|

시장보고서

상품코드

1876633

특수 화학제품 재활용 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Specialty Chemicals Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

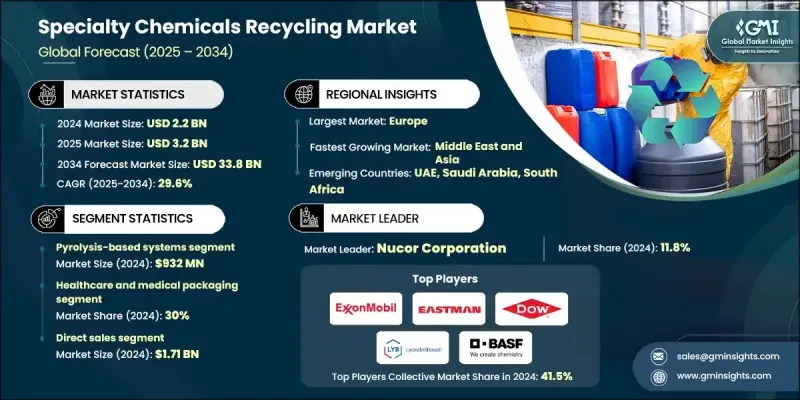

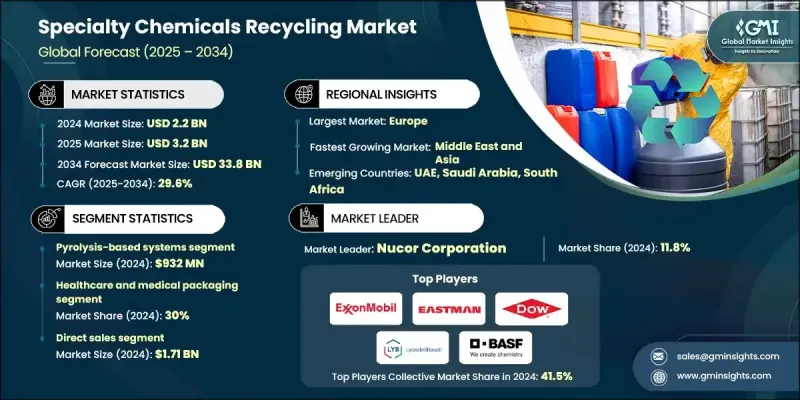

세계의 특수 화학제품 재활용 시장은 2024년에 22억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 29.6%로 성장할 전망이며, 338억 달러에 이를 것으로 예측되고 있습니다.

산업 분야에 있어서 용제, 촉매, 안료, 기타 특수 화학제품별 등 본래라면 폐기물이 되는 귀중한 재료의 회수가 점점 중시됨에 따라 본 시장은 기세를 늘리고 있습니다. 이러한 재료를 재사용 가능한 원료 및 중간 화학제품으로 재활용함으로써 원재료 소비량과 제조 비용을 대폭 절감할 수 있는 동시에 환경 지속가능성 및 순환형 경제의 목표를 추진합니다. 기술 혁신으로 증류, 막분리, 탈중합, 정제 방법 등의 분야에서 재활용 기술이 진화하여 회수 재료의 효율성 및 순도가 향상되고 있습니다. 자동화, 디지털 모니터링, 프로세스 최적화 소프트웨어의 도입으로 일관성 향상, 에너지 사용 절감, 비용 효율성 향상이 더욱 진행되고 있습니다. 이러한 요인으로 인해 의약품, 수처리, 접착제, 페인트, 전자기기 등 다양한 산업에서 특수 화학제품 재활용은 상업적으로 실현 가능하고 환경적으로 책임있는 해결책이 되고 있습니다. 선진국은 엄격한 지속가능성 규제에 의해 주도적인 역할을 하고 있으며, 신흥 시장도 폐기물 감축, 생산 비용 절감, 환경 목표 달성을 위해 이러한 재활용 시스템을 꾸준히 도입하고 있습니다. 폐쇄 루프 생산 시스템으로의 전환은 특수 화학 재활용을 세계 산업 지속가능성을 지원하는 중요한 기반으로 자리 매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 22억 달러 |

| 예측 금액 | 338억 달러 |

| CAGR | 29.6% |

열분해 기반 시스템은 2024년 9억 3,200만 달러의 수익을 창출했습니다. 이러한 시스템은 전통적인 재활용 방법으로 처리할 수 없는 복잡하고 오염된 폐기물 스트림을 처리할 수 있는 능력으로 시장을 선도하고 있습니다. 열분해 기술은 혼합 화학 물질을 재사용 가능한 원료로 변환하여 순환 생산 모델 및 재료 회수 효율을 목표로 하는 산업을 지원합니다. 분해 중합 기술도 이에 이어 고순도 모노머를 회수할 수 있는 이점을 제공합니다. 이것에 의해 신규 원료와 동등한 성능을 가지는 재생 재료의 제조가 가능하게 됩니다. 지속가능한 원료에 대한 관심 증가와 화석 유래 원료에 대한 의존도 감소에 대한 노력은 여러 산업 분야에서 열분해 및 분해 중합 공정의 보급을 촉진하는 주요 요인입니다.

