|

시장보고서

상품코드

1892694

자율주행차 플릿 운영 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Autonomous Vehicle Fleet Operations Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

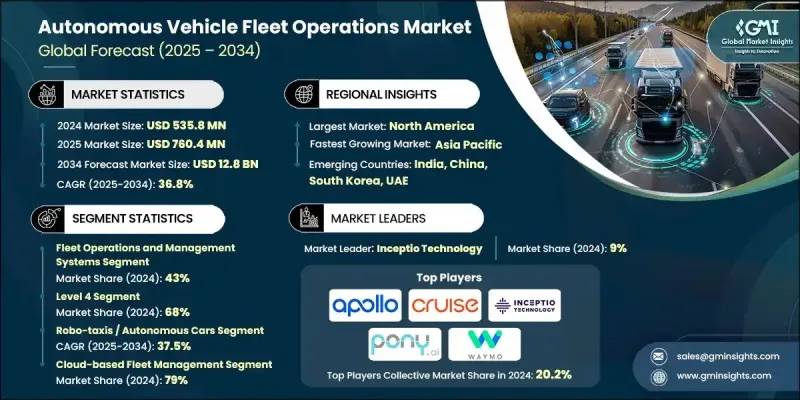

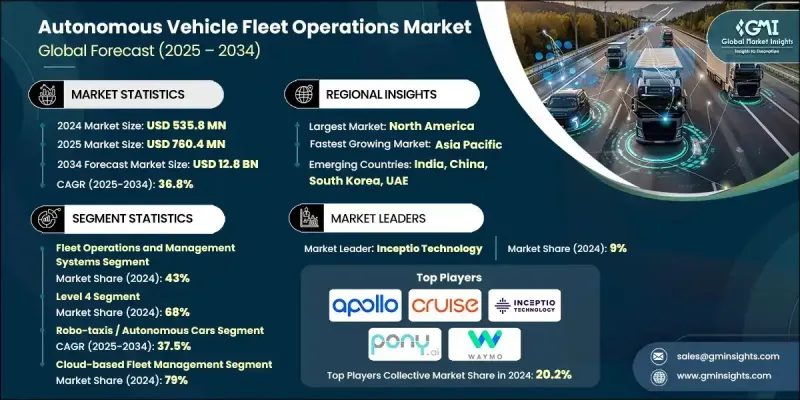

세계의 자율주행차 플릿 운영 시장은 2024년 5억 3,580만 달러에 달했고 2034년 CAGR 36.8%를 나타내 128억 달러에 이를 것으로 전망됩니다.

이 시장은 여객 운송, 배송 서비스, 로보택시 사업에서 기업이 자율주행차의 도입과 규모 확대를 진행함에 따라 급속히 확대되고 있습니다. 레벨 4 및 레벨 5 자율주행 시스템의 진보 외에도 AI 구동형 클라우드 기반 차량 관리 플랫폼과 고속 5G 연결이 결합되어 플릿 운영을 변화시키고 있습니다. 미국에서의 규제면의 지원은 상용 전개를 위한 명확한 틀을 제공하고, 차량 운영사가 안전성을 확보하면서 서비스를 확대하는 자신감을 주고 있습니다. 이러한 변화로 인해 업계는 파일럿 프로그램에서 광범위한 상업 운영으로 전환하여 수익을 창출하고 매일 수천 명의 사용자에게 서비스를 제공합니다. 경제적 이익, 운용효율, 기술 혁신이 도입을 추진하는 한편, 도시모빌리티, 화물물류, 소비자의 기대가 시장정세를 재구축하고 있으며, 자율주행 플릿운용을 현대교통의 기반으로 자리잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 5억 3,580만 달러 |

| 예측 금액 | 128억 달러 |

| CAGR | 36.8% |

플릿 운영·관리 시스템 분야는 2024년에 43%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 37.1%를 나타낼 것으로 예측됩니다. 이 시스템은 중앙 집중식 모니터링, 예측 유지보수, 경로 최적화, 실시간 분석을 위한 소프트웨어를 통합합니다. AI 알고리즘과 사이버 보안 프로토콜은 효율성을 향상시키고 플릿 데이터를 보호합니다. 물류, 화물 운송, 여객 운송 분야에서의 도입 확대가 성장을 견인하고 있으며, 각 회사는 자동 스케줄링, 텔레매틱스 통합, 분석 기능에 의한 플랫폼의 고도화를 통해 운영 비용 절감과 플릿 생산성 향상을 도모하고 있습니다.

