|

시장보고서

상품코드

1892669

유청 단백질 가수분해물 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Whey Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

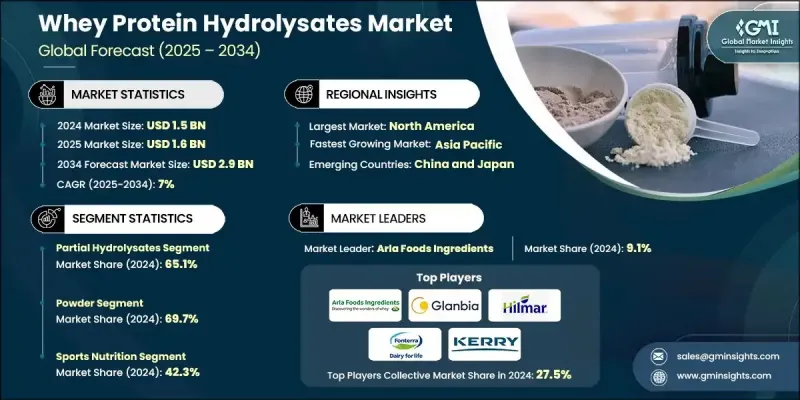

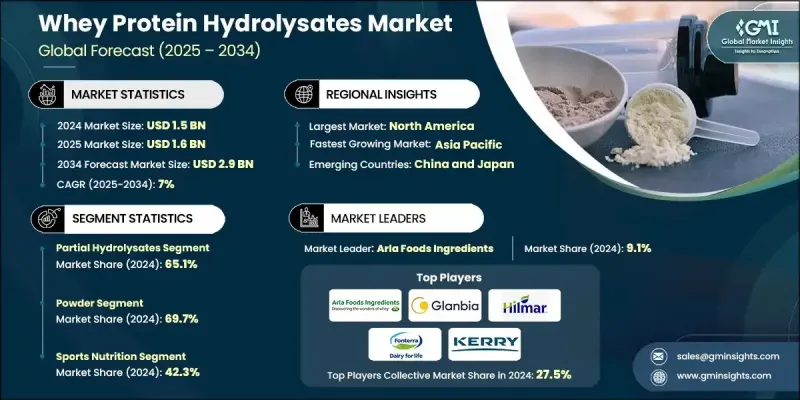

세계의 유청 단백질 가수분해물 시장은 2024년에 15억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 7%로 성장하여 29억 달러에 이를 것으로 예측됩니다.

소비자들이 빠른 흡수성, 높은 소화율, 저알레르기성 단백질 원료를 찾는 경향이 강해지면서 수요는 계속 확대되고 있습니다. 유청단백질 가수분해물은 유청단백질 농축물 또는 분리물을 효소에 의한 가수분해 처리하여 제조되며, 단백질을 작은 펩타이드와 유리 아미노산으로 분해하여 보다 우수한 생리학적 효과를 가져옵니다. 유아용 조제분유, 스포츠 영양식품, 의료용 영양식품, 기능성 식품 분야에서 채택이 가속화되고 있습니다. 많은 성인 인구에 영향을 미치는 유당 불내증에 대한 전 세계적인 인식이 높아지면서 가수분해 유단백질로의 전환이 더욱 가속화되고 있습니다. 이 단백질 원료 산업 분야는 특수 가공 시스템과 엄격한 품질 기준에 의존하여 제조업체가 특정 성능 요구 사항에 맞게 설계된 매우 균일한 펩타이드 구성과 분자량 프로파일을 달성할 수 있도록 합니다. 가수분해 수준은 용해도, 내열성, 유화 특성, 전반적인 생체 이용률 등 의도한 특성에 따라 보통 경미한 수준에서 높은 수준까지 다양하게 설정됩니다. 가공 기술의 발전과 고성능 영양 성분에 대한 소비자의 관심 증가는 시장의 진화를 계속 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 15억 달러 |

