|

시장보고서

상품코드

1892755

중고차 금융 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Used Car Financing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

세계의 중고차 금융 시장은 2025년에 479억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.6%로 성장하여 741억 달러에 이를 것으로 예측됩니다.

가처분 소득 증가가 자동차 수요를 촉진하는 반면, 높은 신차 가격은 구매자의 구매를 망설이게 하는 요인으로 작용하고 있습니다. 중고차 판매가 현실적인 대안으로 떠오르면서 소비자들이 보다 저렴한 가격대의 차량을 이용할 수 있게 되었습니다. 할부(EMI)를 포함한 금융 솔루션이 이 격차를 메우고 있으며, 자동차 소유를 보다 실현 가능하고 편리하게 만들고 있습니다. 업계 단체에 따르면, 대출기관은 다양한 대출 기간에 대응하기 위해 융통성 있는 금리를 제공하고 있으며, 현재 평균 금리는 12-36개월 4.79%, 37-60개월 5.29%라고 합니다. 아시아태평양은 시장의 약 절반을 차지하고 있으며, 중국의 대규모 시장 규모와 인도의 급속한 자동차 보급, 조직화된 소매 네트워크의 성장이 이를 주도하고 있습니다. 북미와 유럽은 성숙한 시장이지만, 디지털 금융 플랫폼, 혁신적인 보험 솔루션, 전기자동차 전문 금융을 통해 지속적으로 기회를 제공하면서 세계 시장의 꾸준한 확장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 479억 달러 |

| 예측 금액 | 741억 달러 |

| CAGR | 4.6% |

은행 부문은 2024년 52.3%의 점유율을 차지했습니다. 저비용 예금 조달 능력, 광범위한 지점망과 온라인 네트워크, 그리고 저위험 대출에 대한 전문성에서 우위를 점하고 있습니다. 대출자는 보통 36-72개월의 기간 동안 80-90%의 담보가치 대비 대출금 비율(LTV)을 확보합니다. 담보대출은 대출자의 리스크를 줄이면서 대출자에게 유리한 금리와 긴 상환기간을 제공하기 때문에 시장 수익의 75.3%를 차지했습니다.

담보대출 부문은 2025년 75.3%의 점유율을 차지할 것으로 예측됩니다. 담보대출은 차량 자체가 담보가 되기 때문에 대출자의 리스크를 줄일 수 있어 매우 선호되는 형태입니다. 신용도가 높은 대출자는 더 긴 상환 기간과 낮은 이자율의 혜택을 받을 수 있습니다. 대출자 입장에서는 필요한 경우 자산을 압류할 수 있는 옵션을 통해 보증을 받을 수 있고, 대출자 입장에서는 유리한 대출 솔루션을 이용할 수 있다는 장점이 있습니다. 이러한 리스크 관리 구조로 인해 담보대출은 중고차 금융 시장의 근간이 되고 있습니다.

미국 중고차 융자 시장은 2025년 83억 달러 규모에 달했습니다. 신차 가격의 급등으로 중고차가 많은 소비자의 선택이 되었고, 대출 수요가 지속되고 있습니다. 은행, 신용조합, 제조업체 금융회사는 프라임, 니어프라임, 서브프라임을 포함한 모든 신용 카테고리의 소비자에게 적극적으로 서비스를 제공합니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 정보원

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 기술 로드맵과 진화

- 기술 도입 수명주기 분석

- 가격 동향

- 지역별

- 제품별

- 특허 분석

- 투자 및 자금조달 분석

- 가격 결정과 금리 분석

- 금리 벤치마킹

- 과거 금리 동향

- 딜러 마크업 경제학

- 부대 상품 가격 결정

- 수수료 체계 분석

- 총 신용 비용 분석

- 거시경제 및 시장 사이클에의 감응도

- 소비자 신용 스코어 분포 분석

- 신용 스코어 경시적인 동향

- 신용 스코어 분포(인구통계별)

