|

시장보고서

상품코드

2038653

택배, 익스프레스 및 소포 서비스 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Courier, Express and Parcel Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

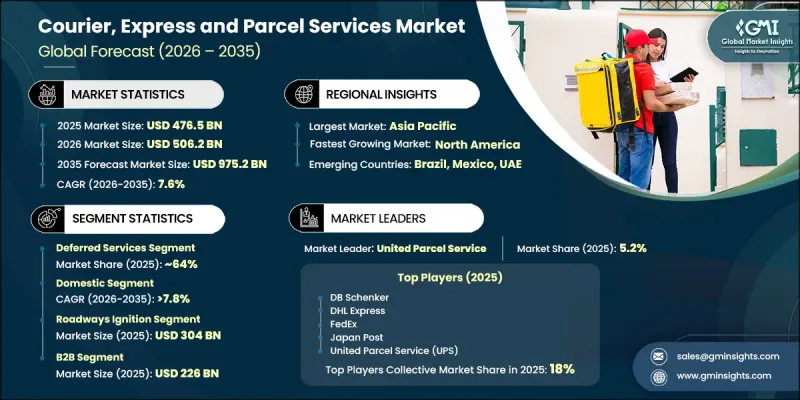

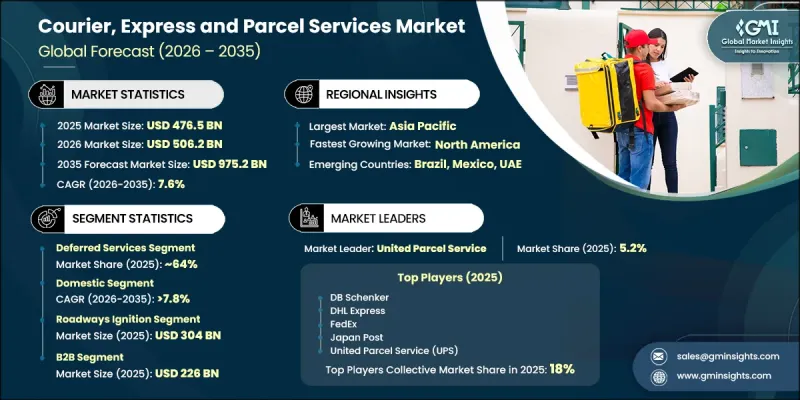

세계의 택배, 익스프레스 및 소포 서비스 시장은 2025년에 4,765억 달러로 평가되었고, CAGR 7.6%로 성장할 전망이며, 2035년까지 9,752억 달러에 이를 것으로 예측됩니다.

디지털 커머스가 소비자의 구매 행동과 물류에 대한 기대치를 끊임없이 변화시키고 있는 가운데, 택배, 익스프레스 및 소포 서비스 산업은 빠르게 성장하고 있습니다. 더 빠른 배송, 배송 상황의 가시성, 그리고 신뢰할 수 있는 서비스 성능에 대한 요구가 높아지면서 물류 사업자의 역량 향상에 대한 요구가 증가하고 있습니다. 소매, 제조, 유통 업계의 기업들은 고객의 기대에 부응하기 위해 풀필먼트의 효율성과 라스트 마일 연결성을 강화하는 데 점점 더 집중하고 있습니다. 배송 속도와 비용 최적화의 균형을 맞추기 위해 기업들은 유연한 물류 모델과 확장 가능한 배송 네트워크를 도입하고 있습니다. 동시에, 도시 및 외딴 지역의 배송량 증가는 인프라 투자와 서비스 혁신을 촉진하고 있습니다. 또한, 업계는 고객 경험 향상, 업무 민첩성 향상, 일관된 서비스 품질 제공에 중점을 두는 방향으로 진화하고 있습니다. 그 결과, 택배, 익스프레스 및 소포 서비스 시장은 세계 무역, 전자상거래의 성장, 통합된 공급망 운영을 지원하는 고도의 기술 주도형 생태계로 변모하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 4,765억 달러 |

| 예측 시장 규모 | 9,752억 달러 |

| CAGR | 7.6% |

디지털 기술의 발전은 업무 효율성과 배송 정확도를 향상시킴으로써 택배, 익스프레스 및 소포 서비스 산업의 양상을 크게 바꾸고 있습니다. 지능형 경로 설정 시스템, 자동화된 소포 처리 및 고급 추적 플랫폼의 통합으로 보다 신속하고 안정적인 물류 업무를 가능하게 합니다. 각 업체들은 데이터 기반 솔루션을 활용하여 워크플로우 효율화, 운송 시간 단축, 배송 투명성 향상을 위해 노력하고 있습니다. 또한, 지속가능성에 대한 관심이 높아지면서 에너지 효율이 높은 운송 수단과 최적화된 경로 계획의 도입이 촉진되고 있습니다. 이러한 추세는 기존의 배송 모델을 혁신하고 서비스 제공업체가 다양한 시장 부문에서 서비스 성능을 향상시키면서 보다 신속하고 확장 가능하며 비용 효율적인 물류 네트워크를 구축할 수 있게 해줍니다.

