|

시장보고서

상품코드

1936514

산업용 소각로 버너 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)Industrial Burner on Incineration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

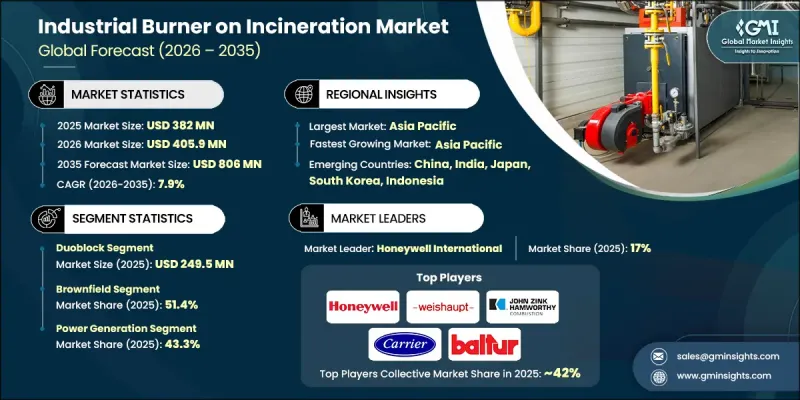

세계의 산업용 소각로 버너 시장은 2025년 3억 8,200만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.9%로 성장할 전망이며, 8억 600만 달러에 이를 것으로 예측됩니다.

이 시장 성장은 화학, 의료, 제조 분야에서 유해 폐기물 및 산업 폐기물 증가에 견인되고 있습니다. 이러한 폐기물에는 신뢰성이 높고 규제에 따른 처리 방법이 요구됩니다. 소각 시스템의 산업용 버너는 독성 화합물의 완전 연소를 보장하고 유해 배출을 최소화하기 위해 규제 준수 및 환경 보호에 매우 중요합니다. 폐기물 발생량 증가에 따라 소각로의 가동 시간이 연장되는 가운데 최적의 온도를 정밀하게 유지할 수 있는 내구성과 효율성이 우수한 버너 시스템에 대한 수요가 높아지고 있습니다. 현대 버너는 연소 공정에 뛰어난 제어성을 제공하여 안전성, 작동 신뢰성 및 배출 효율을 향상시킵니다. 폐기물 관리 시설 운영자는 규제 기준을 충족하면서 비용 효율적이고 신뢰할 수 있는 성능을 실현하기 위해 첨단 버너 솔루션에 대한 투자를 확대하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 3억 8,200만 달러 |

| 예측 금액 | 8억 600만 달러 |

| CAGR | 7.9% |

듀오 블록 버너 부문은 2025년에 2억 4,950만 달러를 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 7.4%를 나타낼 것으로 예측됩니다. 듀오 블록 설계는 버너와 팬을 단일 유닛에 통합하여 정확한 공기 및 연료 혼합, 안정된 화염 제어 및 고효율 연소를 보장합니다. 콤팩트한 구조로 설치 및 유지보수가 간소화되어 산업용 소각로, 유해 폐기물 처리 시설, 폐기물 발전 플랜트에 최적입니다. 산업 폐기물 증가 및 에너지 효율이 뛰어난 환경 규제에 적합한 솔루션에 대한 수요 증가가 지역에 관계없이 듀오 블록 버너의 도입을 촉진하고 있습니다.

발전 부문은 2025년에 43.3%의 점유율을 차지하였으며, 2026-2035년 CAGR 7.9%로 성장할 것으로 예측됩니다. 버너는 화력 발전소 및 폐기물 발전 시설에서 안정적인 화염 성능, 효율적인 열 발생 및 배출 가스 최소화를 보장하는 데 필수적입니다. 전력 수요 증가, 재생에너지 및 대체 에너지 시책의 확대, 엄격한 환경 규제가 고성능 버너의 도입을 촉진하고 있습니다. 고열 부하 하에서 지속적이고 신뢰할 수 있는 운전이 요구되기 때문에 산업용 버너는 에너지 생산에 필수적이며 발전 부문의 이점을 더욱 견고하게 만듭니다.