- 신용 스코어가 융자 조건에 미치는 영향

- 신용 스코어 개선과 회복

- 고객 행동 분석

- 자동차 구입 의사결정 프로세스

- 융자 채널 선택

- 대출 기간 선택 행동

- 계약금 지불 행동

- 부대 상품 구입 행동

- 지불 행동과 실적

- 리스크 평가 및 경감 프레임워크

- 신용 리스크

- 담보 리스크

- 운영 리스크

- 컴플라이언스 및 규제 리스크

- 시장 및 경제 리스크

- 지속가능성과 ESG 동향

- 환경적 배려

- 사회적 배려

- 거버넌스에 관한 고려사항

- 융자 실무 ESG 통합

- 투자자 및 대주의 ESG 이니셔티브

- 향후 전망과 기회

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획과 자금조달

- 벤더 선정 기준

제5장 시장 추산 및 예측 : 대주별, 2022-2035

- 주요 동향

- 은행

- 민간

- 공개

- 논뱅크(NBFC)

- OEM 전속 금융회사

- 기타

제6장 시장 추산 및 예측 : 융자 유형별, 2022-2035

- 주요 동향

- 담보부 대출

- 무담보 대출

- 리스 파이낸싱

제7장 시장 추산 및 예측 : 차종별, 2022-2035

- 주요 동향

- 이코노미카

- 중형차

- 고급차

제8장 시장 추산 및 예측 : 차종별, 2022-2035

- 주요 동향

- 세단

- 해치백 차량

- SUV

제9장 시장 추산 및 예측 : 융자 기간별, 2022-2035

- 주요 동향

- 단기(12-36개월)

- 중기(37-60개월)

- 장기(60개월 이상)

제10장 시장 추산 및 예측 : 차량 연식별, 2022-2035

- 주요 동향

- 신규(3년 미만)

- 구형(3년 이상 경과)

제11장 시장 추산 및 예측 : 용도별, 2022-2035

- 주요 동향

- 개인/소비자

- 기업/상업

제12장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 개요

- Global companies

- Ally Financial

- Capital One Financial Corporation

- JPMorgan Chase

- Bank of America

- Wells Fargo

- Santander Consumer

- TD Auto Finance

- GM Financial

- Ford Motor Credit Company

- Toyota Financial Services

- Honda Financial Services

- Volkswagen Credit

- BMW Financial Services

- Mercedes-Benz Financial Services

- Regional companies

- Navy Federal Credit Union

- First Tech Federal Credit Union

- Truist Financial

- KeyBank

- Huntington National Bank

- PenFed Credit Union

- Emerging companies

- Carvana

- LendingClub

- Upstart Holdings

- AutoFi

- Exeter Finance

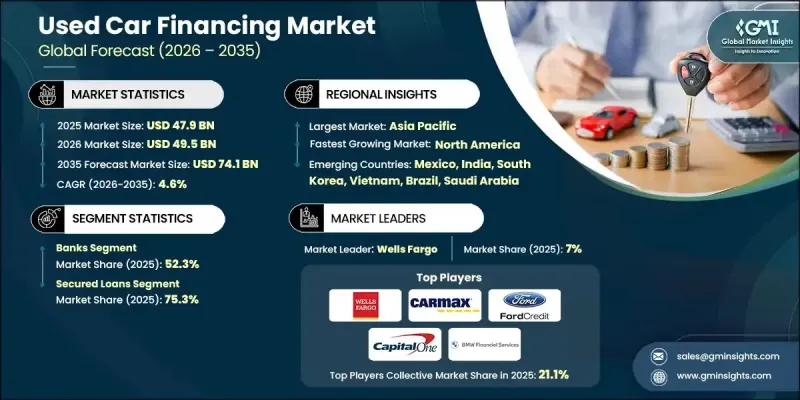

The Global Used Car Financing Market was valued at USD 47.9 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 74.1 billion by 2035.

