|

시장보고서

상품코드

1876635

유단백질 가수분해물 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Dairy Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

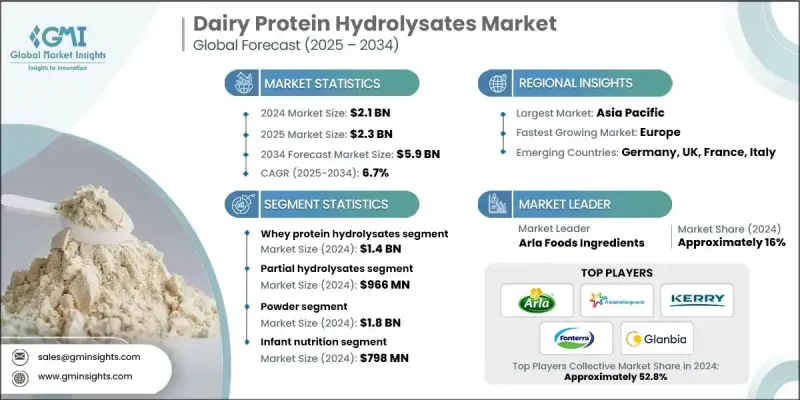

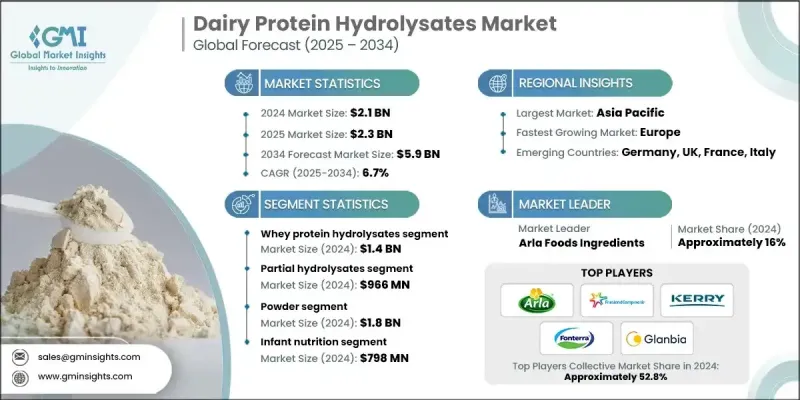

세계의 유단백질 가수분해물 시장은 2024년에 21억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 6.7%로 성장할 전망이며, 59억 달러에 이를 것으로 예측됩니다.

유단백질 가수분해물은 유단백질을 엄격하게 조절하는 효소 가수분해에 의해 생산되는 첨단 생체활성 성분의 일종입니다. 이들 단백질은 완전한 단백질에 비해 소화성 향상, 높은 생체이용률 및 알레르기 유발성의 감소가 인정되어 스포츠 영양, 유아 영양, 의료 영양 등의 영양에 초점을 맞춘 산업에서 귀중한 성분이 되고 있습니다. 가수분해 과정은 큰 단백질 분자가 더 작은 펩티드와 아미노산으로 분해되기 때문에 신체에서 흡수가 빨라지고 효율적으로 이용됩니다. 기능성 영양 및 개별화 영양에 대한 관심이 높아지는 가운데, 제조업체는 특정한 식사나 건강 요구에 대응하기 위해 유단백 가수분해물을 제품에 배합하고 있습니다. 영아 영양 분야는 최대 소비자 부문을 차지하며 세계 수요의 약 38%를 차지합니다. 가수분해에 의해 달성되는 저분자량화 및 소화성의 향상은 특수 영양 제품의 배합에 특히 바람직한 특성입니다. 엄격한 품질 및 안전 기준은 일관된 기능성과 정밀한 가수분해 특성을 갖춘 고품질 유단백질 가수분해물에 대한 수요를 지속적으로 견인하고 있습니다. 첨단 효소 기술은 제조 방법을 변화시키고 제조업체가 펩티드 프로파일과 단백질 구조를 보다 정밀하게 제어할 수 있도록 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 21억 달러 |

