|

시장보고서

상품코드

1906197

독일의 중고차 시장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Used Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

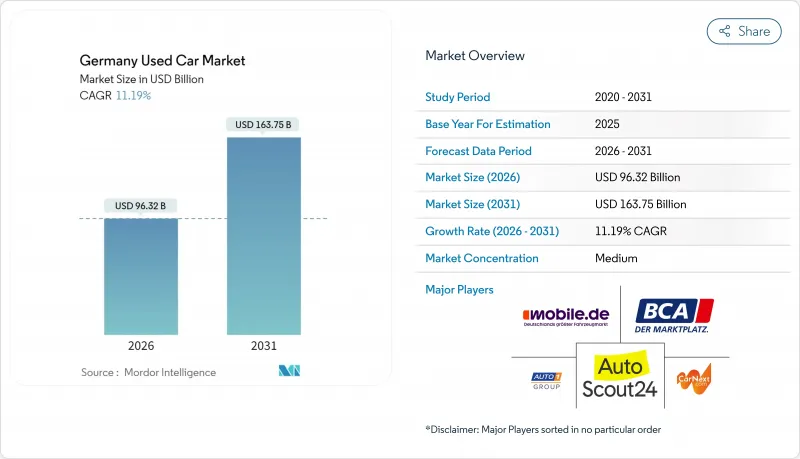

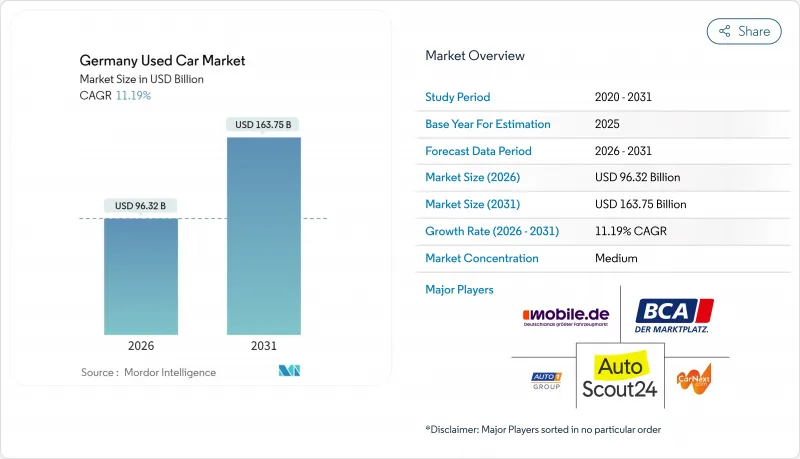

독일의 중고차 시장은 2025년 866억 3,000만 달러로 평가되었고, 2026년 963억 2,000만 달러에서 2031년까지 1,637억 5,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 11.19%를 나타낼 전망입니다.

신차 공급 부족, 노후화된 전국 차량 보유량, 차량 구매 및 판매 과정의 마찰을 줄여주는 온라인 거래 플랫폼의 급속한 확산으로 인해 수요가 견조하게 유지되고 있습니다. 유럽연합 배터리 규정, 저공해 구역 확대 시행, OEM(원제조사) 지원 중고인증차(CPO) 프로그램과 같은 정책적 요인들은 소비자 신뢰도를 재편하고 교체 주기를 단축시키고 있습니다. 배터리 상태 정보 투명성 개선으로 전기차(EV) 재판매 활동이 가속화되는 반면, 휘발유 모델이 여전히 판매량을 주도하고 있습니다. 지역적으로는 남부 제조 중심지인 바덴뷔르템베르크와 바이에른이 우수한 차량 정비 기록으로 프리미엄 잔존 가치를 유지하고 있습니다. 경쟁 강도는 여전히 분산되어 있어, 대형 디지털 기업들이 규모와 데이터 분석을 활용해 소규모 딜러를 앞지르면서 통합의 여지가 남아 있습니다.

