|

시장보고서

상품코드

1889166

복합 운송 시장 : 구성별, 최종 이용 산업별, 지역별 예측Multimodal Transport Market By Configuration (Two Mode, Three Mode, Hybrid/ Others), End-use Industry (Retail, Food & Beverages, Pharmaceuticals & Healthcare, Chemicals & Materials, Manufacturing), Region - Global Forecast to 2032 |

||||||

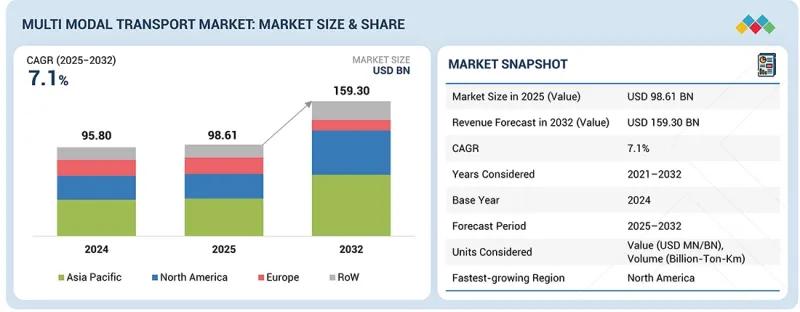

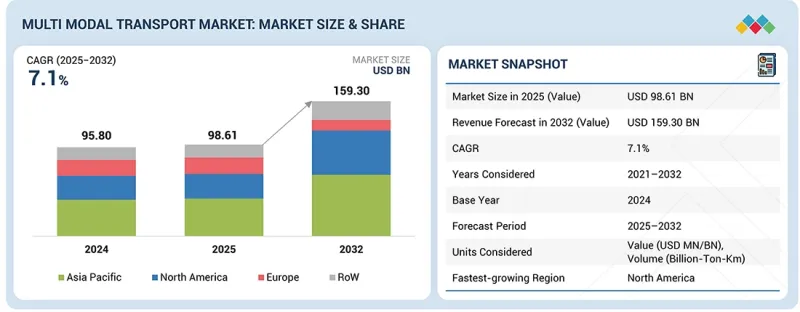

세계의 복합 운송 시장의 규모는 2025년 986억 1,000만 달러에서 2032년까지 1,593억 달러에 이를 것으로 예측되며 CAGR 7.1%의 성장이 예상됩니다.

시장 성장은 점차 분단화가 진행되는 세계 공급망에서 화물 운송을 효율화할 필요성과 단일 트럭 운송에서 통합된 도로, 철도, 수로 네트워크로의 이행에 의해 추진되고 있습니다. 특히 국경을 넘어서는 유통에서 시간적 제약이 중요시되는 가운데, 제조업체와 수출업체는 증가하는 출하수를 관리하고, 일정의 신뢰성을 향상시키고, 운송 시간의 변동을 줄이기 위해 복합 운송 서비스에 대한 의존도를 높이고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 단위 | 100만 또는 10억 달러, 10억톤 |

| 부문 | 구성, 최종 이용 산업, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미 및 기타 지역 |

엔드 투 엔드 시각화, 자동 문서 작성 및 동적 경로 최적화를 가능하게 하는 첨단 디지털 플랫폼은 단일 서비스 내에서 공동 운송의 추가 도입을 지원합니다. 새로운 복합 운송 터미널, 항만과 철도 연결, 내륙 수로의 상승, 복합 물류 파크를 포함한 인프라 업그레이드는 네트워크 유동성을 높이고 핸드 오프를 줄이면서 처리 능력을 향상시킵니다. 이산화탄소 감축 의무와 철도 및 연안 수송에 대한 우대조치 등 모달 시프트와 지속가능성을 촉진하는 정책이 저배출화물 수송과의 조합으로의 이행을 가속화하고 있습니다. 지정학적 혼란, 무역 루트 변화, 니어 쇼어링 동향으로 기업은 운송 루트의 다양화와 운송 네트워크에 대한 중복성 구축을 강요받고 있습니다. 탄력성, 비용 관리 및 확장 가능한 처리 능력에 대한 수요가 증가함에 따라 운송업체와 물류 공급자 간의 긴밀한 협력을 촉진하고 있으며, 복합 운송은 미래에 대응할 수 있는 공급망의 중요한 기반으로 자리매김하고 있습니다.

"하이브리드 방식 구성은 복합 운송 시장에서 예측 기간에 큰 수요를 나타낼 전망입니다."

