|

시장보고서

상품코드

2038306

자동차용 LiDAR 센서 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive LiDAR Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

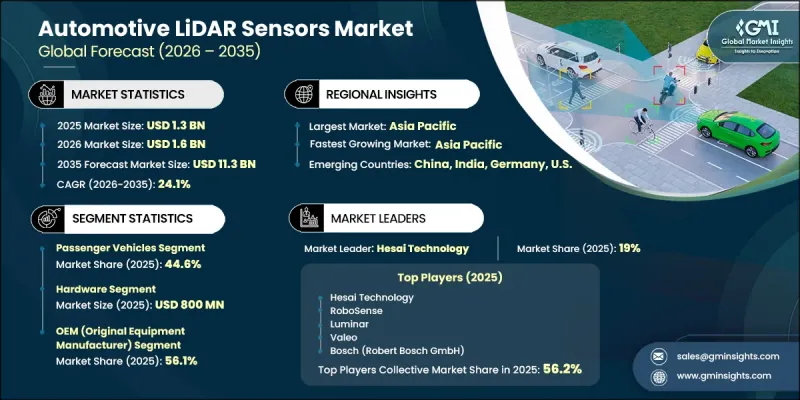

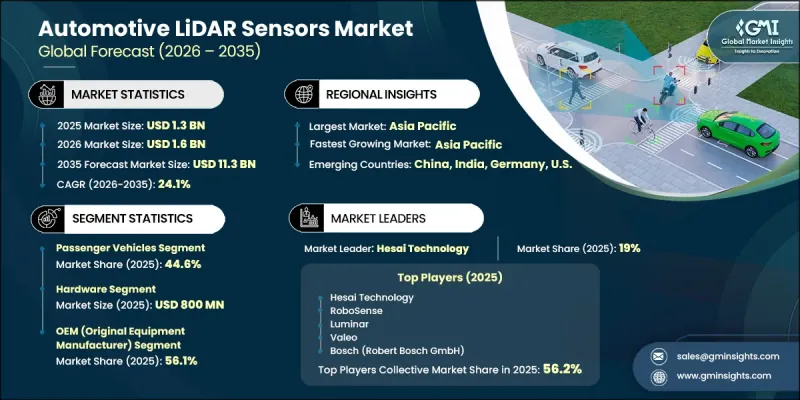

세계의 자동차용 LiDAR 센서 시장은 2025년에 13억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 24.1%로 성장이 전망되며, 113억 달러에 이를 것으로 추정되고 있습니다.

차량 안전, 고정밀 내비게이션, 실시간 환경 인식에 대한 관심이 높아짐에 따라 자동차 제조업체들은 고성능 인지 시스템 도입을 추진하고 있습니다. LiDAR 기술은 차세대 운전 기능에 필수적인 정확한 공간 매핑과 물체 감지를 실현할 수 있어 많은 관심을 받고 있습니다. 모빌리티 솔루션이 발전함에 따라 승용차 및 상용차 카테고리 모두에서 신뢰할 수 있는 고해상도 센서에 대한 수요가 지속적으로 증가하고 있습니다. 센서 설계의 지속적인 혁신, 비용 효율성 향상, 시스템 통합의 발전으로 센서의 보급이 더욱 가속화되고 있습니다. 또한, 안전에 대한 규제 강화와 지능형 교통 시스템(ITS)에 대한 수요 증가는 커넥티드카 및 자율주행차의 미래를 형성하는 데 있어 LiDAR의 중요성을 더욱 부각시키고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 13억 달러 |

| 예측 시장 규모 | 113억 달러 |

| CAGR | 24.1% |

자동차용 LiDAR 센서 시장은 현대 자동차의 첨단운전자보조시스템(ADAS)의 급속한 보급으로 인해 더욱 활성화되고 있습니다. 자동차 제조업체들은 인식 능력을 강화하고 자율주행 기능의 성능을 향상시키기 위해 LiDAR 시스템 탑재를 점점 더 많이 추진하고 있습니다. 이러한 자동화 수준 향상 추세는 보다 안전하고 신뢰할 수 있는 차량 운전을 위한 중요한 구성 요소로서 LiDAR의 역할을 강화하고 있습니다. 소비자의 기대가 안전과 편의성 향상으로 향함에 따라 첨단 센싱 기술에 대한 수요는 계속 증가하고 있으며, 이는 전체 시장의 성장을 뒷받침하고 있습니다.

