|

시장보고서

상품코드

1998656

산업용 버너 및 보일러 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Burner on Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

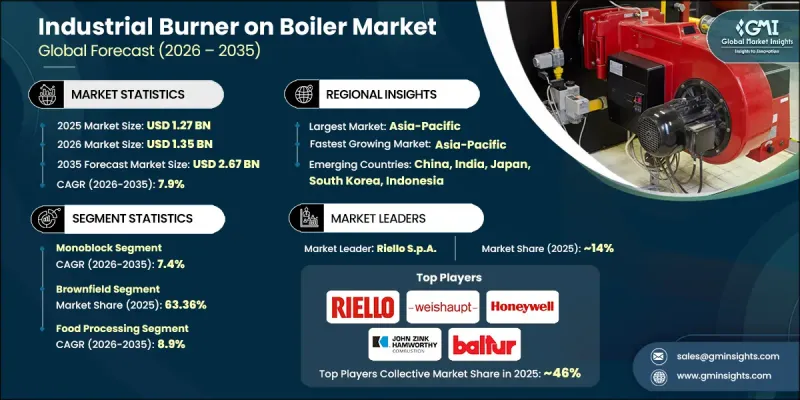

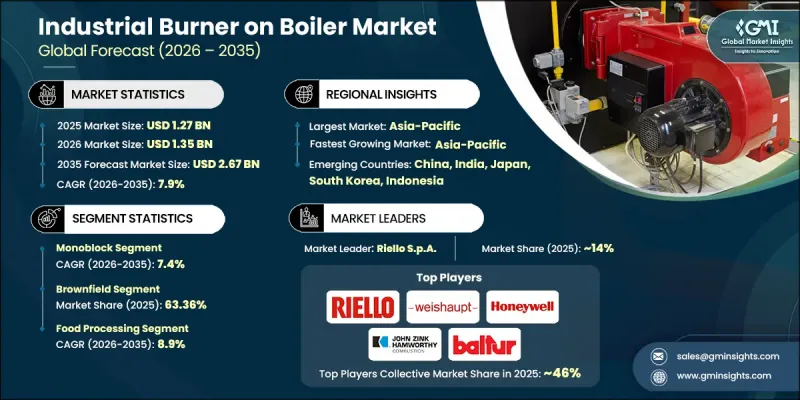

세계의 산업용 버너 및 보일러 시장은 2025년에 12억 7,000만 달러로 평가되었고, CAGR 7.9%로 성장하여 2035년까지 26억 7,000만 달러에 달할 것으로 예측됩니다.

산업 생산 증가와 제조 시설의 지속적인 확장으로 인해 신뢰할 수 있는 보일러 연소 시스템에 대한 수요가 증가하고 있습니다. 산업용 버너는 안정적이고 효율적인 열 발생을 보장하는 데 중요한 역할을 하며, 대규모 생산 환경에서 보일러의 성능을 일정하게 유지하는 데 중요한 역할을 합니다. 신뢰할 수 있는 연소 기술은 시설이 에너지 소비를 최적화하는 동시에 중단을 최소화하면서 공정의 연속적인 작동을 유지하는 데 도움이 됩니다. 에너지 효율 향상과 운영 비용 절감에 대한 압력이 높아지면서 산업 분야에서는 정밀한 연소 제어가 가능한 첨단 버너 기술을 도입하고 있습니다. 또한, 기존 보일러 인프라의 현대화로 인해 버너 시스템 및 관련 장비의 업그레이드에 대한 지속적인 수요가 발생하고 있습니다. 시설에서는 진화하는 환경 규제 기준을 준수하면서 정확한 온도 조절을 지원하는 솔루션을 찾는 움직임이 점점 더 강해지고 있습니다. 버너 설계의 지속적인 기술 발전은 연료 사용 효율 향상과 유지보수 수요 감소에 기여하고 있습니다. 산업 공정이 여전히 증기 및 열 발생에 크게 의존하고 있기 때문에 보일러 시스템에서 첨단 산업용 버너에 대한 수요는 세계 보일러 산업용 버너 시장의 장기적인 성장을 뒷받침하는 주요 원동력이 될 것입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 12억 7,000만 달러 |

| 예측액 | 26억 7,000만 달러 |

| CAGR | 7.9% |

모노블록 부문은 2025년 7억 2,350만 달러에 달했으며, 2026년부터 2035년까지 연평균 7.4%의 성장률을 보일 것으로 예측됩니다. 이 설계는 버너, 팬, 제어 장치와 같은 주요 연소 구성 요소를 하나의 컴팩트한 시스템에 통합하여 업계에서 널리 인정받고 있습니다. 이 통합된 구성은 일관된 공기와 연료의 혼합을 가능하게 하여 안정적인 연소 성능과 열효율 향상을 가져옵니다. 또한, 컴팩트한 구조로 설치 절차가 간소화되고 유지보수의 복잡성이 감소하여 다양한 산업용 난방 환경에서 매력적인 시스템입니다. 신뢰할 수 있는 성능과 높은 에너지 효율을 제공하는 공간 절약형 연소 기술에 대한 수요가 증가함에 따라 모노블록 버너의 도입이 계속 가속화되고 있습니다. 모노블록 버너는 조작의 용이성, 신뢰성 및 단순화된 유지보수 요구 사항으로 인해 전 세계 산업용 버너 및 보일러 산업에서 주요 설계 카테고리로 자리매김하고 있습니다.

