|

시장보고서

상품코드

1959623

반려동물 사료 포장 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Pet Food Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

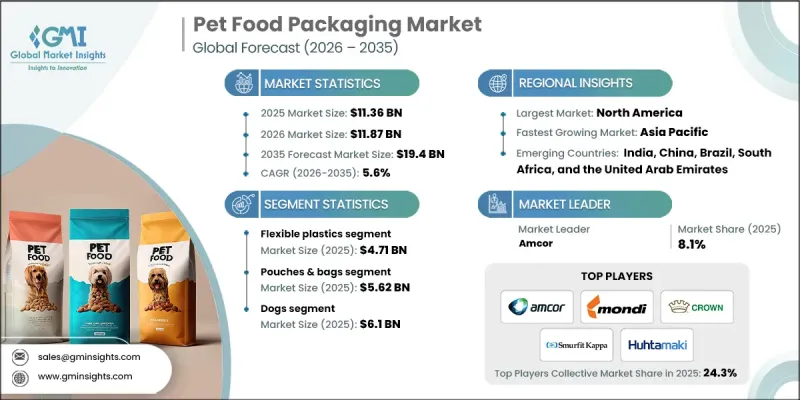

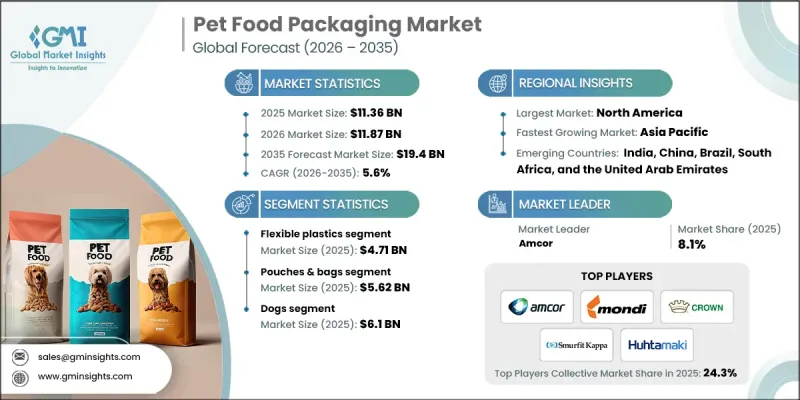

세계의 반려동물 사료 포장 시장은 2025년에 113억 6,000만 달러로 평가되었고, 2035년에는 CAGR 5.6%로 성장하여 194억 달러에 이를 것으로 예측됩니다.

반려동물을 키우는 인구가 증가함에 따라 반려동물사료에 대한 수요가 증가하면서 시장은 꾸준히 확대되고 있습니다. 프리미엄 제품, 유기농 제품, 조리된 반려동물사료에 대한 소비자 선호도가 높아지면서 신선도, 안전성, 편의성을 보장하는 첨단 패키징에 대한 수요가 증가하고 있습니다. 전자상거래 및 온라인 소매 채널의 급속한 성장으로 인해 내구성이 뛰어나고 가볍고 운반하기 쉬운 포장에 대한 요구가 증가하고 있습니다. 지속가능성이 주요 요소로 떠오르면서 순환 경제의 목표를 달성하기 위해 점점 더 많은 브랜드가 재활용 가능, 생분해성, 단일 소재의 포장 솔루션을 찾고 있습니다. 또한, 지속 가능한 소재를 지원하는 규제 프레임워크가 진화하는 한편, 프리미엄화 추세는 의식 있는 반려동물 소유자에게 어필할 수 있는 혁신적인 디자인을 촉진하고 있으며, 시장은 전 세계적으로 경쟁이 치열하고 혁신이 주도하는 시장으로 변모하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 113억 6,000만 달러 |

