉진되고 있습니다. 중국을 대표하는 기술 기업은 실시간 센서 퓨전, 지각, 자율 제어용으로 자동차 등급의 NPU를 개발하고 있으며, 지역 경쟁력을 더욱 강화하는 동시에 자동차 AI 컴퓨팅 분야에서 해외 의존도의 저감을 도모하고 있습니다.

세계의 자동차 신경망 처리 장치(NPU) 시장의 주요 기업은 NVIDIA, Tesla, AMD, 르네사스, Intel(Mobileye), NXP, Hailo, Amazon, IBM, Qualcomm 등이 있습니다. 자동차 신경망 처리 장치 업계의 기업은 차세대 자율주행차 및 커넥티드카 용도를 지원하는 고성능, 절전 칩셋 개발에 주력하고 있습니다. 많은 기업들이 주요 자동차 제조업체와 Tier 1 공급업체와의 제휴를 추진하고 있으며, 자사의 NPU를 차량 제어 시스템과 ADAS 플랫폼에 통합하고 있습니다. R&D 투자는 에지 AI 컴퓨팅의 향상, 심층 학습 알고리즘 최적화, 복잡한 자동차 워크로드를 위한 칩 확장성 향상을 목표로 하고 있습니다. 또한 반도체 제조업체는 생산 능력을 확대하고 소프트웨어와 하드웨어의 공동 설계에 주력함으로써 전기자동차(EV) 및 자동 운전 차량 군에 유연한 도입을 실현하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- ADAS 및 자율주행차의 보급 확대

- AI 탑재 인포테인먼트 시스템에 대한 수요 증가

- 차량의 안전 및 보안 기준에 관한 규제의 추진

- 소프트웨어 정의 차량 아키텍처로의 전환

- 실시간 처리를 위한 엣지 컴퓨팅 요건

- 업계의 잠재적 위험 및 과제

- 초기 도입 및 유지 관리 비용의 높이

- 공급망의 취약성과 반도체 부족

- 시장 기회

- 뉴로모픽 컴퓨팅의 통합

- V2X 통신과 엣지 컴퓨팅의 확장

- 자율형 플릿 도입

- 소프트웨어 수익화 모델

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 분석

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 코스트 내역 분석

- 비즈니스 케이스 및 투자 이익률(ROI) 분석

- 총소유비용(TCO) 프레임워크

- ROI 산출 조사 방법

- 도입 스케줄과 이정표

- 리스크 평가 및 경감책

- 지속가능성과 환경영향 분석

- 수명 주기 평가 및 환경 모델링

- 지속가능한 설계와 최적화

- 환경 컴플라이언스 및 보고

- 그린테크놀로지와 혁신

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수 및 합병

- 제휴 및 공동 사업

- 신제품 발매

- 사업 확장 계획과 자금 조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 하드웨어

- NPU 칩

- 가속기

- 프로세서

- 소프트웨어

- AI 프레임워크

- SDK

- 드라이버

- 서비스

- 통합

- 유지보수

- 컨설팅

제6장 시장 추계·예측 : 처리 방식별(2021-2034년)

- 주요 동향

- 엣지 처리

- 클라우드 처리

- 하이브리드 처리

제7장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- MPV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 전기자동차

제8장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- ADAS(첨단 운전자 보조 시스템)

- 자율 주행

- 차량 내 인포테인먼트(IVI)

- 운전자 모니터링 시스템(DMS)

- 교통 표지 및 물체 인식

- 예측 유지보수 및 차량 진단

- 기타

제9장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- LAMEA 지역

- 브라질

- 멕시코

- 아르헨티나

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계의 기업

- Advanced Micro Devices

- Broadcom

- Intel

- MediaTek

- Mobileye Global

- NVIDIA

- Qualcomm Technologies

- Tesla

- 지역 기업

- Aptiv

- Continental

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Robert Bosch

- STMicroelectronics

- Valeo

- 신흥기업

- Ambarella

- Black Sesame Technologies

- Blaize

- Esperanto Technologies

- Hailo Technologies

- Horizon Robotics

- Kneron

The Global Automotive Neural Processing Unit (NPU) Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 17.1 billion by 2034.

The expanding use of NPUs in vehicles is revolutionizing intelligent mobility by enabling cars to process vast sensor data in real time, interpret their surroundings, and execute rapid, data-driven decisions. These specialized chips power deep learning applications for advanced driver-assistance systems (ADAS), autonomous vehicles, and in-cabin intelligence, significantly enhancing safety, energy optimization, and driving comfort. Automotive manufacturers and Tier-1 suppliers are designing next-generation computing architectures that support predictive analytics, low-latency data fusion, and real-time vehicle decision-making. The ongoing shift toward electrification and connected mobility has further accelerated NPU adoption for predictive energy control, advanced battery management, and vehicle-to-grid coordination. These processors also improve route optimization and range prediction in electric vehicles by learning from environmental conditions and driver behavior. Integration of NPUs with edge and cloud computing enables over-the-air (OTA) updates, intelligent diagnostics, and remote optimization, strengthening sustainability efforts. The COVID-19 pandemic also sped up digital transformation in the automotive value chain, as manufacturers increasingly relied on AI, simulation, and remote diagnostics to ensure production resilience and develop self-healing automotive systems with AI at the edge.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $17.1 Billion |

| CAGR | 21.5% |

The hardware segment held a 68% share in 2024 and is projected to grow at a CAGR of 20.5% through 2034. Hardware continues to dominate the market because NPUs are at the heart of AI-based vehicle computing. Integrated within advanced processors and SoCs, they enable high-speed, low-latency, parallel data processing essential for ADAS, autonomous driving, and infotainment systems. Automakers are heavily investing in hardware innovation to support efficient, real-time decision-making directly within the vehicle ecosystem, minimizing reliance on cloud connectivity and improving processing efficiency at the edge.

