|

시장보고서

상품코드

1959294

식품 폐기물 유래 식물성 착색료 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Plant-based Colors from Food Waste Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

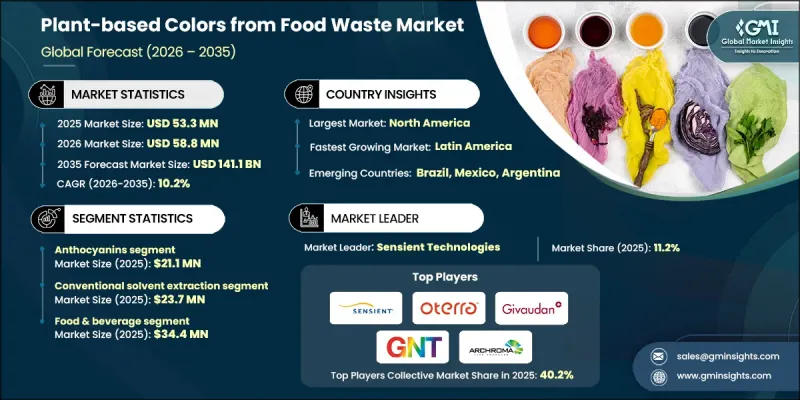

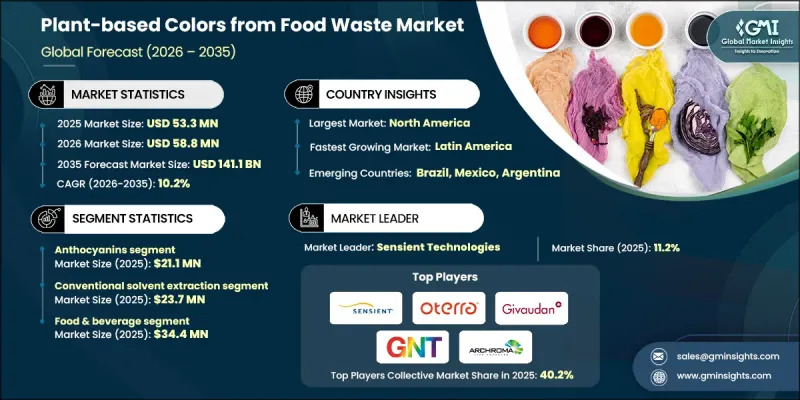

식품 폐기물 유래 식물성 착색료 세계 시장은 2025년에 5,330만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.2%로 성장하여 1억 4,110만 달러에 이를 것으로 예측됩니다.

본 시장은 식품 가공 및 수확 후 처리 과정에서 발생하는 폐식물 원료에서 회수되는 천연 색소에 초점을 맞추었습니다. 이러한 착색제는 충분히 활용되지 않은 식물 성분에서 추출되어 다양한 산업에서 상업적으로 이용 가능한 원료로 전환됩니다. 주요 색소군에는 안토시아닌, 카로티노이드, 엽록소, 베타레인 등이 포함되며, 색조의 강도와 기능적 안정성을 유지하도록 설계된 특수 가공 기술을 통해 회수됩니다. 식물 유래 폐기물 스트림을 천연 착색 솔루션으로 전환하는 것은 매립지 부담을 줄이고 합성 염료에 대한 의존도를 낮춤으로써 순환 경제 목표를 달성하는 데 도움이 됩니다. 환경적 이점 외에도 이러한 색소에는 항산화 및 항균 작용을 하는 생리활성 화합물이 포함되어 있는 경우가 많아 그 가치 제안이 더욱 강화됩니다. 이러한 접근 방식은 자원 효율성을 향상시키는 동시에 농업 및 식품 가공 산업에 새로운 수익원을 창출할 수 있습니다. 투명성, 클린 라벨, 무독성 성분에 대한 소비자 수요가 증가함에 따라 식품, 섬유, 화장품, 포장재 등 다양한 분야에서 채택이 가속화되고 있습니다. 지속가능성이 브랜드 아이덴티티의 핵심으로 떠오르면서 음식물 쓰레기에서 추출한 식물성 색소는 전 세계 공급망에서 전략적 중요성을 더해가고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 5,330만 달러 |

| 예측 금액 | 1억 4,110만 달러 |

| CAGR | 10.2% |

음식물 쓰레기에서 추출한 천연 색소는 소비자들이 인공 염료를 대체할 수 있는 친환경적이고 생분해성 있는 대안을 찾으면서 점점 더 선호되고 있습니다. 클린 라벨 포지셔닝, 합성첨가물 규제 완화, 제품 안전에 대한 인식이 높아지면서 이러한 전환이 가속화되고 있습니다. 기존의 합성 착색제와 달리 식물 유래 색소는 친환경 브랜딩과 건강 지향적 구매 행동에 부합합니다. 재생 가능한 원료와 환경 부하 감소로 인해 지속 가능한 혁신에 집중하는 제조업체에게 매력적인 선택이 되고 있습니다.

