|

시장보고서

상품코드

2038379

단백질 분말 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Protein Powder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

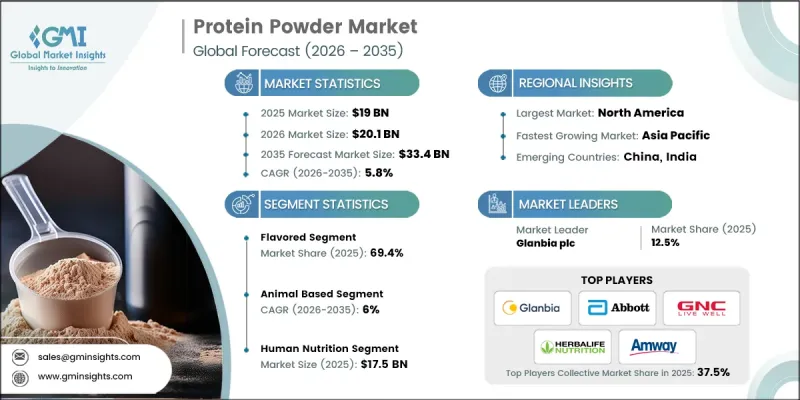

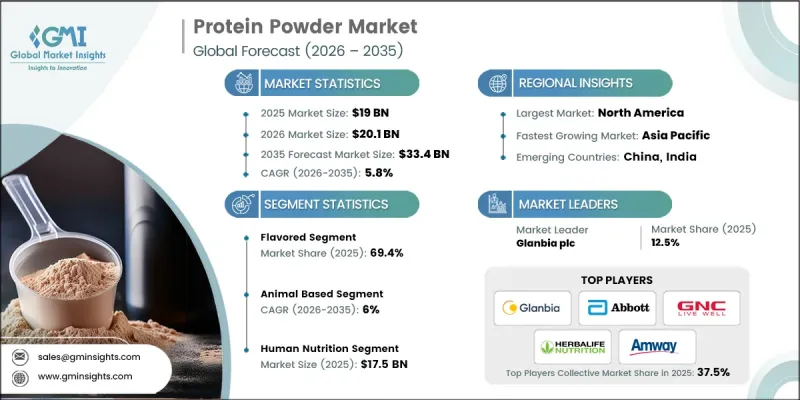

세계의 단백질 분말 시장은 2025년에 190억 달러로 평가되었고, CAGR 5.8%로 성장할 전망이며, 2035년까지 334억 달러에 이를 것으로 추정되고 있습니다.

소비자의 취향이 건강한 라이프 스타일, 기능성 영양 및 혁신적인 제품으로 이동함에 따라 이 산업은 꾸준히 발전하고 있습니다. 지속가능성, 소화기 건강, 윤리적 소싱에 대한 인식이 높아지면서 식물성 및 혼합 단백질 제품으로의 전환이 가속화되고 있습니다. 동시에 제형 기술의 발전으로 맛, 식감, 영양소 흡수율이 향상되어 더 많은 소비자층에게 매력적인 제품이 되었습니다. 개인화가 중요한 트렌드로 떠오르면서 각 브랜드는 개인의 식생활과 건강 목표에 맞는 맞춤형 단백질 솔루션을 도입하고 있습니다. 기능성 성분과 디지털을 활용한 영양 계획도 제품 차별화를 촉진하고 있습니다. 전통적인 단백질 공급원은 여전히 확고한 지위를 유지하고 있지만, 식습관의 변화에 따라 대체 단백질이 점점 더 많은 인기를 얻고 있습니다. 피트니스, 임상 영양 및 일반 웰빙 분야에서 단백질 분말의 역할이 확대되면서 장기적인 시장 성장에 더욱 박차를 가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 190억 달러 |

| 예측 시장 규모 | 334억 달러 |

| CAGR | 5.8% |

향이 첨가된 단백질 분말는 2025년 69.4%의 점유율을 차지했으며, 2035년까지 연평균 5.8%의 성장률을 보일 것으로 예측됩니다. 이 제품들은 맛의 향상, 섭취의 용이성, 그리고 접근성의 용이성 때문에 여전히 높은 인기를 누리고 있습니다. 편리하고 즐길 수 있는 영양 보충 옵션에 대한 소비자의 강한 선호가 수요를 주도하고 있으며, 이 부문은 경쟁이 치열하고 판매량을 중시하는 경향이 있습니다.