| 예측 금액 | 59억 달러 |

| CAGR | 6.7% |

유청 단백질 가수분해물 부문은 2024년에 14억 달러의 수익을 창출하였고, 2025-2034년 연평균 복합 성장률(CAGR) 6.5%로 성장할 전망이며, 2024년에는 68%의 점유율을 차지한 것으로 평가됩니다. 유청 단백질 가수분해물은 완전한 아미노산 조성, 신속한 흡수성, 우수한 용해성으로 계속 시장을 선도하고 있습니다. 뛰어난 영양 특성과 가공의 다양성에 의해 생물학적 이용 능력 및 기능성이 중요한 다양한 제품 배합에 적합합니다. 이러한 장점은 고품질의 단백질 공급원 및 효율적인 영양소 공급이 필요한 용도 분야에서의 이점을 강화합니다.

부분 가수분해물 부문은 2024년에 9억 6,600만 달러 시장 규모를 기록했으며, 2025-2034년 연평균 복합 성장률(CAGR) 6.6%로 성장할 전망입니다. 그 인기는 제어된 효소 가수분해에 의해 실현되는 기능성 효과와 작용 특성의 균형에 기인합니다. 부분 가수분해물은 최적의 펩티드 분포와 단백질 무결성을 유지하면서 쓴맛을 최소화하기 때문에 기능성 식품, 스포츠 영양, 일반 식품 용도에 이상적입니다. 좋은 미각 특성과 우수한 영양 특성이 결합되어 여러 최종 용도 카테고리에서 안정적인 수요를 지원합니다.

북미의 유단백질 가수분해물 시장은 2025-2034년 CAGR 6.5%로 성장할 것으로 예측됩니다. 기능성 및 개인화된 영양에 대한 소비자의 의식 증가는 특히 임상, 스포츠, 유아 영양 분야에서 전문적인 단백질 용도를 중심으로 지역적인 수요를 형성하고 있습니다. 소화기의 건강 및 음식 알레르기에 대한 관심 증가도 고급 단백질 가수분해 기술로의 전환을 가속화하고 있습니다. 이는 제조업체가 기존 단백질 원료를 소화하기 쉽고 저 알레르기성 대체물로 대체하려고 하기 때문입니다.

세계의 유단백질 가수분해물 시장에서 사업을 전개하고 있는 주요 기업으로는 Glanbia Nutritionals, Friesland Campina Ingredients, Arla Foods Ingredients, Fonterra/NZMP, Kerry Group, Lactalis Ingredients, Nestle Health Science, Carbery Group, Agropur Cooperative, Hilmar Ingredients, Milk Specialties Global/Actus Nutrition, Ingredia, Armor Proteines, AMCO Proteins, Costantino & C. spa, Tatua Co-operative, DMK Group/wheyco 및 Saputo Ingredients 등을 들 수 있습니다. 유단백질 가수분해물 시장에서 활동하는 기업들은 경쟁력을 강화하기 위해 혁신, 파트너십, 생산 능력 확대를 중심으로 전략적 노력을 추진하고 있습니다. 많은 기업들이 특정 펩티드 프로파일과 개선된 관능 특성을 가진 맞춤형 가수분해물 배합물을 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다. 식품 및 영양 브랜드와의 전략적 제휴를 통해 보다 광범위한 시장에 접근하고 고급 단백질 원료를 신속하게 상용화할 수 있습니다. 또한 기업은 차세대 효소 기술과 지속 가능한 가공 기술을 통해 생산 효율을 향상시키고 세계적인 품질 및 안전 기준을 충족합니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 과제 및 어려움

- 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 유형별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 대한 배려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 유청 단백질 가수분해물

- 카제인 가수분해물

- 혼합 유단백질 가수분해물

제6장 시장 추계 및 예측 : 가수분해도별(2021-2034년)

- 주요 동향

- 부분 가수분해물(가수분해도 2-15%)

- 고도 가수분해물(가수분해도>15%)

- 고도 가수분해 제품(가수분해도 95% 초과)

