|

시장보고서

상품코드

1998737

자동차용 트랙션 모터 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

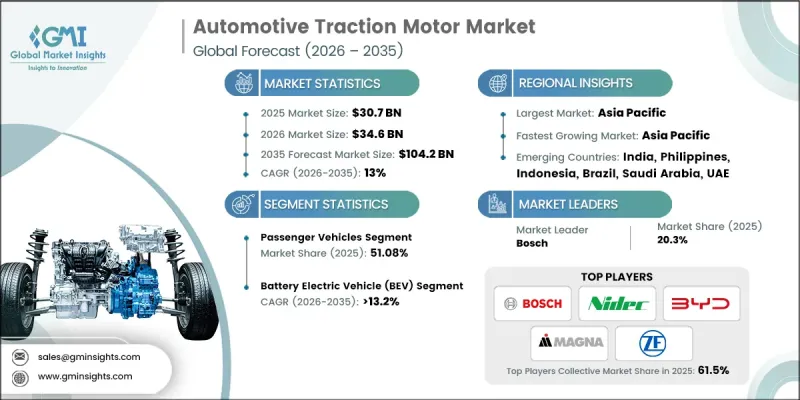

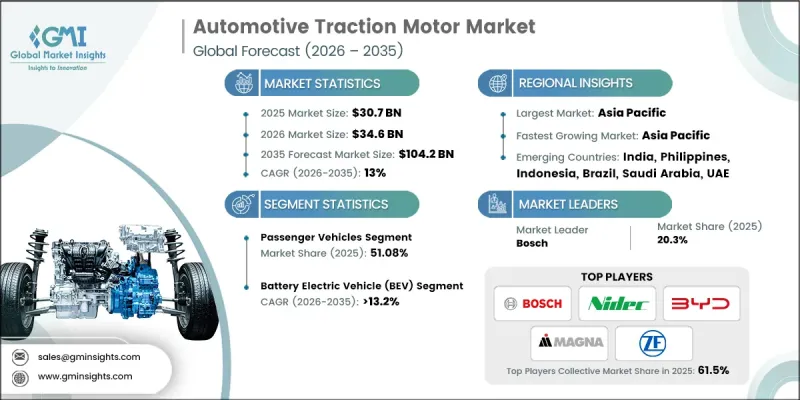

세계의 자동차용 트랙션 모터 시장은 2025년에 307억 달러로 평가되며, CAGR 13%로 성장하며, 2035년까지 1,042억 달러에 달할 것으로 추정되고 있습니다.

자동차 산업의 급속한 전동화로 인해 트랙션 모터는 2차 구동계 요소에서 차량 성능과 에너지 효율을 담당하는 핵심 부품으로 변모하고 있습니다. 전 세계 모빌리티가 전동화 운송으로 전환하는 가운데, 트랙션 모터는 동력 공급, 에너지 사용 최적화, 그리고 진화하는 환경 규제에 대응하기 위해 필수적인 요소로 자리 잡고 있습니다. 이 모터는 현재 완전 전기자동차, 하이브리드차, 전동화 상용차 등 다양한 전기자동차 플랫폼에 광범위하게 적용되고 있습니다. 전기자동차 생산량 증가, 차종 라인업 확대, 그리고 점점 더 엄격해지는 배기가스 저감 정책이 결합되어 첨단 모터 기술에 대한 강력한 수요를 견인하고 있습니다. 자동차 제조업체는 모터의 효율 향상, 토크 출력 개선, 전체 시스템의 경량화 및 안정적인 열 성능 확보에 주력하고 있습니다. 동시에 트랙션 모터와 파워 일렉트로닉스, 배터리 시스템과의 통합은 차량 아키텍처 설계에 대한 보다 종합적인 접근 방식을 촉진하고 있습니다. 모터의 소재와 구성에 대한 기술적 진보도 시장내 경쟁에 영향을 미치고 있으며, 제조업체들은 에너지 효율성 향상, 생산 비용 절감, 장기적인 차량 성능 향상을 위한 솔루션을 지속적으로 개발하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 307억 달러 |