브라운필드 분야는 2025년 63.36%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 7.1%의 성장률을 보일 것으로 전망됩니다. 브라운필드 설치가 시장을 주도하는 주요 요인은 전체 시스템을 교체하지 않고 기존 보일러 인프라를 업그레이드하고 현대화하려는 요구가 증가하고 있기 때문입니다. 기존 시설에 첨단 버너 기술을 통합함으로써 산업 분야에서는 연소 효율을 향상시키면서 배기가스 배출량을 줄일 수 있습니다. 이러한 접근 방식을 통해 기업은 장기적인 생산 중단과 과도한 설비 투자를 피하면서 운영 성과를 향상시킬 수 있습니다. 에너지 최적화, 규제 준수, 기존 산업 설비의 수명 연장에 대한 관심이 높아지면서 브라운필드 프로젝트에 대한 관심이 지속적으로 증가하고 있습니다. 이 설치 모델의 경제적 실용성과 운영상의 이점으로 인해 산업용 버너 및 보일러 시장에서 주류 접근 방식이 되었습니다.

중국의 산업용 버너 및 보일러 시장은 2025년 1억 7,900만 달러에 달할 것으로 예상되며, 2026년부터 2035년까지 연평균 8.1%의 성장률을 보일 것으로 예측됩니다. 활발한 산업 활동과 에너지 집약적 부문의 지속적인 확장은 이 나라가 시장을 선도하는 주요 요인으로 작용하고 있습니다. 대규모 산업 활동에서 에너지 수요가 증가함에 따라 신뢰할 수 있는 열 출력을 제공할 수 있는 효율적인 연소 기술에 대한 수요가 증가하고 있습니다. 산업 시설에서는 중단 없는 생산 사이클을 지원하기 위해 안정적인 화염 안정성, 정밀한 운전 제어 및 높은 열 성능을 갖춘 버너 시스템이 우선시됩니다. 대기 질과 배출가스 감소에 초점을 맞춘 정부 규제 또한 오염물질 배출을 억제하고 연료 효율을 향상시키도록 설계된 첨단 버너 기술의 도입을 촉진하고 있습니다. 또한, 산업 인프라에 대한 지속적인 투자와 보일러 시스템 현대화가 국내 생산 능력을 지속적으로 자극하고 있습니다. 자동 연소 관리 시스템 및 유연한 연료 운전과 같은 기술 발전은 아시아태평양의 보일러 산업용 버너 시장에서 중국의 선도적 지위를 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 버너 설계별, 2022-2035

제6장 시장 추산 및 예측 : 도입 형태별, 2022-2035

제7장 시장 추산 및 예측 : 출력대별, 2022-2035

제8장 시장 추산 및 예측 : 최종 이용 산업별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.23The Global Industrial Burner on Boiler Market was valued at USD 1.27 billion in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 2.67 billion by 2035.

Rising industrial production and the ongoing expansion of manufacturing facilities are creating strong demand for dependable boiler combustion systems. Industrial burners play a critical role in ensuring stable and efficient heat generation, enabling consistent boiler performance across large-scale production environments. Reliable combustion technology helps facilities optimize energy consumption while maintaining continuous process operations with minimal disruptions. Growing pressure to improve energy efficiency and reduce operational costs is encouraging industries to adopt advanced burner technologies capable of delivering precise combustion control. In addition, the modernization of existing boiler infrastructure is driving recurring demand for upgraded burner systems and related equipment. Facilities are increasingly seeking solutions that support accurate temperature regulation while aligning with evolving environmental compliance standards. Continuous technological improvements in burner design also enhance fuel utilization efficiency and reduce maintenance needs. As industrial processes continue to depend heavily on steam and heat generation, the need for advanced industrial burners in boiler systems will remain a major driver supporting the long-term growth of the global industrial burner on boiler market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.27 Billion |

| Forecast Value | $2.67 Billion |

| CAGR | 7.9% |

The monoblock segment reached USD 723.5 million in 2025 and is expected to grow at a CAGR of 7.4% from 2026 through 2035. This design has gained widespread industry acceptance because it integrates key combustion components, including the burner, fan, and control unit, into a single compact system. The unified configuration enables consistent air-fuel mixing, resulting in stable combustion performance and improved thermal efficiency. The compact structure also simplifies installation procedures and reduces servicing complexity, which makes the system attractive for a broad range of industrial heating environments. Demand for space-efficient combustion technologies that offer dependable performance and high energy efficiency continues to accelerate the adoption of monoblock burners. Their ease of operation, reliability, and streamlined maintenance requirements position them as a leading design category within the global industrial burner on boiler industry.

