|

시장보고서

상품코드

1982354

자동차용 보행자 보호 시스템 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Automotive Pedestrian Protection System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

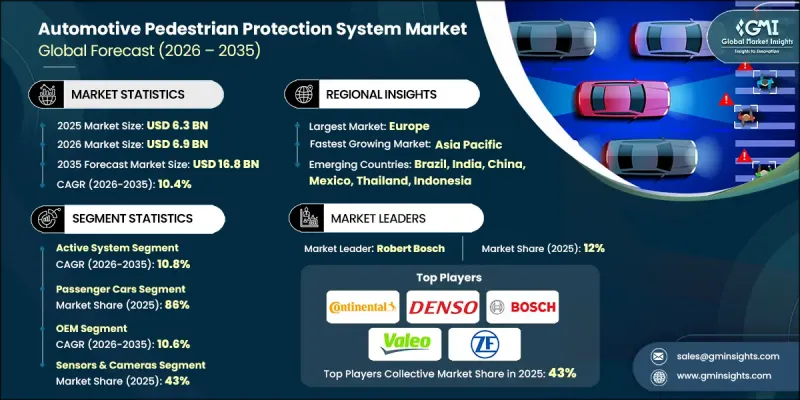

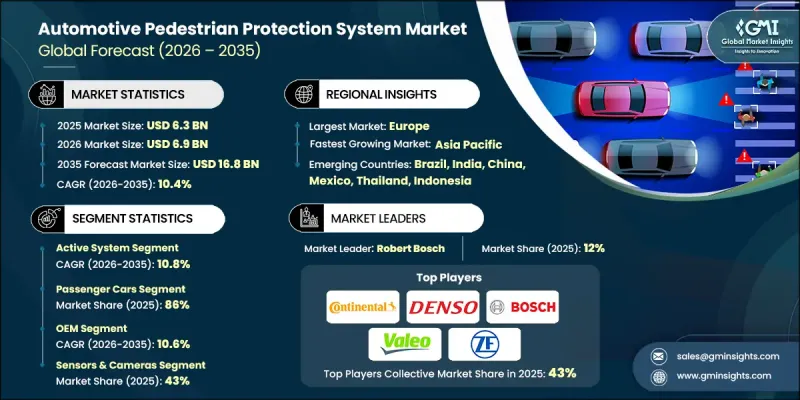

세계의 자동차 보행자 보호 시스템 시장은 2025년 63억 달러로 평가되었으며 CAGR 10.4%로 성장해 2035년까지 168억 달러에 이를 것으로 추정됩니다.

자동차 제조업체가 특히 교통량이 많은 도시에서 보행자의 부상이나 사망을 줄이기 위한 차량 안전 기술을 우선적으로 도입하고 있기 때문에 이 시장은 강한 기세를 보이고 있습니다. 보행자 보호 시스템(PPS)은 고급 긴급 브레이크와 보행자 감지, 전개 가능한 안전 구성 요소, 센서 기반 모니터링 및 지능형 충돌 완화 기술을 결합하여 충돌을 방지하거나 부상 정도를 줄이기 위한 것입니다. 이 시장에는 OEM 및 Tier 1 제조업체에 공급되는 통합 안전 소프트웨어, 센서 하드웨어, 액추에이터 시스템, 구조적 에너지 흡수 설계 및 엔지니어링 지원 서비스가 포함됩니다. 시간이 지남에 따라 보행자 보호 솔루션은 수동 구조 설계에서 실시간 물체 인식과 예측 충돌을 피할 수있는 AI를 활용한 지능형 시스템으로 진화해 왔습니다. 세계 각국의 엄격한 안전 규제와 차량 평가 프로그램으로 도입이 가속화되고 있습니다. 규제 당국은 신차에 보행자와 자전거 이용자를 감지하는 기능을 갖춘 고급 브레이크 시스템을 의무화하고 있기 때문입니다. 클라우드 기반 시뮬레이션 툴과 디지털 검증 플랫폼에 대한 의존도가 높아짐에 따라 시스템의 정확성이 더욱 향상되고 자동차 보행자 보호 시스템 시장 전반의 혁신이 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 63억 달러 |

| 예측 금액 | 168억 달러 |

| CAGR | 10.4% |

액티브 시스템 부문은 2025년에 59%의 점유율을 차지했고 2026년부터 2035년까지 CAGR 10.8%를 나타낼 것으로 예측됩니다. 액티브 보행자 보호 기술은 전방 카메라, 레이더 센서 및 점점 널리 사용되는 LiDAR 시스템을 고급 처리 소프트웨어와 통합한 것입니다. 이러한 시스템은 보행자의 움직임을 감지하고, 궤도의 위험을 평가하고, 충돌 확률을 계산하고, 미리 정의된 안전 임계값에 도달할 때 자동으로 브레이크 기능을 활성화하여 실시간 응답 능력을 크게 향상시킵니다.