The edge processing segment held a 69% share in 2024 and is estimated to grow at a CAGR of 20.6% from 2025 to 2034. Edge-based AI processing is gaining prominence because it allows vehicles to process large data volumes directly on board, reducing delays and ensuring faster decision-making in critical safety applications such as driver monitoring, object detection, and navigation. By reducing dependence on external networks, edge NPUs deliver improved performance, reliability, and responsiveness under varying connectivity conditions, reinforcing their role as a vital component in intelligent vehicle design.

China Automotive Neural Processing Unit (NPU) Market held a 37% share and generated USD 423.9 million in 2024. The country's rapid progress in intelligent and self-driving vehicle technologies has positioned it as a major growth hub. Supportive government initiatives and national policies have encouraged domestic semiconductor innovation and AI hardware localization. Leading Chinese technology firms are designing automotive-grade NPUs for real-time sensor fusion, perception, and autonomous control, further strengthening regional competitiveness and reducing foreign dependency in automotive AI computing.

Key players operating in the Global Automotive Neural Processing Unit (NPU) Market include NVIDIA, Tesla, AMD, Renesas, Intel (Mobileye), NXP, Hailo, Amazon, IBM, and Qualcomm. To strengthen their position, companies in the automotive neural processing unit industry are focusing on developing high-performance, energy-efficient chipsets that support next-generation autonomous and connected vehicle applications. Many firms are forming partnerships with leading automakers and Tier-1 suppliers to integrate their NPUs into vehicle control systems and ADAS platforms. R&D investments are being directed toward advancing edge AI computing, optimizing deep learning algorithms, and enhancing chip scalability for complex automotive workloads. Moreover, semiconductor manufacturers are expanding production capabilities and focusing on software-hardware co-design to ensure flexible deployment across EVs and autonomous fleets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Processing Type

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing ADAS & autonomous vehicle adoption

- 3.2.1.2 Rising demand for ai-powered infotainment systems

- 3.2.1.3 Regulatory push for vehicle safety & security standards

- 3.2.1.4 Shift toward software-defined vehicle architectures

- 3.2.1.5 Edge computing requirements for real-time processing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation and maintenance costs

- 3.2.2.2 Supply chain vulnerabilities & semiconductor shortages

- 3.2.3 Market opportunities

- 3.2.3.1 Neuromorphic computing integration

- 3.2.3.2 V2X communication & edge computing expansion

- 3.2.3.3 Autonomous fleet deployment

- 3.2.3.4 Software monetization models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Business Case & ROI Analysis

- 3.12.1 Total cost of ownership framework

- 3.12.2 ROI calculation methodologies

- 3.12.3 Implementation timeline & milestones

- 3.12.4 Risk assessment & mitigation strategies

- 3.13 Sustainability and environmental impact analysis

- 3.13.1 Lifecycle assessment and environmental modeling

- 3.13.2 Sustainable design and optimization

- 3.13.3 Environmental compliance and reporting

- 3.13.4 Green technology and innovation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LAMEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 NPU chips

- 5.2.2 Accelerators

- 5.2.3 Processors

- 5.3 Software

- 5.3.1 AI frameworks

- 5.3.2 SDKs

- 5.3.3 Drivers

- 5.4 Services

- 5.4.1 Integration

- 5.4.2 Maintenance

- 5.4.3 Consulting

Chapter 6 Market Estimates & Forecast, By Processing, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.1.1 Edge processing

- 6.1.2 Cloud processing

- 6.1.3 Hybrid processing

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUV

- 7.2.4 MPVs

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

- 7.4 Electric Vehicles

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Advanced Driver Assistance Systems (ADAS)

- 8.3 Autonomous Driving

- 8.4 In-Vehicle Infotainment (IVI)

- 8.5 Driver Monitoring Systems (DMS)

- 8.6 Traffic Sign & Object Recognition

- 8.7 Predictive Maintenance & Vehicle Diagnostics

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 LAMEA

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 South Africa

- 10.5.5 Saudi Arabia

- 10.5.6 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Advanced Micro Devices

- 11.1.2 Broadcom

- 11.1.3 Intel

- 11.1.4 MediaTek

- 11.1.5 Mobileye Global

- 11.1.6 NVIDIA

- 11.1.7 Qualcomm Technologies

- 11.1.8 Tesla

- 11.2 Regional Players

- 11.2.1 Aptiv

- 11.2.2 Continental

- 11.2.3 Infineon Technologies

- 11.2.4 NXP Semiconductors

- 11.2.5 Renesas Electronics

- 11.2.6 Robert Bosch

- 11.2.7 STMicroelectronics

- 11.2.8 Valeo

- 11.3 Emerging Players

- 11.3.1 Ambarella

- 11.3.2 Black Sesame Technologies

- 11.3.3 Blaize

- 11.3.4 Esperanto Technologies

- 11.3.5 Hailo Technologies

- 11.3.6 Horizon Robotics

- 11.3.7 Kneron