운동선수 및 보디빌더 부문은 2025년 28%의 점유율을 차지했으며, 2035년까지 연평균 5.5%의 연평균 복합 성장률(CAGR)을 보일 것으로 전망됩니다. 이 부문은 근육 강화 및 성능 향상에 대한 요구로 인해 계속해서 주요 소비자층을 차지하고 있습니다. 동시에 근력 유지 및 회복을 지원하고자 하는 노년층의 확대도 수요 증가에 기여하고 있습니다. 또한, 피트니스 트렌드의 변화와 라이프스타일의 변화에 영향을 받아 젊은 층에서도 단백질 제품 이용이 점점 더 확대되고 있습니다.

북미의 단백질 분말 시장은 2026-2035년 연평균 복합 성장률(CAGR) 6.4%를 나타낼 것으로 예측됩니다. 이 지역은 높은 소비자 인식, 선진적인 제품 혁신, 그리고 개인화된 클린 라벨 영양 제품의 보급 확대에 힘입어 탄탄한 입지를 유지하고 있습니다. 기존 시장 진출기업의 존재와 디지털 소매 채널의 급속한 확장은 다양한 소비자층에서 시장 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 소스별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제9장 시장 추산 및 예측 : 유통 채널별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

AJYThe Global Protein Powder Market was valued at USD 19 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 33.4 billion by 2035.

The industry is evolving steadily as consumer preferences shift toward healthier lifestyles, functional nutrition, and innovative product offerings. Growing awareness of sustainability, digestive wellness, and ethical sourcing is accelerating the transition toward plant-based and blended protein formulations. At the same time, advancements in formulation technologies are improving taste, texture, and nutrient absorption, making products more appealing to a broader consumer base. Personalization is becoming a key trend, with brands introducing customized protein solutions aligned with individual dietary needs and wellness goals. Functional ingredients and digitally supported nutrition planning are also enhancing product differentiation. While traditional protein sources continue to maintain a strong foothold, alternative proteins are gaining momentum due to changing dietary habits. The expanding role of protein powders across fitness, clinical nutrition, and general wellness applications is further supporting long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19 Billion |

| Forecast Value | $33.4 Billion |

| CAGR | 5.8% |

Flavored protein powder accounted for 69.4% share in 2025 and is expected to grow at a CAGR of 5.8% through 2035. These products remain highly popular due to their enhanced taste profiles, ease of consumption, and widespread availability. Strong consumer preference for convenient and enjoyable nutrition options continues to drive demand, making this segment highly competitive and volume-focused.

The athletes and bodybuilders segment held a share of 28% in 2025 and is anticipated to grow at a CAGR of 5.5% by 2035. This segment continues to represent a major consumer base due to the need for muscle development and performance enhancement. At the same time, an expanding demographic of older consumers is contributing to demand, driven by the need to maintain strength and support recovery. Younger populations are also increasingly adopting protein-based products, influenced by evolving fitness trends and lifestyle changes.

North America Protein Powder Market is expected to grow at a CAGR of 6.4% during 2026-2035. The region maintains a strong position due to high consumer awareness, advanced product innovation, and increasing adoption of personalized and clean-label nutrition. The presence of established industry participants and the rapid expansion of digital retail channels are further supporting market growth across diverse consumer segments.