하이브리드 방식 구성은 복합 운송 시장에서 예측 기간에 상당한 수요를 나타낼 전망입니다. 이는 변화하는 무역 조건과 네트워크 제약에 있어서 기업이 화물의 유연한 이동을 점점 요구하게 되기 때문입니다. 고정적인 투웨이 구성과 달리 하이브리드 구성에서는 운송 능력의 여유 상황, 루트의 접근성, 서비스 우선도에 근거해 도로, 철도, 수로나 도로, 항공, 수로 등의 다른 수송 방식의 조합으로 화물을 이행시킬 수 있습니다. 이 적응성이 높은 구조는 의약품, 전자기기, 고적층 제조 등 출하 패턴이 변동하는 업계에서 주목을 받고 있습니다. 이러한 업계에서는 납기 엄수와 위험 분산이 매우 중요합니다. 또한, 국경을 넘은 유통의 확대나 계절적인 수량의 급증도, 혼란 발생 시에 대체 항만이나 내륙 회랑으로 화물을 우회시킬 수 있는 하이브리드 수송의 채용을 촉진하고 있습니다. 물류 공급자는 주요 게이트웨이에서 복합 운송에 대한 연결성을 확대하고 운송업체 간의 협력을 강화하고 실시간 운송 방식을 전환할 수 있는 디지털 툴 통합을 통해 이러한 변화를 지원합니다. 공급망이 보다 민첩한 경영 모델로 전환하는 동안 지속성, 맞춤형 서비스 수준 및 국제적인 화물 흐름에 대한 관리 강화를 요구하는 화주들에게 하이브리드 방식 구성은 중요한 옵션으로 부상하고 있습니다.

"소매 최종 이용 산업이 2024년 복합 운송 시장에서 두 번째로 높은 점유율을 차지했습니다."

소매 최종 이용 산업은 소비자 구매 패턴의 급속한 진화와 다양한 유통기지 간의 제품 이동 동기화에 대한 요구가 증가함에 따라 2024년 복합 운송 시장에서 두 번째로 높은 점유율을 차지했습니다. 오프라인 매장, 온라인 플랫폼, 지역 배송 센터가 통합된 네트워크 역할을 하는 옴니채널 모델의 상승과 함께 소매업체는 빈번한 보충, 분산된 배송 경로 및 변동되는 주문 수를 처리할 수 있는 운송 솔루션이 필요합니다. 복합 운송 시스템을 통해 소매업체는 장거리 운송 효율성과 유연한 지역 배송을 결합할 수 있습니다. 대규모의 벌크 입하에는 해상 수송이나 철도를 이용해, 점포나 도시 거점으로의 시간을 엄수해야 하는 출하 활동에는 도로 수송을 활용합니다. 식료품 EC의 확대나 온도 관리를 필요로 하는 취급 품목 증가 또한 특히 운송 방식 간을 이행할 때의 품질 유지를 위해, 통합 물류에의 의존도를 높이고 있습니다. 게다가, 높은 반품률, 프로모션에 의한 수요의 급증, 휴일 시즌의 수요 증가에 의해 비용 부하를 증가시키지 않고 예측 가능한 리드 타임을 제공하는 운송 모델이 요구되고 있습니다.

이 보고서는 세계의 복합 운송 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 인사이트

- 복합 운송 시장에서의 기업에게 매력적인 기회

- 복합 운송 시장 : 지역별

- 복합 운송 시장 : 구성별

- 복합 운송 시장 : 최종 이용 산업별

제5장 시장 개요

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

제6장 기술, 특허, 디지털, AI의 채용에 의한 전략적 파괴

- 특허 분석

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 기술 로드맵

- 1단계 : 디지털 기반, 가시성(2024-2026년)

- 2단계 : 예측적, 커넥티드, 인텔리전트 업무(2027-2030년)

- 3단계 : 자율적, 하이퍼커넥티드, 지속가능 생태계(2031-2035년)

- 미래의 용도

- AI 및 생성형 AI의 영향

- 주요 이용 사례와 시장의 장래성

- 모범 사례

- 사례 연구

- AI 및 생성형 AI의 채용에 대한 클라이언트의 준비 상황

제7장 지속가능성과 규제정세

- 규제 상황

- 규제기관, 정부기관, 기타 조직

- 업계 표준

- 지속가능성에 대한 노력

- 지속가능성에 미치는 영향과 규제 정책의 노력

- EUROPEAN GREEN DEAL

- TRANS-EUROPEAN TRANSPORT NETWORK(TEN-T)

