|

시장보고서

상품코드

1928942

텔레매틱스 시스템 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Telematics Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

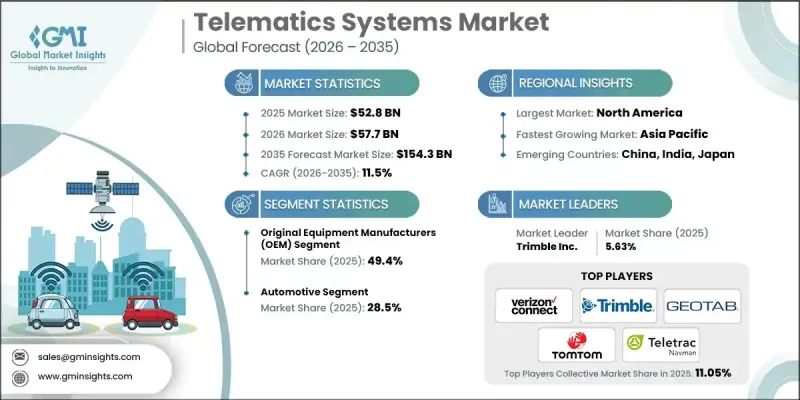

세계의 텔레매틱스 시스템 시장은 2025년에 528억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 11.5%로 성장하여 1,543억 달러에 이를 것으로 예측됩니다.

시장 성장은 차량 및 자산 전반에 걸친 디지털 연결성에 대한 수요 증가, 데이터 기반 차량 운영에 대한 의존도 증가, 전기 모빌리티로의 전환 가속화에 힘입어 성장세를 보이고 있습니다. 조직은 가시성, 안전성, 효율성을 향상시키면서 운영 비용을 절감할 수 있는 솔루션을 우선순위에 두고 있습니다. 규제 프레임워크와 안전 요건도 통합 텔레매틱스 플랫폼의 광범위한 채택을 촉진하고 있습니다. 시장은 차량, 인프라, 클라우드 기반 시스템 간의 원활한 데이터 교환을 가능하게 하는 커넥티비티 기술의 급속한 혁신의 혜택을 계속 누리고 있습니다. 교통 네트워크의 지능화가 진행되면서 텔레매틱스는 모빌리티 생태계의 기본 요소로 진화하고 있습니다. 실시간 인사이트, 예측 분석, 중앙 집중식 모니터링에 대한 관심이 높아짐에 따라 여러 산업 분야에서 수요가 증가하고 있습니다. 데이터 전송, 시스템 확장성, 플랫폼 통합의 지속적인 개선도 도입을 더욱 촉진하고 있습니다. 이러한 요소들이 결합되어 텔레매틱스 시스템은 전 세계 현대 교통, 물류 및 이동성 관리에 있어 중요한 기술로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 528억 달러 |

| 예측 금액 | 1,543억 달러 |

| CAGR | 11.5% |

커넥티드카의 보급 확대는 텔레매틱스 시스템 시장의 주요 성장 요인으로 작용하고 있습니다. 첨단 통신 프레임워크는 차량과 주변 환경과의 지속적인 상호 작용을 통해 운영 인텔리전스 및 의사결정을 향상시킬 수 있습니다. 전기 모빌리티의 급속한 확장은 차량 성능 모니터링을 지원하고 전체 사용자 경험을 향상시키기 위해 텔레매틱스 플랫폼에 대한 수요를 더욱 강화하고 있습니다. 클라우드 기반 아키텍처와 커넥티드 디바이스의 발전으로 데이터 정확도, 시스템 유연성, 확장성이 향상되어 전 세계 시장에서 새로운 성장 기회를 창출하고 있습니다.

2025년 기준, OEM 채널은 49.4%의 점유율을 차지했습니다. 이 부문은 강력한 통합 능력, 효율적인 공급 네트워크, 최종 사용자 요구 사항과의 긴밀한 협력의 이점을 가지고 있습니다. OEM은 전략적 제휴와 기술 통합을 통해 다양한 응용 분야에 걸쳐 확장성과 비용 효율성이 뛰어난 솔루션을 제공하는 데 유리한 위치에 있습니다.

자동차 분야는 2025년 28.5%의 점유율을 차지하며 주요 응용 분야로 부상했습니다. 이 분야의 성장은 차량 기술의 발전, 모빌리티 선호도 변화, 효율성, 안전성, 지속가능성에 대한 관심 증가에 힘입어 성장하고 있습니다. 자동차 이해관계자들은 차세대 모빌리티 솔루션을 제공하기 위해 혁신과 규제 대응에 대한 우선순위를 지속적으로 높이고 있습니다.