의료 및 의료 포장 분야는 2024년에 30%의 점유율을 차지했습니다. 이 분야의 성장은 의약품, 의료기기, 일회용 제품을 위한 무균성, 내구성, 취급성을 겸비한 포장 솔루션에 대한 수요 증가에 지지되고 있습니다. 고령화 사회의 진전, 의료비 증가, 위생 규제의 강화에 수반해, 의료 에코시스템에 있어서 선진적인 재생 가능 포장 재료의 필요성이 강해지고 있습니다. 자동차 분야에서도 전기자동차와 자율주행차 기술의 발전에 따라 복잡한 전자기기 및 센서 시스템을 위한 혁신적이고 지속 가능한 포장 및 화학제품 솔루션에 대한 수요가 현저하게 높아지고 있습니다.

미국의 특수 화학제품 재활용 시장은 2024년 5억 6,940만 달러 규모에 달했습니다. 북미에서는 건설 및 자동차 부문의 강한 수요로 특수 화학제품 재활용 산업이 계속 확대되고 있습니다. 미국에서는 전기자동차의 급속한 보급과 에너지 절약 건축 기술의 도입으로 철강과 알루미늄과 같은 재생 재료에 대한 수요가 증가하고 있습니다. 캐나다에서는 지속가능성과 순환형 경제에 대한 국가적 노력을 배경으로 산업폐기물 및 폐품으로부터의 금속 및 화학제품 회수 기술이 진전하고 있습니다. 이러한 요인이 함께, 이 지역은 자원 효율적인 제조와 지속 가능한 산업 운영으로의 이행을 추진하고 있습니다.

세계의 특수 화학제품 재활용 시장에서 주요 기업로서 Covestro, Chevron Phillips Chemical, BASF SE, Eastman Chemical, Dow Inc., DSM-Firmenich, Arkema, Evonik Industries, ExxonMobil, LyondellBasell, Jiangsu Eastern Shenghong, Indorama Ventures, PETRONAS Chemical Group, Mitsubishi Chemical 및 SABIC 등을 들 수 있습니다. 특수 화학제품 재활용 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 혁신, 협업, 생산 능력 확대에 주력하고 있습니다. 많은 기업들이 공정 효율과 재료 품질을 향상시키기 위해 열분해, 탈중합, 용매 회수 등 첨단 재활용 기술에 대한 투자를 추진하고 있습니다. 고순도 재생 화학제품의 상업화를 가속시키기 위해, 산업 제조업체 및 연구 기관과의 전략적 제휴나 합작 사업의 형성이 진행되고 있습니다. 또한 재활용 업무 최적화, 비용 절감, 추적성 향상을 도모하기 위해 디지털화 및 자동화의 도입도 진행되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 원재료 비용 상승

- 재활용 공정에서의 기술적 진보

- 최종 사용자 산업에서의 수요 증가

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자액

- 재생 화학제품에 대한 변동하는 시장 수요

- 시장 기회

- 첨단 재활용 기술 개발

- 화학 폐기물 거래를 위한 디지털 플랫폼

- 재생 화학제품을 이용한 제품혁신

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 기술 유형별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 대한 배려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 기술 유형별(2021-2034년)

- 주요 동향

- 열분해 기반 시스템

- 탈중합 기술

- 용해 및 정제

- 가스화 및 열처리

- 신기술 및 하이브리드 기술

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 의료 및 의료용 포장

- 자동차 용도

- 전자기기 및 반도체

- 포장 산업

- 건설 및 건축 자재

- 기타 산업 용도

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 온라인

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Arkema

- BASF SE

- Chevron Phillips Chemical

- Covestro

- DSM-Firmenich

- Dow Inc.

- Eastman Chemical

- Evonik Industrie

- ExxonMobil

- Indorama Ventures

- Jiangsu Eastern Shenghong

- LyondellBasell

- Mitsubishi Chemical

- PETRONAS Chemical Group

- SABIC

The Global Specialty Chemicals Recycling Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 29.6% to reach USD 33.8 billion by 2034.