| 예측 금액 | 194억 달러 |

| CAGR | 5.6% |

플렉서블 플라스틱 부문은 2025년 47억 1,000만 달러에 달할 것으로 예측됩니다. 식품 접촉 물질에 대한 규제가 강화되고 순환 경제에 대한 관심이 높아지면서 재생 가능한 플렉서블 플라스틱에 대한 수요가 증가하고 있습니다. 제조업체들은 진화하는 EU의 재활용 기준을 충족시키면서 환경에 민감한 소비자들에게 어필할 수 있는 재생 및 단일 소재의 연질 플라스틱 생산에 주력하고 있습니다. 유연성 포장은 내구성, 경량성, 장기 보존성을 제공하기 때문에 건식, 습식, 반습식 펫푸드 제품에 가장 적합합니다. 기업은 지속 가능한 방식을 채택함으로써 규제 준수와 환경 친화적인 고객층에 대한 브랜드 이미지 강화를 동시에 달성할 수 있습니다.

파우치 및 가방 부문은 2025년 56억 2,000만 달러에 달했습니다. 단일 소재의 재활용 가능한 파우치로의 전환은 재활용 가능성에 대한 규제 압력과 친환경 포장에 대한 소비자 수요에 의해 추진되고 있습니다. 기업들은 법적 재활용 기준을 충족하고 폐기물을 줄이는 단일 소재의 대체품으로 다재다능한 필름을 대체하고 있습니다. 재밀봉이 가능한 1회용 파우치에 대한 수요 증가는 소비자의 편의성, 전자상거래 배송, 용량 관리의 니즈와 맞물려 경쟁에서 차별화를 꾀하는 펫푸드 브랜드에게 점점 더 매력적으로 다가오고 있습니다.

북미 반려동물 사료 포장 시장은 2025년 41.6%의 점유율을 차지했습니다. 이 지역에서는 편의성, 프리미엄화, 지속 가능한 포장에 대한 소비자 수요로 인해 강력한 성장세를 보이고 있습니다. 바쁜 라이프 스타일과 온라인 판매에 대응하기 위해 재밀봉이 가능한 봉지, 1회용 파우치, 배송이 용이한 형태가 표준화되고 있습니다. 품질과 신선함을 전달하는 대담하고 눈길을 끄는 디자인은 매장에서 제품 차별화를 위해 점점 더 많이 활용되고 있습니다. 지속가능성에 대한 인식이 높아지는 가운데, 생산자 책임 규제와 재활용 의무가 확대되면서 포장재 선택에 영향을 미치고 있습니다. 그 결과, 기업들은 규제 기준과 소비자 기대치를 모두 충족시키기 위해 시각적 매력과 기능성을 유지하면서 환경 친화적인 솔루션을 채택하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별, 2022-2035

제6장 시장 추산 및 예측 : 포장 형태별, 2022-2035

제7장 시장 추산 및 예측 : 반려동물 사료 유형별, 2022-2035

제8장 시장 추산 및 예측 : 반려동물 유형별, 2022-2035

제9장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.03.16The Global Pet Food Packaging Market was valued at USD 11.36 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 19.4 billion in 2035.

The market is expanding steadily as rising pet adoption and ownership drive higher demand for pet food products. Increasing consumer preference for premium, organic, and ready-to-eat pet foods is fueling demand for advanced packaging solutions that ensure freshness, safety, and convenience. The rapid growth of e-commerce and online retail channels has amplified the need for packaging that is durable, lightweight, and easy to ship. Sustainability is becoming a major factor, with brands seeking recyclable, biodegradable, and mono-material packaging solutions to meet circular economy goals. Additionally, regulatory frameworks are evolving to support sustainable materials, while premiumization trends encourage innovative designs that appeal to conscious pet owners, making the market highly competitive and innovation-driven globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.36 Billion |

| Forecast Value | $19.4 Billion |

| CAGR | 5.6% |

The flexible plastics segment reached USD 4.71 billion in 2025. Demand for recyclable flexible plastics is rising as governments implement stricter regulations for food-contact materials and circular economy compliance. Manufacturers are increasingly focusing on producing recycled and mono-material flexible plastics that meet evolving EU recyclability standards while appealing to sustainability-conscious consumers. Flexible packaging provides durability, lightweight handling, and extended shelf life, making it ideal for dry, wet, and semi-moist pet food products. By adopting sustainable practices, companies can both comply with regulations and strengthen brand perception among environmentally aware customers.