북미 텔레매틱스 시스템 시장은 2025년 32.5%의 점유율을 차지했습니다. 이 지역의 성장은 규제 준수 요건, 인프라 현대화 이니셔티브, 첨단 차량 기술의 급속한 보급에 의해 뒷받침되고 있습니다. 디지털로 관리되는 운송 서비스에 대한 수요 증가와 배출가스 감축 노력은 지역 전체 시장 확대를 지속적으로 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 커넥티드카에 수요 증가

- 플릿 관리에 대한 수요 증가

- 신코전기자동차 시장

- 비용 절감과 업무 효율화

- 정부 규제와 안전기준

- 업계의 잠재적 리스크&과제

- 데이터 보안에 관한 우려

- 초기 투자액이 높은

- 시장 기회

- 자율주행차와의 통합

- 스마트 시티 텔레매틱스

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 신흥 비즈니스 모델

- 컴플라이언스 요건

- 지속가능성 대책

- 소비자 심리분석

- 지정학적·무역 동향

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 시장 집중도 분석

- 주요 기업의 경쟁 벤치마킹

- 재무 실적 비교

- 매출

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 범위 폭

- 테크놀러지

- 혁신

- 지역별 사업 전개 비교

- 세계 전개 분석

- 서비스 네트워크 커버리지

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더 기업

- 챌린저

- 팔로워

- 니치 기업

- 전략적 전망 매트릭스

- 재무 실적 비교

- 주요 발전, 2022-2025

- 인수합병(M&A)

- 제휴 및 협력 관계

- 기술적 진보

- 확대와 투자 전략

- 지속가능성 이니셔티브

- 디지털 전환 대처

- 4.4.7 신흥/스타트업 경쟁사 동향

제5장 시장 추산·예측 : 제공별, 2022-2035

- 하드웨어

- 서비스

제6장 시장 추산·예측 : 기술별, 2022-2035

- GPS

- 셀룰러

- 위성

- Wi-Fi

- Bluetooth

제7장 시장 추산·예측 : 차종별, 2022-2035

- 이륜차

- 승용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

- OHV(Off-highway Vehicle)

제8장 시장 추산·예측 : 채널별, 2022-2035

- OEM(Original Equipment Manufacturers)

- 애프터마켓

제9장 시장 추산·예측 : 용도별, 2022-2035

- 플릿 관리

- 차량 추적

- 위성 내비게이션

- 차량 안전 통신

- 보험 텔레매틱스

- 인포테인먼트

- 리모트 진단

- 기타

제10장 시장 추산·예측 : 최종 이용 산업별, 2022-2035

- 자동차

- 운송 및 물류

- 보험

- 헬스케어

- 미디어 및 엔터테인먼트

- 정부 및 유틸리티

- 기타

제11장 시장 추산·예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 개요

- AT&T Inc.

- Continental AG

- Geotab Inc.

- Harman International Industries, Inc.(Samsung)

- HERE Technologies

- Intel Corporation

- Mix Telematics

- Octo Telematics

- PTC Inc.

- Robert Bosch GmbH

- Sierra Wireless

- Teletrac Navman

- TomTom International BV

- Trimble Inc.

- Verizon Connect(Verizon Communications Inc.)

The Global Telematics Systems Market was valued at USD 52.8 billion in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 154.3 billion by 2035.

Market growth is driven by rising demand for digital connectivity across vehicles and assets, increasing reliance on data-driven fleet operations, and the accelerating transition toward electric mobility. Organizations are prioritizing solutions that reduce operating expenses while improving visibility, safety, and efficiency. Regulatory frameworks and safety requirements are also encouraging broader adoption of integrated telematics platforms. The market continues to benefit from rapid innovation in connected technologies, which enable seamless data exchange between vehicles, infrastructure, and cloud-based systems. As transportation networks become more intelligent, telematics is evolving into a foundational component for mobility ecosystems. The growing focus on real-time insights, predictive analytics, and centralized monitoring is strengthening demand across multiple industries. Continuous improvements in data transmission, system scalability, and platform integration are further supporting adoption. These factors collectively position telematics systems as a critical technology for modern transportation, logistics, and mobility management worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $52.8 Billion |

| Forecast Value | $154.3 Billion |

| CAGR | 11.5% |

Rising adoption of connected vehicles remains a major growth catalyst for the telematics systems market. Advanced communication frameworks enable continuous interaction between vehicles and their surroundings, improving operational intelligence and decision-making. The rapid expansion of electric mobility is further strengthening demand, as telematics platforms support vehicle performance monitoring and enhance overall user experience. Progress in cloud-based architectures and connected devices is improving data accuracy, system flexibility, and scalability, creating new growth opportunities across global markets.

