|

시장보고서

상품코드

1913380

베이커리 가공 장비 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Bakery Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

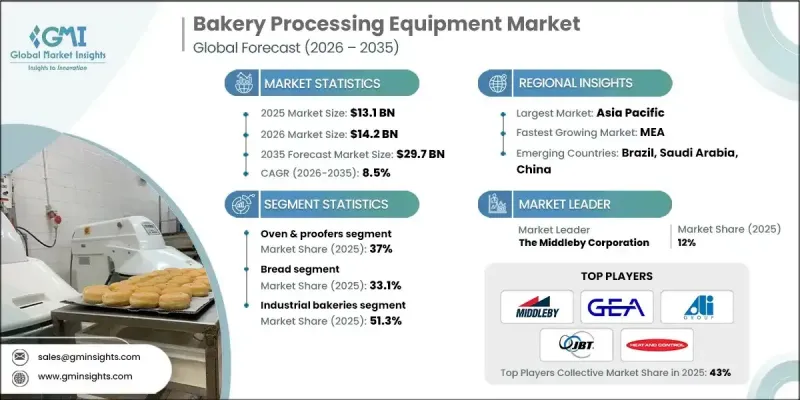

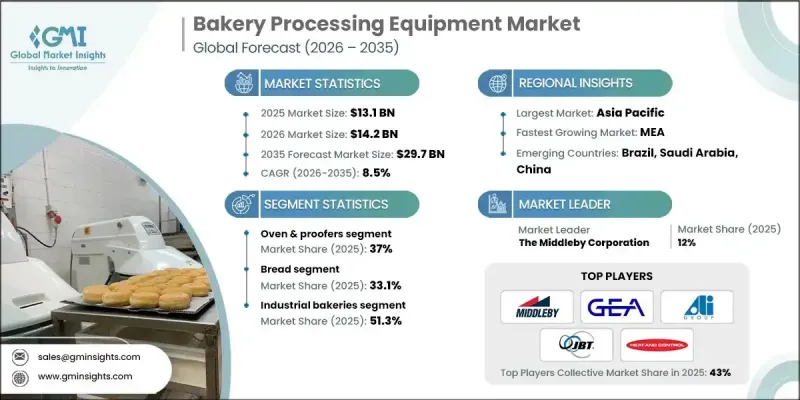

세계의 베이커리 가공 장비 시장은 2025년에 131억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 8.5%로 성장할 전망이며, 297억 달러에 이를 것으로 예측되고 있습니다.

시장의 성장은 효율성 향상, 노동력 의존도 저감, 균일한 제품 기준 유지에 주력하는 기업이 늘어나는 가운데 베어커리 가공 전체에서 자동화로의 전환 가속에 의해 견인되고 있습니다. 엔드 투 엔드 생산 워크플로우를 최적화하기 위해 자동화 시스템의 도입이 확대되고 있으며, 제빵업자는 생산량 증가 요구에 대응하면서 운영 경비를 관리할 수 있도록 지원되고 있습니다. 차별화된 맞춤형 빵 제품에 대한 소비자 수요 증가는 설비 구매 의사결정에 영향을 미치고 있으며, 빈번한 제품 변경에 대응하면서 생산성을 손상시키지 않는 적응성이 높은 기계에 대한 투자를 촉진하고 있습니다. 병행하여 식품 안전 및 위생 기준에 대한 관심 고조가 설비 설계의 우선순위를 형성하고 있습니다. 제조업체는 위생 관리를 지원하고, 오염 위험을 줄이며, 진화하는 규제 요구 사항을 충족하는 기계를 더욱 강조합니다. 설비 공급업체는 청결, 내구성 및 컴플라이언스를 지원하는 설계를 도입하여 대응하여 현대 제빵 환경에서 품질 보증의 중요성을 강화하고 있습니다. 이러한 복합적인 동향으로 인해 베이커리 장비는 확장성, 컴플라이언스 및 소비자 대응을 가능하게 하는 중요한 기반으로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 당초 시장 규모 | 131억 달러 |

| 시장 규모 예측 | 297억 달러 |

| CAGR | 8.5% |

상업용 베이커리 부문은 2025년 51.3%의 점유율을 차지했습니다. 이 부문은 대량 생산의 일관된 품질을 보장하면서 연속 생산을 지원하기 때문에 대규모 고성능 장비에 크게 의존합니다. 이 부문 수요는 정확도 향상, 수작업 감소, 비용 효율적인 대량 생산을 지원하는 솔루션에 계속 집중되고 있습니다.