- PM GATI SHAKTI

- INFRASTRUCTURE INVESTMENT AND JOBS ACT(IIJA)

- 지속가능성에 미치는 영향과 규제 정책의 노력

- 지속 가능성의 필수요건이 복합 운송을 변화시킴

- 지속 가능한 복합 운송 업무를 추진하는 기업의 대처

- 시장의 영향 분석

제8장 업계 동향

- 거시경제지표

- GDP의 동향과 예측

- 세계의 복합 운송 업계 동향

- 생태계 분석

- 복합운송업자(MTO)

- 인프라 및 터미널 업자

- 기술제공자 및 디지털 플랫폼

- 규제기관 및 표준화 단체

- 최종 이용 산업

- 가격 설정 분석

- 화물 수송의 평균 판매 가격 : 방식별(2021-2024년)

- 도로 화물의 평균 판매 가격 : 지역별(2021-2024년)

- 철도 화물의 평균 판매 가격 : 지역별(2021-2024년)

- 항공 화물의 평균 판매 가격 : 지역별(2021-2024년)

- 내륙 수로의 평균 판매 가격 : 지역별(2021-2024년)

- 고객사업에 영향을 주는 동향과 혼란

- 투자 및 자금조달 시나리오

- 자금 조달 : 이용 사례별

- 주요 회의 및 이벤트

- 사례 연구 분석

- 2025년 미국 관세의 영향

- 주요 관세율

- 가격의 영향 분석

- 국가 및 지역에 미치는 영향

- 최종 이용 산업에 대한 영향

제9장 복합 운송 시장 : 서비스 유형별

- 화물 수송

- 창고 보관 및 배송

- 수송

- 부가가치 서비스

- 통관 중개

제10장 복합 운송 시장 : 솔루션별

- 공급망

- 화물

- 수송 방식

- 택배 우편

- 트럭 적재

- 발송

제11장 복합 운송 시장 : 구성별

- 투웨이 구성

- 쓰리웨이 구성

- 하이브리드 및 기타 구성

- 중요한 인사이트

제12장 복합 운송 시장 : 최종 이용 산업별

- 소매

- 식품 및 음료(F&B)

- 화학제품 및 재료

- 의약품 및 의료

- 제조

- 석유 및 가스

- 기타 최종 이용 산업

- 중요한 인사이트

제13장 복합 운송 시장 : 지역별

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 유럽

- 거시경제 전망

- 프랑스

- 독일

- 스페인

- 이탈리아

- 폴란드

- 기타 유럽

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 기타 지역

- 아르헨티나

- 브라질

- 사우디아라비아

- 튀르키예

- 기타

제14장 경쟁 구도

- 개요

- 주요 진입기업의 전략 및 강점

- 시장 점유율 분석(2024년)

- 수익 분석(2020-2024년)

- 기업 평가 및 재무 지표

- 브랜드 및 제품 비교

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

- 경쟁 시나리오

제15장 기업 프로파일

- 주요 기업

- DSV

- DEUTSCHE POST AG

- KUEHNE NAGEL

- NIPPON EXPRESS HOLDINGS

- AP MOLLER-MAERSK

- CMA CGM GROUP

- MARUBENI CORPORATION

- CH ROBINSON WORLDWIDE, INC.

- GEODIS

- XPO, INC.

- NYK LINE

- EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.

- UNITED PARCEL SERVICE OF AMERICA, INC.

- HAPAG-LLOYD AG

- KLN LOGISTICS GROUP LIMITED

- 기타 기업

- C & S TRANSPORTATION SERVICES, LLC.

- BDP INTERNATIONAL INC.

- CROWLEY

- DACHSER

- JB HUNT TRANSPORT, INC.

- RHENUS LOGISTICS SE & CO. KG.

- RYDER SYSTEM, INC.

- DP WORLD

- CJ LOGISTICS CORPORATION

- LOGISTEED, LTD.

