|

시장보고서

상품코드

1998734

전지형차(ATV) 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)All-Terrain Vehicle (ATV) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

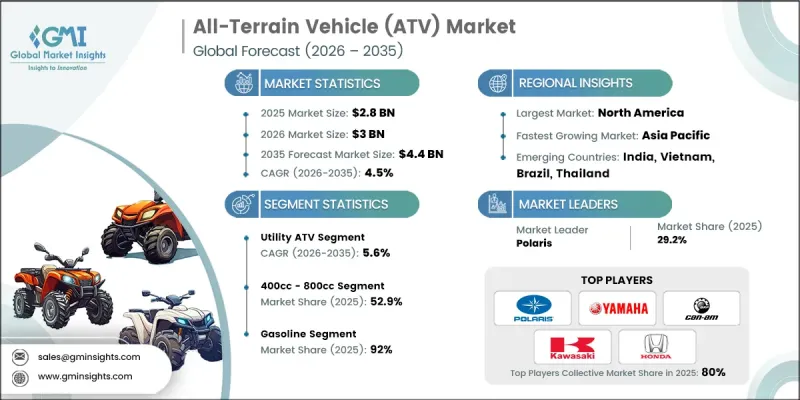

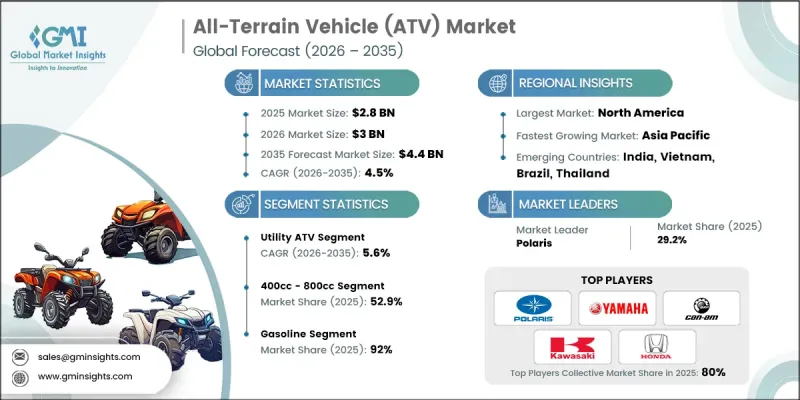

세계의 전지형차(ATV) 시장은 2025년에 28억 달러로 평가되며, CAGR 4.5%로 성장하며, 2035년까지 44억 달러에 달할 것으로 추정되고 있습니다.

전천후 차량 시장의 성장은 아웃도어 활동 참여 증가와 험한 지형을 주행할 수 있는 차량에 대한 수요 증가에 힘입은 바 큽니다. 아웃도어 레크리에이션에 대한 관심이 높아지면서 소비자들은 점점 더 안정적인 오프로드 주행 성능과 오지 접근이 가능한 차량을 원하고 있습니다. 동시에 열악한 환경에서 활동하는 산업도 내구성이 뛰어나고 다용도한 운송 솔루션에 대한 수요에 기여하고 있습니다. 농업, 토지 관리 등 업무용으로 전 지형 대응 차량의 이용 확대도 시장 발전을 촉진하고 있습니다. 이 차량들은 기존 교통수단이 실용적이지 않은 지역에서 이동 수단과 업무 효율성을 제공합니다. 규제 프레임워크와 토지 관리 정책도 시장의 방향성에 영향을 미치고 있으며, 제조업체들이 환경 기준과 사용 가이드라인을 준수하는 차량을 설계하도록 유도하고 있습니다. 이에 따라 각 업체들은 성능, 내구성, 지속가능성 향상에 초점을 맞춘 혁신적인 차량 설계를 도입하고 있습니다. 또한 산업 및 레크리에이션 이용자들이 환경 친화적인 대안을 찾는 가운데, 전기 전천후 차량의 단계적 도입도 중요한 동향으로 떠오르고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 28억 달러 |

| 예측액 | 44억 달러 |

| CAGR | 4.5% |

유틸리티 ATV 부문은 2025년 56%의 점유율을 차지하며, 2026-2035년 연평균 복합 성장률(CAGR) 5.6%로 성장할 것으로 전망됩니다. 이러한 차량에 대한 수요는 험준한 지형이나 어려운 지형을 가로지르는 신뢰할 수 있는 운송 수단이 필요한 분야에서의 실용적인 용도에 의해 크게 지원되고 있습니다. 유틸리티 ATV는 야외 환경에서 이동성과 장비 운반이 필요한 업무 활동에 널리 활용되고 있습니다. 다용도하고 내구성이 뛰어나 자재 운반, 정기 점검 및 일반 현장 작업에 적합합니다. 산업 분야에서 야외 작업 환경에서의 효율성이 지속적으로 강조되면서, 이러한 기능을 지원하는 차량에 대한 수요는 꾸준히 증가할 것으로 예측됩니다. 또한 토지 관리 및 농작업의 기계화가 진행되고 있는 것도 유틸리티 용도에 특화된 ATV의 꾸준한 보급에 기여하고 있습니다.

