|

시장보고서

상품코드

1928921

자율주행 라스트 마일 배송 시장 기회, 성장 동인, 업계 동향 분석 및 예측(2026-2035년)Autonomous Last Mile Delivery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

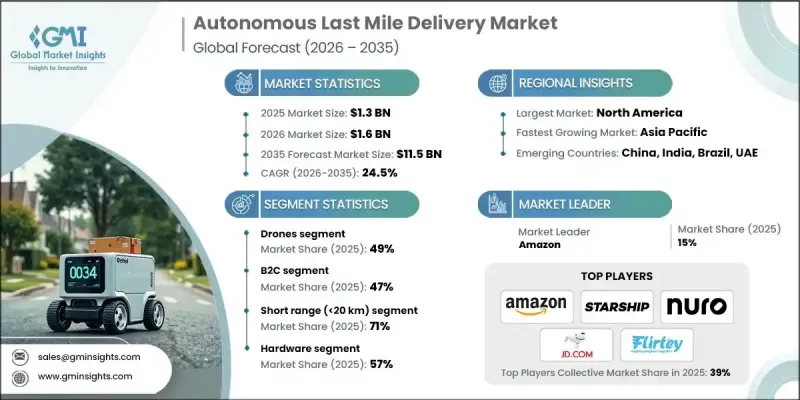

세계의 자율주행 라스트 마일 배송 시장은 2025년에 13억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 24.5%로 성장하여 115억 달러에 달할 것으로 예측됩니다.

자율주행 라스트마일 배송은 인공지능, 로봇공학, 자율주행 차량을 활용하여 사람의 개입 없이 상품을 배송 거점에서 최종 사용자까지 운송하는 혁신적인 물류 솔루션으로 널리 알려져 있습니다. 이 기술은 다양한 배송 환경에서 효율적으로 작동하도록 설계된 다양한 플랫폼을 포괄합니다. 시장의 성장은 디지털 커머스의 급속한 확대, 인건비 상승, 자율 시스템의 능력 향상에 의해 촉진되고 있습니다. 온라인 구매 활동 증가는 확장성과 유연성을 갖춘 배송 모델에 대한 수요를 크게 증가시키고 있습니다. 동시에 기술 비용 절감과 운영 효율성 향상으로 자율주행 배송 솔루션의 경제성이 향상되어 기존 배송 방식과의 경쟁력이 강화되고 있습니다. 규제 측면의 발전도 상용화를 지원하고 있으며, 명확한 정책 프레임워크가 사업자의 불확실성을 줄여주고 있습니다. 이러한 추세는 물류 전략의 재구성, 소비자의 배송 기대치에 대한 영향, 도시 및 교외 지역의 인프라 계획 변경을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 13억 달러 |

| 예측 금액 | 115억 달러 |

| CAGR | 24.5% |

드론 배송 부문은 2025년 49%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 22.8%의 성장률을 보일 것으로 전망됩니다. 드론 플랫폼은 특히 규제가 느슨한 공역에서 지상의 혼잡을 피하면서 신속한 배송을 지원할 수 있는 능력으로 주목받고 있습니다. 전력 시스템, 내비게이션 소프트웨어, 운영 신뢰성의 지속적인 개선으로 실용적인 이용 사례와 배송 효율성이 확대되고 있습니다.

BtoC 부문은 2025년 47%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 24.2%로 가장 빠른 속도로 성장할 것으로 예측됩니다. 이 부문의 성장은 더 빠른 상품 제공과 유연한 배송 시간에 대한 소비자의 기대가 높아졌기 때문입니다. 자율 배송 솔루션은 연속 운행 및 배송 비용 절감을 통해 이러한 요구 사항을 충족하는 데 적합합니다.