독일의 중고차 시장 동향 및 인사이트

평균 차령 상승이 교체 수요를 촉진

독일의 승용차 평균 연식은 현재 10.1년입니다. 12년 이상 된 차량이 34.17%를 차지하며, 소유주들이 최신 안전 및 인포테인먼트 기능을 추구함에 따라 예측 가능한 교체 수요가 발생하고 있습니다. 체계적인 딜러들은 신뢰성 우려를 완화하는 금융 및 보증 상품을 패키지화하여 이점을 활용합니다. 가처분 소득이 높은 남부 지역은 차량 연식이 상대적으로 낮아 동부 지역보다 교체 수요가 더 강합니다. 구독 서비스 제공업체는 단기 계약 주기마다 거의 새 차에 가까운 재고를 시장에 내놓아 교체 주기를 더욱 가속화합니다.

신차 공급 부족으로 중고차 가격 상승

국내 차량 생산량이 2024년 수십 년 만에 최저 수준으로 떨어지면서 납기 지연이 장기화되고 구매자들이 인증 중고차로 눈을 돌리게 되었습니다. 프리미엄 부문은 8-12주에 달하는 공장 생산 지연을 겪고 있으며, 조직화된 딜러들은 이 기간을 활용해 잉여 지역에서 수요가 높은 대도시로 재고를 이동시키고 있습니다. 특히 전기차와 하이브리드 모델에서 중고차 가격의 탄력성이 두드러지는데, 이는 재고 부족 신차의 대체재 역할을 하기 때문입니다.

도시 저공해 구역 확대 속 디젤 수요 감소

유로 4 및 유로 5 규제로 인해 주요 도시에서 구형 디젤 차량의 경쟁력이 약화되고 있습니다. 슈투트가르트 시만 해도 약 19만 대의 디젤 차량을 제한해 도심 내 차량 가치를 하락시켰습니다. 잉여 재고는 점차 동유럽으로 수출되며 무역업자에게 물류 기회를 제공하지만 국내 공급량은 감소하고 있습니다.

부문 분석

해치백은 밀집된 도시 지역에서의 기동성으로 현재 23.84% 점유율로 판매량 1위를 차지하고 있습니다. SUV는 14.63%의 연평균 성장률(CAGR)을 기록할 것으로 예상되며, 이는 다른 어떤 차체 스타일보다 훨씬 높은 수치입니다. 세단은 크로스오버가 동일한 편의성을 더 큰 실용성으로 충족시키면서 점진적인 감소를 겪고 있습니다. 다목적 차량(MPV)은 틈새 가족 시장을 겨냥한 매력을 지니고 있으며, 컨버터블과 스포츠카는 대중 시장보다는 수집가들의 관심을 유지하고 있습니다.

남부 부유 주들은 가처분 소득 수준과 교외형 운전 패턴에 힘입어 SUV 보급률이 가장 높습니다. 반대로 좁은 도로와 주차 공간 제약으로 소형 차량이 선호되는 북부 해안 지역에서는 소형 부문이 여전히 우세합니다. 이러한 차이는 딜러들에게 지역별 차익 거래 기회를 제공합니다.

2025년 독일 중고차 시장 규모에서 조직화된 업체들이 62.55%를 차지했으며 12.29%의 연평균 성장률을 보이고 있습니다. 소비자들은 점차 보증 범위, 금융 지원, 신뢰할 수 있는 애프터서비스를 요구하며, 이는 체계적인 딜러십이 제공하는 장점입니다. 비체계적 판매자들은 여전히 할인 구매자를 끌어모으지만 거래 복잡성이 증가함에 따라 입지를 잃고 있습니다.

대도시 중심지는 더 빠른 통합을 목격하고 있습니다. 상승하는 부동산 비용으로 독립 판매장들은 대형 네트워크와 제휴하거나 퇴출되고 있습니다. 디지털 플랫폼은 도달 범위를 확대하여 체계적 판매자들이 전국적으로 차량을 조달하면서도 지역화된 서비스를 제공할 수 있게 하여 시장 점유를 가속화하고 있습니다.