| 예측액 | 1,042억 달러 |

| CAGR | 13% |

승용차 부문은 2025년 51.08%의 점유율을 차지하며, 2035년까지 연평균 12.3%의 성장률을 보일 것으로 전망됩니다. 이 부문의 탄탄한 입지는 주로 세계 전기 승용차 보급 가속화와 다양한 가격대의 전기 모델 공급 확대에 의해 지원되고 있습니다. 자동차 제조업체들은 다양한 승용차 카테고리의 전동화를 우선시하고 있으며, 이로 인해 현대 차량에 구동 모터의 탑재가 크게 증가하고 있습니다. 또한 전용 EV 플랫폼으로의 전환과 고급 승용차의 멀티 모터 구성 채택 확대로 차량 당 모터 사용량이 증가하면서 승용차 부문 시장 점유율을 더욱 강화하고 있습니다.

배터리 전기자동차(BEV) 부문은 2025년 67.2%의 점유율을 차지하며, 2026-2035년 연평균 복합 성장률(CAGR) 13.2%로 성장할 것으로 전망됩니다. 이러한 압도적인 우위는 주로 배터리 전기자동차가 이동 수단으로 전기 추진 시스템에 전적으로 의존하고 있기 때문입니다. 내연기관과 전기 파워트레인을 결합한 하이브리드차량과 달리 BEV는 전적으로 전기 모터로 구동되므로 1대당 견인 모터 수요가 직접적으로 증가합니다. 또한 많은 고성능 전기자동차는 출력과 차량 제어를 향상시키기 위해 멀티 모터 구성을 채택하고 있습니다. 전 세계적인 무공해 모빌리티 추진 노력, 배터리 비용의 하락, 충전 인프라의 지속적인 확충은 BEV의 생산과 보급을 더욱 가속화하고 있으며, 그 결과 트랙션 모터 기술에 대한 수요가 증가하고 있습니다.

2025년 중국 자동차 견인 모터 시장은 104억 달러 규모로 64.21%의 점유율을 차지했습니다. 중국은 세계 전기자동차 제조의 선도적 위치와 차량 전동화에 대한 강력한 지원으로 지역 시장에서 확고한 입지를 유지하고 있습니다. 중국은 대규모 전기자동차 생산, 통합된 공급망, 배터리 및 파워 일렉트로닉스의 강력한 제조 능력을 포함한 종합적인 생태계를 구축하고 있습니다. 신에너지 차량 보급과 전기 이동성 인프라 확충을 위한 정부의 구상은 전기 승용차 및 상용 운송 솔루션의 도입을 지속적으로 촉진하고 있습니다. 이러한 요인들로 인해 효율적이고 신뢰할 수 있는 전기 추진을 위해 설계된 첨단 트랙션 모터 시스템에 대한 수요가 크게 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 차량별, 2022-2035

제6장 시장 추산·예측 : 전기 구동 방식별, 2022-2035

제7장 시장 추산·예측 : 동력원별, 2022-2035

제8장 시장 추산·예측 : 출력별, 2022-2035

제9장 시장 추산·예측 : 지역별, 2022-2035

제10장 기업 개요

KSA 26.04.20The Global Automotive Traction Motor Market was valued at USD 30.7 billion in 2025 and is estimated to grow at a CAGR of 13% to reach USD 104.2 billion by 2035.

