|

시장보고서

상품코드

1892713

배터리 재활용 화학제품 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Battery Recycling Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

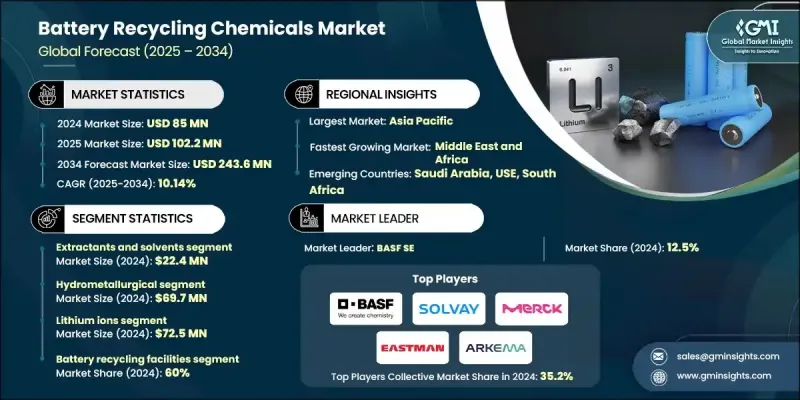

세계의 배터리 재활용 화학제품 시장은 2024년에 8,500만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10.14%로 성장하여 2억 4,360만 달러에 이를 것으로 예측됩니다.

화학적 재활용 촉매는 물리적 처리에 의존하지 않고 분자 수준의 변환을 촉매하여 폐폴리머 및 플라스틱을 원래의 단량체 및 기타 고부가가치 화합물로 전환하는 데 중요한 역할을 합니다. 이러한 촉매는 반응 성능 향상, 선택성 최적화, 지속 가능한 공정 실현을 통해 선진적인 순환 경제 접근 방식을 지원합니다. 폐기물 관리 전략이 품질이 저하된 제품별 생산이 아닌 재료의 품질을 회복할 수 있는 솔루션으로 전환됨에 따라 배터리 재활용 화학물질에 대한 관심이 높아지고 있습니다. 환경 부하 증가, 규제 요건 강화, 플라스틱 및 배터리 산업에서 지속 가능한 재료에 대한 수요 증가로 인해 화학 재활용 기술의 채택이 가속화되고 있습니다. 촉매는 고분자 구조를 분해하는 데 필요한 에너지를 줄이고, 촉매 조성에 따라 열분해, 가수분해, 탈중합 등의 공정을 가능하게 합니다. 이러한 광범위한 변화는 화학적 재활용 기술이 현대의 물질 회수에 필수적인 요소가 되고 있으며, 더 깨끗한 폐쇄 루프 자원 시스템으로의 전환을 지원하는 데 있어 중요한 역할을 하고 있음을 보여줍니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 8,500만 달러 |

| 예측 금액 | 2억 4,360만 달러 |

| CAGR | 10.14% |

습식 야금 공정 분야는 2024년 6,970만 달러의 수익을 창출했습니다. 이 방법은 분리 및 회수를 정밀하게 제어할 수 있기 때문에 폐배터리에서 금속을 추출할 때 널리 사용되고 있으며, 귀중한 원소에 대해 안정적인 결과를 가져옵니다. 반면, 건식 야금법은 고온을 이용하여 배터리 재료의 혼합물을 분해하지만, 수용액 기반 처리에 비해 일반적으로 더 많은 에너지가 필요합니다.

2024년 기준, 배터리 재활용 시설 부문은 60%의 점유율을 차지했습니다. 각국이 자원 효율과 저환경 생산에 우선순위를 두고 있는 가운데, 금속 제련, 화학 처리, 자동차 제조, 전자제품 재활용 등의 분야는 지속적으로 성장하고 있습니다. 전기자동차, 에너지 저장 기술, 전자기기의 사용이 증가함에 따라 사용 후 제품에서 필수 재료를 회수할 필요성이 높아지고 있습니다. 재활용 및 정제 기술은 리튬, 코발트, 니켈과 같은 중요한 자원에 대한 접근성을 유지하면서 전체 환경 부하를 줄이는 데 기여합니다.