승용차 부문은 고급차 및 중형차에서 첨단운전자보조시스템(ADAS)의 채택 확대에 힘입어 2025년 44.6%의 점유율을 차지했습니다. 각 제조업체들은 운전 성능과 운영 효율성을 향상시키기 위해 신차 플랫폼에 첨단 안전 기능과 자동화 기능을 탑재하고 있습니다. 안전과 첨단 기능에 대한 소비자의 관심이 높아지면서 이 분야에서 LiDAR 기술의 채택이 더욱 가속화되고 있으며, LiDAR의 선도적 입지를 더욱 공고히 하고 있습니다.

처리 장치 부문은 2035년까지 연평균 복합 성장률(CAGR) 26.6%를 나타낼 것으로 예측됩니다. 이러한 성장은 LiDAR 센서가 생성하는 복잡한 데이터를 처리할 수 있는 고성능 컴퓨팅 시스템에 대한 수요 증가에 기인합니다. 인공지능과 차량용 컴퓨팅 플랫폼을 포함한 처리 기술의 발전으로 실시간 데이터 분석과 신속한 의사결정이 가능해졌습니다. 자동 운전 시스템에는 빠르고 정확한 응답이 필요하기 때문에 고급 처리 장치에 대한 수요는 지속적으로 크게 증가하고 있습니다.

북미의 자동차용 LiDAR 센서 시장은 첨단 안전기술의 적극적인 도입과 차량 내 자율주행 기능의 통합이 진행됨에 따라 2025년 28.5%의 점유율을 차지했습니다. 이 지역은 연구개발에 대한 막대한 투자와 더불어 지능형 모빌리티 솔루션에 대한 관심이 높아지고 있는 것이 특징입니다. 자동차 제조업체들은 다양한 주행 조건에서의 성능 향상을 위해 LiDAR 탑재 시스템 개발을 적극적으로 추진하고 있습니다. 또한, 지원적인 규제 프레임워크와 운송 기술 혁신을 촉진하는 노력도 이 지역 시장 확대에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 차종별(2022-2035년)

제6장 시장 추산 및 예측 : 컴포넌트별(2022-2035년)

제7장 시장 추산 및 예측 : 판매 채널별(2022-2035년)

제8장 시장 추산 및 예측 : 기술 유형별(2022-2035년)

제9장 시장 추산 및 예측 : 통신 거리별(2022-2035년)

제10장 시장 추산 및 예측 : 용도별(2022-2035년)

제11장 시장 추산 및 예측 : 지역별(2022-2035년)

제12장 기업 개요

AJY 26.06.11The Global Automotive Lidar Sensors Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 24.1% to reach USD 11.3 billion by 2035.

Increasing emphasis on vehicle safety, precision navigation, and real-time environmental awareness is encouraging automakers to incorporate high-performance perception systems. LiDAR technology is gaining strong traction due to its ability to deliver accurate spatial mapping and object detection, which are critical for next-generation driving capabilities. As mobility solutions evolve, the demand for reliable, high-resolution sensors continues to rise across both passenger and commercial vehicle categories. Continuous innovation in sensor design, improved cost efficiency, and advancements in system integration are further supporting widespread adoption. Additionally, regulatory focus on safety and the growing need for intelligent transportation systems are reinforcing the importance of LiDAR in shaping the future of connected and autonomous vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $11.3 Billion |

| CAGR | 24.1% |

The automotive LiDAR sensors market is further supported by the rapid deployment of advanced driver assistance technologies in modern vehicles. Automakers are increasingly integrating LiDAR systems to enhance perception capabilities and improve the performance of automated driving features. This growing shift toward higher levels of automation is strengthening the role of LiDAR as a critical component in enabling safer and more reliable vehicle operation. As consumer expectations evolve toward enhanced safety and convenience, the demand for advanced sensing technologies continues to gain momentum, supporting overall market growth.

The passenger vehicles segment held a 44.6% share in 2025, driven by the rising adoption of advanced driver assistance systems in premium and mid-range vehicles. Manufacturers are integrating sophisticated safety and automation features into new vehicle platforms to enhance driving performance and operational efficiency. Increasing consumer focus on safety and advanced functionality is further accelerating the adoption of LiDAR technology within this segment, reinforcing its leading position.