The market is gaining traction as industries increasingly focus on recovering valuable materials such as solvents, catalysts, pigments, and other specialty chemical by-products that would otherwise become waste. Recycling these materials into reusable feedstocks or intermediate chemicals significantly reduces raw material consumption and manufacturing costs while promoting environmental sustainability and circular economy goals. Technological advancements are transforming the recycling landscape through innovations in distillation, membrane separation, depolymerization, and purification methods, enabling greater efficiency and purity in recovered materials. Automation, digital monitoring, and process optimization software are further improving consistency, reducing energy usage, and enhancing cost-effectiveness. These factors make specialty chemical recycling a more commercially viable and environmentally responsible solution across industries, including pharmaceuticals, water treatment, adhesives, coatings, and electronics. Developed economies are taking the lead with stringent sustainability regulations, while emerging markets are steadily adopting these recycling systems to minimize waste, lower production costs, and meet environmental targets. The shift toward closed-loop production systems is positioning specialty chemical recycling as a key enabler of global industrial sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $33.8 Billion |

| CAGR | 29.6% |

The pyrolysis-based systems generated USD 932 million in 2024. These systems are leading the market due to their capability to process complex and contaminated waste streams that conventional recycling methods cannot manage. Pyrolysis technology converts mixed chemical materials into reusable feedstocks, supporting industries striving for circular production models and material recovery efficiency. Depolymerization technologies closely follow, offering the advantage of recovering high-purity monomers that can be used to manufacture recycled materials with identical performance to their virgin counterparts. The rising focus on sustainable raw materials and the drive to reduce dependency on fossil-based inputs are key factors encouraging the widespread adoption of both pyrolysis and depolymerization processes across multiple industrial sectors.

The healthcare and medical packaging segment held a 30% share in 2024. This segment's growth is fueled by increasing demand for sterile, durable, and easy-to-handle packaging solutions for pharmaceuticals, medical devices, and disposable products. The expanding aging population, along with rising healthcare expenditure and stricter hygiene regulations, has strengthened the need for advanced recyclable packaging materials in the healthcare ecosystem. The automotive sector is also witnessing significant progress due to technological evolution in electric and autonomous vehicles, which require innovative and sustainable packaging and chemical solutions for intricate electronic and sensor systems.

U.S. Specialty Chemicals Recycling Market accounted for USD 569.4 million in 2024. In North America, the specialty chemicals recycling industry continues to expand due to strong demand from the construction and automotive sectors. In the U.S., the rapid adoption of electric vehicles and energy-efficient building practices is increasing the need for recycled materials such as steel and aluminum. Canada is advancing in metal and chemical recovery from both industrial and obsolete waste, driven by its national commitment to sustainability and circular economy practices. Together, these factors are propelling the region's transition toward resource-efficient manufacturing and sustainable industrial operations.

Prominent players active in the Global Specialty Chemicals Recycling Market include Covestro, Chevron Phillips Chemical, BASF SE, Eastman Chemical, Dow Inc., DSM-Firmenich, Arkema, Evonik Industries, ExxonMobil, LyondellBasell, Jiangsu Eastern Shenghong, Indorama Ventures, PETRONAS Chemical Group, Mitsubishi Chemical, and SABIC. Leading companies in the Specialty Chemicals Recycling Market are focusing on innovation, collaboration, and capacity expansion to strengthen their market foothold. Many are investing in advanced recycling technologies such as pyrolysis, depolymerization, and solvent recovery to enhance process efficiency and material quality. Strategic alliances and joint ventures with industrial manufacturers and research organizations are being formed to accelerate the commercialization of high-purity recycled chemicals. Firms are also adopting digitalization and automation to optimize recycling operations, reduce costs, and improve traceability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology type

- 2.2.2 Application

- 2.2.3 Distribution channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising raw material costs

- 3.2.1.2 Technological advancements in recycling processes

- 3.2.1.3 Growing demand from End use industries

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1 High initial investment

- 3.3.2 Fluctuating market demand for recycled chemicals

- 3.4 Market opportunities

- 3.4.1 Development of advanced recycling technologies

- 3.4.2 Digital platforms for chemical waste trading

- 3.4.3 Product innovation using recycled chemicals

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By technology type

- 3.11 Future market trends

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Patent landscape

- 3.14 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.14.1 Major importing countries

- 3.14.2 Major exporting countries

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable practices

- 3.15.2 Waste reduction strategies

- 3.15.3 Energy efficiency in production

- 3.15.4 Eco-friendly initiatives

- 3.16 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pyrolysis-based systems

- 5.3 Depolymerization technologies

- 5.4 Dissolution and purification

- 5.5 Gasification and thermal processing

- 5.6 Emerging and hybrid technologies

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Healthcare and medical packaging

- 6.3 Automotive applications

- 6.4 Electronics and semiconductors

- 6.5 Packaging industries

- 6.6 Construction and building materials

- 6.7 Other industrial applications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Online

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arkema

- 9.2 BASF SE

- 9.3 Chevron Phillips Chemical

- 9.4 Covestro

- 9.5 DSM-Firmenich

- 9.6 Dow Inc.

- 9.7 Eastman Chemical

- 9.8 Evonik Industrie

- 9.9 ExxonMobil

- 9.10 Indorama Ventures

- 9.11 Jiangsu Eastern Shenghong

- 9.12 LyondellBasell

- 9.13 Mitsubishi Chemical

- 9.14 PETRONAS Chemical Group

- 9.15 SABIC