미국의 배터리 재활용 화학물질 시장은 2024년 1,810만 달러에 달할 것으로 예측됩니다. 미국과 캐나다를 포함한 북미에서는 첨단 습식 야금 및 화학 솔루션을 통해 중요 금속을 회수하는 기업이 증가하면서 산업이 확대되고 있습니다. 전기 모빌리티와 그리드 저장 시스템의 괄목할 만한 성장으로 확장성과 효율성을 겸비한 처리 기술의 필요성이 대두되고 있으며, 지속 가능한 재활용에 대한 지속적인 규제 지원은 화학적 회수 기술에 대한 투자를 계속 유도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 화학제품 유형별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 동향

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산 및 예측 : 화학제품 유형별, 2021-2034

- 주요 동향

- 침출제

- 환원제 및 산화제

- 추출제 및 용매

- 침전제

- 이온 교환 재료

- 피로메트 첨가제

- 직접 재활용

- 기타

제6장 시장 추산 및 예측 : 프로세스별, 2021-2034

- 주요 동향

- 습식 제련

- 불법 제련

- 직접/물리적 처리

- 생물학적 침출

- 하이브리드 공정

제7장 시장 추산 및 예측 : 배터리 화학별, 2021-2034

- 주요 동향

- 리튬 이온

- 납축전지

- 니켈계

- 알칼리 배터리 및 기타

제8장 시장 추산 및 예측 : 최종 이용 산업별, 2021-2034

- 주요 동향

- 배터리 재활용 시설

- 금속 제련소·제련소

- 화학 처리 플랜트

- 자동차 제조업체

- 전자기기 재활용 업자

- 산업용 배터리 재활용 업자

제9장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 개요

- BASF SE

- Solvay SA

- Merck KGaA

- Eastman Chemical Company

- Arkema SA

- Umicore NV

- Redwood Materials Inc

- Ascend Elements Inc

- Fortum Corporation

- Guangdong Brunp Recycling Technology Co Ltd(GEM)

- Contemporary Amperex Technology Co Limited(CATL)

- Hydrovolt AS

- RecycLiCo Battery Materials Inc

- Cylib GmbH

- Glencore PLC

- Sibanye-Stillwater Limited

- Terrafame Oy

- American Battery Technology Company

- Aqua Metals Inc

- Neometals Ltd

- EnviroLeach Technologies Inc

- Battery Resourcers Inc

The Global Battery Recycling Chemicals Market was valued at USD 85 million in 2024 and is estimated to grow at a CAGR of 10.14% to reach USD 243.6 million by 2034.

Chemical recycling catalysts play a crucial role in converting waste polymers and plastics into their original monomers or other high-value compounds by triggering molecular-level transformations rather than relying on physical processing. These catalysts support advanced circular-economy approaches by improving reaction performance, optimizing selectivity, and enabling more sustainable processing. Interest in battery recycling chemicals is rising as waste-management strategies shift toward solutions that can restore material quality instead of producing downgraded outputs. Increasing environmental pressures, more aggressive regulatory requirements, and stronger demand for sustainable materials within the plastics and battery industries are accelerating adoption. Catalysts help reduce the energy needed to break polymer structures, enabling processes such as pyrolysis, hydrolysis, and depolymerization, depending on catalyst composition. This broader shift underscores how chemical recycling technologies are becoming essential in modern material recovery and in supporting the global transition toward cleaner, closed-loop resource systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $85 Million |

| Forecast Value | $243.6 Million |

| CAGR | 10.14% |

The hydrometallurgical processes segment generated USD 69.7 million in 2024. This approach is widely used to extract metals from spent batteries because it allows precise control over separation and recovery, yielding consistent results for valuable elements. Pyrometallurgical methods rely on high heat to simplify battery material mixtures, although these processes typically require more energy compared with aqueous-based treatments.

The battery recycling facilities segment held a 60% share in 2024. With countries prioritizing resource efficiency and low-impact production, sectors such as metal refining, chemical processing, automotive manufacturing, and electronics recycling continue to grow. Rising usage of electric vehicles, energy storage technologies, and electronic devices is increasing the need to reclaim essential materials from end-of-life products. Recycling and refining methods help maintain access to critical resources such as lithium, cobalt, and nickel while reducing overall environmental burden.

