|

시장보고서

상품코드

1885826

유기 단백질 가수분해물 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Organic Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

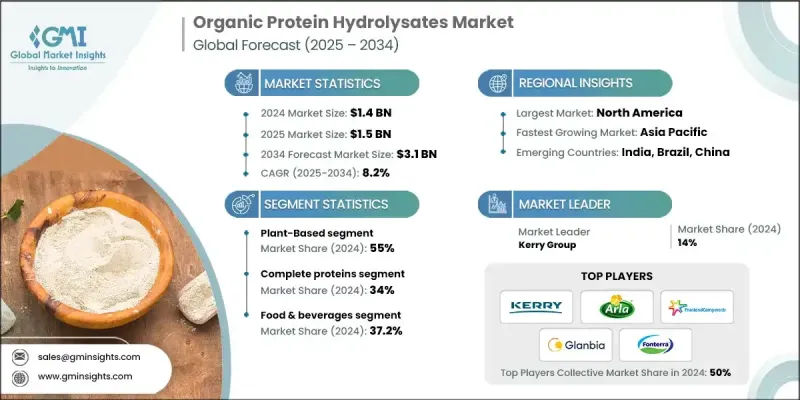

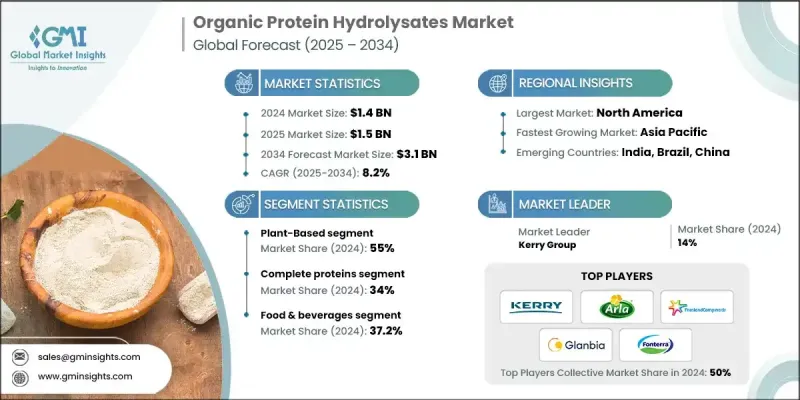

세계의 유기 단백질 가수분해물 시장은 2024년에 14억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.2%로 성장할 전망이며, 31억 달러에 이를 것으로 예측됩니다.

유기 영양, 고단백 식품의 동향, 개별화 영양 수요가 맞물려 수요가 가속화되고 있으며, 여러 소비자 및 산업 부문에서 유기 단백질 가수분해물에 대한 수요가 높아지고 있습니다. 그 생물활성 특성, 저알레르겐성, 흡수율의 향상은 제품 개발을 추진하고 프리미엄 가격 설정을 지지하고 있습니다. 세계 시장이 보다 농축되고 전문적인 단백질 형태로 이행하는 가운데, 기능성 식품 및 가공 식품에 있어서 채용 확대가 전망됩니다. 건강 지향의 고조, 유기 바이오 베이스 원료의 사용 증가, 스포츠, 의료 및 라이프 스타일 영양 분야의 성장이 가수분해물의 매력을 강화하고 있습니다. 유기 농업에 대한 규제면의 지원 및 효소 처리 기술의 진보가 맞물려 생산 능력이 확대되고 있습니다. 또, 보다 온화하고 소화하기 쉬운 단백질원의 필요성으로부터, 유아, 소아 및 의료용 영양 분야에서의 침투도 진행되고 있습니다. 이러한 요인들이 결합되어 세계의 유기 단백질 가수분해물의 장기적인 성장세를 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 14억 달러 |