지연 배송 서비스 부문은 2025년 64%의 점유율을 차지했으며, 2035년까지 연평균 7.8%의 성장률을 보일 것으로 전망됩니다. 이 부문은 비용 효율성이 뛰어나고 즉각적인 배송이 필요하지 않은 대량의 화물을 처리하는 데 적합하기 때문에 선도적인 지위를 유지하고 있습니다. 기업들은 유통 전략의 최적화, 운영 비용 관리, 일관된 배송 일정 유지를 위해 지연 배송 솔루션에 의존하고 있습니다. 기업들이 물류 업무의 효율성과 확장성을 최우선시하는 가운데, 이러한 서비스가 여러 산업에서 널리 활용되고 있다는 점은 안정적인 수요를 보장합니다.

도로 운송 부문은 2025년 3,040억 달러 시장 규모를 기록했으며, 택배, 익스프레스 및 소포 서비스 시장에서 주요 운송 수단으로 우위를 점하고 있습니다. 도로 기반 물류 네트워크는 유연성, 접근성 및 직접적인 연결성을 제공하기 때문에 지역 및 지역 배송 모두에서 매우 효과적입니다. 효율적인 라스트마일 업무를 유지하면서 대량의 화물을 처리할 수 있는 능력은 현대 물류 시스템에서 중요한 역할을 하고 있음을 입증합니다. 도로 운송의 적응성은 서로 다른 배송 채널 간의 원활한 통합을 가능하게 하여 다양한 지역에 걸쳐 일관된 서비스 제공을 지원합니다.

2025년 중국의 택배, 익스프레스 및 소포 서비스 시장은 57%의 점유율을 차지했으며, 1,099억 달러 시장 규모를 기록했습니다. 탄탄한 물류 인프라와 높은 디지털 커머스 보급률로 인해 이 나라는 계속해서 지역 시장을 주도하고 있습니다. 첨단 물류 시스템 및 배송 역량에 대한 지속적인 투자를 통해 업무 효율성과 배송 성능을 강화하고 있습니다. 또한, 각 기업들이 배송 네트워크 확장, 라스트마일 솔루션 개선, 국경 간 물류 역량 강화에 투자하면서 다른 지역 시장도 성장세를 보이고 있으며, 이는 아시아태평양의 택배, 익스프레스 및 소포 서비스 산업 전체 성장에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 서비스별(2022-2035년)

제6장 시장 추산 및 예측 : 운송 수단별(2022-2035년)

제7장 시장 추산 및 예측 : 고객별(2022-2035년)

제8장 시장 추산 및 예측 : 목적지별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

AJY 26.06.11The Global Courier, Express and Parcel Services Market was valued at USD 476.5 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 975.2 billion by 2035.

The courier, express and parcel services industry is expanding rapidly as digital commerce continues to reshape consumer purchasing behavior and logistics expectations. Rising demand for faster delivery timelines, improved shipment visibility, and dependable service performance is pushing logistics providers to upgrade their capabilities. Businesses across retail, manufacturing, and distribution are increasingly focused on strengthening fulfillment efficiency and last-mile connectivity to meet customer expectations. The need to balance delivery speed with cost optimization is encouraging companies to adopt flexible logistics models and scalable delivery networks. At the same time, increasing shipment volumes across both urban and remote areas are driving investments in infrastructure and service innovation. The industry is also evolving with a strong emphasis on enhancing customer experience, improving operational agility, and delivering consistent service quality. As a result, the courier, express and parcel services market continues to transform into a highly technology-driven ecosystem that supports global trade, e-commerce growth, and integrated supply chain operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $476.5 Billion |

| Forecast Value | $975.2 Billion |

| CAGR | 7.6% |

Advancements in digital technologies are significantly transforming the courier, express and parcel services landscape by improving operational efficiency and delivery accuracy. The integration of intelligent routing systems, automated parcel handling, and advanced tracking platforms is enabling faster and more reliable logistics operations. Companies are leveraging data-driven solutions to streamline workflows, reduce transit times, and enhance shipment transparency. In addition, the growing focus on sustainability is encouraging the adoption of energy-efficient transportation methods and optimized route planning. These developments are reshaping traditional delivery models, allowing service providers to build more responsive, scalable, and cost-effective logistics networks while delivering improved service performance across diverse market segments.

The deferred services segment accounted for 64% share in 2025 and is projected to grow at a CAGR of 7.8% through 2035. This segment maintains a leading position due to its cost efficiency and suitability for handling large shipment volumes that do not require immediate delivery. Businesses rely on deferred solutions to optimize distribution strategies, manage operational costs, and maintain consistent delivery timelines. The widespread use of these services across multiple industries ensures stable demand, as companies continue to prioritize efficiency and scalability in their logistics operations.