The pouches and bags segment reached USD 5.62 billion in 2025. The shift toward mono-material recyclable pouches is driven by regulatory pressure on recyclability and consumer demand for environmentally responsible packaging. Companies are replacing multi-material films with single-material alternatives that satisfy legal recycling thresholds and reduce waste. The growing preference for resealable and single-serve pouches aligns with consumer convenience, e-commerce delivery, and portion control needs, making this format increasingly attractive to pet food brands seeking competitive differentiation.

North America Pet Food Packaging Market accounted for 41.6% share in 2025. The region is witnessing strong growth due to consumer demand for convenience, premiumization, and sustainable packaging. Resealable bags, single-serve pouches, and easy-to-ship formats are becoming standard to accommodate busy lifestyles and online sales. Bold, eye-catching designs that convey quality and freshness are increasingly used to differentiate products on shelves. Awareness of sustainability is rising, with extended producer responsibility regulations and recyclability mandates shaping packaging choices. As a result, companies are adopting eco-friendly solutions while maintaining visual appeal and functionality to satisfy both regulatory standards and consumer expectations.

Key players operating in the Global Pet Food Packaging Market include Huhtamaki, Amcor, Ball Corporation, Mondi, Sealed Air, Crown Holdings, Smurfit Kappa, ProAmpac, Constantia Flexibles, Tetra Pak, Coveris, Winpak, and Packaging Corporation of America. Companies in the pet food packaging market are adopting several strategies to enhance their market presence and strengthen their foothold. They are investing heavily in research and development to create sustainable, recyclable, and biodegradable packaging that meets evolving regulatory standards. Partnerships with pet food manufacturers and converters enable tailored solutions and faster adoption of innovative formats. Companies are also expanding production capacities and distribution networks to ensure timely supply to e-commerce and retail channels. Brand differentiation is achieved through high-quality, visually appealing designs that communicate freshness and premium value.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Pet food type trends

- 2.2.4 Pet type trends

- 2.2.5 Distribution channel trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet adoption and ownership

- 3.2.1.2 Increasing demand for premium and organic pet food

- 3.2.1.3 Growing e-commerce and online retail channels

- 3.2.1.4 Innovations in sustainable and eco-friendly packaging

- 3.2.1.5 Expansion of ready-to-eat and convenient pet food products

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High cost of advanced packaging materials

- 3.2.2.2 Stringent regulatory standards and compliance requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.10.1 Sustainable Materials Assessment

- 3.10.2 Carbon Footprint Analysis

- 3.10.3 Circular Economy Implementation

- 3.10.4 Sustainability Certifications and Standards

- 3.10.5 Sustainability ROI Analysis

- 3.11 Global Consumer Sentiment Analysis

- 3.12 Patent Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Flexible plastics

- 5.3 Rigid plastics

- 5.4 Metal

- 5.5 Paper & paperboard

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Pouches & bags

- 6.3 Cans

- 6.4 Cartons & boxes

- 6.5 Bottles & jars

- 6.6 Trays & tubs

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Pet Food Type, 2022 - 2035 (USD Million & Kilo Tons)

- 7.1 Key Trends

- 7.2 Dry food

- 7.3 Wet food

- 7.4 Treats & snacks

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Pet Type, 2022 - 2035 (USD Million & Kilo Tons)

- 8.1 Key Trends

- 8.2 Dogs

- 8.3 Cats

- 8.4 Birds

- 8.5 Fish

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million & Kilo Tons)

- 9.1 Key Trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Amcor

- 11.1.2 Sealed Air

- 11.1.3 Huhtamaki

- 11.1.4 Tetra Pak

- 11.1.5 Sonoco

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Packaging Corporation of America

- 11.2.1.2 Winpak

- 11.2.1.3 Crown Holdings

- 11.2.1.4 Ball Corporation

- 11.2.2 Europe

- 11.2.2.1 Mondi

- 11.2.2.2 Smurfit Kappa

- 11.2.2.3 Constantia Flexibles

- 11.2.2.4 Coveris

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 ProAmpac