Key companies operating in the Protein Powder Market include Abbott Laboratories, Glanbia plc, Amway Corporation, Nestle S.A., GNC Holdings Inc., Herbalife Nutrition Ltd., Tata Consumer Products, Melaleuca Inc., Atlantic Multipower UK Limited, and GSK Consumer Healthcare (Haleon). Companies in the protein powder market are strengthening their market position by investing in research and development to introduce innovative formulations with improved taste, texture, and nutritional value. They are expanding their product portfolios to include plant-based, blended, and functional protein options that cater to evolving consumer preferences. Strategic partnerships and collaborations are being utilized to enhance distribution networks and expand global reach. Firms are also focusing on digital transformation, leveraging e-commerce platforms and personalized nutrition tools to engage consumers directly. In addition, companies are emphasizing clean-label ingredients, sustainable sourcing, and transparent branding to build trust. Enhanced marketing strategies and influencer-driven campaigns are further supporting brand visibility and customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Source

- 2.2.4 Application

- 2.2.5 End-user

- 2.2.6 Distribution channel

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LATAM

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Unflavored

- 5.3 Flavored (Chocolate, Vanilla, Strawberry, Others)

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Plant-Based

- 6.2.1 Soy

- 6.2.2 Pea

- 6.2.3 Rice

- 6.2.4 Hemp

- 6.2.5 Spirulina

- 6.2.6 Wheat

- 6.2.7 Mixed Plant

- 6.2.8 Others

- 6.3 Animal-Based

- 6.3.1 Whey Protein

- 6.3.2 Whey Concentrate

- 6.3.3 Whey Isolate

- 6.3.4 Whey Hydrolysate

- 6.3.5 Casein

- 6.3.6 Egg Protein

- 6.3.7 Collagen

- 6.3.8 Insect Protein

- 6.3.9 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Human Nutrition

- 7.2.1 Sports Nutrition

- 7.2.2 Functional Foods

- 7.2.3 Weight Management

- 7.2.4 Clinical/Medical

- 7.2.5 General Wellness

- 7.3 Animal Nutrition

- 7.3.1 Aquaculture

- 7.3.2 Poultry

- 7.3.3 Swine

- 7.3.4 Cattle

- 7.3.5 Equine

- 7.3.6 Others

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Athletes & Bodybuilders

- 8.2.1 Professional Athletes

- 8.2.2 Amateur Bodybuilders

- 8.3 Fitness Enthusiasts

- 8.3.1 Gym-Goers

- 8.3.2 Recreational Exercisers

- 8.4 Health-Conscious

- 8.4.1 Weight Management

- 8.4.2 General Wellness

- 8.5 Clinical/Medical Users

- 8.5.1 Post-Surgery Recovery

- 8.5.2 Malnutrition Treatment

- 8.5.3 Aging & Sarcopenia

- 8.6 Teenage & Youth

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Online Retail

- 9.2.1 E-commerce Platforms

- 9.2.2 D2C Websites

- 9.2.3 Subscription Services

- 9.3 Supermarkets/Hypermarkets

- 9.3.1 Modern Trade Chains

- 9.3.2 Traditional Supermarkets

- 9.4 Specialty Stores

- 9.4.1 Nutrition & Health Food

- 9.4.2 Supplement Specialty

- 9.5 Pharmacies/Drugstores

- 9.5.1 Chain Pharmacies

- 9.5.2 Independent Pharmacies

- 9.6 Others

- 9.6.1 Gyms & Fitness Centers

- 9.6.2 Direct Sales

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Glanbia plc

- 11.2 Abbott Laboratories

- 11.3 GNC Holdings, Inc.

- 11.4 Herbalife Nutrition Ltd.

- 11.5 Amway Corporation

- 11.6 Nestle S.A.

- 11.7 GSK Consumer Healthcare (Haleon)

- 11.8 Melaleuca Inc.

- 11.9 Atlantic Multipower UK Limited

- 11.10 Tata Consumer Products