| 예측 금액 | 31억 달러 |

| CAGR | 8.2% |

식물 유래 원료 부문은 2024년에 55%의 점유율을 차지하였고, 2034년까지 연평균 복합 성장률(CAGR) 8%로 성장이 예상됩니다. 제조업체가 새로운 식물성 및 해양 원료를 원료 포트폴리오에 추가하고 맞춤형 아미노산 조성 및 기능 특성을 실현함에 따라 이 카테고리는 계속 성장하고 있습니다. 지속가능성에 대한 관심, 비유전자 재조합(비GMO) 포지셔닝, 책임 있는 조달에 중점을 둔 소비자의 선호도는 북미와 유럽 시장에서 특히 강한 추세를 보이고 있습니다.

완전 단백질 분절은 2024년에 34%의 점유율을 차지하였고, 2034년까지 연평균 복합 성장률(CAGR) 8.6%로 성장할 것으로 예측됩니다. 완전한 아미노산 프로파일과 고급 기능 특성에 대한 수요는 단백질 유형의 차별화를 형성합니다. 우유 유래 단백질은 임상영양 및 퍼포먼스 영양 분야에서 여전히 주류이며, 콜라겐계 원료는 가동성 및 미용 지향 부문으로 높은 수요를 유지하고 있습니다. 시장은 특정 건강 효과를 표적으로 하는 펩티드 제제 및 지적 재산권에 근거한 제품 주장으로 점차 이행하고 있습니다.

북미의 유기 단백질 가수분해물 시장은 2024년 4억 2,800만 달러를 창출했으며, 2034년까지 9억 5,200만 달러에 이를 전망입니다. 이 지역은 성숙한 유기 영양 문화, 스포츠 및 반려동물 제품 분야에서 높은 채용률, 고품질의 깨끗한 라벨 단백질에 지불하려는 소비자 기반의 혜택을 누리고 있습니다. 건강 및 영양 분야에서의 신속한 혁신으로 알려진 미국에서는 특히 고도의 퍼포먼스 분야나 임상 용도에 있어서, 다양한 제품 카테고리에 걸쳐 유기 단백질 가수분해물의 상업화가 계속 확대되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 클린 라벨 및 유기 단백질에 대한 수요 증가

- 스포츠, 유아 및 임상 영양 분야의 성장

- 효소 처리 기술의 진보

- 업계의 잠재적 위험 및 과제

- 기존의 단백질원에 비해 높은 생산비용

- 원료의 가용성 및 인증의 제한

- 시장 기회

- 유기 바이오 자극제 및 어그리뉴트리션 분야로의 확대

- 식물 유래 및 알레르겐 프리의 배합 동향

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 소스별

- 향후 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 소스별(2021-2034년)

- 주요 동향

- 식물 유래

- 콩

- 밀

- 완두콩

- 쌀

- 옥수수

- 지방종자(예 : 해바라기, 유채)

- 기타 식물성 원료

- 동물 유래

- 우유(카제인, 유청)

- 계란

- 육류 및 가금류

- 생선 및 해양

- 콜라겐 및 젤라틴

- 기타 원료

제6장 시장 추계 및 예측 : 단백질 유형별(2021-2034년)

- 주요 동향

- 완전 단백질(필수 아미노산을 모두 포함)

- 불완전한 단백질

- 콜라겐 및 젤라틴 단백질

- 카제인 및 유청 단백질

- 특수 및 기능성 단백질(생물활성 펩티드, 특주 블렌드)

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 음식

- 기능성 식품

- 스포츠 영양 및 퍼포먼스 제품

- 유아용 및 임상 영양

- 제빵 및 과자류

- 유제품 및 유제품 대체품

- 고기 대체품 및 고기 제품

- 음료(RTD, 분말음료, 스무디)

- 스낵 편의점

- 동물 영양

- 반려동물 사료(개, 고양이, 기타)

- 수산 사료(생선, 새우, 기타)

- 가축 사료(가금류, 돼지, 반추 동물)