제16장 부록

CSM 25.12.23The multimodal transport market is projected to reach USD 159.30 billion by 2032 from USD 98.61 billion in 2025 at a CAGR of 7.1%. Market growth is fueled by the need to streamline freight movement across increasingly fragmented global supply chains and the shift from single-mode trucking to integrated road-rail-waterway networks. Manufacturers and exporters are increasingly relying on multimodal services to manage rising shipment volumes, improve schedule reliability, and reduce transit variability, particularly as cross-border distribution becomes more time-sensitive.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion), Volume (Billion-Ton-Km) |

| Segments | By Configuration, End-use Industry, Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

Advanced digital platforms enabling end-to-end visibility, automated documentation, and dynamic route optimization, supporting greater adoption of coordinated transport under a single service umbrella. Infrastructure upgrades, including new intermodal terminals, port-rail links, the revival of inland waterways, and multimodal logistics parks, are enhancing network fluidity and enabling higher throughput with fewer handoffs. Policy measures promoting modal shift and sustainability, such as carbon-reduction mandates and incentives for rail and coastal shipping, are accelerating the transition toward lower-emission freight combinations. Geopolitical disruptions, shifting trade lanes, and nearshoring trends are prompting companies to diversify routing options and build redundancy into transport networks. The rising demand for resilience, cost discipline, and scalable capacity is also driving closer collaboration between shippers and logistics providers, positioning multimodal transport as a critical enabler of future-ready supply chains.

"Hybrid-mode configurations are expected to witness significant demand in the multimodal transport market during the forecast period."

Hybrid-mode configurations are expected to experience notable demand in the multimodal transport market during the forecast period, as companies increasingly require flexible movement of freight across changing trade conditions and network constraints. Unlike fixed two-mode arrangements, hybrid setups enable cargo to shift between different transport combinations, such as road-rail-waterways or road-air-waterways, based on capacity availability, route accessibility, and service priorities. This adaptable structure is gaining traction among industries with variable shipment patterns, including pharmaceuticals, electronics, and high-value manufacturing, where delivery timing and risk diversification are critical. Growth in cross-border distribution and seasonal volume surges is also encouraging the adoption of hybrid movements that can reroute cargo through alternative ports or inland corridors when disruptions occur. Logistics providers are supporting this shift by expanding multimodal connectivity at key gateways, enhancing coordination across carriers, and integrating digital tools that enable real-time mode switching. As supply chains shift toward more agile operating models, hybrid-mode configurations are emerging as a crucial option for shippers seeking continuity, tailored service levels, and enhanced control over international freight flows.

"The retail end-use industry held the second-largest share of the multimodal transport market in 2024."

The retail end-use industry accounted for the second-largest share of the multimodal transport market in 2024, driven by the rapid evolution of consumer buying patterns and the increasing need for synchronized product movement across diverse distribution points. With the rise of omnichannel models, where physical stores, online platforms, and regional fulfillment centers operate as a unified network, retailers require transport solutions that can handle frequent restocking, dispersed delivery routes, and fluctuating order volumes. Multimodal setups enable retailers to combine long-haul efficiency with flexible regional distribution, using sea or rail for bulk inbound flows and road for time-sensitive outbound movements to stores and urban hubs. The expansion of grocery e-commerce and temperature-controlled product lines is also creating greater reliance on integrated logistics, particularly for maintaining product integrity during transfers between modes. Additionally, high return rates, promotional spikes, and holiday-season surges demand transport models that offer predictable lead times without increasing cost burdens.

" Asia Pacific held the largest share of the multimodal transport market in 2024."

The Asia Pacific accounted for the largest share of the multimodal transport market in 2024, driven by its dominant position in global manufacturing, export-oriented production, and rapidly expanding regional trade flows. The presence of major industrial hubs across China, India, Japan, and Southeast Asia has created dense freight corridors that link factories, inland logistics zones, and maritime gateways, resulting in a high reliance on integrated road-rail-sea combinations for both domestic distribution and international shipment cycles. The region's extensive port network, including major transshipment centers such as Singapore, Shanghai, and Busan, enhances connectivity to North America, Europe, and the Middle East. The rising intra-Asia trade is increasing demand for shorter, multimodal routes between emerging consumer markets. Large-scale infrastructure programs, such as China's Belt and Road Initiative, India's multimodal logistics parks, and Southeast Asia's rail expansion projects, are improving capacity, reducing transfer bottlenecks, and enabling faster modal transitions. Additionally, rapid growth in e-commerce, urban consumption, and contract manufacturing is driving higher freight volumes that require coordinated transport solutions. As companies prioritize cost efficiency, resilience, and regional supply-chain integration, the Asia Pacific is expected to retain its leading position throughout the forecast period.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: MNC 90% and Tier I - 10%

- By Designation: C- Level 45%, Director-Level- 30%, and Others - 25%

- By Region: Asia Pacific - 35%, North America - 40%, and Europe - 25%

The multi-modal transport market is dominated by major players, including DSV (Denmark), Deutsche Post AG (Germany), Kuehne+Nagel (Switzerland), NIPPON EXPRESS HOLDINGS (Japan), and A.P. Moller - Maersk (Denmark). These companies are expanding their portfolios to strengthen their multimodal transport market position.