Rising disposable income has fueled automotive demand, yet the high cost of new vehicles continues to make buyers hesitant. Used car sales have emerged as a practical alternative, enabling consumers to access vehicles at lower price points. Financing solutions, including EMIs, are bridging this gap, making car ownership more attainable and convenient. Lenders are offering flexible interest rates to accommodate varying loan tenures, with rates currently averaging around 4.79% for 12-36 months and 5.29% for 37-60 months, according to industry associations. The Asia-Pacific region accounts for roughly half of the market, driven by China's scale and India's rapid motorization alongside the growth of organized retail networks. North America and Europe remain mature markets but continue to present opportunities through digital financing platforms, innovative insurance solutions, and specialized financing for electric vehicles, supporting steady market expansion globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $47.9 Billion |

| Forecast Value | $74.1 Billion |

| CAGR | 4.6% |

The banks segment held a 52.3% share in 2024. Their dominance stems from low-cost deposit capabilities, wide branch and online networks, and expertise in low-risk lending. Borrowers typically secure 80-90% loan-to-value ratios over 36-72 months. Secured loans accounted for 75.3% of the market revenue, as collateralized loans reduce lender risk while offering borrowers favorable rates and longer tenures.

The secured loans segment held a 75.3% share in 2025. Secured loans are highly preferred because the vehicle itself serves as collateral, reducing risk for lenders. Borrowers with strong credit profiles can benefit from longer repayment terms and lower interest rates. From the lender's perspective, these loans provide assurance through the option to repossess the asset if needed, while borrowers gain access to favorable financing solutions. This risk-managed structure makes secured loans the cornerstone of the used car financing market.

U.S. Used Car Financing Market reached USD 8.3 billion in 2025. High new car prices have made used vehicles the preferred choice for many, sustaining demand for financing. Banks, credit unions, and captive finance companies actively serve consumers across credit categories, including prime, near-prime, and subprime borrowers.

Key players in the Used Car Financing Market include CarMax Auto Finance, Capital One Auto Finance, Ally Financial, Ford Motor Credit Company, Carvana, BMW Financial Services, JPMorgan Chase, GM Financial, Wells Fargo, and Toyota Financial Services. Companies in the Used Car Financing Market are leveraging flexible financing structures, including variable interest rates and customizable EMI plans, to attract a broader customer base. Many are investing in digital platforms and mobile applications to simplify loan applications, approvals, and repayments, increasing convenience for borrowers. Partnerships with dealerships, online marketplaces, and financial institutions allow lenders to expand distribution channels and tap into new regional markets. Risk assessment and credit scoring technologies are being enhanced to accommodate prime, near-prime, and subprime borrowers while minimizing defaults. Additionally, marketing initiatives emphasize affordability, convenience, and vehicle accessibility, strengthening brand presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Lender

- 2.2.3 Loan Type

- 2.2.4 Vehicle Class

- 2.2.5 Vehicle Type

- 2.2.6 Loan Duration

- 2.2.7 Vehicle Age

- 2.2.8 User

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising used vehicle prices expanding addressable market

- 3.2.1.2 Digital pre-qualification reducing friction & improving conversion

- 3.2.1.3 Extended loan terms improving affordability & access

- 3.2.1.4 Embedded finance partnerships expanding distribution

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising interest rates increasing borrowing costs

- 3.2.2.2 Vehicle price normalization risk compressing margins

- 3.2.3 Market opportunities

- 3.2.3.1 Embedded finance partnerships

- 3.2.3.2 EV used car financing emerging niche

- 3.2.3.3 Small business & fleet financing growth

- 3.2.3.4 Credit union-bank partnership models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology roadmaps & evolution

- 3.7.4 Technology adoption lifecycle analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Patent analysis