- 특수 사료 및 기능성 사료

- 농업 및 작물 영양

- 생물 자극제 및 식물 성장 촉진제

- 엽면 살포제

- 토양 개량제

- 종자 처리제

- 화장품 및 퍼스널케어

- 스킨 케어

- 헤어 케어

- 뉴트리코스메틱스 및 내면의 아름다움

- 의약품 및 영양제

- 영양보조식품

- 의료 및 임상 영양

- 약물 전달 기술 및 특수 제제

- 공업용 및 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Arla Foods Ingredients

- Kerry Group

- FrieslandCampina Ingredients

- Glanbia Nutritionals

- Hilmar Ingredients

- Fonterra Co-operative Group

- Lactalis Ingredients

- A. Costantino & CSpA

- Essentia Protein Solutions

- VITAMINAS, SA(Bioiberica Group)

- Armor Proteines

- AMCO Proteins

- Tate &Lyle

- ADM(Archer Daniels Midland)

- Cargill

- Ingredion Incorporated

- Roquette Freres

- Symrise

- Gelita AG

- Weishardt Group

The Global Organic Protein Hydrolysates Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 3.1 billion by 2034.

Demand is accelerating as organic nutrition, high-protein dietary trends, and personalized nutrition converge, increasing the need for hydrolyzed organic proteins across multiple consumer and industrial segments. Their bioactive characteristics, reduced allergenic potential, and improved absorption rates continue to drive product development and support premium pricing. Broader adoption within functional and processed foods is expected as the global market shifts toward more concentrated and specialized protein formats. Rising interest in wellness, increased use of organic bio-based inputs, and growth in sports, medical, and lifestyle nutrition have strengthened the appeal of hydrolysates. Regulatory backing for organic agriculture, combined with advancements in enzymatic processing, is expanding production capabilities. Penetration is also rising in infant, pediatric, and medical nutrition due to the need for gentler and easier-to-digest protein sources. These factors collectively reinforce long-term momentum for organic protein hydrolysates worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 8.2% |

The plant-based sources segment held a 55% share in 2024 and will grow at an 8% CAGR through 2034. The category continues to grow as manufacturers broaden their raw material portfolios across new botanical and marine sources to achieve customized amino acid compositions and functional characteristics. Sustainability concerns, non-GMO positioning, and consumer preference for responsible sourcing remain particularly strong across North American and European markets.

The complete proteins segment held a 34% share in 2024 and is expected to grow at an 8.6% CAGR through 2034. Demand for full amino acid profiles and advanced functional attributes is shaping protein-type differentiation. Dairy-derived proteins remain dominant in clinical and performance nutrition, while collagen-based ingredients maintain strong traction in mobility and beauty-focused segments. The market is gradually shifting toward more specialized peptide formulations aimed at targeted health positioning and intellectual property-based product claims.

North America Organic Protein Hydrolysates Market generated USD 428 million in 2024 to reach USD 952 million by 2034. The region benefits from a mature organic nutrition culture, strong adoption in sports and pet products, and a consumer base willing to pay for high-quality, clean-label proteins. The United States, known for rapid innovation in health and nutrition, continues to expand the commercialization of organic protein hydrolysates across diverse product categories, especially in advanced performance and clinical applications.

Key companies active in the Organic Protein Hydrolysates Market include Arla Foods Ingredients, Kerry Group, FrieslandCampina Ingredients, Glanbia Nutritionals, Hilmar Ingredients, Fonterra Co-operative Group, Lactalis Ingredients, A. Costantino & C. S.p.A., Essentia Protein Solutions, VITAMINAS, S.A. (Bioiberica Group), Armor Proteines, AMCO Proteins, Tate & Lyle, ADM (Archer Daniels Midland), Cargill, Ingredion Incorporated, Roquette Freres, Symrise, Gelita AG, and Weishardt Group. Companies in the Global Organic Protein Hydrolysates Market are strengthening their competitive positioning through targeted innovation, strategic portfolio expansion, and improved processing capabilities. Many are investing in advanced enzymatic technologies to create differentiated peptide profiles tailored for specific health and performance needs. Firms are also expanding raw material sourcing to include a broader mix of plant and animal proteins to serve diverse applications and regulatory preferences. Strategic collaborations with formulators and nutrition brands help accelerate go-to-market pathways and support specialized product development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Protein Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for clean-label, organic proteins