북미 자율주행 라스트마일 배송 시장은 2024년 36%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 22.1%의 성장률을 보일 것으로 전망됩니다. 이 지역의 선도적 위치는 첨단 디지털 소매 인프라, 유리한 규제 환경, 자동화 도입 증가, 기술 개발 기업의 높은 집중도에 의해 뒷받침되고 있습니다. 미국은 조기 도입과 대규모 배포 이니셔티브를 통해 지역 성장에 기여하는 주요 국가로 남아있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 플랫폼별, 2022-2035년

제6장 시장 추산 및 예측 : 제공 형태별, 2022-2035년

제7장 시장 추산 및 예측 : 범위별, 2022-2035년

제8장 시장 추산 및 예측 : 솔루션별, 2022-2035년

제9장 시장 추산 및 예측 : 용도별, 2022-2035년

제10장 시장 추산 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

LSH 26.02.27The Global Autonomous Last Mile Delivery Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 24.5% to reach USD 11.5 billion by 2035.

Autonomous last-mile delivery is widely recognized as a transformative logistics solution that relies on artificial intelligence, robotics, and self-operating vehicles to move goods from fulfillment points to end users without human intervention. The technology spans a range of platforms designed to operate efficiently across varied delivery environments. Market growth is being fueled by the rapid expansion of digital commerce, escalating workforce expenses, and continuous improvements in autonomous system capabilities. Rising online purchasing activity has significantly increased demand for scalable and flexible delivery models. At the same time, declining technology costs and improved operational efficiency are enhancing the economic viability of autonomous delivery solutions, allowing them to compete more effectively with conventional delivery methods. Regulatory progress is also supporting commercialization, as clearer policy frameworks are reducing uncertainty for operators. Together, these dynamics are reshaping logistics strategies, influencing consumer delivery expectations, and prompting changes in urban and suburban infrastructure planning.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 24.5% |

The drone-based delivery segment held a share of 49% in 2025 and is forecast to grow at a CAGR of 22.8% from 2026 to 2035. Drone platforms are gaining traction due to their ability to support rapid deliveries while avoiding ground-level congestion, particularly in less densely regulated airspace. Ongoing improvements in power systems, navigation software, and operational reliability are expanding their practical use cases and delivery efficiency.

The business-to-consumer segment accounted for 47% share in 2025 and is projected to grow at the fastest pace, with a CAGR of 24.2% through 2035. Growth in this segment is attributed to increasing consumer expectations for faster fulfillment and flexible delivery windows. Autonomous delivery solutions are well-suited to meet these requirements through continuous operation and reduced delivery costs.

North America Autonomous Last Mile Delivery Market captured 36% share in 2024 and is expected to grow at a CAGR of 22.1% during 2035. The region's leadership is supported by advanced digital retail infrastructure, favorable regulatory developments, increasing automation adoption, and a strong concentration of technology developers. The United States remains the primary contributor to regional growth due to early adoption and large-scale deployment initiatives.

Key companies operating in the Global Autonomous Last Mile Delivery Market include Starship Technologies, Amazon, Wing Aviation, Nuro, Zipline, UPS, JD.com, Kiwibot, and Flirtey. Companies active in the Autonomous Last Mile Delivery Market are strengthening their positions through technology development, pilot deployments, and strategic partnerships. Many players are investing heavily in artificial intelligence, navigation systems, and fleet management platforms to improve reliability and scalability. Collaborations with retailers, logistics providers, and local authorities are helping accelerate real-world deployment and regulatory alignment. Firms are also expanding geographic coverage through phased rollouts and focusing on cost optimization to improve commercial viability. Continuous testing, data-driven optimization, and modular platform design are enabling companies to adapt quickly to evolving delivery requirements and secure long-term market footholds.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Platform

- 2.2.3 Delivery Mode

- 2.2.4 Range

- 2.2.5 Solutions

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 E-commerce growth boosts last-mile delivery demand

- 3.2.1.3 Rising labor costs favor automation

- 3.2.1.4 AI and robotics advancements improve efficiency

- 3.2.1.5 Urbanization and traffic congestion increase need for autonomous delivery

- 3.2.1.6 Sustainability initiatives promote electric autonomous vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory and legal barriers slow deployment

- 3.2.2.2 High initial investment limits adoption

- 3.2.3 Market opportunities

- 3.2.3.1 Smart city integration for delivery corridors

- 3.2.3.2 Healthcare and pharmaceutical deliveries

- 3.2.3.3 Fleet-as-a-service models

- 3.2.3.4 Cross-industry partnerships

- 3.2.3.5 Expansion in emerging markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US - Federal Motor Vehicle Safety Standards (FMVSS) exemption templates for sidewalk robots under 400 pounds, replacing waiver-by-waiver process.