승용차 부문은 2025년에 86%의 점유율을 차지했으며 CAGR 10.2%를 나타낼 것으로 예측됩니다. 이 부문 수요는 유럽 신차평가 프로그램(Euro NCAP)과 미국 도로교통안전국(NHTSA)과 같은 조직에 의해 개발된 엄격한 보행자 안전평가 기준을 뒷받침하며, 이러한 기준은 능동보행자 안전성능에 특히 중점을 두고 있습니다. 모든 차량 범주에 걸친 규제 압력은 제조업체가 컴플라이언스를 보장하고 시스템 효율성을 최적화하기 위해 고급 시뮬레이션 및 검증 플랫폼의 채택을 촉진합니다.

독일 자동차 보행자 보호 시스템 시장은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 10.9%를 나타낼 것으로 예측됩니다. 이 나라의 주도적 지위는 BMW, Mercedes-Benz, Audi, Porsche와 같은 주요 자동차 제조업체들이 안전 기술 혁신에 적극적으로 투자함으로써 지원되고 있습니다. 도시의 이동성의 복잡화와 혼합 교통 환경 증가는 동적인 실제 환경에서 효과적으로 기능하도록 설계된 신뢰할 수 있는 보행자 보호 시스템의 도입을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 보행자 안전에 관한 엄격한 규제 및 의무

- 도시 지역의 보행자 사망률 상승

- 첨단 안전 기능에 대한 소비자 수요 증가

- ADAS 및 자율주행 기술의 보급 확대

- 보험 업계에 의한 안전 평가 차량의 추진

- 업계의 잠재적 위험 및 과제

- 높은 도입 및 통합 비용

- 악천후에서 시스템 효율 저하

- 기술적인 복잡성에 의한 애프터마켓 도입의 한정

- 패시브 시스템(외부 에어백)의 일회용 특성

- 시장 기회

- 기존의 상용차 플릿용 레트로핏 솔루션

- V2X 및 스마트 시티 인프라와의 통합

- 안전기준이 정비되고 있는 신흥 시장

- AI를 활용한 야간 감지 시스템

- 패시브 보호 시스템용 경량 소재

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 연방 안전 규칙 및 ADAS 도입 지침

- 캐나다 - 커넥티드 및 자율주행차용 안전 프레임워크(CASF)

- 유럽

- 독일 - Euro NCAP 보행자 안전 평가

- 영국 - 브렉시트 후 ADAS의 유연성

- 프랑스 - 국내 ADAS 시험 및 ITS 전략

- 이탈리아 - ITS 실증 실험 및 스마트 인프라

- 아시아태평양

- 중국 - 산업 정보화부(MIIT)에 의한 C-V2X의 의무화 및 규격

- 인도 - 신흥 ADAS 및 자동차 커넥티비티에 관한 규제

- 일본 - ITS 연결 및 주파수 정책

- 호주 - 기술 중립적인 ITS 정책

- 라틴아메리카

- 멕시코 - NOM 자동차 안전 기준

- 아르헨티나 - 교통법 24.449호

- 중동 및 아프리카

- 남아프리카 - 도로교통법(1996년)

- 사우디아라비아 - 교통 법규 및 비전 2030의 교통 이니셔티브

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 센서 기술의 진화(카메라, LiDAR, 레이더, 초음파)

- 센서 퓨전과 통합

- 보행자 감지에서의 AI 및 머신러닝

- 신흥기술

- 감지 능력 향상을 위한 V2X 통신

- 야간 및 저조도 환경의 검출 기술

- 현재의 기술 동향

- 특허 분석

- 주요 특허 동향

- 기술 혁신의 핫스팟

- 주요 기업에 의한 특허 출원

- 신흥의 지적 재산 전략

- 가격 분석

- 과거 가격 동향 분석

- 사업자 유형별 가격 전략(프리미엄, 밸류, 코스트 플러스)

