|

시장보고서

상품코드

2027586

로봇 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Robot Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

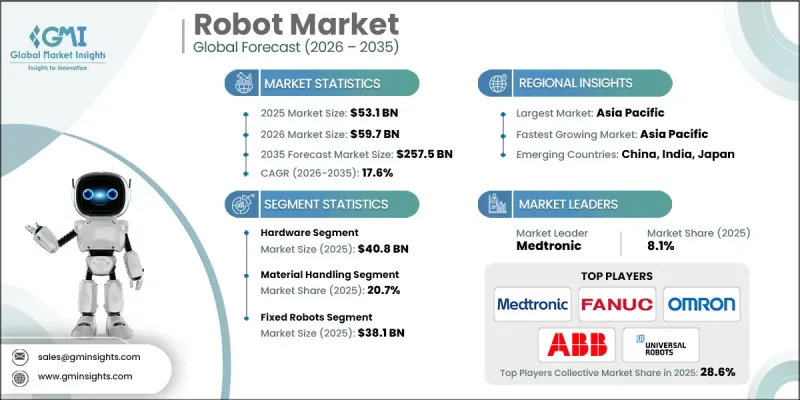

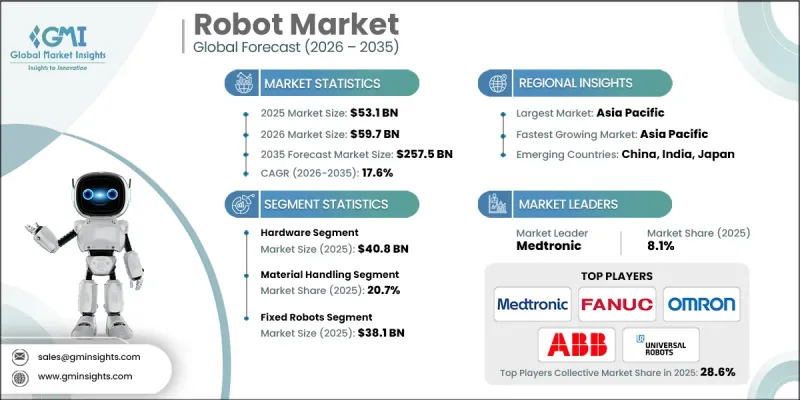

세계의 로봇 시장은 2025년에 531억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 17.6%를 나타내 2,575억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 로봇공학, 인공지능, 머신러닝의 급속한 발전으로 인해 산업 전반에 걸쳐 업무 프로세스를 혁신하고 있습니다. 이러한 기술들은 보다 높은 수준의 자동화와 정확성을 실현하여 공급망 운영을 재구축하고 고객 대응 시스템을 강화하고 있습니다. 현대의 로봇 시스템은 첨단 감지 기능, 지능형 동작 계획 및 향상된 적응성으로 설계되어 복잡한 작업을 높은 정밀도로 수행 할 수 있습니다. 기업들은 증가하는 업무 수요에 대응하고, 효율성을 높이고, 처리 시간을 단축하기 위해 로봇 솔루션을 도입하는 사례가 늘고 있습니다. 보다 신속하고 정확한 주문 처리에 대한 요구가 높아지면서 물류 및 업무 워크플로우에 로봇 기술의 통합이 더욱 가속화되고 있습니다. 또한, 직원들의 생산성과 업무 확장성에 대한 압박이 커지면서 기업들은 반복적이고 육체적으로 힘든 작업을 처리할 수 있는 자동화 솔루션을 도입하고 있습니다. 각 산업계가 효율성과 성능 최적화에 집중하고 있는 가운데, 로봇 시스템 도입은 전 세계 시장 전체에서 크게 확대될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 531억 달러 |

| 예측액 | 2,575억 달러 |

| CAGR | 17.6% |

하드웨어 분야는 2025년 408억 달러 시장 규모를 기록했습니다. 이 분야의 성장은 협동 로봇의 보급 확대와 로봇의 핵심 구성 요소의 지속적인 개선으로 뒷받침되고 있습니다. 고급 컨트롤러, 액추에이터, 엔드 이펙터를 통해 다양한 응용 분야에서 보다 정밀하고 효율적인 로봇 조작이 가능합니다. 센서는 기계가 주변 환경을 감지하고 자율적으로 작동할 수 있도록 함으로써 로봇의 기능 향상에 매우 중요한 역할을 하고 있습니다. 정교하고 복잡한 작업을 수행할 수 있는 첨단 로봇 시스템에 대한 수요가 증가함에 따라 첨단 센싱 기술의 채택이 증가하고 있습니다. 이러한 발전은 로봇 하드웨어의 전반적인 성능과 신뢰성을 향상시키고, 시장에서 그 중요성을 더욱 강화하고 있습니다.