The processing unit segment is anticipated to grow at a CAGR of 26.6% through 2035. This growth is attributed to the increasing need for high-performance computing systems capable of processing complex data generated by LiDAR sensors. Advancements in processing technologies, including artificial intelligence and in-vehicle computing platforms, enable real-time data interpretation and faster decision-making. As autonomous driving systems require rapid and accurate responses, demand for advanced processing units continues to rise significantly.

North America Automotive Lidar Sensors Market accounted for 28.5% share in 2025, supported by the strong adoption of advanced safety technologies and the increasing integration of autonomous features in vehicles. The region is characterized by significant investments in research and development, along with a growing focus on intelligent mobility solutions. Automakers are actively developing LiDAR-enabled systems to improve performance across varying driving conditions. Supportive regulatory frameworks and initiatives promoting innovation in transportation technologies are further contributing to market expansion across the region.

Key companies operating in the Global Automotive Lidar Sensors Market include Luminar Technologies, Ouster Inc., Innoviz Technologies, Hesai Technology, RoboSense (Suteng Innovation), Valeo, Continental AG, Bosch (Robert Bosch GmbH), Denso Corporation, Aeva Technologies, Cepton Inc., Quanergy Solutions, Ibeo Automotive Systems, and Sony Semiconductor Solutions. Companies in the Automotive Lidar Sensors Market are focusing on technological innovation and strategic collaborations to strengthen their competitive position. They are investing heavily in research and development to improve sensor accuracy, range, and cost efficiency while enhancing scalability for mass production. Partnerships with automotive manufacturers and technology firms are helping accelerate integration into next-generation vehicles. Companies are also expanding production capabilities and optimizing supply chains to meet growing demand. Emphasis on software development, including AI-driven perception systems, is improving data processing and real-time decision-making capabilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vehicle type trends

- 2.2.2 Component trends

- 2.2.3 Sales channel trends

- 2.2.4 Technology type trends

- 2.2.5 Range capability trends

- 2.2.6 Application trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of ADAS and semi-autonomous driving features

- 3.2.1.2 Strong push for vehicle safety and evolving regulatory expectations

- 3.2.1.3 Rising demand for 3D mapping and high-definition environmental modeling

- 3.2.1.4 Growing use of LiDAR in commercial vehicles and intelligent mobility ecosystems

- 3.2.1.5 Rapid advancements in low-cost solid-state and FMCW LiDAR

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of LiDAR sensors and system integration

- 3.2.2.2 Limited readiness of supporting autonomous driving infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Growing integration of LiDAR in Level 3 and Level 4 vehicle platforms

- 3.2.3.2 Expansion of LiDAR-enabled smart mobility and commercial fleet automation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.3 Commercial vehicles

- 5.4 Off-road vehicles

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Processing unit

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 OEM (original equipment manufacturer)

- 7.3 Tier-1 supplier

Chapter 8 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Mechanical LiDAR

- 8.3 Solid-state LiDAR

- 8.3.1 MEMS-based LiDAR

- 8.3.2 Flash LiDAR

- 8.3.3 Optical phased array (OPA) LiDAR

- 8.3.4 FMCW LiDAR

- 8.4 Hybrid LiDAR

Chapter 9 Market Estimates and Forecast, By Range Capability, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Short-range (<50 meters)

- 9.3 Mid-range (50-170 meters)

- 9.4 Long-range (>170 meters)

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 L2+ ADAS

- 10.3 L3-L5 autonomous driving

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Hesai Technology

- 12.1.2 RoboSense

- 12.1.3 Luminar

- 12.1.4 Valeo

- 12.1.5 Bosch (Robert Bosch GmbH)

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Ouster Inc.

- 12.2.1.2 Aeva Technologies

- 12.2.1.3 Cepton Inc.

- 12.2.1.4 Quanergy Solutions

- 12.2.2 Asia Pacific

- 12.2.2.1 Denso Corporation

- 12.2.2.2 Sony Semiconductor Solutions

- 12.2.3 Europe

- 12.2.3.1 Ibeo Automotive Systems

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Innoviz Technologies

- 12.3.2 Muetec Inc.