기존 용매 추출 부문은 2025년 2,370만 달러를 차지할 것으로 예측됩니다. 이 방법은 조작의 편리성, 비용 효율성, 상대적으로 낮은 자본 요구 사항으로 인해 여전히 널리 사용되고 있습니다. 특히 인프라 제약이 기술 도입에 영향을 미치는 신흥 시장에서 대규모 색소 회수를 지속적으로 지원하고 있습니다. 그러나 업계 관계자들은 색소의 품질과 안정성을 유지하면서 수율 효율을 높이고, 용매 잔류물을 줄이며, 환경에 미치는 영향을 최소화하기 위해 첨단 추출 방법에 대한 평가를 강화하고 있습니다.

식음료 부문은 2025년 3,440만 달러의 매출을 기록했습니다. 이 분야의 견조한 성장은 원료의 투명성과 추적 가능한 조달에 대한 소비자 수요에 의해 주도되고 있습니다. 제조업체들은 합성 대체품을 대체하고 규제 기준을 충족하기 위해 식품 폐기물에서 추출한 식물성 색소를 제품 배합에 통합하고 있습니다. 이 천연 색소는 음료, 유제품, 스낵, 과자류에 생생한 시각적 매력을 제공하는 동시에 지속가능성을 강조할 수 있도록 도와줍니다. 브랜드가 책임감 있는 조달과 깨끗한 배합을 중시하는 가운데, 식음료 업계 수요는 계속 견고하게 유지되고 있습니다.

북미의 음식물 쓰레기 유래 식물성 색소 시장은 2025년 2,200만 달러에서 2035년까지 5,080만 달러로 성장할 것으로 예측됩니다. 이러한 지역적 확장은 천연 성분에 대한 소비자의 인식이 높아지고 환경 관리에 대한 업계의 강력한 노력에 의해 뒷받침되고 있습니다. 식품, 음료, 화장품 제조업체들은 순환형 생산 목표를 추진하기 위해 농산물별 고부가가치 색소로 전환하는 기술에 투자하고 있습니다. 합성첨가물 사용을 줄이기 위한 규제 노력은 시장 성장을 더욱 촉진하고 있습니다. 북미는 탄탄한 공급망과 혁신 주도형 비즈니스 모델을 통해 세계 매출 성장에 기여하는 주요 지역으로 자리매김하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 색소 유형별, 2022-2035년

제6장 시장 추산·예측 : 추출 기술별, 2022-2035년

제7장 시장 추산·예측 : 용도별, 2022-2035년

제8장 시장 추산·예측 : 지역별, 2022-2035년

제9장 기업 개요

LSH 26.03.26The Global Plant-based Colors from Food Waste Market was valued at USD 53.3 million in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 141.1 million by 2035.

The market focuses on natural pigments recovered from discarded plant materials generated during food processing and post-harvest handling. These colorants are extracted from underutilized plant fractions and transformed into commercially viable ingredients for multiple industries. Key pigment groups include anthocyanins, carotenoids, chlorophylls, and betalains, which are recovered through specialized processing techniques designed to preserve color intensity and functional stability. Converting plant-based waste streams into natural color solutions supports circular economy objectives by reducing landfill burden and lowering reliance on synthetic dyes. In addition to environmental benefits, these pigments often contain bioactive compounds with antioxidant and antimicrobial properties, enhancing their value proposition. The approach creates new revenue channels for agricultural and food-processing industries while improving resource efficiency. Rising consumer demand for transparency, clean-label formulations, and non-toxic ingredients is accelerating adoption across food, textile, cosmetic, and packaging applications. As sustainability becomes central to brand identity, plant-based colors sourced from food waste are gaining strategic importance in global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.3 Million |

| Forecast Value | $141.1 Million |

| CAGR | 10.2% |

Natural pigments derived from food waste are increasingly preferred as consumers seek environmentally responsible and biodegradable alternatives to artificial dyes. Clean-label positioning, regulatory shifts away from synthetic additives, and growing awareness of product safety are reinforcing this transition. Unlike conventional synthetic colorants, plant-based pigments align with eco-conscious branding and wellness-driven purchasing behavior. Their renewable origin and reduced environmental footprint make them attractive to manufacturers focused on sustainable innovation.