- 3.2.1.2 Growth in sports, infant, clinical nutrition

- 3.2.1.3 Advances in enzymatic processing technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs versus conventional proteins

- 3.2.2.2 Limited raw material availability and certification

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into organic biostimulants and agrinutrition

- 3.2.3.2 Plant-based and allergen-free formulation trends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Source

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-Based

- 5.2.1 Soy

- 5.2.2 Wheat

- 5.2.3 Pea

- 5.2.4 Rice

- 5.2.5 Corn

- 5.2.6 Oilseeds (e.g., sunflower, rapeseed)

- 5.2.7 Other plant sources

- 5.3 Animal-Based

- 5.3.1 Milk (casein, whey)

- 5.3.2 Egg

- 5.3.3 Meat & Poultry

- 5.3.4 Fish & Marine

- 5.3.5 Collagen & Gelatin

- 5.4 Other sources

Chapter 6 Market Estimates and Forecast, By Protein Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Complete Proteins (all essential amino acids)

- 6.3 Incomplete Proteins

- 6.4 Collagen & Gelatin Proteins

- 6.5 Casein & Whey Proteins

- 6.6 Specialty / Functional Proteins (bioactive peptides, tailored blends)

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & Beverages

- 7.2.1 Functional Foods

- 7.2.2 Sports Nutrition & Performance Products

- 7.2.3 Infant & Clinical Nutrition

- 7.2.4 Bakery & Confectionery

- 7.2.5 Dairy & Dairy Alternatives

- 7.2.6 Meat Analogs & Meat Products

- 7.2.7 Beverages (RTD, powdered drinks, smoothies)

- 7.2.8 Snacks & Convenience Foods

- 7.3 Animal Nutrition

- 7.3.1 Pet Food (dogs, cats, others)

- 7.3.2 Aquafeed (fish, shrimp, others)

- 7.3.3 Livestock Feed (poultry, swine, ruminants)

- 7.3.4 Specialty & Performance Feeds

- 7.4 Agriculture & Crop Nutrition

- 7.4.1 Biostimulants & Plant Growth Promoters

- 7.4.2 Foliar Sprays

- 7.4.3 Soil Amendments

- 7.4.4 Seed Treatments

- 7.5 Cosmetics & Personal Care

- 7.5.1 Skin Care

- 7.5.2 Hair Care

- 7.5.3 Nutricosmetics / Beauty-from-within

- 7.6 Pharmaceuticals & Nutraceuticals

- 7.6.1 Dietary Supplements

- 7.6.2 Medical & Clinical Nutrition

- 7.6.3 Drug Delivery & Specialty Formulations

- 7.7 Industrial & Other Applications

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arla Foods Ingredients

- 9.2 Kerry Group

- 9.3 FrieslandCampina Ingredients

- 9.4 Glanbia Nutritionals

- 9.5 Hilmar Ingredients

- 9.6 Fonterra Co-operative Group

- 9.7 Lactalis Ingredients

- 9.8 A. Costantino & C. S.p.A.

- 9.9 Essentia Protein Solutions

- 9.10 VITAMINAS, S.A. (Bioiberica Group)

- 9.11 Armor Proteines

- 9.12 AMCO Proteins

- 9.13 Tate & Lyle

- 9.14 ADM (Archer Daniels Midland)

- 9.15 Cargill

- 9.16 Ingredion Incorporated

- 9.17 Roquette Freres

- 9.18 Symrise

- 9.19 Gelita AG

- 9.20 Weishardt Group