레벨 4 부문은 2024년에 68%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 37.2%를 나타낼 것으로 예측됩니다. 레벨 4 시스템은 정의된 운영 설계 영역 내에서 완전한 자율성을 실현하고 지정된 지역, 도로 유형 및 환경 조건에서 인간의 개입 없이 차량을 운행할 수 있습니다. 레벨 4 기술의 상업적 보급은 규제 당국의 승인, 경제적 실현 가능성, 운용 효율을 반영하고 있으며 다양한 지리적·기상 조건 하에서도 안전성을 유지하면서 노동 비용을 삭감할 수 있는 점이 평가되고 있습니다.

북미의 자율주행차 플릿 운영 시장은 2024년 47%의 점유율을 차지했습니다. 이 지역은 많은 벤처 캐피탈, 기업 투자 및 연구 개발 비용으로 세계 시장을 선도하고 있습니다. 주요 자율주행 기업에 대한 투자는 플릿의 확대와 상업화를 가속화하고 있습니다. 정부기관, 주교통국, 업계 컨소시엄 간의 연계를 통해, 지역의 능력 강화, 안전 프로토콜의 확립, 원격 조작 기준, 인프라 정비가 진행되어 시장의 성장을 더욱 추진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률 분석

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 레벨 4 자율 주행 모빌리티 및 배송 차량의 도입 확대

- 비용 효율이 뛰어난 무인 운전 수송 업무에 대한 수요 증가

- AI, 엣지 컴퓨팅, 텔레매틱스, 5G 접속성의 진전

- 로보택시, 자율주행 셔틀, 라스트마일 배송 서비스 확대

- 실시간으로의 플릿 감시, 안전성, 예측 보전에 대한 요구 증가

- 업계의 잠재적 위험 및 과제

- 인프라, 하드웨어 및 백엔드 기술의 고비용

- 접속형 및 원격 관리형 플릿에 있어서 사이버 시큐리티 리스크

- 시장 기회

- 도시 모빌리티에서의 로보 택시 및 자율 주행 셔틀의 대규모 도입

- 라스트 마일 배송 및 물류 업무의 자동화

- 광업, 항만, 공항, 창고에 있어서 산업용 플릿 자동화

- 세계 감시를 위한 원격 플릿 운영 센터 개발

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 세계적인 규제 환경의 개요

- 유엔 유럽 경제위원회(UNECE) 규제 및 국제적인 조화

- 미국에 있어서 연방 정부와 주 정부의 관할 권한

- EU 형식 승인 프레임워크 및 실시

- 아시아태평양의 규제 단편화에 관한 분석

- 지역별 시험·파일럿 프로그램 요건

- 안전인증 및 검증기준

- 데이터 프라이버시 및 사이버 보안 규제

- 책임과 보험 틀의 진화

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 현황

- 현재 기술 동향

- 센서 기술의 진화(LiDAR, 레이더, 카메라 시스템)