오븐 프루퍼 카테고리는 2023년에 37%의 점유율을 차지했습니다. 이 부문은 제품의 균일성, 구조 및 종합적인 품질에 직접적인 영향을 미치는 소성 및 발효 조건의 제어에 중심적인 역할을 합니다. 이 카테고리의 장비는 신뢰할 수 있는 생산 결과를 지원하는 안정적인 가공 환경을 유지할 수 있는 능력을 높이 평가합니다.

유럽의 베이커리 가공 장비 시장은 강력한 혁신 능력, 엄격한 품질 기준, 지속가능성에 대한 관심 증가에 힘입어 2025년에는 39억 달러에 달했습니다. 현지 제조업체들은 규제 프레임워크 및 변화하는 소비자의 기대에 부응하면서 첨단 엔지니어링, 에너지 효율 및 환경 친화적인 생산 기법을 계속 선호합니다.

자주 묻는 질문

목차

제1장 분석 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계의 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 베이커리 업계의 일손 부족을 보완하기 위한 자동화 진전

- 냉동 및 포장 베이커리 제품의 성장

- 식품 안전 및 제품의 일관성에 대한 주력

- 업계의 잠재적 위험 및 과제

- 소규모 베이커리에서 높은 초기 설비 투자 비용

- 기존 시설에서 스페이스 및 유틸리티의 제약

- 시장 기회

- 소매 체인 및 점내 베이커리의 확대

- 클린 라벨, 글루텐 프리 및 특수 제품의 동향

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서문

- 기업별 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 동향

- 기업 합병 및 인수(M&A)

- 사업 제휴 및 협력

- 신제품 발매

- 사업 확대 계획

제5장 시장의 추정 및 예측 : 제품 유형별(2022-2035년)

- 오븐 프루퍼

- 믹서

- 250kg 미만

- 250-500 kg

- 500-1,000 kg

- 1,000-1,500 kg

- 1,500kg 이상

- 슬라이서

- 100 kg 미만

- 100-150 kg

- 150-250 kg

- 250-350 kg

- 350kg 이상

- 시트 성형기 및 몰드 성형기

- 500-1,000 kg

- 1,000-1,500 kg

- 1,500kg 이상

- 기타

제6장 시장의 추정 및 예측 : 용도별(2022-2035년)

- 빵

- 페이스트리

- 피자

- 크로와상

- 플랫 브레드

- 파이 및 키시

- 비스킷

- 토르티야

제7장 시장의 추정 및 예측 : 최종 용도별(2022-2035년)

- 상업용 베이커리

- 장인 베이커리

- 소매용 베이커리

- 기타

제8장 시장의 추정 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- The Middleby Corporation

- GEA Group

- ALI Group SRL A Socio Unico

- John Bean Technologies Corporation

- Markel Ventures Inc.

- Heat and Control, Inc.

- Rheon Automatic Machinery Co., Ltd.

- Fritsch Group

- Baker Perkins Ltd.

- Gemini Bakery Equipment Company

The Global Bakery Processing Equipment Market was valued at USD 13.1 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 29.7 billion by 2035.