2025년 기준, 고정형 로봇 부문은 381억 달러로 업계에서 확고한 입지를 구축했습니다. 이 부문은 로봇 설계 및 엔지니어링 분야의 지속적인 기술 발전으로 인해 성능이 향상되고 응용 분야가 확대되는 혜택을 누리고 있습니다. 고정형 로봇 시스템은 높은 정밀도와 일관성이 요구되는 작업에 널리 활용되고 있으며, 다양한 산업 공정에서 필수적인 존재로 자리 잡고 있습니다. 반복적이고 위험한 작업을 정확하게 수행할 수 있는 능력은 생산성을 향상시키는 동시에 작업장의 안전성을 높입니다. 각 산업계가 업무 효율화를 위해 자동화에 대한 투자를 지속하고 있는 가운데, 고정형 로봇 시스템에 대한 수요는 지속적으로 견조할 것으로 예측됩니다.

북미의 로봇 시장은 2025년 110.6%의 점유율을 차지했으며, 혁신 주도형 첨단 로봇 생태계를 강조하고 있습니다. 이 지역은 자동화 기술 도입률이 높고, 로봇 개발자, 통합업체, 최종 사용자로 구성된 탄탄한 네트워크의 혜택을 누리고 있습니다. 첨단 제조 및 스마트 생산 환경에 대한 강력한 투자가 시장 확대를 뒷받침하고 있습니다. 미국은 생산성 향상과 노동력 관련 이슈에 대한 대응이 요구되는 가운데, 지역 성장을 견인하는 중요한 역할을 담당하고 있습니다. 지속적인 기술 혁신과 전략적 투자를 통해 이 지역의 로봇 시장에서의 리더십을 유지할 수 있을 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 구성 요소별(2022-2035년)

제7장 시장 추산 및 예측 : 이동 수단별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 이용 산업별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

KTH 26.05.20The Global Robot Market was valued at USD 53.1 billion in 2025 and is estimated to grow at a CAGR of 17.6% to reach USD 257.5 billion by 2035.

Market growth is driven by rapid advancements in robotics, artificial intelligence, and machine learning, which are transforming operational processes across industries. These technologies are reshaping supply chain operations and enhancing customer-facing systems by enabling greater automation and precision. Modern robotic systems are designed with advanced sensing capabilities, intelligent motion planning, and enhanced adaptability, allowing them to perform complex tasks with high accuracy. Businesses are increasingly adopting robotic solutions to manage rising operational demands, improve efficiency, and reduce processing time. The growing need for faster and more accurate order handling is further accelerating the integration of robotics into logistics and operational workflows. In addition, increasing pressure on workforce productivity and operational scalability is encouraging organizations to adopt automation solutions that can handle repetitive and physically demanding tasks. As industries continue to focus on efficiency and performance optimization, the adoption of robotic systems is expected to expand significantly across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.1 Billion |

| Forecast Value | $257.5 Billion |

| CAGR | 17.6% |

The hardware segment generated USD 40.8 billion in 2025. Growth in this segment is supported by rising adoption of collaborative robots and continuous improvements in core robotic components. Advanced controllers, actuators, and end-effectors are enabling more precise and efficient robotic operations across a wide range of applications. Sensors play a crucial role in enhancing robotic functionality by allowing machines to detect their environment and operate autonomously. Increasing demand for sophisticated robotic systems capable of performing detailed and complex tasks is driving the adoption of advanced sensing technologies. These developments are strengthening the overall performance and reliability of robotic hardware, reinforcing its importance in the market.

The fixed robots segment accounted for USD 38.1 billion in 2025, reflecting its strong presence in the industry. This segment is benefiting from ongoing technological advancements in robotic design and engineering, which are improving performance and expanding application areas. Fixed robotic systems are widely utilized for tasks requiring high precision and consistency, making them essential in various industrial processes. Their ability to perform repetitive and hazardous operations with accuracy enhances workplace safety while improving productivity. As industries continue to invest in automation to achieve operational efficiency, demand for fixed robotic systems is expected to remain strong.

North America Robot Market held a 110.6% share in 2025, highlighting its advanced and innovation-driven ecosystem. The region demonstrates high adoption of automation technologies and benefits from a well-established network of robotics developers, integrators, and end users. Strong investment in advanced manufacturing and smart production environments is supporting market expansion. The United States plays a key role in driving regional growth, supported by an increasing focus on productivity enhancement and the need to address labor-related challenges. Continuous technological advancements and strategic investments are expected to sustain the region's leadership in the robot market.