U.S. Battery Recycling Chemicals Market reached USD 18.1 million in 2024. In North America, which includes both the U.S. and Canada, the industry is expanding as companies work to recover key metals through advanced hydrometallurgical and chemical solutions. Strong growth in electric mobility and grid storage systems is driving the need for scalable, efficient treatments, and ongoing regulatory support for sustainable recycling continues to attract investment in chemical recovery technologies.

Major companies involved in the Global Battery Recycling Chemicals Market include BASF SE, Solvay SA, Merck KGaA, Eastman Chemical Company, Arkema SA, Umicore NV, Redwood Materials Inc, Ascend Elements Inc, Fortum Corporation, Guangdong Brunp Recycling Technology Co Ltd (GEM), Contemporary Amperex Technology Co Limited (CATL), Hydrovolt AS, RecycLiCo Battery Materials Inc, Cylib GmbH, Glencore PLC, Sibanye-Stillwater Limited, Terrafame Oy, American Battery Technology Company, Aqua Metals Inc, Neometals Ltd, EnviroLeach Technologies Inc, and Battery Resourcers Inc. Companies competing in the battery recycling chemicals sector are reinforcing their market presence by scaling hydrometallurgical capabilities, improving catalyst formulations, and expanding integrated recycling partnerships with battery manufacturers. Many firms are optimizing process efficiency by reducing reaction temperatures, improving metal-recovery yields, and adopting selective leaching and purification methods that deliver higher-quality outputs. Organizations are also forming regional alliances to secure feedstock, enhance supply-chain resilience, and ensure reliable access to end-of-life batteries. Increased investment in environmentally compliant technologies and low-emission processing systems remains a priority as regulatory expectations rise.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Chemicals type

- 2.2.2 Process type

- 2.2.3 Battery chemistry

- 2.2.4 End use industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in EVs & energy-storage drives supply surge

- 3.2.1.2 Adoption of advanced recovery technologies

- 3.2.1.3 Rising demand from emerging battery chemistries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and operational costs

- 3.2.2.2 Complex and diverse battery chemistries

- 3.2.3 Market opportunities

- 3.2.3.1 Innovation in specialized chemicals

- 3.2.3.2 Integration with circular economy initiatives

- 3.2.3.3 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By chemicals type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Chemicals Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Leaching agents

- 5.3 Reductants/Oxidants

- 5.4 Extractants & solvents

- 5.5 Precipitating agents

- 5.6 Ion-exchange materials

- 5.7 Pyromet additives

- 5.8 Direct recycling

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Process Type, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Hydrometallurgical

- 6.3 Pyrometallurgical

- 6.4 Direct & physical

- 6.5 Bioleaching

- 6.6 Hybrid process

Chapter 7 Market Estimates and Forecast, By Battery Chemistry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Lithium-Ion

- 7.3 Lead-Acid

- 7.4 Nickel-Based

- 7.5 Alkaline & Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Battery recycling facilities

- 8.3 Metal refineries & smelters

- 8.4 Chemical processing plants

- 8.5 Automotive OEMs

- 8.6 Electronics recyclers

- 8.7 Industrial battery recyclers

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Solvay SA

- 10.3 Merck KGaA

- 10.4 Eastman Chemical Company

- 10.5 Arkema SA

- 10.6 Umicore NV

- 10.7 Redwood Materials Inc

- 10.8 Ascend Elements Inc

- 10.9 Fortum Corporation

- 10.10 Guangdong Brunp Recycling Technology Co Ltd (GEM)

- 10.11 Contemporary Amperex Technology Co Limited (CATL)

- 10.12 Hydrovolt AS

- 10.13 RecycLiCo Battery Materials Inc

- 10.14 Cylib GmbH

- 10.15 Glencore PLC

- 10.16 Sibanye-Stillwater Limited

- 10.17 Terrafame Oy

- 10.18 American Battery Technology Company

- 10.19 Aqua Metals Inc

- 10.20 Neometals Ltd

- 10.21 EnviroLeach Technologies Inc

- 10.22 Battery Resourcers Inc