Research Coverage:

The report covers the multimodal transport market in terms of configuration type (two-mode, three-mode, and hybrid/others), end-use industry (retail, manufacturing, healthcare & pharmaceuticals, food & beverages, chemicals & materials, oil & gas, and others), and region. It covers the competitive landscape and company profiles of the significant multimodal transport market players.

The study also includes an in-depth competitive analysis of the key market players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the multimodal transport market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

- The report will also help stakeholders understand the current and future pricing trends of the multimodal transport market.

- The report will help market leaders/new entrants with information on various trends in the multimodal transport market based on configuration type, end-use industry, and region.

The report provides insight into the following points:

- Analysis of key drivers (electrification to dominate the freight movement globally, cost efficiency through optimization and dynamic mode routing), restraints (dominance of road transport due to its flexibility and reliability, hindering modal shifts, limited adoption among SMEs due to complexity and resource constraints), opportunities (market access and entry into new trade routes, reduction of trade barriers fosters smoother cross-border movement of goods), and challenges (regulatory and legal barriers, including varying policies across regions)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the multimodal transport market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the multimodal transport market across varied regions)

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the multimodal transport market

- Competitive Assessment: In-depth assessment of shares, growth strategies, and service offerings of leading players, such as DSV (Denmark), Deutsche Post AG (Germany), Kuehne+Nagel (Switzerland), NIPPON EXPRESS HOLDINGS (Japan), and A.P. Moller - Maersk (Denmark), in the multimodal transport market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary participants

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH LIMITATIONS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 3.3 DISRUPTIVE TRENDS SHAPING MARKET

- 3.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 3.5 MNM INSIGHTS INTO MULTIMODAL TRANSPORT

- 3.6 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MULTIMODAL TRANSPORT MARKET

- 4.2 MULTIMODAL TRANSPORT MARKET, BY REGION

- 4.3 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION

- 4.4 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Shift from conventional diesel-powered trucks to electric vehicles in logistics sector

- 5.2.1.1.1 Growth in electric truck sales

- 5.2.1.1.2 Policy and regulatory frameworks favoring electric truck adoption

- 5.2.1.2 Rise of sustainable fuels in transportation

- 5.2.1.3 Cost efficiency through optimization and dynamic mode routing

- 5.2.1.1 Shift from conventional diesel-powered trucks to electric vehicles in logistics sector

- 5.2.2 RESTRAINTS

- 5.2.2.1 Dominance of road transport due to its flexibility and reliability

- 5.2.2.2 Limited adoption among SMEs due to complexity and resource constraints

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Market access and entry into new trade routes

- 5.2.3.2 Reduction of trade barriers for smoother cross-border movement of goods

- 5.2.4 CHALLENGES

- 5.2.4.1 Regulatory and legal barriers

- 5.2.1 DRIVERS

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 PATENT ANALYSIS

- 6.1.1 LIST OF PATENTS

- 6.2 TECHNOLOGY ANALYSIS

- 6.2.1 KEY TECHNOLOGIES

- 6.2.1.1 Digital twins for transport networks

- 6.2.1.2 Multimodal transport management systems (TMS 2.0)

- 6.2.1.3 Blockchain

- 6.2.1.4 Autonomous & connected freight systems

- 6.2.1.5 Robotics & high-automation warehousing

- 6.2.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.2.1 Cybersecurity & secure access systems

- 6.2.2.2 RFID, NFC, and smart labeling

- 6.2.2.3 Power AR/VR for training and operations

- 6.2.3 ADJACENT TECHNOLOGIES

- 6.2.3.1 Holographic navigation interfaces

- 6.2.3.2 Urban and autonomous last-mile delivery

- 6.2.1 KEY TECHNOLOGIES

- 6.3 TECHNOLOGY ROADMAP

- 6.3.1 INTRODUCTION

- 6.3.2 PHASE 1 (2024-2026): DIGITAL FOUNDATION & VISIBILITY

- 6.3.3 PHASE 2 (2027-2030): PREDICTIVE, CONNECTED, AND INTELLIGENT OPERATIONS

- 6.3.4 PHASE 3 (2031-2035): AUTONOMOUS, HYPERCONNECTED, AND SUSTAINABLE ECOSYSTEMS

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES

- 6.5.3 CASE STUDIES

- 6.5.4 CLIENTS' READINESS TO ADOPT AI/GEN AI

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3.1 EUROPEAN GREEN DEAL

- 7.3.2 TRANS-EUROPEAN TRANSPORT NETWORK (TEN-T)