Market momentum is driven by the accelerating shift toward automation across bakery operations, as businesses focus on improving efficiency, lowering workforce dependency, and maintaining uniform product standards. Automated systems are increasingly being adopted to optimize end-to-end production workflows, helping bakeries meet rising output requirements while controlling operational expenses. Growing consumer demand for differentiated and made-to-order bakery offerings is also influencing equipment purchasing decisions, encouraging investment in adaptable machinery capable of handling frequent product changes without affecting throughput. In parallel, heightened attention to food safety and hygiene standards is shaping equipment design priorities. Bakeries place greater emphasis on machinery that supports sanitation, reduces contamination risk, and aligns with evolving regulatory expectations. Equipment suppliers are responding by introducing designs that support cleanliness, durability, and compliance, reinforcing the importance of quality assurance in modern bakery environments. These combined trends continue to position bakery processing equipment as a critical enabler of scalable, compliant, and consumer-responsive production.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.1 Billion |

| Forecast Value | $29.7 Billion |

| CAGR | 8.5% |

The industrial bakeries segment accounted for 51.3% share in 2025. This segment relies heavily on large-scale, high-performance equipment to support continuous production while ensuring consistent quality across large volumes. Demand from this segment remains focused on solutions that improve precision, reduce manual intervention, and support cost-efficient mass production.

The ovens and proofers category represented 37% share in 2023. This segment plays a central role in controlling baking and fermentation conditions, which directly influences product consistency, structure, and overall quality. Equipment in this category is valued for its ability to maintain stable processing environments that support reliable production outcomes.

Europe Bakery Processing Equipment Market reached USD 3.9 billion in 2025, supported by strong innovation capabilities, rigorous quality benchmarks, and a growing focus on sustainability. Regional manufacturers continue to prioritize advanced engineering, energy efficiency, and environmentally responsible production practices, aligning with regulatory frameworks and evolving consumer expectations.

Key companies active in the Global Bakery Processing Equipment Market include GEA Group, Baker Perkins Ltd., The Middleby Corporation, Rheon Automatic Machinery Co., Ltd., Gemini Bakery Equipment Company, ALI Group S.R.L. A Socio Unico, Heat and Control, Inc., John Bean Technologies Corporation, Fritsch Group, and Markel Ventures Inc. Companies operating in the Global Bakery Processing Equipment Market are strengthening their competitive position through technology-driven innovation and customer-focused solutions. Many manufacturers are investing in automation and digital integration to enhance equipment performance and operational reliability. Customization capabilities are being expanded to help bakeries respond to changing consumer preferences without sacrificing efficiency. Strategic partnerships with bakery operators are supporting long-term equipment adoption and service-based revenue models.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation to offset bakery labor shortages

- 3.2.1.2 Growth in frozen and packaged bakery products

- 3.2.1.3 Focus on food safety and product consistency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront capital cost for small bakeries

- 3.2.2.2 Space and utility constraints in existing facilities

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of retail chains and in-store bakeries

- 3.2.3.2 Clean-label, gluten-free and specialty product trends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: The trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Oven & proofers

- 5.3 Mixers

- 5.3.1 Below 250 kg

- 5.3.2 250-500 kg

- 5.3.3 500-1,000 kg

- 5.3.4 1,000-1,500 kg

- 5.3.5 Above 1,500 kg

- 5.4 Slicer

- 5.4.1 Below 100 kg

- 5.4.2 100-150 kg

- 5.4.3 150-250 kg

- 5.4.4 250-350 kg

- 5.4.5 Above 350 kg

- 5.5 Sheeters & molders

- 5.5.1 500-1,000 kg

- 5.5.2 1,000-1,500 kg

- 5.5.3 Above 1,500 kg

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bread

- 6.3 Pastry

- 6.4 Pizza

- 6.5 Croissant

- 6.6 Flatbread

- 6.7 Pie/Quiche

- 6.8 Biscuits

- 6.9 Tortilla

Chapter 7 Market Estimates and Forecast, By End Use 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Industrial bakeries

- 7.3 Artisanal bakeries

- 7.4 Retail bakeries

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 The Middleby Corporation

- 9.2 GEA Group

- 9.3 ALI Group S.R.L. A Socio Unico

- 9.4 John Bean Technologies Corporation

- 9.5 Markel Ventures Inc.

- 9.6 Heat and Control, Inc.

- 9.7 Rheon Automatic Machinery Co., Ltd.

- 9.8 Fritsch Group

- 9.9 Baker Perkins Ltd.

- 9.10 Gemini Bakery Equipment Company