The rapid electrification of the automotive industry is transforming the traction motor from a secondary drivetrain element into a central component responsible for vehicle performance and energy efficiency. As global mobility transitions toward electrified transportation, traction motors have become essential for delivering power, optimizing energy usage, and supporting compliance with evolving environmental regulations. These motors are now widely integrated across various electrified vehicle platforms, including fully electric vehicles, hybrid vehicles, and electrified commercial fleets. Rising electric vehicle production, expanding vehicle model offerings, and increasingly strict emission reduction policies are collectively driving strong demand for advanced motor technologies. Automotive manufacturers are focusing on enhancing motor efficiency, improving torque output, reducing overall system weight, and ensuring stable thermal performance. At the same time, the integration of traction motors with power electronics and battery systems is encouraging a more comprehensive approach to vehicle architecture design. Technological advancements in motor materials and configurations are also influencing competition within the market as manufacturers continue to develop solutions that improve energy efficiency, reduce production costs, and enhance long-term vehicle performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $30.7 Billion |

| Forecast Value | $104.2 Billion |

| CAGR | 13% |

The passenger cars segment accounted for 51.08% share in 2025 and is projected to grow at a CAGR of 12.3% through 2035. The strong position of this segment is primarily supported by the accelerating adoption of electric passenger vehicles worldwide and the increasing availability of electrified models across different price categories. Automotive manufacturers are prioritizing the electrification of various passenger vehicle categories, which has significantly increased the installation of traction motors in modern vehicles. In addition, the transition toward dedicated electric vehicle platforms and the growing adoption of multi-motor configurations in premium passenger vehicles are increasing the number of motors used per vehicle, further strengthening the market share of the passenger car segment.

The battery electric vehicle segment held a 67.2% share in 2025 and is expected to grow at a CAGR of 13.2% between 2026 and 2035. This strong dominance is largely attributed to the complete reliance of battery electric vehicles on electric propulsion systems for mobility. Unlike hybrid vehicles that combine internal combustion engines with electric powertrains, battery electric vehicles operate entirely using electric motors, which directly increases traction motor demand per vehicle. In addition, many high-performance electric vehicles utilize multiple motor configurations to enhance power output and vehicle control. Global initiatives promoting zero-emission mobility, declining battery costs, and the continuous expansion of charging infrastructure are further accelerating the production and adoption of battery electric vehicles, thereby increasing demand for traction motor technologies.

China Automotive Traction Motor Market generated USD 10.4 billion in 2025 and held 64.21% share. The country maintains a strong position in the regional market due to its leadership in global electric vehicle manufacturing and its strong support for vehicle electrification. China has developed a comprehensive ecosystem that includes large-scale electric vehicle production, integrated supply chains, and strong manufacturing capabilities for batteries and power electronics. Government initiatives aimed at promoting new energy vehicles and expanding electric mobility infrastructure continue to encourage the adoption of electrified passenger vehicles and commercial transportation solutions. These factors are contributing to substantial demand for advanced traction motor systems designed to deliver efficient and reliable electric propulsion.

Key companies operating in the Global Automotive Traction Motor Market include Bosch, Denso, ZF Friedrichshafen, Continental, Magna, Valeo, Hitachi, Mitsubishi Electric, Aisin, and General Motors. Companies competing in the Automotive Traction Motor Market are implementing a variety of strategies to strengthen their competitive position and expand global market share. Leading manufacturers are investing heavily in research and development to improve motor efficiency, increase power density, and enhance thermal management capabilities. Many companies are also focusing on developing advanced motor architectures that reduce reliance on expensive raw materials while improving performance and durability. Strategic collaborations with automotive manufacturers and technology partners are helping companies accelerate innovation and integrate traction motors more effectively with electric powertrain systems. Additionally, organizations are expanding manufacturing facilities, strengthening supply chains, and increasing production capacity to meet the rapidly growing demand for electric vehicles. Continuous technological advancement, platform integration, and global expansion remain essential strategies for maintaining competitiveness in the automotive traction motor market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Electric Drivetrain

- 2.2.4 Motor

- 2.2.5 Power Output

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global electric vehicle production

- 3.2.1.2 Increase in stringent emission and fuel efficiency regulations

- 3.2.1.3 Surge in electrification of public transport and logistics fleets

- 3.2.1.4 Rise in consumer demand for high-performance EVs

- 3.2.1.5 Increase in investments toward localized EV manufacturing ecosystems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuation in rare-earth material prices

- 3.2.2.2 High initial R&D and capital investment requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in EV adoption across emerging economies

- 3.2.3.2 Rise in electrification of two- and three-wheelers

- 3.2.3.3 Increase in government-backed electric bus deployment programs

- 3.2.3.4 Surge in demand for premium and performance EV segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory guidline

- 3.4.1 North America

- 3.4.1.1 U.S.: EV Tax Credits, EPA Emission Standards & DOE Electric Drive Efficiency Programs

- 3.4.1.2 Canada: Zero-Emission Vehicle (ZEV) Mandate & Transport Canada Safety Standards

- 3.4.2 Europe

- 3.4.2.1 Germany: EU CO Fleet Emission Targets & End-of-Life Vehicle (ELV) Directive

- 3.4.2.2 UK: Zero Emission Vehicle (ZEV) Mandate & Type Approval Regulations

- 3.4.2.3 France: Energy Transition Law & EV Industrial Strategy

- 3.4.2.4 Italy: National Energy & Climate Plan (PNIEC) Alignment

- 3.4.3 Asia Pacific

- 3.4.3.1 China: NEV Mandate & Dual Credit Policy

- 3.4.3.2 India: FAME II & PLI Scheme for Auto Components

- 3.4.3.3 Japan: Green Growth Strategy & JEVS Standards

- 3.4.3.4 Australia: National Electric Vehicle Strategy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: Rota 2030 Program

- 3.4.4.2 Mexico: USMCA Localization Requirements

- 3.4.4.3 Argentina: National Sustainable Mobility Policies

- 3.4.5 MEA

- 3.4.5.1 UAE: Net Zero 2050 Strategy & EV Infrastructure Expansion

- 3.4.5.2 Saudi Arabia: Vision 2030 & EV Localization Strategy

- 3.4.5.3 South Africa: Green Transport Strategy

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook & opportunities

- 3.13 Trade statistics (Driven by Paid Database)

- 3.13.1 Production hubs

- 3.13.2 Consumption hubs

- 3.13.3 Export and import

- 3.14 Key Trade corridors & tariff impact

- 3.14.1 US-china trade dynamics

- 3.14.2 EU internal market trade

- 3.14.3 Asia-pacific regional trade

- 3.15 Impact of AI & Generative AI on the Market

- 3.15.1 AI-Driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Investment & funding analysis

- 3.16.1 Private equity & venture capital activity

- 3.16.2 M&a trends & strategic consolidations

- 3.16.3 Government funding & R&D grants

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Medium Commercial Vehicles (MCV)

- 5.3.3 Heavy Commercial Vehicles (HCV)

- 5.4 Two-wheelers

- 5.5 Off-road vehicles

Chapter 6 Market Estimates & Forecast, By Electric Drivetrain, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicle (BEV)

- 6.3 Hybrid Electric Vehicle (HEV)

- 6.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 7 Market Estimates & Forecast, By Motor, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 PMSM

- 7.3 AC Induction

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Less than 200 KW

- 8.3 200-400 KW

- 8.4 Above 400 KW

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aisin

- 10.1.2 BorgWarner

- 10.1.3 Bosch

- 10.1.4 BYD

- 10.1.5 DENSO

- 10.1.6 Nidec

- 10.1.7 Tesla

- 10.1.8 Valeo

- 10.1.9 Vitesco Technologies

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 General Motors

- 10.2.2 Hitachi Astemo

- 10.2.3 Huawei Digital Power

- 10.2.4 Hyundai Mobis

- 10.2.5 Inovance Automotive

- 10.2.6 Jing-Jin Electric

- 10.2.7 Magna International

- 10.2.8 MAHLE

- 10.2.9 Mitsubishi Electric

- 10.2.10 Schaeffler Group

- 10.3 Emerging players

- 10.3.1 Equipmake

- 10.3.2 LG Magna e-Powertrain

- 10.3.3 Lucid Motors

- 10.3.4 Rivian

- 10.3.5 YASA (Mercedes-Benz)