- 7.3.3 PM GATI SHAKTI

- 7.3.4 INFRASTRUCTURE INVESTMENT AND JOBS ACT (IIJA)

- 7.4 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4.1 SUSTAINABILITY IMPERATIVES TRANSFORMING MULTIMODAL TRANSPORT

- 7.4.1.1 Modal shift for emission reduction

- 7.4.1.2 Electrification & alternative fuels

- 7.4.1.3 Green corridors & eco-efficient hubs

- 7.4.2 CORPORATE INITIATIVES DRIVING SUSTAINABLE MULTIMODAL OPERATIONS

- 7.4.2.1 Digital optimization & AI

- 7.4.2.2 Green warehousing & intermodal terminals

- 7.4.3 MARKET IMPACT ANALYSIS

- 7.4.1 SUSTAINABILITY IMPERATIVES TRANSFORMING MULTIMODAL TRANSPORT

8 INDUSTRY TRENDS

- 8.1 MACROECONOMIC INDICATORS

- 8.1.1 INTRODUCTION

- 8.1.2 GDP TRENDS AND FORECAST

- 8.1.3 TRENDS IN GLOBAL MULTIMODAL TRANSPORT INDUSTRY

- 8.2 ECOSYSTEM ANALYSIS

- 8.2.1 MULTIMODAL TRANSPORT OPERATORS (MTOS)

- 8.2.2 INFRASTRUCTURE & TERMINAL OPERATORS

- 8.2.3 TECHNOLOGY PROVIDERS & DIGITAL PLATFORMS

- 8.2.4 REGULATORY BODIES & STANDARDS ORGANIZATIONS

- 8.2.5 END-USE INDUSTRIES

- 8.3 PRICING ANALYSIS

- 8.3.1 AVERAGE SELLING PRICE OF FREIGHT TRANSPORT, BY MODE, 2021-2024

- 8.3.2 AVERAGE SELLING PRICE OF ROAD FREIGHT, BY REGION, 2021-2024

- 8.3.3 AVERAGE SELLING PRICE OF RAIL FREIGHT, BY REGION, 2021-2024

- 8.3.4 AVERAGE SELLING PRICE OF AIR FREIGHT, BY REGION, 2021-2024

- 8.3.5 AVERAGE SELLING PRICE, INLAND WATERWAYS, BY REGION, 2021-2024

- 8.4 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 8.5 INVESTMENT AND FUNDING SCENARIO

- 8.6 FUNDING, BY USE CASE

- 8.7 KEY CONFERENCES AND EVENTS

- 8.8 CASE STUDY ANALYSIS

- 8.8.1 NOKIA ACHIEVED MAJOR EMISSION SAVINGS THROUGH DHL'S MULTIMODAL SOLUTION

- 8.8.2 DSV ENABLED ALLBIRDS TO SCALE UK E-COMMERCE AND RETAIL FULFILMENT WITH TAILORED LOGISTICS SUPPORT

- 8.8.3 C.H. ROBINSON HELPED LEADING US RETAILER ACHIEVE 98 % ON-TIME DELIVERY AND SAVE 12,000 LABOR HOURS THROUGH CONSOLIDATION-LED SUPPLY-CHAIN PROGRAM