- 자율주행을 위한 AI와 머신러닝

- 고정밀 매핑 및 위치 지정 기술

- V2X 통신 규격과 도입 상황

- 신흥 기술

- 원격조작·텔레오퍼레이션 기술

- 엣지 컴퓨팅 및 차재 처리

- 플릿 보호를 위한 사이버 보안 기술

- OTA 소프트웨어 업데이트 기능

- 현재 기술 동향

- 가격 분석과 비용 구조

- 차종별 차량 취득 비용

- 개조 차량과 전용 설계 차량의 경제성 비교

- 플릿 관리 기술 비용

- 원격 운용 센터의 인력 배치 및 인프라 비용

- 보수·운영 경비 분석

- 보험 및 배상 책임 비용의 동향

- 총소유비용(TCO) 비교

- 플릿 서비스용 가격 설정 모델

- 특허 분석

- 기술 분야별 특허 출원 동향

- 주요 특허 보유자 및 혁신 리더

- 플릿 관리 기술 특허

- 원격조작·배차시스템의 특허

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경 배려형 이니셔티브

- 탄소발자국에 관한 고려 사항

- 고객의 채용 상황과 사용자 체험 분석

- 상용 로보택시 도입 지표

- 대중교통기관의 채용 의향

- 사용자 체험의 질과 만족도 요인

- 운영 신뢰성 및 서비스 중단 분석

- 내게 필요한 옵션과 종합적인 설계로 사용자 경험

- 상업화물·물류 분야에 있어서 유저 채용 상황

- 광업에 있어서 도입 상황과 운용상의 수용도

- 경제적 영향과 산업변혁

- 인건비 절감 가능성

- 자본 투자와 인프라 요건

- 플릿 가동률과 운용 효율의 경제성

- 업계 재편과 시장 구조의 재구성

- 공공 부문 투자와 경제개발

- 보험·배상 책임 시장의 변혁

- 리스크 평가와 시장 환경의 역풍

- 안전 인시던트 및 규제 당국에 의한 집행 조치

- 규제의 단편화와 컴플라이언스의 복잡성

- 기술적 제약과 운영 설계 영역의 제약

- 사이버 보안 위협 및 데이터 프라이버시 위험

- 자본 집약도와 수익화의 불확실성

- 공공의 수용과 신뢰의 장벽

- 노동력 대체와 노동조합의 반대

- 사업자간의 주요 실적 평가 지표(KPI)의 비교 분석

- 플릿 규모와 전개 지표

- 운용 효율과 가동률 지표

- 신뢰성 및 서비스 중단 지표

- 안전성능지표

- 경제적 성과 지표

- 기술 성숙도 지표

- 규제 준수·인가 지표

- 고객 채용률과 시장 침투율 지표

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 사업 확대 계획과 자금 조달

- 벤처캐피탈 및 프라이빗 주식 투자 동향

- 정부 보조금 프로그램 및 공적 자금

- 자율주행차 기술에 대한 OEM 투자

- 합병·인수 활동 분석

- 자금 조달상의 과제와 자본 요건

제5장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 플릿 운영 및 관리 시스템

- 안전, 규정 준수 및 모니터링 시스템

- 연결성 및 통신 시스템

- 내비게이션 및 차량 소프트웨어 시스템

제6장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 로보택시/자율주행차

- 자율주행 셔틀

- 자율주행 트럭

- 자율주행 배송 밴

- 배송 로봇/인도 로봇

- 자율주행 산업용 차량

제7장 시장 추계·예측 : 자율주행 수준별(2021-2034년)

- 주요 동향

- 레벨 3

- 레벨 4

- 레벨 5

제8장 시장 추계·예측 : 배포 모드별(2021-2034년)

- 주요 동향

- 클라우드 기반 플릿 관리

- On-Premise 솔루션

제9장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 여객 모빌리티 사업자

- 화물 및 물류 사업자

- 산업 및 비도로 사업자

- 상업 및 공공시설 분야

- 기타

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 포르투갈

- 크로아티아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

제11장 기업 프로파일

- 세계 기업

- Aurora Innovation

- AutoX

- Baidu Apollo

- Cruise

- General Motors

- Inceptio Technology

- Mobileye

- Plus.ai

- Pony.ai

- Scania

- Torc Robotics

- Waymo

- Zoox

- 지역 기업

- ComfortDelGro

- Pinellas Suncoast Transit Authority

- Valley Metro(Phoenix)

- WeRide

- 신흥 기업

- Forterra

- Kodiak Robotics

- LILEE Systems

- Motional

- Perrone Robotics

The Global Autonomous Vehicle Fleet Operations Market was valued at USD 535.8 million in 2024 and is estimated to grow at a CAGR of 36.8% to reach USD 12.8 billion by 2034.

The market is rapidly expanding as companies adopt and scale self-driving vehicles across passenger mobility, delivery services, and robo-taxi operations. Advances in Level 4 and Level 5 autonomous systems, coupled with AI-driven, cloud-based fleet management platforms and high-speed 5G connectivity, are transforming fleet operations. Regulatory support in the U.S. provides clear frameworks for commercial deployments, giving fleet operators confidence to scale services while ensuring safety. This shift is moving the industry from pilot programs to widespread commercial operations, creating substantial revenue and serving thousands daily. Economic benefits, operational efficiency, and technological innovation are driving adoption, while urban mobility, freight logistics, and consumer expectations continue to reshape the market landscape, positioning autonomous fleet operations as a cornerstone of modern transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $535.8 Million |

| Forecast Value | $12.8 Billion |

| CAGR | 36.8% |

The fleet operations and management systems segment held a 43% share in 2024 and is expected to grow at a CAGR of 37.1% through 2034. These systems integrate software for centralized monitoring, predictive maintenance, route optimization, and real-time analytics. AI algorithms and cybersecurity protocols enhance efficiency and protect fleet data. Growth is driven by adoption in logistics, freight, and passenger transport, with companies refining platforms through automated scheduling, telematics integration, and analytics to reduce operational costs and increase fleet productivity.