2025년 기준, 가솔린 자동차 부문은 92%의 점유율을 차지했습니다. 가솔린 차량은 안정적인 성능과 주유 인프라의 편리함으로 인해 여전히 널리 선호되고 있습니다. 이 차량들은 안정적인 에너지 공급이 필수적인 다양한 업무 및 레크리에이션 용도를 지원하고 있습니다. 많은 지역에서 휘발유 주유소가 널리 보급되어 있으며, 연료에 대한 안정적인 접근성이 보장되고 있으며, 이는 휘발유 구동 전 지형 대응 차량의 지속적인 보급을 촉진하고 있습니다. 강력한 엔진 성능과 긴 항속거리로 인해 차량의 안정된 성능이 필수적인 험지에서의 가혹한 용도에 적합합니다.

미국 전 지형 대응 차량(ATV) 시장은 85%의 점유율을 차지하고 있으며, 2025년에는 17억 달러 규모에 도달할 것으로 예측됩니다. 이 국가 시장은 잘 정립되어 있으며, 안전, 토지 이용 가이드라인, 차량 기준을 중시하는 체계적인 규제 환경 하에서 운영되고 있습니다. 전 지형 차량(ATV)에 대한 수요는 오프로드 이동이 일상 업무에서 중요한 역할을 하는 지방에서 특히 높습니다. 농업 및 토지 관리 활동에서 이러한 차량의 광범위한 사용은 안정적인 시장 수요를 지원하고 있습니다. 농업과 목축에 이용되는 광활한 토지는 광범위한 부지 내에서 신뢰할 수 있는 운송 수단에 대한 지속적인 수요를 창출하고 있습니다. 또한 레크리에이션 목적의 오프로드 활동은 책임 있는 차량 이용을 장려하는 지정된 트레일과 접근하기 쉬운 야외 공간으로 지원되는 레크리에이션 목적의 오프로드 활동도 시장 수요의 중요한 요소로 남아 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 차종별, 2022-2035

제6장 시장 추산·예측 : 배기량별, 2022-2035

제7장 시장 추산·예측 : 연료별, 2022-2035

제8장 시장 추산·예측 : 구동 방식별, 2022-2035

제9장 시장 추산·예측 : 용도별, 2022-2035

제10장 시장 추산·예측 : 지역별, 2022-2035

제11장 기업 개요

KSA 26.04.20The Global All-Terrain Vehicle (ATV) Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 4.4 billion by 2035.

Growth in the all-terrain vehicle market is largely supported by increasing participation in outdoor activities and the growing need for vehicles capable of navigating challenging landscapes. As interest in outdoor recreation continues to rise, consumers are increasingly seeking vehicles designed for reliable off-road mobility and access to remote areas. At the same time, industries that operate in rugged environments are contributing to the demand for durable and versatile transportation solutions. The expanding use of all-terrain vehicles in professional applications such as agriculture and land management is also strengthening market development. These vehicles provide mobility and operational efficiency in areas where conventional transportation options are less practical. Regulatory frameworks and land management policies are also influencing the direction of the market, encouraging manufacturers to design vehicles that comply with environmental standards and usage guidelines. In response, companies are introducing innovative vehicle designs that focus on improved performance, durability, and sustainability. The gradual adoption of electric all-terrain vehicles is also emerging as an important trend as industries and recreational users look for environmentally responsible alternatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 4.5% |

The utility ATV segment held 56% share in 2025 and is projected to grow at a CAGR of 5.6% between 2026 and 2035. Demand for these vehicles is largely supported by their practical applications in sectors that require reliable transportation across uneven or difficult terrain. Utility all-terrain vehicles are widely utilized for operational activities that require mobility and equipment handling in outdoor environments. Their versatility and durability make them suitable for tasks that involve the transportation of materials, routine inspections, and general field operations. As industries continue to prioritize efficiency in outdoor work environments, the demand for vehicles that can support these functions is expected to remain strong. The increasing mechanization of land management and agricultural operations also contributes to the consistent adoption of utility-focused all-terrain vehicles.

The gasoline segment held a share of 92% in 2025. Gasoline-powered vehicles remain widely preferred due to their dependable performance and the convenience of refueling infrastructure. These vehicles continue to support a broad range of operational and recreational uses where a reliable energy supply is essential. The extensive availability of gasoline refueling points across many regions ensures consistent access to fuel, which strengthens the continued adoption of gasoline-powered all-terrain vehicles. Their strong engine performance and long operational range make them suitable for demanding applications in remote environments where consistent vehicle performance is critical.

United States All-Terrain Vehicle (ATV) Market accounted for 85% share, generating USD 1.7 billion in 2025. The market in the country is well established and operates within a structured regulatory environment that emphasizes safety, land usage guidelines, and vehicle standards. Demand for all-terrain vehicles is particularly strong in rural areas where off-road mobility plays a key role in daily operations. The widespread use of these vehicles in agricultural and land management activities supports steady market demand. Large land areas used for farming and ranching create consistent requirements for reliable transportation across extensive properties. In addition, recreational off-road activities remain an important contributor to market demand, supported by designated trails and accessible outdoor spaces that encourage responsible vehicle use.