The original equipment manufacturer channel accounted for 49.4% share in 2025. This segment benefits from strong integration capabilities, efficient supply networks, and close alignment with end-user requirements. OEMs are well-positioned to deliver scalable and cost-effective solutions across diverse application areas through strategic alliances and technology integration.

The automotive sector held a 28.5% share in 2025, making it the leading application segment. Growth in this segment is supported by advancements in vehicle technology, evolving mobility preferences, and the increasing focus on efficiency, safety, and sustainability. Automotive stakeholders continue to prioritize innovation and regulatory alignment to deliver next-generation mobility solutions.

North America Telematics Systems Market accounted for 32.5% share in 2025. Regional growth is supported by regulatory compliance requirements, infrastructure modernization initiatives, and rapid adoption of advanced vehicle technologies. Rising demand for digitally managed transportation services and emission reduction efforts continues to reinforce market expansion across the region.

Key companies operating in the Global Telematics Systems Market include Geotab Inc., Trimble Inc., Verizon Connect, TomTom International BV, Continental AG, Robert Bosch GmbH, Harman International Industries, HERE Technologies, Mix Telematics, AT&T Inc., Octo Telematics, Intel Corporation, Teletrac Navman, PTC Inc., and Sierra Wireless. Companies in the Global Telematics Systems Market are strengthening their competitive position through continuous technology development and strategic expansion. Many players are investing in cloud-based platforms, advanced analytics, and artificial intelligence to enhance data accuracy and service reliability. Partnerships with automotive manufacturers, mobility providers, and enterprise customers support long-term revenue growth. Firms are also expanding their geographic presence and tailoring solutions to regional regulatory and operational requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot, 2022-2035

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Technology trends

- 2.2.3 Vehicle type trends

- 2.2.4 Channel trends

- 2.2.5 Application trends

- 2.2.6 End-use industry trends

- 2.2.7 Regional trends

- 2.3 TAM analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for connected vehicles

- 3.2.1.2 Increasing demand for fleet management

- 3.2.1.3 Emerging electric vehicle market

- 3.2.1.4 Cost reduction and operational efficiency

- 3.2.1.5 Government regulations and safety standards

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Data security concerns

- 3.2.2.2 High initial investment

- 3.2.3 Market Opportunities

- 3.2.3.1 Integration with autonomous vehicles

- 3.2.3.2 Telematics in smart cities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.11 Consumer sentiment analysis

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit Margin

- 4.3.1.3 R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1 Product Range Breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global Footprint Analysis

- 4.3.3.2 Service Network Coverage

- 4.3.3.3 Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.4.7 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Global Positioning System (GPS)

- 6.3 Cellular

- 6.4 Satellite

- 6.5 Wi-Fi

- 6.6 Bluetooth

Chapter 7 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Two-wheelers

- 7.3 Passenger Cars

- 7.4 Light Commercial Vehicles (LCVs)

- 7.5 Heavy Commercial Vehicles (HCVs)

- 7.6 Off-highway Vehicles

Chapter 8 Market Estimates and Forecast, By Channel, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Original Equipment Manufacturers (OEM)

- 8.3 Aftermarket

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Fleet Management

- 9.3 Vehicle Tracking

- 9.4 Satellite Navigation

- 9.5 Vehicle Safety Communication

- 9.6 Insurance Telematics

- 9.7 Infotainment

- 9.8 Remote Diagnostics

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Transportation and Logistics

- 10.4 Insurance

- 10.5 Healthcare

- 10.6 Media and Entertainment

- 10.7 Government and Utilities

- 10.8 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AT&T Inc.

- 12.2 Continental AG

- 12.3 Geotab Inc.

- 12.4 Harman International Industries, Inc. (Samsung)

- 12.5 HERE Technologies

- 12.6 Intel Corporation

- 12.7 Mix Telematics

- 12.8 Octo Telematics

- 12.9 PTC Inc.

- 12.10 Robert Bosch GmbH

- 12.11 Sierra Wireless

- 12.12 Teletrac Navman

- 12.13 TomTom International BV

- 12.14 Trimble Inc.

- 12.15 Verizon Connect (Verizon Communications Inc.)