The Level 4 segment held a 68% share in 2024 and is projected to grow at a CAGR of 37.2% through 2034. Level 4 systems deliver full autonomy within defined operational design domains, allowing vehicles to operate without human intervention in specified areas, road types, or environmental conditions. Widespread commercial adoption of Level 4 technology reflects regulatory approvals, economic viability, and operational efficiency, as fleets can reduce labor costs while maintaining safety across varied geographic and weather conditions.

North America Autonomous Vehicle Fleet Operations Market accounted for a 47% share in 2024. The region leads the global market due to significant venture capital, corporate investment, and R&D expenditure. Investments in major AV companies have accelerated fleet expansion and commercialization. Collaboration between government agencies, state transportation departments, and industry consortia is strengthening regional capabilities, establishing safety protocols, teleoperation standards, and infrastructure upgrades, further boosting market growth.

Key players in the Global Autonomous Vehicle Fleet Operations Market include Aurora Innovation, AutoX, Baidu Apollo, Cruise, Inceptio Technology, Mobileye, Plus.ai, Pony.ai, Torc Robotics, and Waymo. Companies in the Autonomous Vehicle Fleet Operations Market are strengthening their presence through heavy investment in R&D to improve autonomy, AI algorithms, and fleet safety systems. Strategic partnerships with governments, regulators, and infrastructure providers help secure regulatory approvals and facilitate large-scale deployment. Firms are expanding pilot programs into commercial operations while integrating cloud-based fleet management platforms for real-time monitoring, predictive maintenance, and route optimization. Investment in high-speed connectivity, including 5G and edge computing, enhances vehicle communication and operational efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Vehicle

- 2.2.4 Autonomy Level

- 2.2.5 Deployment Mode

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising deployment of Level 4 autonomous mobility and delivery fleets

- 3.2.1.2 Growing demand for cost-efficient and driverless transportation operations

- 3.2.1.3 Advancements in AI, edge computing, telematics, and 5G connectivity

- 3.2.1.4 Expansion of robo-taxi, autonomous shuttle, and last-mile delivery services

- 3.2.1.5 Increasing need for real-time fleet monitoring, safety, and predictive maintenance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure, hardware, and backend technology costs

- 3.2.2.2 Cybersecurity risks in connected and remotely managed fleets

- 3.2.3 Market opportunities

- 3.2.3.1 Large-scale deployment of robo-taxis and autonomous shuttles in urban mobility

- 3.2.3.2 Automation of last-mile delivery and logistics operations

- 3.2.3.3 Industrial fleet automation in mining, ports, airports, and warehouses

- 3.2.3.4 Development of remote fleet operations centers for global supervision

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global regulatory landscape overview

- 3.4.2 UNECE regulations & international harmonization

- 3.4.3 Federal vs state jurisdiction in the United States

- 3.4.4 EU type-approval framework & implementation

- 3.4.5 Asia-Pacific regulatory fragmentation analysis

- 3.4.6 Testing & pilot program requirements by region

- 3.4.7 Safety certification & validation standards

- 3.4.8 Data privacy & cybersecurity regulations

- 3.4.9 Liability & insurance framework evolution

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Sensor technology evolution (LiDAR, radar, camera systems)

- 3.7.1.2 AI & machine learning for autonomous driving

- 3.7.1.3 HD mapping & localization technologies

- 3.7.1.4 V2X communication standards & deployment

- 3.7.2 Emerging technologies

- 3.7.2.1 Remote operations & teleoperation technologies

- 3.7.2.2 Edge computing & onboard processing

- 3.7.2.3 Cybersecurity technologies for fleet protection

- 3.7.2.4 OTA software update capabilities

- 3.7.1 Current technological trends

- 3.8 Pricing analysis & cost structure

- 3.8.1 Vehicle acquisition costs by type

- 3.8.2 Retrofitting vs purpose-built vehicle economics

- 3.8.3 Fleet management technology costs

- 3.8.4 Remote operations center staffing & infrastructure costs

- 3.8.5 Maintenance & operating expense analysis

- 3.8.6 Insurance & liability cost trends

- 3.8.7 Total cost of ownership (TCO) comparison

- 3.8.8 Pricing models for fleet services

- 3.9 Patent analysis

- 3.9.1 Patent filing trends by technology area

- 3.9.2 Key patent holders & innovation leaders

- 3.9.3 Fleet management technology patents

- 3.9.4 Remote operations & dispatch system patents

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.11 Carbon footprint considerations