- 3.4.1.2 Canada - Anticipated updates to beyond-visual-line-of-sight (BVLOS) operations regulations and new weight regulations for drone delivery with enhanced safety rules for urban operations.

- 3.4.2 Europe

- 3.4.2.1 Germany - Federal Ministry of Transport and Digital Infrastructure autonomous vehicle testing infrastructure framework with €3.2 billion investment and dedicated autonomous vehicle zones in Hamburg and Munich Emergen Research

- 3.4.2.2 UK - Automated Vehicles Act 2024 establishing comprehensive legal framework with secondary regulations expected by 2027

- 3.4.2.3 France - Black-box recorder requirement for all self-driving cars starting 2025 to establish accident responsibility and transparency

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Beijing Autonomous Vehicle Regulation (April 2025) outlining procedures for AV pilot applications and Ministry of Industry and Information Technology regulations addressing safety concerns

- 3.4.3.2 India - Draft Civil Drone (Promotion and Regulation) Bill 2025 mandating registration, Unique Identification Numbers (UIN), type certification for drone manufacturers, and 5% GST on commercial UAVs

- 3.4.3.3 Japan - National METI roadmap (2025) to scale higher-capability autonomous last-mile delivery solutions beyond low-speed models legalized in 2023

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Regional autonomy with Sao Paulo Level 3 autonomous taxi pilots (2024), no national framework yet established

- 3.4.5 MEA

- 3.4.5.1 Saudi Arabia - Vision 2030 initiative targeting 50% increase in autonomous vehicle presence on public roads with government-driven investment and regulatory reforms to remove AV deployment barriers

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Use cases & success stories

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Platform, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Drones

- 5.2.1 Multi-rotor drones

- 5.2.2 Fixed-wing drones

- 5.2.3 Hybrid VTOL drones

- 5.3 Robots

- 5.3.1 Sidewalk delivery robots

- 5.3.2 Autonomous ground vehicles (AGVs)

- 5.3.3 Indoor delivery robots

- 5.4 Trucks & vans

Chapter 6 Market Estimates & Forecast, By Delivery Mode, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 B2B

- 6.3 B2C

- 6.4 C2C

Chapter 7 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short range (<20 km)

- 7.3 Long range (>20 km)

Chapter 8 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Hardware

- 8.2.1 Vehicle platforms

- 8.2.2 Sensors (LiDAR, cameras, ultrasonic, radar)

- 8.2.3 Batteries / Power systems

- 8.3 Software

- 8.3.1 Autonomous navigation software

- 8.3.2 Fleet management platforms

- 8.3.3 AI / Machine learning algorithms

- 8.4 Services

- 8.4.1 Maintenance & support

- 8.4.2 System integration & consultancy

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 E-commerce

- 9.3 Food and grocery

- 9.4 Parcel & courier services

- 9.5 Pharmaceutical

- 9.6 Furniture & appliance

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Amazon

- 11.1.2 DHL

- 11.1.3 Flirtey

- 11.1.4 JD.com

- 11.1.5 Matternet

- 11.1.6 Nuro

- 11.1.7 Starship Technologies

- 11.1.8 UPS

- 11.1.9 Wing Aviation

- 11.1.10 Zipline

- 11.2 Regional Players

- 11.2.1 JD Logistics

- 11.2.2 Kiwibot

- 11.2.3 Postmates

- 11.2.4 RoboSense

- 11.2.5 Segway Robotics

- 11.2.6 SF Express

- 11.2.7 Swiggy

- 11.2.8 TeleRetail Robotics

- 11.2.9 Yandex Delivery

- 11.2.10 Zomato

- 11.3 Emerging Technology Innovators

- 11.3.1 Flytrex

- 11.3.2 Manna Aero

- 11.3.3 Ottonomy.IO

- 11.3.4 Refraction AI

- 11.3.5 Serve Robotics