2025년 기준 가솔린 모델이 60.92% 점유율을 유지했습니다. 그러나 명확한 배터리 건강 기준과 확장되는 급속 충전 인프라의 지원으로 BEV(순수 전기차)는 21.93%라는 놀라운 연평균 성장률(CAGR)로 확대될 전망입니다. 디젤은 저공해 구역 정책으로 구조적 하락세를 보이지만, 물류 중심의 농촌 지역에서는 여전히 가치가 있습니다. 하이브리드 차량은 주행 거리 신뢰성을 제공하면서 신흥 배출 기준을 충족하는 과도기적 부문를 담당합니다.

남부 주들은 OEM 인센티브와 밀집된 충전기 네트워크의 혜택을 받아 중고 BEV의 초기 도입 지역입니다. 동부 지역은 아직 뒤처져 있지만 인프라 격차가 해소되면서 상승 잠재력을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 평균 차량 연령 상승으로 교체 수요 증가

- 신차 공급 부족으로 중고차 가격 상승

- 온라인 거래 플랫폼 확산

- EU 배터리 규정으로 BEV 재판매 가속화

- 구독 모델로 신차급 중고차 수요 촉진

- OEM 인증 중고차(CPO) 프로그램 확산

- 시장 성장 억제요인

- 도시 저공해 구역 확대에 따른 디젤 수요 감소

- 높은 금리로 인한 금융 접근성 제한

- 디지털 등록 지연으로 인한 소유권 이전 지체

- 수출로 인한 국내 시장 내 합리적 가격 차량 유출

- 가치/가치 체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액(달러) 및 수량(대수))

- 차량 유형별

- 해치백 자동차

- 세단

- 스포츠 유틸리티 차량(SUV)

- 다목적 차량(MPV)

- 기타(컨버터블, 쿠페, 크로스오버, 스포츠카)

- 공급업체더 유형별

- 조직화

- 비조직화

- 연료 유형별

- 가솔린차

- 디젤차

- 하이브리드 자동차(HEV 및 PHEV)

- 배터리식 전기자동차(BEV)

- 기타(LPG, CNG 등)

- 차량 연식별

- 0-2년

- 3-5년

- 6-년

- 9-12년

- 12년 이상

- 가격대별

- 5,000달러 미만

- 5,000-9,999달러

- 10,000-14,999달러

- 15,000-19,999달러

- 20,000-29,999달러

- 30,000달러 이상

- 판매 채널별

- 온라인

- 오프라인

- 소유 형태별

- 최초 소유자의 재판매

- 복수 소유자

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AUTO1 Group SE(wirkaufendeinauto.de, AutoHero)

- mobile.de GmbH

- AutoScout24GmbH

- CarNext.com

- BCA Autoauktionen GmbH

- heycar GmbH

- Driverama Germany GmbH

- Cinch Cars Ltd.

- Cazoo Ltd.

- pkw.de Autoborse GmbH

- OOYYO Corporation

- 12Gebrauchtwagen.de

- FairCar GmbH

- Autobid.de(AlphAuction GmbH)

- Gebrauchtwagen.de AG

- Carsale24GmbH

- Cargurus Germany GmbH

- Autoscout24 Dealer Financing

- Emil Frey Gruppe(Used-Car Superstores)

제7장 시장 기회와 장래의 전망

HBR 26.01.26The German used car market was valued at USD 86.63 billion in 2025 and estimated to grow from USD 96.32 billion in 2026 to reach USD 163.75 billion by 2031, at a CAGR of 11.19% during the forecast period (2026-2031).