| 예측 금액 | 29억 달러 |

| CAGR | 7% |

부분 가수분해물 부문은 2024년 65.1%의 점유율을 차지했으며, 2034년까지 연평균 6.9%의 성장률을 보일 것으로 전망됩니다. 이 원료들은 균형 잡힌 구조를 유지하여 소화율을 높이고 알레르기 반응을 감소시키면서 음료 및 식품 배합에 광범위하게 사용될 수 있는 바람직한 기능적 특성을 유지합니다. 고도 가수분해 제품에 비해 쓴맛이 적기 때문에 배합의 유연성을 높이고 추가 향료 솔루션의 필요성을 줄입니다.

스포츠 영양 분야는 2024년 42.3%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 7.3%를 보일 것으로 예측됩니다. 가수분해 유청단백질은 빠른 흡수 속도, 근육 단백질 합성에 대한 강한 영향, 운동 후 회복에 대한 역할로 인해 이 분야에서 널리 선호되고 있습니다. 소비자의 단백질 품질에 대한 높은 인식과 소매 및 EC 채널에서 확립된 판매 경로가 이 분야의 지속적인 성장에 기여하고 있습니다.

북미 가수분해 유청 단백질 시장은 2024년 36.9%의 점유율을 차지했습니다. 이는 발달한 영양 산업, 강력한 가공 능력, 고품질 단백질 원료의 높은 채택률에 의해 뒷받침됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 형태별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산 및 예측 : 가수분해도별, 2021-2034

- 주요 동향

- 부분 가수분해

- 첨단 가수분해

제6장 시장 추산 및 예측 : 형태별, 2021-2034

- 주요 동향

- 분말

- 액체

제7장 시장 추산 및 예측 : 용도별, 2021-2034

- 주요 동향

- 유아 영양

- 스포츠 영양

- 담백질 분말

- RTD 쉐이크

- 임상 영양

- 기능성 식품 및 음료

- 고단백 음료

- 베이커리 및 제과

- 유제품

- 혼합 분말

- 동물 영양

- 축산

- 반려동물 사료

제8장 시장 추산 및 예측 : 유통 채널별, 2021-2034

- 주요 동향

- 소매 채널

- 슈퍼마켓 및 하이퍼마켓

- 전문 코셔 식품점

- 편의점

- 온라인 및 전자상거래

- 소비자용 직접 판매

- 브랜드 공식 사이트 판매

- 정기 구입 서비스

- 전자상거래 플랫폼

- 외식산업용 유통 채널

제9장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 개요

- Arla Foods Ingredients

- Glanbia Nutritionals

- Hilmar Ingredients

- Fonterra Co-operative Group

- Kerry Group

- FrieslandCampina Ingredients

- Nestle Health Science

- Carbery Group

- Agropur Ingredients

- Lactalis Ingredients

- Saputo Dairy Ingredients

- Ingredia

The Global Whey Protein Hydrolysates Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 2.9 billion by 2034.

Demand continues to expand as consumers shift toward protein ingredients that offer rapid absorption, high digestibility, and reduced allergenic potential. Whey protein hydrolysates are produced through controlled enzymatic hydrolysis of whey protein concentrate or isolate, breaking down the proteins into smaller peptides and free amino acids that deliver improved physiological benefits. Their adoption has accelerated across infant formulas, sports nutrition, medical nutrition, and functional food applications. Growing global awareness of lactose intolerance, which affects a large portion of the adult population, further supports the shift toward hydrolyzed dairy proteins. This segment of the protein ingredients industry relies on specialized processing systems and strict quality criteria, as manufacturers design highly consistent peptide compositions and molecular weight profiles tailored to specific performance needs. Hydrolysis levels typically range from mild to extensive, depending on intended characteristics such as solubility, heat tolerance, emulsification behavior, and overall bioavailability. Advancements in processing methods and rising consumer interest in high-performance nutritional ingredients continue to shape the evolution of the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 7% |

The partial hydrolysates segment held 65.1% share in 2024 and is projected to grow at a CAGR of 6.9% through 2034. These ingredients maintain a balanced structure, offering improved digestibility and reduced allergenicity while preserving desirable functional traits that support widespread use in food and beverage formulations. Their lower bitterness compared to extensively hydrolyzed products increases formulation flexibility and reduces the need for added flavor solutions.