The brownfield segment accounted for 63.36% share in 2025 and is projected to grow at a CAGR of 7.1% from 2026 to 2035. Market leadership of brownfield installations is largely attributed to the rising need to upgrade and modernize existing boiler infrastructure without replacing entire systems. Integrating advanced burner technologies into existing facilities enables industries to enhance combustion efficiency while reducing emissions. This approach enables companies to enhance operational performance while avoiding extended production interruptions and excessive capital investment. Growing attention toward energy optimization, regulatory compliance, and extending the service life of existing industrial equipment continues to drive interest in brownfield projects. The economic practicality and operational advantages of this installation model make it the dominant approach within the industrial burner on boiler market.

China Industrial Burner on Boiler Market reached USD 179 million in 2025 and is expected to grow at a CAGR of 8.1% between 2026 and 2035. Strong industrial activity and continuous expansion of energy-intensive sectors are major contributors to the country's market leadership. Increasing energy requirements across large-scale industrial operations are generating higher demand for efficient combustion technologies capable of delivering reliable heat output. Industrial facilities prioritize burner systems that offer consistent flame stability, precise operational control, and high thermal performance to support uninterrupted production cycles. Government regulations focused on air quality and emission reduction are also encouraging the adoption of advanced burner technologies designed to limit pollutant output and improve fuel efficiency. Additionally, ongoing investments in industrial infrastructure and the modernization of boiler systems continue to stimulate domestic production capabilities. Technological advancements such as automated combustion management systems and flexible fuel operation are further strengthening China's leading position in the Asia Pacific industrial burner on boiler market.

Key companies participating in the Global Industrial Burner on Boiler Market include Alzeta Corporation, Andritz AG, Baltur, Bentone, Ebico, Fives Group, Honeywell International, John Zink Hamworthy Combustion, NIBE Group, Oilon Group Oy, Oxilon Pvt. Ltd., Riello S.p.A., Selas Heat Technology Company, Weishaupt GmbH, and Zeeco, Inc. Companies competing in the Global Industrial Burner on Boiler Market are focusing on multiple strategic initiatives to reinforce their competitive position and expand market reach. Manufacturers are prioritizing research and development activities to introduce advanced combustion technologies that improve efficiency, reduce emissions, and enhance operational reliability. Many companies are also strengthening their manufacturing capabilities and optimizing supply chains to address growing industrial demand. Strategic collaborations with industrial equipment providers and engineering firms help organizations develop tailored burner solutions that meet evolving operational requirements. In addition, businesses are expanding global distribution networks and strengthening after-sales service capabilities to improve customer engagement and long-term client retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Burner design

- 2.2.3 Installation

- 2.2.4 Power Range

- 2.2.5 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for steam and heat in process industries

- 3.2.1.2 Expansion of power generation and cogeneration facilities

- 3.2.1.3 Growth of food processing, chemicals, and pulp and paper industries

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High capital cost of advanced low-NOx burner systems

- 3.2.2.2 Complex integration with existing boiler and control systems

- 3.2.3 Opportunities

- 3.2.3.1 Rising adoption of dual-fuel and multi-fuel burner technologies

- 3.2.3.2 Integration of digital controls and automation in burner management systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Burner Design, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Monoblock

- 5.3 Duoblock

Chapter 6 Market Estimates & Forecast, By Installation, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Brownfield

- 6.3 Greenfield

Chapter 7 Market Estimates & Forecast, By Power Range, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 < 300 kW

- 7.3 300 kW - 1 MW

- 7.4 1 - 5 MW

- 7.5 5 - 20MW

- 7.6 20 - 50 MW

- 7.7 > 50 MW

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Power generation

- 8.3 Chemical and petrochemical

- 8.4 Metalworking

- 8.5 Food processing

- 8.6 Textile

- 8.7 Pulp and paper

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Alzeta Corporation

- 10.2 Andritz AG

- 10.3 Baltur

- 10.4 Bentone

- 10.5 Ebico

- 10.6 Fives Group

- 10.7 Honeywell International

- 10.8 John Zink Hamworthy Combustion

- 10.9 NIBE Group

- 10.10 Oilon Group Oy

- 10.11 Oxilon Pvt. Ltd.

- 10.12 Riello S.p.A.

- 10.13 Selas Heat Technology Company

- 10.14 Weishaupt GmbH

- 10.15 Zeeco, Inc.