Key companies participating in the Global All-Terrain Vehicle (ATV) Market include Polaris, Yamaha, Honda, Kawasaki, Suzuki, Arctic Cat, BRP, Textron, CFMoto, and Kymco. Companies operating in the Global All-Terrain Vehicle (ATV) Market are focusing on several strategic initiatives to strengthen their competitive position and expand their market reach. Product innovation remains a primary strategy, with manufacturers investing in advanced vehicle technologies that enhance durability, performance, and user safety. Many companies are also developing electric and environmentally friendly vehicle options to align with evolving environmental regulations and sustainability goals. Strategic partnerships with distributors and regional dealers are helping manufacturers expand their presence across key geographic markets. Additionally, firms are increasing investments in research and development to improve vehicle efficiency and introduce new features that enhance user experience. Expanding production capacity and strengthening supply chain networks are also helping companies respond effectively to growing global demand for all-terrain vehicles.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Displacement

- 2.2.4 Fuel

- 2.2.5 Drive

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in outdoor recreation participation

- 3.2.1.2 Expansion of precision agriculture practices

- 3.2.1.3 Rising rural infrastructure and land management spending

- 3.2.1.4 Product innovation in powertrain and suspension systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Safety concerns and accident rates

- 3.2.2.2 Environmental restrictions on off road access

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification of off-road vehicles

- 3.2.3.2 Growth in defense and border surveillance applications

- 3.2.3.3 Aftermarket accessories and performance upgrades

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States all terrain vehicle safety regulations and Consumer Product Safety Commission guidelines

- 3.4.1.2 Federal land access and off road vehicle management rules

- 3.4.1.3 Emission standards for off road spark ignition engines

- 3.4.1.4 Canada off road vehicle safety and provincial registration requirements

- 3.4.2 Europe

- 3.4.2.1 European Union type approval framework for quadricycles and off road vehicles

- 3.4.2.2 ECE vehicle safety and braking system regulations

- 3.4.2.3 Country level homologation and road use restrictions

- 3.4.2.4 Environmental and noise emission compliance standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China off road vehicle manufacturing and emission standards

- 3.4.3.2 India quadricycle and off highway vehicle homologation norms

- 3.4.3.3 Japan vehicle safety and small off road mobility guidelines

- 3.4.3.4 Australia off road vehicle design and safety requirements

- 3.4.3.5 ASEAN regional vehicle certification frameworks

- 3.4.4 Latin America

- 3.4.4.1 Brazil off road vehicle safety and environmental compliance rules

- 3.4.4.2 Argentina vehicle registration and usage regulations

- 3.4.4.3 Mexico manufacturing standards and safety compliance

- 3.4.4.4 Regional off road vehicle regulatory frameworks

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE off road vehicle licensing and desert operation rules

- 3.4.5.2 Saudi Arabia vehicle safety and inspection standards

- 3.4.5.3 South Africa off road vehicle registration and safety requirements

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by primary research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type

- 3.9 Trade Data Analysis (Driven by paid database)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Capacity & Production Landscape (Driven by primary research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.12 Patent analysis (Driven by primary research)

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Impact of AI and Generative AI on the Market

- 3.14.1 AI Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.14.3 Risks Limitations and Regulatory Considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Utility ATV

- 5.3 Sport ATV

- 5.4 Recreational ATV

- 5.5 Youth ATV

Chapter 6 Market Estimates & Forecast, By Displacement, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Below 400cc

- 6.3 400cc - 800cc

- 6.4 Above 800cc

Chapter 7 Market Estimates & Forecast, By Fuel, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Electric

Chapter 8 Market Estimates & Forecast, By Drive, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 2-Wheel Drive (2WD)

- 8.3 4-Wheel Drive (4WD)

- 8.4 All-Wheel Drive (AWD)

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Agriculture & Farming

- 9.3 Forestry

- 9.4 Military & Defense

- 9.5 Sports & Racing

- 9.6 Recreation & Tourism

- 9.7 Industrial & Utility Services

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BRP

- 11.1.2 Honda

- 11.1.3 Kawasaki

- 11.1.4 Polaris

- 11.1.5 Suzuki

- 11.1.6 Textron

- 11.1.7 Yamaha

- 11.2 Regional Players

- 11.2.1 Arctic Cat

- 11.2.2 Italika

- 11.2.3 John Deere

- 11.2.4 Kubota

- 11.2.5 Kymco

- 11.2.6 TGB

- 11.3 Emerging Players / Disruptors

- 11.3.1 Apollo

- 11.3.2 Bashan

- 11.3.3 CFMoto

- 11.3.4 Coolster

- 11.3.5 Hisun

- 11.3.6 Linhai

- 11.3.7 Taotao