- 8.8.4 XPO LOGISTICS IMPLEMENTED RIVER-BASED MULTIMODAL DELIVERY SOLUTION TO SERVE SHOPS IN PARIS

- 8.8.5 UPS BUILT END-TO-END SUPPLY CHAIN AND FREIGHT STRATEGY TO SERVE GLOBAL MARKETS

- 8.9 IMPACT OF US 2025 TARIFFS

- 8.9.1 INTRODUCTION

- 8.9.2 KEY TARIFF RATES

- 8.9.3 PRICE IMPACT ANALYSIS

- 8.9.4 IMPACT ON COUNTRIES/REGIONS

- 8.9.5 IMPACT ON END-USE INDUSTRIES

9 MULTIMODAL TRANSPORT MARKET, BY SERVICE TYPE

- 9.1 INTRODUCTION

- 9.2 FREIGHT FORWARDING

- 9.2.1 DIGITAL TRANSFORMATION AND AI-DRIVEN ORCHESTRATION RESHAPING GLOBAL FREIGHT FORWARDING SERVICE

- 9.3 WAREHOUSING & DISTRIBUTION

- 9.3.1 DIGITAL WAREHOUSING AND INTEGRATED DISTRIBUTION NETWORKS REDEFINING MULTIMODAL LOGISTICS PERFORMANCE

- 9.4 TRANSPORTATION

- 9.4.1 OPTIMIZING END-TO-END FREIGHT MOVEMENT WITH INTEGRATED, DATA-DRIVEN TRANSPORT NETWORKS

- 9.5 VALUE-ADDED SERVICES

- 9.5.1 ELEVATING CUSTOMER EXPERIENCE THROUGH ADVANCED, CUSTOMIZED VALUE-ADDED LOGISTICS SERVICES

- 9.6 CUSTOMS BROKERAGE

- 9.6.1 STREAMLINING GLOBAL TRADE FLOWS WITH INTEGRATED, HIGH-EFFICIENCY CUSTOMS BROKERAGE SOLUTIONS

10 MULTIMODAL TRANSPORT MARKET, BY SOLUTION

- 10.1 INTRODUCTION

- 10.2 SUPPLY CHAIN

- 10.2.1 RISING INVESTMENTS AND DIGITAL INTEGRATION TRANSFORMING MULTIMODAL SUPPLY CHAIN SOLUTIONS GLOBALLY

- 10.3 CARGO

- 10.3.1 GLOBAL INITIATIVES AND DIGITAL ADVANCEMENTS ACCELERATING CARGO SOLUTIONS IN MULTIMODAL TRANSPORT NETWORKS

- 10.4 CARRIAGE MODE

- 10.4.1 ADVANCED CARRIAGE NETWORKS AND STRATEGIC INVESTMENTS ENHANCING EFFICIENCY ACROSS GLOBAL MULTIMODAL TRANSPORT SYSTEMS

- 10.5 COURIER

- 10.5.1 DRIVING HIGH-SPEED FREIGHT MOVEMENT WITH UNIFIED, TECHNOLOGY-ENABLED COURIER SERVICES

- 10.6 TRUCK LOADING

- 10.6.1 BOOSTING MULTIMODAL EFFICIENCY WITH AGILE, DIGITALLY ENABLED TRUCK LOADING OPERATIONS

- 10.7 SHIPPING

- 10.7.1 BOOSTING MULTIMODAL EFFICIENCY WITH AGILE, DIGITALLY ENABLED TRUCK-LOADING OPERATIONS

11 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION

- 11.1 INTRODUCTION

- 11.2 TWO-MODE CONFIGURATION

- 11.2.1 STRENGTHENING GLOBAL LOGISTICS THROUGH EXPANDING DOMINANCE OF TWO-MODE MULTIMODAL CONFIGURATIONS

- 11.3 THREE-MODE CONFIGURATION

- 11.3.1 ENHANCING GLOBAL TRADE CONNECTIVITY THROUGH STRATEGIC INVESTMENTS IN THREE-MODE TRANSPORT INFRASTRUCTURE

- 11.4 HYBRID/OTHER CONFIGURATIONS

- 11.4.1 HIGHER LEVEL OF AUTONOMY AND HIGH-SPEED IN-VEHICLE NETWORKS TO DRIVE MARKET

- 11.5 PRIMARY INSIGHTS

12 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 RETAIL

- 12.2.1 EXPANDING INTERMODAL TERMINALS, UPGRADED INLAND PORTS, AND NEW TRADE CORRIDORS TO DRIVE MARKET

- 12.3 FOOD & BEVERAGES (F&B)

- 12.3.1 EXPANDING AGRICULTURAL AND FOOD COMMODITY TRADE TO DRIVE MARKET

- 12.4 CHEMICALS & MATERIALS

- 12.4.1 GROWTH OF FREIGHT VOLUMES ASSOCIATED WITH BASIC, SPECIALTY, AND HIGH-VALUE CHEMICAL SHIPMENTS TO DRIVE MARKET

- 12.5 PHARMACEUTICALS & HEALTHCARE

- 12.5.1 HIGH PRODUCT VALUE, TIME SENSITIVITY, AND STRINGENT HANDLING REQUIREMENTS TO DRIVE MARKET

- 12.6 MANUFACTURING

- 12.6.1 LARGE-SCALE MOVEMENT OF RAW MATERIALS AND FINISHED GOODS TO DRIVE MARKET

- 12.7 OIL & GAS

- 12.7.1 RISING GLOBAL OIL SUPPLY TO INTENSIFY MULTIMODAL LOGISTICS DEMAND ACROSS COMPLEX ENERGY VALUE CHAINS

- 12.8 OTHER END-USE INDUSTRIES

- 12.9 PRIMARY INSIGHTS

13 MULTIMODAL TRANSPORT MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 MACROECONOMIC OUTLOOK

- 13.2.2 CHINA

- 13.2.2.1 Focus on integrated logistics, trade expansion, and green transportation to drive market