The conventional solvent extraction segment accounted for USD 23.7 million in 2025. This method remains widely utilized due to its operational simplicity, cost-effectiveness, and relatively low capital requirements. It continues to support large-scale pigment recovery, particularly in emerging markets where infrastructure constraints influence technology adoption. However, industry participants are increasingly evaluating advanced extraction approaches to improve yield efficiency, reduce solvent residues, and minimize environmental impact while maintaining pigment quality and stability.

The food & beverage segment generated USD 34.4 million in 2025. Strong growth in this sector is driven by consumer demand for ingredient transparency and traceable sourcing. Manufacturers are incorporating food waste-derived plant-based colors into product formulations to replace synthetic alternatives and meet regulatory standards. These natural pigments deliver vibrant visual appeal across beverages, dairy products, snacks, and confectionery applications while reinforcing sustainability narratives. As brands emphasize responsible sourcing and cleaner formulations, demand within the food and beverage industry continues to strengthen.

North America Plant-based Colors from Food Waste Market is projected to grow from USD 22 million in 2025 to USD 50.8 million by 2035. Regional expansion is supported by heightened consumer awareness regarding natural ingredients and strong industry commitment to environmental stewardship. Food, beverage, and cosmetic manufacturers are investing in technologies that convert agricultural by-products into high-value pigments to advance circular production goals. Regulatory initiatives aimed at reducing synthetic additive usage further stimulate market growth. Established supply chains and innovation-driven business models position North America as a key contributor to global revenue expansion.

Major companies operating in the Global Plant-based Colors from Food Waste Market include GNT Group, Sensient Technologies Corporation, Chr. Hansen Holdings (Oterra), Givaudan SA, Givaudan Sense Colour, Archroma (EarthColors), Prodalim (Upcycled Colors), E. & J. Gallo Winery (Natural Colorants Division), and KAIKU (UK). These organizations are actively developing advanced pigment extraction technologies and expanding sustainable ingredient portfolios to strengthen their competitive presence. Companies in the plant-based colors from food waste market are reinforcing their market position through investment in research and development to improve pigment stability, color intensity, and application versatility. Strategic collaborations with food processors and agricultural suppliers secure consistent raw material streams and enhance traceability. Many firms are adopting proprietary extraction technologies that increase yield efficiency while reducing environmental impact. Sustainability certifications and transparent sourcing practices are being leveraged to build brand credibility and consumer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Pigment Type

- 2.2.2 Extraction Technology

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for natural colors

- 3.2.1.2 Expansion of plant-based and clean-label products

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Competitive pressure from synthetic colors

- 3.2.3 Market opportunities

- 3.2.3.1 Integration into cosmetic and pharmaceutical industries

- 3.2.3.2 Collaborations with food processing companies

- 3.2.3.3 Innovation in functional colors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Pigment type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Pigment Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Anthocyanins

- 5.3 Betalains

- 5.4 Carotenoids

- 5.5 Chlorophylls

- 5.6 Phycobiliproteins

Chapter 6 Market Estimates and Forecast, By Extraction Technology, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional solvent extraction

- 6.3 Ultrasound-assisted extraction (UAE)

- 6.4 Microwave-assisted extraction (MAE)

- 6.5 Supercritical fluid extraction (SFE)

- 6.6 Enzyme-assisted extraction (EAE)

- 6.7 Pulsed electric field (PEF)

- 6.8 Pressurized liquid extraction (PLE)

- 6.9 Precision fermentation & biotechnology

- 6.10 Hybrid & integrated extraction systems

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Cosmetics & personal care

- 7.4 Textile & fashion

- 7.5 Pharmaceutical & nutraceutical

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Sensient Technologies Corporation

- 9.2 Chr. Hansen Holdings (Oterra)

- 9.3 Givaudan SA

- 9.4 Givaudan Sense Colour

- 9.5 GNT Group

- 9.6 Archroma (EarthColors)

- 9.7 Prodalim (Upcycled Colors)

- 9.8 E. & J. Gallo Winery (Natural Colorants Division)

- 9.9 KAIKU (UK)