- 3.10 Investment & Funding Analysis

- 3.10.1 Venture capital in auto fintech

- 3.10.2 Private equity activity in subprime lending

- 3.10.3 Bank investment in digital capabilities

- 3.10.4 Securitization market trends

- 3.11 Pricing & interest rate analysis

- 3.11.1 Interest rate benchmarking

- 3.11.2 Historical interest rate trends

- 3.11.3 Dealer markup economics

- 3.11.4 Add-on product pricing

- 3.11.5 Fee structure analysis

- 3.11.6 Total cost of credit analysis

- 3.12 Macroeconomic & market cycle sensitivity

- 3.12.1 Macroeconomic drivers of used car financing demand

- 3.12.2 Vehicle market dynamics

- 3.12.3 Credit cycle dynamics

- 3.12.4 Recession & economic downturn sensitivity

- 3.12.5 Expansion & recovery dynamics

- 3.12.6 Vehicle ownership rates

- 3.13 Consumer credit score distribution analysis

- 3.13.1 Credit score trends over time

- 3.13.2 Credit score distribution by demographics

- 3.13.3 Credit score impact on loan terms

- 3.13.4 Credit score improvement & rehabilitation

- 3.14 Customer behavior analysis

- 3.14.1 Vehicle purchase decision process

- 3.14.2 Financing channel selection

- 3.14.3 Loan term selection behavior

- 3.14.4 Down payment behavior

- 3.14.5 Add-on product purchase behavior

- 3.14.6 Payment behavior & performance

- 3.15 Risk assessment & mitigation framework

- 3.15.1 Credit risk

- 3.15.2 Collateral risk

- 3.15.3 Operational risk

- 3.15.4 Compliance & regulatory risk

- 3.15.5 Market & economic risk

- 3.16 Sustainability & ESG trends

- 3.16.1 Environmental considerations

- 3.16.2 Social considerations

- 3.16.3 Governance considerations

- 3.16.4 ESG integration in lending practices

- 3.16.5 Investor & lender ESG commitments

- 3.17 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Lender, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Banks

- 5.2.1 Private

- 5.2.2 Public

- 5.3 NBFCs

- 5.4 OEM captive finance companies

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Loan Type, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Secured Loans

- 6.3 Unsecured Loans

- 6.4 Lease Financing

Chapter 7 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Economy Cars

- 7.3 Mid-range

- 7.4 Luxury Cars

Chapter 8 Market Estimates & Forecast, By Vehicle Type, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Sedan

- 8.3 Hatchbacks

- 8.4 SUVs

Chapter 9 Market Estimates & Forecast, By Loan Duration, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Short-term (12-36 months)

- 9.3 Medium-term (37-60 months)

- 9.4 Long-term (Above 60 months)

Chapter 10 Market Estimates & Forecast, By Vehicle Age, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Newer (Upto 3 years)

- 10.3 Older (Above 3 years)

Chapter 11 Market Estimates & Forecast, By Use, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 Individuals/consumers

- 11.3 Businesses/commercial

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.3.8 Benelux

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 ANZ

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global companies

- 13.1.1 Ally Financial

- 13.1.2 Capital One Financial Corporation

- 13.1.3 JPMorgan Chase

- 13.1.4 Bank of America

- 13.1.5 Wells Fargo

- 13.1.6 Santander Consumer

- 13.1.7 TD Auto Finance

- 13.1.8 GM Financial

- 13.1.9 Ford Motor Credit Company

- 13.1.10 Toyota Financial Services

- 13.1.11 Honda Financial Services

- 13.1.12 Volkswagen Credit

- 13.1.13 BMW Financial Services

- 13.1.14 Mercedes-Benz Financial Services

- 13.2 Regional companies

- 13.2.1 Navy Federal Credit Union

- 13.2.2 First Tech Federal Credit Union

- 13.2.3 Truist Financial

- 13.2.4 KeyBank

- 13.2.5 Huntington National Bank

- 13.2.6 PenFed Credit Union

- 13.3 Emerging companies

- 13.3.1 Carvana

- 13.3.2 LendingClub

- 13.3.3 Upstart Holdings

- 13.3.4 AutoFi

- 13.3.5 Exeter Finance