- 총소유비용(TCO) 분석

- 이용 사례와 성공 사례

- 사례 연구

- PPS 기술의 OEM 통합

- 상용차 플릿에 도입

- 보행자 보호 프로그램의 레트로핏

- 스마트 시티 도시 지역에서의 실증 프로젝트

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고찰

- AI 및 생성형 AI가 시장에 미치는 영향

- AI에 의한 기존 비즈니스 모델의 변화

- 부문별 생성형 AI의 이용 사례와 도입 로드맵

- 위험, 제약 및 규제 고려 사항

- 향후의 동향과 시장 전망

- 차세대 센서 기술

- 자율주행 생태계와의 통합

- AI를 활용한 예측형 보행자 안전 시스템

- 신흥 시장에서의 확대

- 시장 리스크와 리스크 경감 전략

- 규제 준수 위험

- 기술 도입의 장벽

- 공급망의 혼란

- 사이버 보안 및 데이터 프라이버시에 대한 우려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 구성 부품별(2022-2035년)

- 센서 및 카메라

- 제어 유닛

- 액추에이터

- 기타

제6장 시장 추계 및 예측 : 제품별(2022-2035년)

- 액티브 시스템

- 패시브 시스템

제7장 시장 추계 및 예측 : 차종별(2022-2035년)

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제8장 시장 추계 및 예측 : 유통 채널별(2022-2035년)

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 스웨덴

- 덴마크

- 폴란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이스라엘

제10장 기업 프로파일

- 세계기업

- Autoliv

- Continental

- Denso

- Ford Motor

- Magna International

- Mobileye

- Nissan Motor

- Robert Bosch

- Toyota Motor

- ZF Friedrichshafen

- 지역 기업

- Aptiv

- HELLA

- Hitachi Astemo

- Hyundai Mobis

- Knorr-Bremse

- Magneti Marelli

- Subaru

- Valeo

- 신흥기업 및 기술기반기업

- Gentex

- Luminar Technologies

The Global Automotive Pedestrian Protection System Market was valued at USD 6.3 billion in 2025 and is estimated to grow at a CAGR of 10.4% to reach USD 16.8 billion by 2035.

The market is gaining strong momentum as automakers prioritize vehicle safety technologies designed to reduce pedestrian injuries and fatalities, particularly in high-traffic urban environments. Pedestrian protection systems (PPS) combine advanced emergency braking with pedestrian detection, deployable safety components, sensor-based monitoring, and intelligent impact mitigation technologies to either prevent collisions or reduce injury severity. The market encompasses integrated safety software, sensor hardware, actuator systems, structural energy-absorbing designs, and engineering support services supplied to OEMs and Tier 1 manufacturers. Over time, pedestrian protection solutions have evolved from passive structural designs to intelligent, AI-enabled systems capable of real-time object recognition and predictive collision avoidance. Strict safety mandates and vehicle rating programs worldwide are accelerating adoption, as regulators require advanced braking systems with pedestrian and cyclist detection capabilities in new vehicles. Growing reliance on cloud-based simulation tools and digital validation platforms is further enhancing system accuracy and accelerating innovation across the automotive pedestrian protection system market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.3 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 10.4% |

The active system segment accounted for 59% share in 2025 and is anticipated to grow at a CAGR of 10.8% from 2026 to 2035. Active pedestrian protection technologies integrate forward-facing cameras, radar sensors, and increasingly LiDAR systems with advanced processing software. These systems detect pedestrian movement, assess trajectory risks, calculate collision probability, and automatically activate braking functions when predefined safety thresholds are reached, significantly improving real-time response capabilities.

The passenger cars segment held 86% share in 2025 and is projected to grow at a CAGR of 10.2%. Demand within this segment is supported by stringent pedestrian safety assessment standards established by organizations such as the European New Car Assessment Programme and the National Highway Traffic Safety Administration, which place significant emphasis on active pedestrian safety performance. Regulatory pressure across vehicle categories is encouraging manufacturers to adopt advanced simulation and validation platforms to ensure compliance and optimize system efficiency.

Germany Automotive Pedestrian Protection System Market is forecast to grow at a CAGR of 10.9% between 2026 and 2035. The country's leadership is supported by strong investments in safety innovation from major automotive manufacturers such as BMW, Mercedes-Benz, Audi, and Porsche. Increasing urban mobility complexity and mixed-traffic environments are driving the integration of highly reliable pedestrian protection systems designed to operate effectively in dynamic real-world conditions.

