|

시장보고서

상품코드

1936628

선박용 추진 엔진 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Marine Propulsion Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

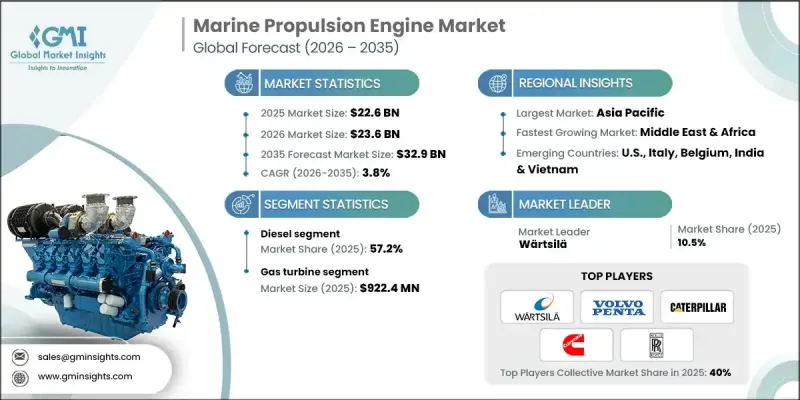

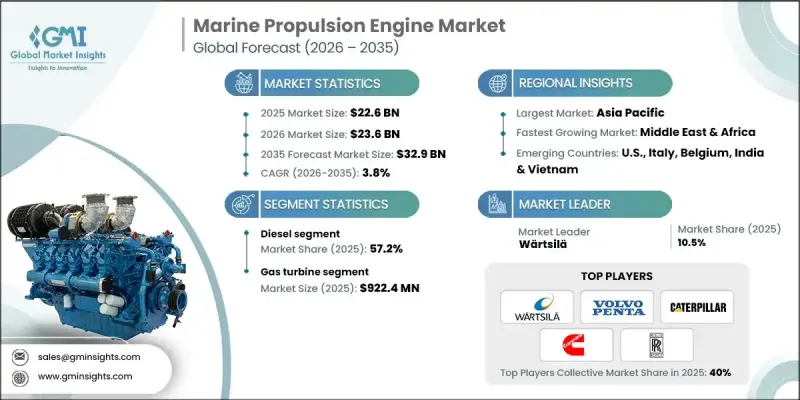

세계의 선박용 추진 엔진 시장은 2025년에 226억 달러로 평가되었으며, 2035년까지 CAGR 3.8%로 성장하여 329억 달러에 달할 것으로 예측됩니다.

시장 성장은 전 세계적으로 해상 운항 전반에 걸쳐 배출량 감축을 위한 노력이 강화되면서 선단 운영자들은 장기적인 규제 대응을 위해 추진 기술을 재평가해야 하는 상황에 직면해 있습니다. 수요는 신뢰성과 출력 성능을 유지하면서 대체 연료 및 저탄소 연료로 구동할 수 있는 보다 깨끗하고 효율적인 추진 시스템으로 전환되고 있습니다. 선박 추진 엔진은 통합된 추진 구성요소를 통해 에너지를 제어된 운동으로 변환하여 선박의 이동에 필요한 추력을 생성하는 핵심 기계 시스템 역할을 합니다. 세계 무역량의 증가와 항로 연장으로 인해 더 높은 내구성, 효율성, 성능 안정성을 실현하는 엔진의 필요성이 높아지고 있습니다. 상업, 해양, 정부 부문의 노후화된 선박을 대상으로 하는 선대 갱신 프로그램이 디지털 기술이 적용된 추진 플랫폼에 대한 투자를 촉진하고 있습니다. 가동시간과 수명주기 효율성을 향상시키기 위해 실시간 모니터링, 데이터 분석, 예지보전 기능을 통합한 지능형 엔진 아키텍처가 점점 더 우선순위가 높아지고 있습니다. 선주들은 또한 내구성과 운영 안정성을 손상시키지 않으면서도 연료 적응성을 지원하는 유연한 추진 구성을 선호합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 226억 달러 |

| 예측 금액 | 329억 달러 |

| CAGR | 3.8% |

풍력 및 태양광 기반 선박 추진 엔진 부문은 2035년까지 15억 달러에 달할 것으로 예상됩니다. 재생에너지와 선내 에너지 저장 및 제어 시스템을 결합한 하이브리드 추진 아키텍처는 수요가 적은 운항 조건에서 연료 사용을 최적화하고자 하는 사업자들의 주목을 받고 있습니다. 고급 에너지 관리 프레임워크는 부하 분산 및 배출 성능을 향상시키는 동시에 보다 효율적인 항해 계획을 지원합니다.

연료전지 선박 추진 엔진 부문은 2025년 3.9%의 점유율을 차지했습니다. 선박 운항 사업자들이 진화하는 환경 규제에 따라 무공해 추진 옵션을 추구함에 따라 점차적으로 채택이 증가하고 있습니다. 확장 가능한 시스템 설계와 모듈식 통합 접근 방식을 통해 운영상의 중복성과 다양한 선박 요구사항에 대한 적응성을 보장하면서 단계적 도입이 가능합니다.