- 13.2.3 JAPAN

- 13.2.3.1 Modal shifts from road to rail and coastal shipping to reduce carbon emissions to drive market

- 13.2.4 INDIA

- 13.2.4.1 Emphasis on integrated logistics ecosystem that connects road, rail, air, and waterways to drive market

- 13.2.5 SOUTH KOREA

- 13.2.5.1 Rise in logistics infrastructure investments to drive market

- 13.2.6 REST OF ASIA PACIFIC

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK

- 13.3.2 FRANCE

- 13.3.2.1 Several targeted financial aid schemes to strengthen first- and last-mile connections to drive market

- 13.3.3 GERMANY

- 13.3.3.1 Goal of increasing rail freight's modal share to 25% by 2030

- 13.3.4 SPAIN

- 13.3.4.1 Investments in intermodal terminals, rail infrastructure upgrades, and acquisition of low-emission locomotives to drive market

- 13.3.5 ITALY

- 13.3.5.1 Investments in port-rail interfaces, multimodal terminal upgrades, and digital freight management systems to drive market

- 13.3.6 POLAND

- 13.3.6.1 Infrastructure modernization to enhance rail, road, and sea connectivity to drive market

- 13.3.7 REST OF EUROPE

- 13.4 NORTH AMERICA

- 13.4.1 MACROECONOMIC OUTLOOK

- 13.4.2 US

- 13.4.2.1 Government programs to promote zero-emission vehicles to drive growth

- 13.4.3 CANADA

- 13.4.3.1 Logistics modernization, digital documentation, and streamlined customs procedures to drive market

- 13.4.4 MEXICO

- 13.4.4.1 Upgrades to key ports, expanded highways, and industrial park developments to drive market

- 13.5 REST OF THE WORLD

- 13.5.1 ARGENTINA

- 13.5.2 BRAZIL

- 13.5.3 SAUDI ARABIA

- 13.5.4 TURKEY

- 13.5.5 OTHERS

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 MARKET SHARE ANALYSIS, 2024

- 14.4 REVENUE ANALYSIS, 2020-2024

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 End-use industry footprint

- 14.7.5.4 Service type footprint

- 14.7.5.5 Solution footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING

- 14.8.5.1 List of startups/SMEs

- 14.8.5.2 Competitive benchmarking of startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 SERVICE LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 DSV

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Service launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 DEUTSCHE POST AG

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 KUEHNE+NAGEL

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 NIPPON EXPRESS HOLDINGS

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Service launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 A.P. MOLLER - MAERSK

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 CMA CGM GROUP

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Expansions

- 15.1.6.3.3 Others

- 15.1.7 MARUBENI CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.8 C.H. ROBINSON WORLDWIDE, INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.9 GEODIS

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.10 XPO, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.11 NYK LINE

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Service launches

- 15.1.11.3.2 Deals

- 15.1.12 EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.13 UNITED PARCEL SERVICE OF AMERICA, INC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.14 HAPAG-LLOYD AG

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Service launches

- 15.1.14.3.2 Deals

- 15.1.15 KLN LOGISTICS GROUP LIMITED

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.1 DSV

- 15.2 OTHER PLAYERS

- 15.2.1 C & S TRANSPORTATION SERVICES, LLC.

- 15.2.2 BDP INTERNATIONAL INC.

- 15.2.3 CROWLEY

- 15.2.4 DACHSER

- 15.2.5 J.B. HUNT TRANSPORT, INC.

- 15.2.6 RHENUS LOGISTICS SE & CO. KG.

- 15.2.7 RYDER SYSTEM, INC.

- 15.2.8 DP WORLD

- 15.2.9 CJ LOGISTICS CORPORATION

- 15.2.10 LOGISTEED, LTD.

16 APPENDIX

- 16.1 KEY INSIGHTS OF INDUSTRY EXPERTS

- 16.2 DISCUSSION GUIDE

- 16.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.4 CUSTOMIZATION OPTIONS

- 16.4.1 MULTIMODAL TRANSPORT MARKET, BY CONTAINER FREIGHT, AT REGIONAL LEVEL

- 16.5 RELATED REPORTS

- 16.6 AUTHOR DETAILS