The sports nutrition segment accounted for a 42.3% share in 2024 and is anticipated to grow at a CAGR of 7.3% through 2034. Hydrolyzed whey proteins are widely preferred in this category due to their faster uptake rate, strong impact on muscle protein synthesis, and role in post-exercise recovery. High consumer recognition of protein quality and established sales channels across retail and e-commerce contribute to sustained segment momentum.

North America Whey Protein Hydrolysates Market held a 36.9% share in 2024, supported by a well-developed nutrition industry, strong processing capabilities, and high adoption of premium protein ingredients.

Major companies active in the Whey Protein Hydrolysates Market include Arla Foods Ingredients, Glanbia Nutritionals, Kerry Group, Hilmar Ingredients, Saputo Dairy Ingredients, Fonterra Co-operative Group, FrieslandCampina Ingredients, Nestle Health Science, Agropur Ingredients, Ingredia, Lactalis Ingredients, and Carbery Group. Companies competing in the Whey Protein Hydrolysates Market are prioritizing advanced enzymatic technologies to create differentiated peptide profiles with enhanced functional and nutritional performance. Many manufacturers are scaling production capacity and upgrading process controls to maintain consistent hydrolysis levels and meet rising demand from sports, infant, and clinical nutrition sectors. Strategic product diversification, including formulations with improved sensory characteristics, supports broader commercial adoption. Firms are also strengthening long-term partnerships with food, beverage, and supplement brands to secure stable supply channels.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 Degree of hydrolysis

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing sports nutrition market & protein supplementation

- 3.2.1.2 Increasing clinical nutrition demand

- 3.2.1.3 Consumer preference for clean label & functional ingredients

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & price sensitivity

- 3.2.2.2 Bitterness & sensory challenges limiting consumer acceptance

- 3.2.3 Market opportunities

- 3.2.3.1 Bioactive peptide-enriched hydrolysates for cardiovascular health

- 3.2.3.2 MFGM-enriched hydrolysates for cognitive & muscle health

- 3.2.3.3 Hybrid dairy-plant protein hydrolysate blends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By form

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Degree of Hydrolysis, 2021-2034 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Partial hydrolysates

- 5.3 Highly hydrolyzed

Chapter 6 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 Infant nutrition

- 7.3 Sports nutrition

- 7.3.1 Protein Powders

- 7.3.2 Ready to drink shakes

- 7.4 Clinical nutrition

- 7.5 Functional foods & beverages

- 7.5.1 High-Protein Beverages

- 7.5.2 Bakery & Confectionery

- 7.5.3 Dairy Products

- 7.5.4 Ready-to-Mix Powders

- 7.6 Animal nutrition

- 7.6.1 Livestock

- 7.6.2 Pet food

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 Retail channels

- 8.2.1 Supermarkets and hypermarkets

- 8.2.2 Specialty kosher stores

- 8.2.3 Convenience stores

- 8.3 Online and E-commerce

- 8.3.1 Direct-to-consumer sales

- 8.3.2 Brand website sales

- 8.3.3 Subscription services

- 8.3.4 E-commerce platforms

- 8.4 Foodservice channels

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arla Foods Ingredients

- 10.2 Glanbia Nutritionals

- 10.3 Hilmar Ingredients

- 10.4 Fonterra Co-operative Group

- 10.5 Kerry Group

- 10.6 FrieslandCampina Ingredients

- 10.7 Nestle Health Science

- 10.8 Carbery Group

- 10.9 Agropur Ingredients

- 10.10 Lactalis Ingredients

- 10.11 Saputo Dairy Ingredients

- 10.12 Ingredia