The roadways segment generated USD 304 billion in 2025, reflecting its dominance as the primary mode of transportation within the courier, express and parcel services market. Road-based logistics networks offer flexibility, accessibility, and direct connectivity, making them highly effective for both regional and local deliveries. Their ability to support high shipment volumes while maintaining efficient last-mile operations reinforces their critical role in modern logistics systems. The adaptability of road transportation enables seamless integration across different delivery channels, supporting consistent service execution across diverse geographic areas.

China Courier, Express and Parcel Services Market accounted for 57% share in 2025, generating USD 109.9 billion. The country continues to lead the regional landscape due to its strong logistics infrastructure and high level of digital commerce adoption. Ongoing investments in advanced logistics systems and distribution capabilities are strengthening operational efficiency and delivery performance. Other regional markets are also gaining momentum as companies invest in expanding delivery networks, improving last-mile solutions, and enhancing cross-border logistics capabilities, contributing to the overall growth of the Asia Pacific courier, express and parcel services industry.

Key companies operating in the Global Courier, Express and Parcel Services Market include DHL Express, FedEx, United Parcel Service, DB Schenker, SF Express, Japan Post, Royal Mail, La Poste, TNT Express, and Yamato. Companies in the Courier, Express and Parcel Services Market are focusing on strengthening their competitive position through investments in automation, digital platforms, and advanced analytics to enhance operational efficiency and service quality. Strategic expansion of logistics networks and fulfillment centers is enabling faster delivery and broader geographic coverage. Partnerships, mergers, and collaborations are being used to improve service capabilities and market reach. Firms are also prioritizing customer-centric solutions, including flexible delivery options and real-time tracking, to enhance user experience. Sustainability initiatives such as optimized routing and eco-friendly transportation are gaining importance. Continuous innovation and infrastructure development are helping companies maintain long-term growth and competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Transportation Mode

- 2.2.4 Customer

- 2.2.5 Destination

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Expansion of E-commerce

- 3.2.1.2 Rising Demand for Faster Deliveries

- 3.2.1.3 Technological Advancements

- 3.2.1.4 Growth in Cross-Border Trade

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Last-Mile Delivery Costs

- 3.2.2.2 Labor Shortages & Operational Complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of Sustainable Delivery Solutions

- 3.2.3.2 Expansion of Same Day & Hyperlocal Delivery

- 3.2.3.3 Green Logistics Initiatives

- 3.2.3.4 Digital Payment & Tracking Solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis (Driven by Primary Research)

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S.: FAA, DOT, FMCSA regulations

- 3.5.1.2 Canada: Transport Canada, Canada Post regulations

- 3.5.2 Europe

- 3.5.2.1 Germany: BMDV, EU delivery standards

- 3.5.2.2 France: Ministry of Transport, EU directives

- 3.5.2.3 UK: Department for Transport, EU/UK compliance

- 3.5.2.4 Italy: Ministry of Infrastructure & Transport

- 3.5.3 Asia Pacific

- 3.5.3.1 China: MIIT, China Post regulations

- 3.5.3.2 Japan: MLIT, Japan Post regulations

- 3.5.3.3 South Korea: MOLIT, national postal standards

- 3.5.3.4 India: MoRTH, India Post regulations

- 3.5.4 Latin America

- 3.5.4.1 Brazil: ANTT, DENATRAN regulations

- 3.5.4.2 Mexico: Ministry of Communications & Transport

- 3.5.5 Middle East and Africa

- 3.5.5.1 UAE: RTA, ESMA Regulations

- 3.5.5.2 Saudi Arabia: Ministry of Transport, SASO Standards

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 Gen AI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Deferred Services

- 5.3 Courier Services

- 5.4 International Services

- 5.5 Same-Day Delivery

Chapter 6 Market Estimates & Forecast, By Transportation Mode, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Roadways

- 6.3 Railways

- 6.4 Airways

- 6.5 Waterways

Chapter 7 Market Estimates & Forecast, By Customer, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 B2B

- 7.3 B2C

- 7.4 C2C

Chapter 8 Market Estimates & Forecast, By Destination, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Domestic

- 8.3 International

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 E-commerce

- 9.3 Retail

- 9.4 Manufacturing

- 9.5 Healthcare

- 9.6 Financial Services

- 9.7 IT and Telecommunications

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 DB Schenker

- 11.1.2 DHL Express

- 11.1.3 FedEx

- 11.1.4 Japan Post

- 11.1.5 La Poste

- 11.1.6 Royal Mail

- 11.1.7 SF Express

- 11.1.8 TNT Express

- 11.1.9 United Parcel Service

- 11.1.10 Yamato

- 11.2 Regional Player

- 11.2.1 Aramex

- 11.2.2 Blue Dart Express

- 11.2.3 Canada Post

- 11.2.4 China Post

- 11.2.5 General Logistics Systems

- 11.2.6 Kerry Logistics

- 11.2.7 PostNL

- 11.2.8 Purolator

- 11.2.9 Seur

- 11.2.10 SF International