Robust demand stems from tight new-car supply, an aging national vehicle fleet, and the rapid uptake of online transaction platforms that reduce friction in vehicle sourcing and sales. Policy drivers such as the European Union Battery Regulation, broader low-emission-zone roll-outs, and OEM-backed certified-pre-owned (CPO) programs are reshaping consumer confidence and shortening replacement cycles. Electric-vehicle (EV) resale activity is accelerating as battery-health transparency improves, while petrol models continue to dominate volumes. Regionally, the southern manufacturing hubs of Baden-Wurttemberg and Bayern benefit from better vehicle maintenance records, supporting premium residual values. Competitive intensity remains fragmented, leaving room for consolidation as larger digital players leverage scale and data analytics to outpace smaller dealers.

Germany Used Car Market Trends and Insights

Rising Average Vehicle Age Boosts Replacement Demand

Germany's passenger-car fleet now averages 10.1 years. Vehicles older than 12 years hold a 34.17% share, creating predictable replacement pressure as owners seek newer safety and infotainment features. Organized dealers capitalize by packaging finance and warranty offerings that mitigate reliability concerns. Southern states, where disposable incomes are higher, keep fleets younger, leaving eastern regions to generate stronger replacement flows. Subscription providers further accelerate turnover by releasing nearly-new stock after each short-term contract cycle.

Tight Supply of New Cars Elevates Used-Car Prices

Domestic vehicle production fell to a decades-low level in 2024, causing extended lead times and steering buyers toward certified pre-owned alternatives. Premium segments face 8-12-week factory delays, a window that organized dealers exploit by moving stock from surplus regions to high-demand metros. Resilient used-car prices are especially evident in electric and hybrid models, which serve as substitutes for out-of-stock new vehicles.

Diesel Demand Falls Amid Urban Low-Emission Zones

Euro 4 and Euro 5 restrictions render older diesel units less attractive in major cities. Stuttgart alone restricts roughly 190,000 diesel cars, depressing valuations within its urban core. Surplus stock is increasingly exported to Eastern Europe, creating logistical opportunities for traders but eroding domestic availability.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Online Transaction Platforms

- EU Battery Regulation Accelerates BEV Remarketing

- High Interest Rates Restrict Financing Affordability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hatchbacks currently lead volume at 23.84% share due to their maneuverability in dense urban areas. SUVs are projected to record a 14.63% CAGR, well ahead of any other body style. Sedans face a gradual decline as crossovers satisfy the same comfort demands with greater practicality. Multi-purpose vehicles hold niche family appeal, while convertibles and sports cars sustain collector interest rather than mass-market traction.

Affluent southern states exhibit the highest SUV penetration, supported by disposable income levels and suburban driving patterns. Conversely, compact segments remain dominant in northern coastal regions where narrow streets and tighter parking favor smaller footprints. The differential offers dealers geographical arbitrage opportunities.

Organized players commanded 62.55% of the German used car market size in 2025 and are growing at 12.29% CAGR. Consumers increasingly seek warranty coverage, financing, and reliable after-sales service, advantages that structured dealerships deliver. Unorganized sellers still attract bargain hunters but lose ground as transaction complexity rises.

Metropolitan centers witness faster consolidation; rising real-estate costs push independent lots to partner with larger networks or exit. Digital platforms amplify reach, allowing organized vendors to source nationally while offering localized service, accelerating their market capture.

Petrol models retained 60.92% share in 2025. However, BEVs will expand at a striking 21.93% CAGR, aided by clear battery-health standards and expanding fast-charging grids. Diesel faces structural decline owing to low-emission-zone policies, though it remains valuable in logistics-heavy rural districts. Hybrid vehicles serve a transitional segment, providing range confidence while meeting emerging emissions expectations.

Southern states, benefitting from OEM incentives and dense charger networks, are early adopters of used BEVs. Eastern regions lag yet present upside potential as infrastructure gaps close.

