|

시장보고서

상품코드

2019227

자율주행 트랙터 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Autonomous Tractors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

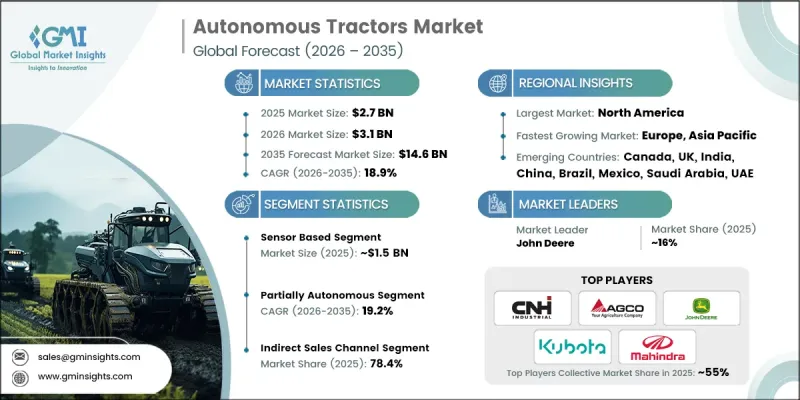

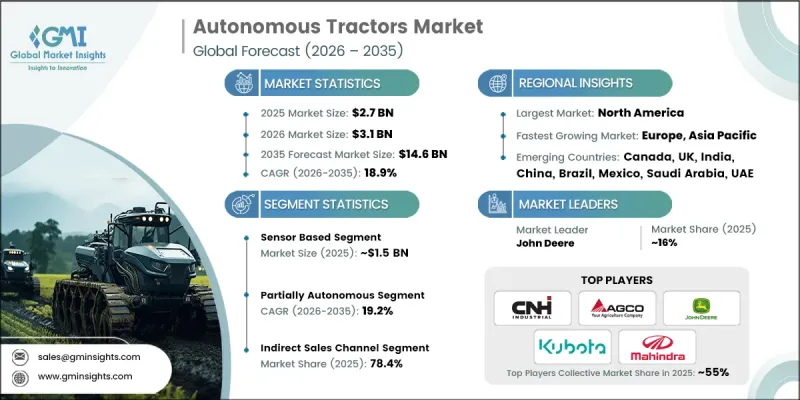

세계의 자율주행 트랙터 시장은 2025년에 27억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 18.9%로 성장하여 146억 달러에 이를 것으로 추정되고 있습니다.

이러한 급속한 성장은 주로 노동력 부족과 효율적인 농업 경영에 대한 수요 증가에 힘입어 현대 농업의 모습을 바꾸고 있습니다. 많은 지역, 특히 선진국에서는 농업 종사자의 고령화가 진행되면서 이 산업에 진입하는 젊은 농부들이 줄어들고 있습니다. 자율주행 트랙터는 인간 노동에 대한 의존도를 줄임으로써 이러한 문제를 해결할 수 있습니다. 이를 통해 기계가 피로하지 않고 장시간 작동할 수 있고, 반복적이거나 단조로운 작업을 관리할 수 있어 농부들이 대규모 농장을 보다 효율적으로 관리할 수 있게 됩니다. 인건비 상승과 노동력 부족으로 인해 자율주행 트랙터는 적기 파종, 시비, 수확 작업에 필수적인 동시에 생산성과 자원 관리 향상에 기여하고 있습니다.

| 시장 규모 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 27억 달러 |

| 예측액 | 146억 달러 |

| CAGR | 18.9% |

정밀농업의 도입도 또 다른 중요한 성장 요인입니다. 농가에서는 첨단 GPS, 인공지능, 센서 시스템 등의 기술을 도입하는 움직임이 가속화되고 있으며, 이를 통해 트랙터를 고정밀도로 가동할 수 있게 되었습니다. 자율주행 트랙터는 이러한 기술을 활용하여 작물 수확량을 최적화하고 낭비를 줄이며 물, 종자, 비료의 효율적인 사용을 보장합니다.

센서 기반 시스템 시장은 2025년 15억 달러에 달할 것으로 예상되며, 2026년부터 2035년까지 연평균 19.5%의 성장률을 보일 것으로 예측됩니다. LiDAR, 초음파, 적외선, 근접센서 등의 시스템을 통해 토양 상태와 작물 생육상황을 실시간으로 모니터링하고 장애물을 감지하여 복잡한 밭 환경에서도 트랙터를 안전하게 유도할 수 있습니다. 디지털 농업의 확대에 따라 환경 데이터를 분석하고 자율적으로 작업을 조정할 수 있는 지능형 시스템에 대한 수요가 급증하고 있습니다.

부분 자율주행 트랙터 부문은 2025년 57%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 19.2%를 나타낼 것으로 예측됩니다. 이 모델들은 GPS 보조 조향, 자동 속도 제어, 유도 내비게이션과 의사 결정에 있어 인간의 감독을 결합하여 완전 자율 주행 유닛에 대한 비용 효율적인 대안을 제공합니다. 기존 인프라와 농업 관행과의 호환성을 통해 도입 장벽을 낮추고 학습 기간을 단축하여 예산이 한정된 개발도상국의 농부들에게 특히 매력적인 선택이 될 수 있습니다.

미국 자율주행 트랙터 시장은 2025년 7억 달러 규모에 달할 것으로 예상되며, 2035년까지 연평균 19.2%의 성장률을 보일 것으로 전망됩니다. 미국 농부들은 생산성 향상, 노동력 의존도 감소, 자원 활용의 최적화를 위해 자동화 및 정밀 농업 기술을 일찍이 도입하고 있습니다. AI, IoT, GPS, 데이터 분석을 자율 주행 트랙터에 통합하는 기업을 포함한 강력한 농업 기술 제공업체 생태계가 스마트 농업의 도입을 촉진하고 혁신을 주도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기술별, 2022-2035

제6장 시장 추산 및 예측 : 자동화 레벨별, 2022-2035

제7장 시장 추산 및 예측 : 출력별, 2022-2035

제8장 시장 추산 및 예측 : 작물 유형별, 2022-2035

제9장 시장 추산 및 예측 : 용도별, 2022-2035

제10장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.05.08The Global Autonomous Tractors Market was valued at USD 2.7 billion in 2025 and is estimated to grow at a CAGR of 18.9% to reach USD 14.6 billion by 2035.

The rapid growth is reshaping modern agriculture, driven largely by labor shortages and the increasing demand for efficient farming operations. In many regions, particularly in developed economies, the farming workforce is aging, and fewer young farmers are entering the industry. Autonomous tractors address these challenges by reducing dependence on human labor, allowing machinery to operate long hours without fatigue, manage repetitive or tedious tasks, and enable farmers to oversee large-scale farms more efficiently. Rising labor costs and scarce workforce availability make autonomous tractors essential for timely planting, fertilizing, and harvesting operations, while also improving productivity and resource management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.7 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 18.9% |

The adoption of precision agriculture is another key growth factor. Farmers are increasingly integrating technologies such as advanced GPS, artificial intelligence, and sensor systems, which allow tractors to operate with high accuracy. Autonomous tractors use these technologies to optimize crop yields, reduce waste, and ensure efficient use of water, seeds, and fertilizers.

The sensor-based systems segment reached USD 1.5 billion in 2025, are expected to grow at a CAGR of 19.5% from 2026 to 2035. Sensors such as LiDAR, ultrasonic, infrared, and proximity systems enable real-time monitoring of soil conditions, crop health, and obstacle detection, guiding tractors safely through complex field environments. As digital farming expands, demand for intelligent systems capable of interpreting environmental data and autonomously adjusting operations is rising sharply.

The partially autonomous tractors segment held 57% share in 2025 and is projected to grow at a CAGR of 19.2% from 2026 to 2035. These models combine GPS-assisted steering, auto-speed control, and guided navigation with human oversight for decision-making, offering a cost-effective alternative to fully autonomous units. Their compatibility with existing infrastructure and farming practices reduces adoption barriers and shortens the learning curve, making them especially attractive to farmers in developing regions where budgets are constrained.

U.S. Autonomous Tractors Market captured USD 0.7 billion in 2025, and is expected to grow at a CAGR of 19.2% through 2035. U.S. farmers are early adopters of automation and precision farming technologies to enhance productivity, lower labor dependence, and optimize resource usage. A strong ecosystem of agri-tech providers, including companies that integrate AI, IoT, GPS, and data analytics into autonomous tractors, facilitates adoption and drives innovation in smart farming.

Prominent players in the Global Autonomous Tractors Market include AGCO, Argo Tractors, AutoNxt Automation, Autonomous Tractor Corporation, CNH Industrial, Dutch Power Company, John Deere, Kubota Corporation, Mahindra and Mahindra Ltd, Raven Industries, SDF Group, Trimble, TYM Corporation, Yanmar Co. Ltd, and Zimeno Inc. (DBA Monarch Tractor). Companies in the autonomous tractor market strengthen their position by focusing on continuous R&D and technology integration, offering partially and fully autonomous models to cater to varying farm sizes and budgets, and providing end-to-end solutions combining hardware, software, and data analytics. Partnerships and strategic collaborations with tech firms enable rapid innovation and adoption of AI, sensor, and IoT technologies. Firms also expand through geographical diversification, targeting emerging markets with customized offerings suitable for local agricultural practices. Enhancing customer support, training programs, and providing flexible financing options further improve accessibility, building trust and long-term customer loyalty while sustaining market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Automation

- 2.2.4 Power output

- 2.2.5 Crop type

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Labor shortages in agriculture

- 3.2.1.2 Rising demand for precision agriculture

- 3.2.1.3 Increasing farm productivity and efficiency

- 3.2.1.4 Sustainability and environmental concerns

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Technical complexity and skill gaps

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 GPS guidance

- 5.3 Sensor based

- 5.4 Remote control

Chapter 6 Market Estimates & Forecast, By Automation, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Fully autonomous

- 6.3 Partially autonomous

- 6.4 Highly autonomous

Chapter 7 Market Estimates & Forecast, By Power Output, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Light duty (<50 HP)

- 7.3 Medium-duty (50-100 HP)

- 7.4 Heavy-duty (>100 HP)

Chapter 8 Market Estimates & Forecast, By Crop Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Cereal crops

- 8.3 Row crops

- 8.4 Specialty crops

- 8.5 Forage crops

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Agriculture

- 9.2.1 Tillage and soil preparation

- 9.2.2 Planting and seeding

- 9.2.3 Crop monitoring and management

- 9.2.4 Harvesting operations

- 9.3 Mining

- 9.3.1 Material handling and transport

- 9.3.2 Site preparation and maintenance

- 9.4 Waste management

- 9.4.1 Collection and sorting

- 9.4.2 Site maintenance and operations

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 AGCO

- 12.2 Argo Tractors

- 12.3 AutoNext Automation

- 12.4 Autonomous Tractor Corporation

- 12.5 CNH Industrial

- 12.6 Dutch Power Company

- 12.7 John Deere

- 12.8 Kubota Corporation

- 12.9 Mahindra and Mahindra Ltd

- 12.10 Raven Industries

- 12.11 SDF Group

- 12.12 Trimble

- 12.13 TYM Corporation

- 12.14 Yanmar Co. Ltd

- 12.15 Zimeno Inc.