Key companies operating in the Global Robot Market include ABB Ltd., Aethon, Blue Ocean Robotics, Boston Dynamics, Clearpath Robotics, Ecovacs Robotics, Fanuc Corporation, Intuitive Surgical, iRobot Corporation, Knightscope, Inc., and Medtronic. Companies in the Global Robot Market are strengthening their competitive position through continuous innovation and strategic expansion initiatives. Industry players are investing in advanced technologies such as AI integration, autonomous systems, and enhanced sensing capabilities to improve product performance and expand application areas. Organizations are forming partnerships and collaborations to accelerate research and development efforts and broaden their technological expertise. Market participants are also focusing on expanding their geographic presence and enhancing distribution networks to reach a wider customer base. In addition, companies are prioritizing customization and flexible solutions to meet specific industry requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Component trends

- 2.2.3 Mobility trends

- 2.2.4 Application trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in e-commerce and logistics demands

- 3.2.1.2 Increasing labor costs and labor shortages

- 3.2.1.3 Rising application of robot in healthcare

- 3.2.1.4 Growing popularity of Robotics-as-a-Service (RaaS)

- 3.2.1.5 Rapid technological developments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost

- 3.2.2.2 Technical complexity associated with robots

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of collaborative robots (cobots) across SMEs

- 3.2.3.2 Integration of AI and machine learning in robotics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Industrial robots

- 5.2.1 Articulated robots

- 5.2.2 Scara robots

- 5.2.3 Cartesian robots

- 5.2.4 Delta robots

- 5.2.5 Collaborative robots (cobots)

- 5.2.6 Parallel robots

- 5.2.7 Others

- 5.3 Service robots

- 5.3.1 Personal service robots

- 5.3.2 Professional service robots

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Mechanical component

- 6.2.1.1 Actuation & drive components

- 6.2.1.2 Joint & bearing systems

- 6.2.1.3 Springs & elastic components

- 6.2.1.4 Fastening & connection components

- 6.2.1.5 End effectors & tooling

- 6.2.1.6 Others

- 6.2.2 Electronic components

- 6.2.2.1 Motors and actuators

- 6.2.2.2 Sensors

- 6.2.2.3 Controllers and processors

- 6.2.2.4 Power supplies and batteries

- 6.2.2.5 Others

- 6.2.1 Mechanical component

- 6.3 Software

- 6.4 Services

- 6.4.1 Engineering and installation

- 6.4.2 Maintenance and Support

- 6.4.3 Training and education

Chapter 7 Market Estimates and Forecast, By Mobility, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fixed robotics

- 7.3 Mobile robotics

- 7.4 Humanoid robotics

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Assembly & production

- 8.3 Inspection & quality control

- 8.4 Material handling

- 8.5 Welding & soldering

- 8.6 Packaging & palletizing

- 8.7 Medical assistance

- 8.8 Security & surveillance

- 8.9 Retail & customer interaction robots

- 8.10 Education

- 8.11 Others

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Manufacturing & industrial

- 9.2.1 Automotive

- 9.2.2 Electronics & semiconductor

- 9.2.3 Food & beverage

- 9.2.4 Pharmaceuticals

- 9.2.5 Metal & machinery

- 9.2.6 Others

- 9.3 Healthcare

- 9.4 Defense

- 9.5 Agriculture

- 9.6 Household

- 9.7 Retail & e-commerce

- 9.8 Hospitality

- 9.9 Logistics

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 ABB Ltd.

- 11.1.2 Fanuc Corporation

- 11.1.3 KUKA AG

- 11.1.4 Yaskawa Electric Corporation

- 11.1.5 Mitsubishi Electric Corporation

- 11.1.6 Omron Corporation

- 11.1.7 Intuitive Surgical

- 11.1.8 Medtronic

- 11.2 Regional key players

- 11.2.1 Clearpath Robotics

- 11.2.2 MiR (Mobile Industrial Robots)

- 11.2.3 Staubli Group

- 11.2.4 Universal Robots

- 11.2.5 Aethon

- 11.3 Niche Players/Disruptors

- 11.3.1 Boston Dynamics

- 11.3.2 Blue Ocean Robotics

- 11.3.3 Ecovacs Robotics

- 11.3.4 iRobot Corporation

- 11.3.5 Knightscope, Inc.

- 11.3.6 Segway Robotics

- 11.3.7 SoftBank Robotics