The Germany Used Car Market Report is Segmented by Vehicle Type (Hatchbacks, Sedans, and More), Vendor Type (Organized and Unorganized), Fuel Type (Petrol and More), Vehicle Age (0 To 2 Years and More), Price Segment (Below USD 5, 000 and More), Sales Channel (Online and Offline), and Ownership (First-Owner Resale and Multi-Owner). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- AUTO1 Group SE (wirkaufendeinauto.de, AutoHero)

- mobile.de GmbH

- AutoScout24 GmbH

- CarNext.com

- BCA Autoauktionen GmbH

- heycar GmbH

- Driverama Germany GmbH

- Cinch Cars Ltd.

- Cazoo Ltd.

- pkw.de Autoborse GmbH

- OOYYO Corporation

- 12Gebrauchtwagen.de

- FairCar GmbH

- Autobid.de (AlphAuction GmbH)

- Gebrauchtwagen.de AG

- Carsale24 GmbH

- Cargurus Germany GmbH

- Autoscout24 Dealer Financing

- Emil Frey Gruppe (Used-Car Superstores)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising average vehicle age boosts replacement demand

- 4.2.2 Tight supply of new cars elevates used-car prices

- 4.2.3 Proliferation of online transaction platforms

- 4.2.4 EU Battery Regulation accelerates BEV remarketing

- 4.2.5 Subscription models spur demand for nearly-new cars

- 4.2.6 OEM certified-pre-owned (CPO) programs gain traction

- 4.3 Market Restraints

- 4.3.1 Diesel demand falls amid urban Low-Emission Zones

- 4.3.2 High interest rates restrict financing affordability

- 4.3.3 Digital registration backlogs slow title transfers

- 4.3.4 Exports siphon affordable stock from domestic market

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Hatchbacks

- 5.1.2 Sedans

- 5.1.3 Sport-Utility Vehicles (SUVs)

- 5.1.4 Multi-Purpose Vehicles (MPVs)

- 5.1.5 Others (convertibles, coupes, crossovers, sports cars)

- 5.2 By Vendor Type

- 5.2.1 Organised

- 5.2.2 Unorganized

- 5.3 By Fuel Type

- 5.3.1 Petrol

- 5.3.2 Diesel

- 5.3.3 Hybrid Vehicles (HEV and PHEV)

- 5.3.4 Battery-Electric Vehicles (BEV)

- 5.3.5 Others (LPG, CNG, etc.)

- 5.4 By Vehicle Age

- 5.4.1 0 to 2 Years

- 5.4.2 3 to 5 Years

- 5.4.3 6 to 8 Years

- 5.4.4 9 to 12 Years

- 5.4.5 Above 12 Years

- 5.5 By Price Segment

- 5.5.1 Below USD 5,000

- 5.5.2 USD 5,000 to USD 9,999

- 5.5.3 USD 10,000 to USD 14,999

- 5.5.4 USD 15,000 to USD 19,999

- 5.5.5 USD 20,000 to USD 29,999

- 5.5.6 USD 30,000 and Above

- 5.6 By Sales Channel

- 5.6.1 Online

- 5.6.2 Offline

- 5.7 By Ownership

- 5.7.1 First-owner Resale

- 5.7.2 Multi-owner

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AUTO1 Group SE (wirkaufendeinauto.de, AutoHero)

- 6.4.2 mobile.de GmbH

- 6.4.3 AutoScout24 GmbH

- 6.4.4 CarNext.com

- 6.4.5 BCA Autoauktionen GmbH

- 6.4.6 heycar GmbH

- 6.4.7 Driverama Germany GmbH

- 6.4.8 Cinch Cars Ltd.

- 6.4.9 Cazoo Ltd.

- 6.4.10 pkw.de Autoborse GmbH

- 6.4.11 OOYYO Corporation

- 6.4.12 12Gebrauchtwagen.de

- 6.4.13 FairCar GmbH

- 6.4.14 Autobid.de (AlphAuction GmbH)

- 6.4.15 Gebrauchtwagen.de AG

- 6.4.16 Carsale24 GmbH

- 6.4.17 Cargurus Germany GmbH

- 6.4.18 Autoscout24 Dealer Financing

- 6.4.19 Emil Frey Gruppe (Used-Car Superstores)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment