|

시장보고서

상품코드

1885851

식품 폐기물 유래 단백질 가수분해물 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Food Waste-Derived Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

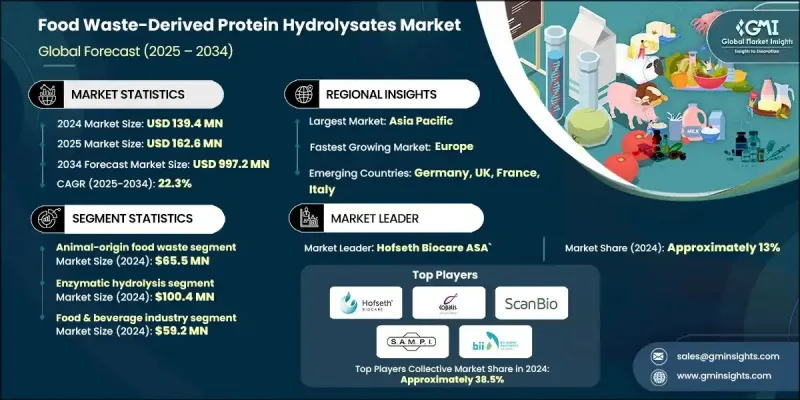

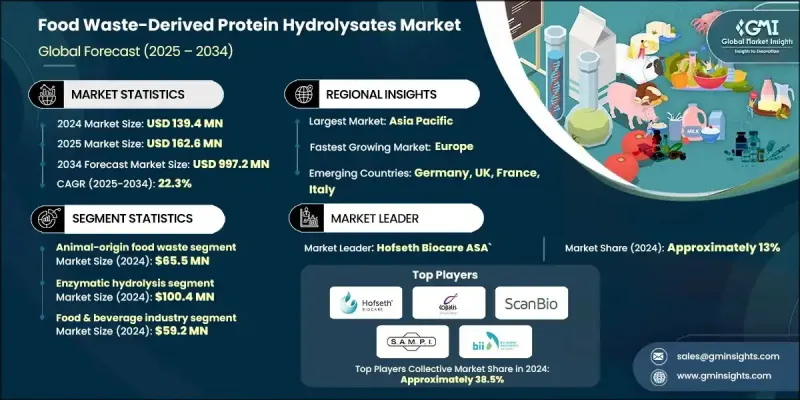

세계의 식품 폐기물 유래 단백질 가수분해물 시장은 2024년 1억 3,940만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 22.3%로 성장할 전망이며, 9억 9,720만 달러에 달할 것으로 예측되고 있습니다.

폐기된 식물성 및 동물성 식품 원료를 효소적, 화학적 가수분해에 의해 생성되는 이들 단백질은 순환형 바이오 이코노미로의 이행에 중심적인 역할을 합니다. 이 과정은 원래 폐기되는 자원을 기능성 단백질 및 생물학적 활성 펩티드로 전환시켜 기존 단백질 소스와 동등 이상의 성능을 발휘합니다. 지속가능성에 대한 기대감이 높아짐에 따라 제조업체는 엄격한 폐기물 감소 정책과 환경 기준을 준수하기 때문에 폐기물 유래 원료 채택을 확대하고 있습니다. 식품 손실 감소 및 영양 순환 실현을 위한 세계적인 노력은 가수분해물의 기능성 식품, 영양 보조 식품, 지속 가능한 동물 영양 솔루션에 대한 통합을 추진하고 있습니다. 세계 각국의 규제 당국은 기존의 폐기 방법에 비해 환경 부하가 낮기 때문에 식품 폐기물의 업사이클링을 촉진하는 정책을 계속 추진하고 있습니다. 식품 폐기물의 유효 활용은 온실가스 배출량을 대폭 삭감하고 유기 폐기물의 대부분이 매립지에 도달하는 것을 막기 위해 환경면 및 경제면 모두에서 매력적인 선택지가 되고 있습니다. 이러한 규제, 환경, 산업 주도의 요인이 함께 식품 폐기물 유래 가수분해물 원료에 대한 수요는 여러 분야에서 계속 가속하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 1억 3,940만 달러 |

| 예측 금액 | 9억 9,720만 달러 |

| CAGR | 22.3% |

동물성 식품 폐기물은 2024년에 6,550만 달러 시장 규모를 창출해 2025-2034년 연평균 복합 성장률(CAGR) 22.1%로 성장할 것으로 예측됩니다. 이 카테고리가 주도적인 지위에 있는 이유는 단백질 함량이 영양가가 높고 생물활성 펩타이드의 강력한 잠재성을 가지고 있기 때문입니다. 다양한 동물성 잔류물의 고품질 아미노산 프로파일, 높은 생물학적 가치, 우수한 기능적 특성으로 인해, 이러한 가수분해물은 강력한 생물학적 활성이 필요한 영양 보충제, 특수 사료 배합, 기능성 식품 용도에 이상적입니다.

효소 가수분해 부문은 2024년에 1억 40만 달러에 이르렀고, 2025-2034년 연평균 복합 성장률(CAGR) 22.4%로 성장하여, 시장의 72%를 차지할 것으로 예측됩니다. 이 기술이 주류를 유지하는 이유는 펩티드 구조의 정밀한 개발을 가능하게 하고 민감한 생물학적 활성 성분을 유지할 수 있기 때문입니다. 프로테아제 효소를 제어하고 사용함으로써 제조자는 분자량 분포를 조정하고 일관된 기능성 원료를 만들 수 있습니다. 이 때문에 효소 가수분해는 고품질의 식품, 뉴트라슈티컬, 기능성 원료의 생산에 있어서 선호되는 수법이 되고 있습니다.

북미의 식품 폐기물 유래 단백질 가수분해물 시장은 2025-2034년 연평균 복합 성장률(CAGR) 20.7%로 성장할 것으로 예측됩니다. 지속가능한 공급망에 중점을 두고 순환형 바이오 이코노미 전략에 대한 기업의 관심 증가는 지역 채용을 강화하고 있습니다. 식품 폐기물 감소와 기존 단백질 공급원을 환경 친화적인 대체품으로 대체하는 것에 대한 관심 확대는 기업에 첨단 추출 및 가치화 기술에 대한 투자를 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 과제 및 어려움

- 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 원료 유형별 동향

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 동향

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 원료 유형별(2021-2034년)

- 주요 동향

- 동물성 식품 폐기물

- 식물성 식품 폐기물

- 혼합 식품 폐기물

제6장 시장 추계 및 예측 : 가수분해 기술별(2021-2034년)

- 주요 동향

- 효소 가수분해

- 화학 가수분해

- 복합 처리 기술

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 식음료 업계

- 기능성 식품

- 제빵 및 과자류

- 음료 및 강화 음료

- 기타

- 사료 산업

- 가금 사료

- 수산 양식용 사료

- 축산 사료(소, 돼지)

- 기타

- 영양보조식품 산업

- 단백질 보충제

- 아미노산 보충제

- 스포츠 및 퍼포먼스 영양

- 영양보조식품

- 기타

- 농업 산업

- 바이오 비료

- 생물자극제

- 토양 개량제

- 기타

- 기타 최종 이용 산업

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Hofseth Biocare ASA

- Copalis Sea Solutions

- Scanbio Marine Group

- SAMPI

- Bio-Marine Ingredients Ireland

- Diana Aqua(Symrise)

- Triplenine Group

- Janatha Fish Meal &Oil Products

- Agropur

- FrieslandCampina Ingredients

- Ingredia

- Arla Foods Ingredients

The Global Food Waste-Derived Protein Hydrolysates Market was valued at USD 139.4 million in 2024 and is estimated to grow at a CAGR of 22.3% to reach USD 997.2 million by 2034.

These proteins, generated through enzymatic and chemical hydrolysis of discarded plant and animal food materials, play a central role in the transition toward a circular bioeconomy. The process transforms otherwise wasted resources into functional proteins and bioactive peptides that deliver performance equal to or better than traditional protein sources. As sustainability expectations intensify, manufacturers are increasingly adopting waste-derived ingredients to align with strict waste reduction policies and environmental standards. Global commitments to reduce food loss and close nutrient loops are supporting the integration of hydrolysates into functional foods, dietary supplements, and sustainable animal nutrition solutions. Regulatory authorities worldwide continue to enforce policies encouraging the upcycling of food waste due to its lower ecological footprint compared to conventional disposal. Valorization of food waste significantly cuts greenhouse gas emissions and prevents a major share of organic waste from reaching landfills, making it an environmentally and economically appealing pathway. These combined regulatory, environmental, and industry-driven factors continue to accelerate demand for food waste-derived hydrolysate ingredients across multiple sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $139.4 Million |

| Forecast Value | $997.2 Million |

| CAGR | 22.3% |

The animal-origin food waste generated USD 65.5 million in 2024 and is expected to grow at a 22.1% CAGR from 2025 to 2034. This category leads because its protein content is highly nutritious and offers strong potential for bioactive peptides. High-quality amino acid profiles, elevated biological value, and excellent functional characteristics from various animal-based residues make these hydrolysates well-suited for nutritional supplements, specialized feed formulations, and functional food applications requiring robust bioactivity.

The enzymatic hydrolysis segment reached USD 100.4 million in 2024 and is anticipated to grow at a 22.4% CAGR from 2025 to 2034, accounting for 72% of the market. This method remains dominant because it enables the precise development of peptide structures and preserves sensitive bioactive components. Controlled use of proteolytic enzymes allows manufacturers to tailor molecular weight distribution and create consistent functional ingredients, making enzymatic hydrolysis the preferred approach for high-grade food, nutraceutical, and functional ingredient production.

North America Food Waste-Derived Protein Hydrolysates Market is projected to grow at a 20.7% CAGR from 2025 to 2034. Rising emphasis on sustainable supply chains and increasing corporate attention to circular bioeconomy strategies are strengthening regional adoption. Expanding interest in reducing food waste and replacing conventional protein sources with environmentally responsible alternatives is pushing companies to invest in advanced extraction and valorization technologies.

Major companies in the Global Food Waste-Derived Protein Hydrolysates Market include Scanbio Marine Group, Copalis Sea Solutions, Hofseth Biocare ASA, Bio-Marine Ingredients Ireland, Diana Aqua (Symrise), Triplenine Group, Agropur, SAMPI, FrieslandCampina Ingredients, Ingredia, Arla Foods Ingredients, and Janatha Fish Meal & Oil Products. Leading companies are strengthening their presence by expanding production capacity, improving extraction technologies, and enhancing supply chain integration. Many manufacturers are investing in advanced enzymatic processing systems to increase peptide purity, improve yield efficiency, and maintain consistent quality. Strategic partnerships with food processors and aquaculture firms help secure long-term access to raw materials, reducing waste and stabilizing sourcing. Firms are also focusing on product diversification to serve nutraceutical, food, and animal nutrition markets with tailored hydrolysate formulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Source material type trends

- 2.2.2 Hydrolysis technology trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By source material type trends

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source Material Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Animal-origin food waste

- 5.3 Plant-origin food waste

- 5.4 Mixed food waste streams

Chapter 6 Market Estimates and Forecast, By Hydrolysis Technology, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Enzymatic hydrolysis

- 6.3 Chemical hydrolysis

- 6.4 Combined processing technologies

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage industry

- 7.2.1 Functional foods

- 7.2.2 Bakery & confectionery

- 7.2.3 Beverages & fortified drinks

- 7.2.4 Other

- 7.3 Animal feed industry

- 7.3.1 Poultry feed

- 7.3.2 Aquaculture feed

- 7.3.3 Livestock feed (cattle, swine)

- 7.3.4 Others

- 7.4 Nutraceutical industry

- 7.4.1 Protein supplements

- 7.4.2 Amino acid supplements

- 7.4.3 Sports & performance nutrition

- 7.4.4 Dietary supplements

- 7.4.5 Others

- 7.5 Agricultural industry

- 7.5.1 Biofertilizers

- 7.5.2 Biostimulants

- 7.5.3 Soil conditioners

- 7.5.4 Others

- 7.6 Other end use industries

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Hofseth Biocare ASA

- 9.2 Copalis Sea Solutions

- 9.3 Scanbio Marine Group

- 9.4 SAMPI

- 9.5 Bio-Marine Ingredients Ireland

- 9.6 Diana Aqua (Symrise)

- 9.7 Triplenine Group

- 9.8 Janatha Fish Meal & Oil Products

- 9.9 Agropur

- 9.10 FrieslandCampina Ingredients

- 9.11 Ingredia

- 9.12 Arla Foods Ingredients