제7장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 동향

- 분말 형태

- 페이스트상

- 액체 농축물

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 유아용 영양 식품

- 고도 가수분해 제제(eHF)

- 부분 가수분해 배합 사료(pHF)

- 아미노산 기반 배합 사료(AAF)

- 기타(팔로우 온, 성장기 및 특정 의료용 유아용 식품)

- 스포츠 영양학

- 프리워크아웃 보충제

- 트레이닝 후 및 회복용 보충제

- 단백질 파우더 및 RTD 음료

- 기타(바, 고형 제품, 엘리트 선수용 영양 보조 식품)

- 임상영양학

- 경장 영양(경관 영양)

- 비경구 영양(정맥내 투여)

- 의료용 식품 및 질환 특화형 제제

- 기타(영양 불량, 집중 치료, 상처 회복)

- 동물영양

- 유용소 사료

- 가금 사료

- 수산 사료(생선 및 새우의 영양)

- 기타(돼지, 반려동물 먹이, 특수 동물 영양)

- 바이오테크놀러지 및 세포 배양 배지

- 세포 배양 배지 첨가제(혈청 대체품)

- 바이오프로세스 용도(단백질 및 세포 생산)

- 의약품 제조(백신 및 바이오 의약품)

- 기타(조사, 재생 의료, 분석 시험)

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Arla Foods Ingredients

- FrieslandCampina Ingredients

- Kerry Group

- Fonterra/NZMP

- Glanbia Nutritionals

- Nestle Health Science

- Lactalis Ingredients

- Carbery Group

- Milk Specialties Global/Actus Nutrition

- Agropur Cooperative

- Hilmar Ingredients

- Ingredia

- AMCO Proteins

- Armor Proteines

- Tatua Co-operative

The Global Dairy Protein Hydrolysates Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 5.9 billion by 2034.

Dairy protein hydrolysates represent an advanced class of bioactive ingredients produced through carefully controlled enzymatic hydrolysis of milk proteins. These proteins are recognized for their enhanced digestibility, high bioavailability, and reduced allergenic potential compared to intact proteins, making them valuable components in nutrition-focused industries such as sports, infant, and medical nutrition. Through the hydrolysis process, large protein molecules are broken into smaller peptides and amino acids, allowing for faster absorption and efficient utilization by the body. With increasing interest in functional and personalized nutrition, manufacturers are incorporating dairy protein hydrolysates to meet targeted dietary and health needs. The infant nutrition category represents the largest consumer segment, accounting for nearly 38% of global demand. The lower molecular weight and improved digestibility achieved through hydrolysis make these proteins particularly desirable for formulating specialized nutrition products. Stringent quality and safety standards continue to drive demand for high-grade dairy protein hydrolysates with consistent functional performance and precise hydrolysis characteristics. Advanced enzymatic technologies are transforming production methods, enabling manufacturers to better control peptide profiles and protein structure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 6.7% |

The whey protein hydrolysates segment generated USD 1.4 billion in revenue in 2024 and is forecasted to grow at a CAGR of 6.5% from 2025 to 2034, holding a 68% share in 2024. Whey protein hydrolysates continue to lead the market due to their complete amino acid composition, rapid absorption, and exceptional solubility. Their superior nutritional properties and processing versatility make them suitable for various product formulations where bioavailability and functionality are crucial. These advantages reinforce their dominance in applications that require high-quality protein sources and efficient nutrient delivery.

The partial hydrolysates segment generated USD 966 million in 2024 and is expected to grow at a CAGR of 6.6% during 2025-2034. Their popularity lies in the balance between functional benefits and sensory qualities achieved through controlled enzymatic hydrolysis. Partial hydrolysates exhibit optimal peptide distribution and preserved protein integrity while minimizing bitterness, making them ideal for use in functional foods, sports nutrition, and general dietary applications. Their favorable taste profile and strong nutritional characteristics contribute to consistent demand across multiple end-use categories.