- 3.12 Customer adoption & user experience analysis

- 3.12.1 Commercial robotaxi adoption metrics

- 3.12.2 Public transit agency adoption intentions

- 3.12.3 User experience quality & satisfaction factors

- 3.12.4 Operational reliability & service disruption analysis

- 3.12.5 Accessibility & inclusive design user experience

- 3.12.6 Commercial freight & logistics user adoption

- 3.12.7 Mining industry adoption & operational acceptance

- 3.13 Economic impact & industry transformation

- 3.13.1 Labor cost reduction potential

- 3.13.2 Capital investment & infrastructure requirements

- 3.13.3 Fleet utilization & operational efficiency economics

- 3.13.4 Industry consolidation & market restructuring

- 3.13.5 Public sector investment & economic development

- 3.13.6 Insurance & liability market transformation

- 3.14 Risk assessment & market headwinds

- 3.14.1 Safety incidents & regulatory enforcement actions

- 3.14.2 Regulatory fragmentation & compliance complexity

- 3.14.3 Technology limitations & operational design domain constraints

- 3.14.4 Cybersecurity threats & data privacy risks

- 3.14.5 Capital intensity & path to profitability uncertainty

- 3.14.6 Public acceptance & trust barriers

- 3.14.7 Workforce displacement & labor opposition

- 3.15 Comparative analysis of key performance indicators (KPIs) across operators

- 3.15.1 Fleet scale & deployment metrics

- 3.15.2 Operational efficiency & utilization metrics

- 3.15.3 Reliability & service disruption metrics

- 3.15.4 Safety performance metrics

- 3.15.5 Economic performance metrics

- 3.15.6 Technology maturity metrics

- 3.15.7 Regulatory compliance & approval metrics

- 3.15.8 Customer adoption & market penetration metrics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

- 4.6.4.1 Venture capital & private equity investment trends

- 4.6.4.2 Government grant programs & public funding

- 4.6.4.3 OEM investment in AV fleet technologies

- 4.6.4.4 Merger & acquisition activity analysis

- 4.6.4.5 Funding challenges & capital requirements

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Fleet operations and management systems

- 5.3 Safety, compliance and monitoring systems

- 5.4 Connectivity and communication systems

- 5.5 Navigation and vehicle software systems

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Robo-taxis / autonomous cars

- 6.3 Autonomous shuttles

- 6.4 Autonomous trucks

- 6.5 Autonomous delivery vans

- 6.6 Delivery robots / sidewalk robots

- 6.7 Autonomous industrial vehicles

Chapter 7 Market Estimates & Forecast, By Autonomy Level, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Level 3

- 7.3 Level 4

- 7.4 Level 5

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Cloud-based fleet management

- 8.3 On-premises solutions

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Passenger mobility operators

- 9.3 Freight and logistics operators

- 9.4 Industrial and off-highway operators

- 9.5 Commercial and institutional sectors

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aurora Innovation

- 11.1.2 AutoX

- 11.1.3 Baidu Apollo

- 11.1.4 Cruise

- 11.1.5 General Motors

- 11.1.6 Inceptio Technology

- 11.1.7 Mobileye

- 11.1.8 Plus.ai

- 11.1.9 Pony.ai

- 11.1.10 Scania

- 11.1.11 Torc Robotics

- 11.1.12 Waymo

- 11.1.13 Zoox

- 11.2 Regional Players

- 11.2.1 ComfortDelGro

- 11.2.2 Pinellas Suncoast Transit Authority

- 11.2.3 Valley Metro (Phoenix)

- 11.2.4 WeRide

- 11.3 Emerging Technology Innovators

- 11.3.1 Forterra

- 11.3.2 Kodiak Robotics

- 11.3.3 LILEE Systems

- 11.3.4 Motional

- 11.3.5 Perrone Robotics