Key companies operating in the Global Automotive Pedestrian Protection System Market include ZF Friedrichshafen, Aptiv, Denso, Valeo, Robert Bosch, Autoliv, Continental, Marelli, Hitachi Astemo, and Hella. Companies in the Automotive Pedestrian Protection System Market strengthen their competitive position through continuous investment in research and development focused on AI-driven sensing, advanced braking algorithms, and sensor fusion technologies. Strategic collaborations with OEMs and Tier 1 suppliers enable co-development of integrated safety platforms tailored to specific vehicle architectures. Firms are expanding simulation capabilities using cloud-based validation tools to accelerate product certification and regulatory compliance. Geographic expansion, portfolio diversification, and modular system designs allow suppliers to serve both premium and mass-market vehicle segments. In addition, companies emphasize cost optimization, scalable production, and software updates to enhance long-term system performance, ensuring sustainable growth and stronger market penetration in the evolving global automotive safety landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Components

- 2.2.3 Product

- 2.2.4 Vehicles

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent global pedestrian safety regulations & mandates

- 3.2.1.2 Rising pedestrian fatality rates in urban areas

- 3.2.1.3 Increasing consumer demand for advanced safety features

- 3.2.1.4 Growing adoption of ADAS & autonomous driving technologies

- 3.2.1.5 Insurance industry push for safety-rated vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation & integration costs

- 3.2.2.2 Low system efficiency in adverse weather conditions

- 3.2.2.3 Limited aftermarket adoption due to technical complexity

- 3.2.2.4 One-time use nature of passive systems (external airbags)

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit solutions for existing commercial vehicle fleets

- 3.2.3.2 Integration with V2X & smart city infrastructure

- 3.2.3.3 Emerging markets with developing safety standards

- 3.2.3.4 AI-enhanced nighttime detection systems

- 3.2.3.5 Lightweight materials for passive protection systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal safety rules & ADAS deployment guidance

- 3.4.1.2 Canada - Safety framework for connected & automated vehicles (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- Euro NCAP pedestrian safety ratings

- 3.4.2.2 UK- Post-Brexit ADAS flexibility

- 3.4.2.3 France- National ADAS testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging ADAS & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Sensor technology evolution (camera, LiDAR, RADAR, ultrasonic)

- 3.7.1.2 Sensor fusion & integration

- 3.7.1.3 AI & machine learning in pedestrian detection

- 3.7.2 Emerging technologies

- 3.7.2.1 V2X communication for enhanced detection

- 3.7.2.2 Nighttime & low-light detection technologies

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 Key patent trends

- 3.8.2 Technology innovation hotspots

- 3.8.3 Patent filing by key players

- 3.8.4 Emerging IP strategies

- 3.9 Pricing analysis

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Total cost of ownership (TCO) analysis

- 3.10 Use cases & success stories

- 3.11 Case studies

- 3.11.1 OEM integration of PPS technologies

- 3.11.2 Commercial vehicle fleet deployments

- 3.11.3 Retrofit pedestrian protection programs

- 3.11.4 Urban pilot projects in smart cities

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Future trends and market outlook

- 3.14.1 Next-generation sensor technologies

- 3.14.2 Integration with autonomous driving ecosystems

- 3.14.3 AI-driven predictive pedestrian safety systems

- 3.14.4 Expansion in emerging markets

- 3.15 Market risks and mitigation strategies

- 3.15.1 Regulatory compliance risks

- 3.15.2 Technology adoption barriers

- 3.15.3 Supply chain disruptions

- 3.15.4 Cybersecurity and data privacy concerns

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Sensors & cameras

- 5.3 Control unit

- 5.4 Actuators

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Active system

- 6.3 Passive system

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.3.9 Denmark

- 9.3.10 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Israel

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Autoliv

- 10.1.2 Continental

- 10.1.3 Denso

- 10.1.4 Ford Motor

- 10.1.5 Magna International

- 10.1.6 Mobileye

- 10.1.7 Nissan Motor

- 10.1.8 Robert Bosch

- 10.1.9 Toyota Motor

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 Aptiv

- 10.2.2 HELLA

- 10.2.3 Hitachi Astemo

- 10.2.4 Hyundai Mobis

- 10.2.5 Knorr-Bremse

- 10.2.6 Magneti Marelli

- 10.2.7 Subaru

- 10.2.8 Valeo

- 10.3 Emerging Players & Technology Enablers

- 10.3.1 Gentex

- 10.3.2 Luminar Technologies