중국의 산업용 소각로 버너 시장은 2025년에 5,090만 달러에 이르렀으며, 2026-2035년 연평균 복합 성장률(CAGR) 8.3%를 나타낼 것으로 예측됩니다. 급속한 산업화, 도시 쓰레기 및 유해 폐기물 증가, 폐기물 에너지화 플랜트 및 화학 플랜트의 확장이 대용량 버너 수요를 견인하고 있습니다. 배출 규제와 효율적인 폐기물 관리를 촉진하는 정부 정책은 시장 보급을 더욱 강화하고 있습니다. 산업 분야에서는 신뢰성이 높고 고성능이며, 연속 운전하에서 복수의 연료 유형에 대응 가능한 버너가 요구되고 있습니다. 도시화 및 확대하는 도시 폐기물 처리 인프라도 중국의 지속적인 시장 성장에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 안전한 처분이 필요한 유해 폐기물 및 산업 폐기물 증가

- 산업 폐기물 및 도시 쓰레기로부터 에너지를 회수하는 시설 확대

- 폐기물 처리 및 배출 규제에 관한 환경 규제 강화

- 과제 및 어려움

- 첨단 저배출 버너 시스템의 높은 자본 비용

- 소각 시설에 대한 시민의 반대 및 규제 당국의 감시

- 기회

- 초저 NOx 및 고효율 버너 기술의 개발

- 갱신된 규제에 대응하기 위한 노후화한 소각로의 개수 수요

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 버너 설계별(2022-2035년)

- 모노 블록

- 듀오 블록

제6장 시장 추계 및 예측 : 설비별(2022-2035년)

- 기존 시설

- 신규 개발

제7장 시장 추계 및 예측 : 출력 범위별(2022-2035년)

- 300 kW 미만

- 300 kW-1 MW

- 1-5 MW

- 5-20MW

- 20-50MW

- 50 MW 이상

제8장 시장 추계 및 예측 : 최종 이용 산업별(2022-2035년)

- 발전

- 화학제품 및 석유화학제품

- 금속가공

- 식품가공

- 섬유산업

- 펄프 및 제지

- 기타

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제10장 기업 프로파일

- Alfa Laval

- Babcock Wanson

- Baltur

- Bloom Engineering Company

- Carrier

- Fives Group

- Forbes Marshall Pvt. Ltd.

- Honeywell International

- John Zink Hamworthy Combustion

- Limpsfield Combustion Engineering

- Max Weishaupt

- Miura America Co.

- Oilon Group Oy

- QED Combustion

- Selas Heat Technology Company

The Global Industrial Burner on Incineration Market was valued at USD 382 million in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 806 million by 2035.

The market growth is driven by rising volumes of hazardous and industrial waste across chemical, healthcare, and manufacturing sectors, which require reliable and compliant disposal methods. Industrial burners in incineration systems ensure complete combustion of toxic compounds and minimize harmful emissions, making them critical for regulatory compliance and environmental protection. As waste generation intensifies, operational hours for incinerators increase, creating demand for durable and efficient burner systems capable of maintaining optimal temperature with precision. Modern burners offer superior control over combustion processes, improving safety, operational reliability, and emission efficiency. Waste management facility operators are increasingly investing in advanced burner solutions to meet regulatory standards while achieving cost-effective and dependable performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $382 Million |

| Forecast Value | $806 Million |

| CAGR | 7.9% |

The duoblock burner segment accounted for USD 249.5 million in 2025 and is expected to grow at a CAGR of 7.4% through 2035. Duoblock designs integrate the burner and fan into a single unit, ensuring precise air-fuel mixing, stable flame control, and highly efficient combustion. Their compact construction simplifies installation and maintenance, making them ideal for industrial incinerators, hazardous waste treatment facilities, and waste-to-energy plants. Rising industrial waste volumes and the push for energy-efficient, environmentally compliant solutions are driving the adoption of duoblock burners across regions.