미국 선박 추진 엔진 시장은 2025년 68.6%의 점유율을 차지하며 22억 달러 규모에 달할 것으로 예상됩니다. 이러한 성장은 연안 운송, 내륙수로, 해양 작업을 포함한 국내 해양 활동의 증가에 힘입어 효율적이고 고성능 추진 시스템에 대한 수요를 견인하고 있습니다. 특히 상선 및 해군 함정용 조선 분야에 대한 대규모 투자가 시장 확대를 더욱 촉진하고 있습니다. 신규 건조 선박에 저배출, 디지털 기술이 적용된 엔진이 점점 더 많이 채택되고 있기 때문입니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 제품별, 2022-2035

제6장 시장 규모 및 예측 : 지역별, 2022-2035

제7장 기업 개요

KSM 26.03.05The Global Marine Propulsion Engine Market was valued at USD 22.6 billion in 2025 and is estimated to grow at a CAGR of 3.8% to reach USD 32.9 billion by 2035.

Market growth is shaped by the intensifying global push to lower emissions across maritime operations, prompting fleet operators to reassess propulsion technologies for long-term regulatory alignment. Demand is shifting toward cleaner, more efficient propulsion systems capable of operating on alternative and low-carbon fuels while maintaining reliability and power output. Marine propulsion engines serve as the core mechanical systems that generate thrust for vessel movement by converting energy into controlled motion through integrated propulsion components. Rising global trade volumes and extended shipping routes are reinforcing the need for engines that deliver greater endurance, efficiency, and performance consistency. Fleet renewal programs targeting aging vessels across commercial, offshore, and government segments are driving investment in digitally advanced propulsion platforms. Intelligent engine architectures that incorporate real-time monitoring, data analytics, and predictive maintenance capabilities are increasingly prioritized to improve uptime and lifecycle efficiency. Shipowners are also favoring flexible propulsion configurations that support fuel adaptability without compromising durability or operational stability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.6 Billion |

| Forecast Value | $32.9 Billion |

| CAGR | 3.8% |

The wind and solar-based marine propulsion engine segment is projected to reach USD 1.5 billion by 2035. Hybridized propulsion architectures that combine renewable inputs with onboard energy storage and control systems are gaining traction as operators seek to optimize fuel usage during low-demand operating conditions. Advanced energy management frameworks are improving load balancing and emissions performance while supporting more efficient voyage planning.

The fuel cell-based marine propulsion engines segment accounted for a 3.9% share in 2025. Adoption is gradually increasing as vessel operators pursue zero-emission propulsion options aligned with evolving environmental mandates. Scalable system designs and modular integration approaches are enabling gradual deployment while ensuring operational redundancy and adaptability to different vessel requirements.

United States Marine Propulsion Engine Market held a 68.6% share in 2025, generating USD 2.2 billion. This growth is being fueled by increasing domestic maritime activity, including coastal shipping, inland waterways, and offshore operations, which are driving demand for efficient, high-performance propulsion systems. Substantial investments in shipbuilding, particularly for commercial and naval fleets, are further bolstering market expansion, as new vessels are increasingly being equipped with low-emission, digitally enabled engines.

Key participants active in the Global Marine Propulsion Engine Market include Wartsila, Caterpillar, Rolls-Royce, Yanmar Marine International, Cummins, AB Volvo Penta, Mitsubishi Heavy Industries, Scania, Deutz AG, HD Hyundai Heavy Industries Engine & Machinery, Yamaha Motor, Perkins Engines, Anglo Belgian Corporation, Vetus, Nanni, Masson Marine, Ingeteam, Steyr, Deere & Company, and Isuzu Motors Engine Sales. These companies maintain competitive positioning through innovation, portfolio diversification, and global service networks. To strengthen their foothold in pharmaceutical and healthcare-related marine applications, propulsion engine manufacturers are prioritizing reliability, precision control, and low-emission performance. Companies are developing propulsion solutions optimized for vessels supporting medical logistics, offshore healthcare access, and temperature-sensitive cargo transport. Strategic investments focus on noise reduction, vibration control, and stable power delivery to protect sensitive onboard equipment. Manufacturers are also expanding service agreements and remote diagnostics to ensure uninterrupted operations in critical missions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of marine propulsion engine

- 3.8 Price trend analysis

- 3.8.1 By product

- 3.8.2 By region

- 3.9 Emerging opportunities & trends

- 3.10 Digitalization and IoT integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Wind & solar

- 5.4 Gas turbine

- 5.5 Fuel cell

- 5.6 Steam turbine

- 5.7 Natural gas

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 Italy

- 6.3.4 France

- 6.3.5 Russia

- 6.3.6 Denmark

- 6.3.7 Netherlands

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.4.6 Vietnam

- 6.4.7 Singapore

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 Iran

- 6.5.4 Angola

- 6.5.5 Egypt

- 6.5.6 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

- 6.6.3 Mexico

Chapter 7 Company Profiles

- 7.1 AB Volvo Penta

- 7.2 Anglo Belgian Corporation

- 7.3 Caterpillar

- 7.4 Cummins

- 7.5 Deere & Company

- 7.6 Deutz AG

- 7.7 HD Hyundai Heavy Industries Engine & Machinery

- 7.8 Ingeteam

- 7.9 Isuzu Motors Engine Sales

- 7.10 Masson Marine

- 7.11 Mitsubishi Heavy Industries

- 7.12 Nanni

- 7.13 Perkins Engines

- 7.14 Rolls-Royce

- 7.15 Scania

- 7.16 Steyr

- 7.17 Vetus

- 7.18 Wartsila

- 7.19 Yamaha Motor

- 7.20 Yanmar Marine International