North America Dairy Protein Hydrolysates Market is projected to grow at a CAGR of 6.5% between 2025 and 2034. Growing consumer awareness of functional and personalized nutrition is shaping regional demand, particularly across specialized protein applications in clinical, sports, and infant nutrition. Rising attention to digestive health and food allergies is also accelerating the shift toward advanced protein hydrolysis technologies as manufacturers aim to replace traditional protein ingredients with more digestible, hypoallergenic alternatives.

Key companies operating in the Global Dairy Protein Hydrolysates Market include Glanbia Nutritionals, FrieslandCampina Ingredients, Arla Foods Ingredients, Fonterra/NZMP, Kerry Group, Lactalis Ingredients, Nestle Health Science, Carbery Group, Agropur Cooperative, Hilmar Ingredients, Milk Specialties Global/Actus Nutrition, Ingredia, Armor Proteines, AMCO Proteins, Costantino & C. spa, Tatua Co-operative, DMK Group/wheyco, and Saputo Ingredients. Companies active in the Dairy Protein Hydrolysates Market are pursuing strategic initiatives centered on innovation, partnerships, and capacity expansion to strengthen their competitive standing. Many are investing heavily in research and development to create customized hydrolysate formulations with specific peptide profiles and improved sensory characteristics. Strategic collaborations with food and nutrition brands are enabling broader market access and faster commercialization of advanced protein ingredients. Firms are also enhancing production efficiency through next-generation enzymatic technologies and sustainable processing practices to meet global quality and safety standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Degree of hydrolysis trends

- 2.2.3 Form trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Whey protein hydrolysates

- 5.3 Casein hydrolysates

- 5.4 Mixed milk protein hydrolysates

Chapter 6 Market Estimates and Forecast, By Degree of Hydrolysis, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Partial hydrolysates (DH 2-15%)

- 6.3 Extensive hydrolysates (DH >15%)

- 6.4 Highly hydrolyzed products (DH >95%)

Chapter 7 Market Estimates and Forecast, By Form, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Powder form

- 7.3 Paste form

- 7.4 Liquid concentrates

Chapter 8 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Infant nutrition

- 8.2.1 Extensively hydrolyzed formulas (eHF)

- 8.2.2 Partially hydrolyzed formulas (pHF)

- 8.2.3 Amino acid-based formulas (AAF)

- 8.2.4 Others (follow-on, growing-up, and special medical purpose infant foods)

- 8.3 Sports nutrition

- 8.3.1 Pre-workout supplements

- 8.3.2 Post-workout & recovery supplements

- 8.3.3 Protein powders & RTD beverages

- 8.3.4 Others (bars, solid form products, and elite athlete nutrition)

- 8.4 Clinical nutrition

- 8.4.1 Enteral nutrition (tube feeding)

- 8.4.2 Parenteral nutrition (IV administration)

- 8.4.3 Medical foods & disease-specific formulations

- 8.4.4 Others (malnutrition, critical care, and wound recovery)

- 8.5 Animal nutrition

- 8.5.1 Dairy cattle feed

- 8.5.2 Poultry feed

- 8.5.3 Aquafeed (fish & shrimp nutrition)

- 8.5.4 Others (swine, pet food, and specialty animal nutrition)

- 8.6 Biotechnology & cell culture media

- 8.6.1 Cell culture media supplements (serum replacements)

- 8.6.2 Bioprocessing applications (protein & cell production)

- 8.6.3 Pharmaceutical manufacturing (vaccines & biologics)

- 8.6.4 Others (research, regenerative medicine, and analytical testing)

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arla Foods Ingredients

- 10.2 FrieslandCampina Ingredients

- 10.3 Kerry Group

- 10.4 Fonterra/NZMP

- 10.5 Glanbia Nutritionals

- 10.6 Nestle Health Science

- 10.7 Lactalis Ingredients

- 10.8 Carbery Group

- 10.9 Milk Specialties Global/Actus Nutrition

- 10.10 Agropur Cooperative

- 10.11 Hilmar Ingredients

- 10.12 Ingredia

- 10.13 AMCO Proteins

- 10.14 Armor Proteines

- 10.15 Tatua Co-operative