The power generation segment held a 43.3% share in 2025 and is projected to grow at a CAGR of 7.9% from 2026 to 2035. Burners are essential in thermal power plants and waste-to-energy facilities to ensure stable flame performance, efficient heat generation, and minimized emissions. Increasing electricity demand, growth in renewable and alternative energy initiatives, and stringent environmental regulations are fueling the adoption of high-performance burners. The requirement for continuous, reliable operation under high thermal loads makes industrial burners indispensable for energy production, reinforcing the dominance of the power generation segment.

China Industrial Burner on Incineration Market reached USD 50.9 million in 2025 and is expected to grow at a CAGR of 8.3% between 2026 and 2035. Rapid industrialization, increasing municipal and hazardous waste, and expansion of waste-to-energy and chemical plants are driving demand for high-capacity burners. Government policies promoting emission control and efficient waste management further support market adoption. Industrial sectors require burners that are reliable, high-performing, and capable of handling multiple fuel types under continuous operations. Urbanization and growing municipal waste treatment infrastructure also contribute to sustained market growth in China.

Key players in the Global Industrial Burner on Incineration Market include Babcock Wanson, Alfa Laval, Bloom Engineering Company, Selas Heat Technology Company, Carrier, Miura America Co., Fives Group, John Zink Hamworthy Combustion, Limpsfield Combustion Engineering, Honeywell International, Baltur, Forbes Marshall Pvt. Ltd., Max Weishaupt, Oilon Group Oy, and QED Combustion. Companies in the industrial burner on incineration market focus on strategies such as expanding regional distribution networks and increasing manufacturing capacities to meet growing demand. R&D investments enable the development of energy-efficient, low-emission burner systems with enhanced precision and durability. Strategic partnerships and collaborations with waste management operators and energy facilities strengthen market reach. Firms are integrating advanced combustion technologies and automated controls to optimize performance, reduce operational downtime, and comply with regulatory standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Burner design

- 2.2.3 Installation

- 2.2.4 Power Range

- 2.2.5 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising volumes of hazardous and industrial waste requiring safe disposal

- 3.2.1.2 Expansion of industrial and municipal waste-to-energy facilities

- 3.2.1.3 Stricter environmental regulations on waste treatment and emission control

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High capital cost of advanced low-emission burner systems

- 3.2.2.2 Public opposition and regulatory scrutiny toward incineration facilities

- 3.2.3 Opportunities

- 3.2.3.1 Development of ultra-low NOx and high-efficiency burner technologies

- 3.2.3.2 Retrofit demand for aging incinerators to meet updated regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Burner Design, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Monoblock

- 5.3 Duoblock

Chapter 6 Market Estimates & Forecast, By Installation, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Brownfield

- 6.3 Greenfield

Chapter 7 Market Estimates & Forecast, By Power Range, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 < 300 kW

- 7.3 300 kW - 1 MW

- 7.4 1 - 5 MW

- 7.5 5 - 20MW

- 7.6 20 - 50 MW

- 7.7 > 50 MW

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Power generation

- 8.3 Chemical and petrochemical

- 8.4 Metalworking

- 8.5 Food processing

- 8.6 Textile

- 8.7 Pulp and paper

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Alfa Laval

- 10.2 Babcock Wanson

- 10.3 Baltur

- 10.4 Bloom Engineering Company

- 10.5 Carrier

- 10.6 Fives Group

- 10.7 Forbes Marshall Pvt. Ltd.

- 10.8 Honeywell International

- 10.9 John Zink Hamworthy Combustion

- 10.10 Limpsfield Combustion Engineering

- 10.11 Max Weishaupt

- 10.12 Miura America Co.

- 10.13 Oilon Group Oy

- 10.14 QED Combustion

- 10.15 Selas Heat Technology Company