|

시장보고서

상품코드

2066618

스페인의 택배, 특송, 소포(CEP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spain Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

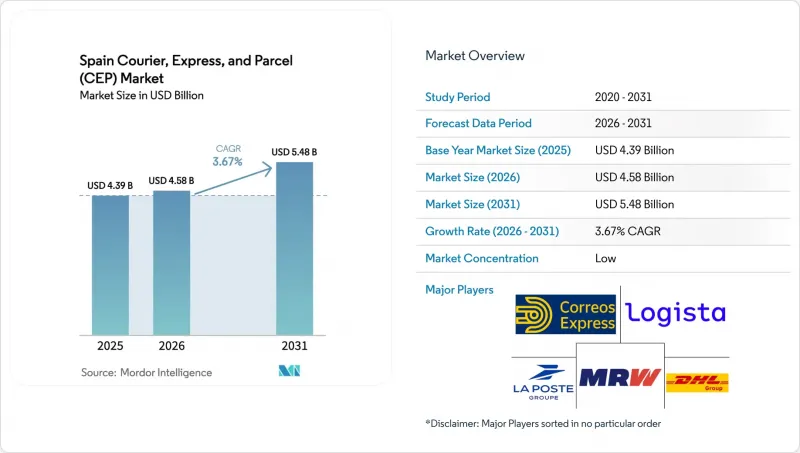

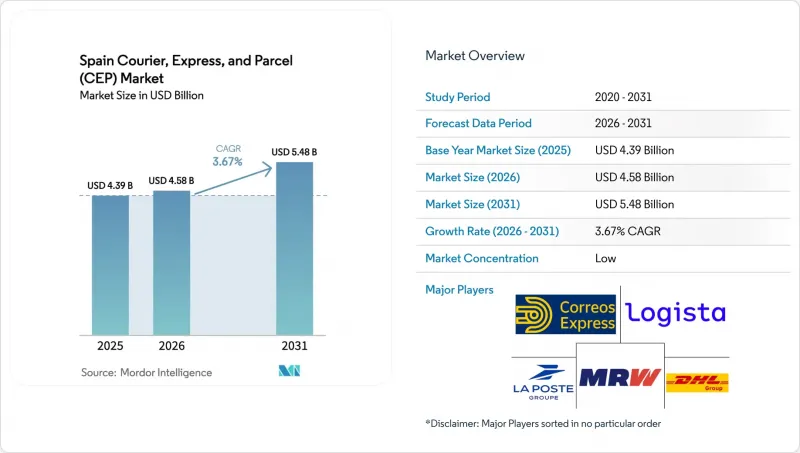

Mordor Intelligence에 의하면, 스페인의 택배, 특송, 소포(CEP) 시장 규모는 2025년에 43억 9,000만 달러로 평가되었습니다. 2026년 45억 8,000만 달러에서 2031년까지 54억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 3.67%를 나타낼 전망입니다.

스페인의 두 자릿수 전자상거래 보급률, 22%라는 높은 수준을 유지하는 반품률, 그리고 콜드체인 서비스에 대한 수요 증가로 인해 소포 처리량은 증가 추세를 이어가고 있습니다. 본 보고서는 배송지(국내, 국제), 배송 속도(특급, 비특급), 모델(B2B 등), 출하 중량(중량물, 경량물, 중경량물), 운송 수단(항공, 육상, 기타), 최종 사용자 산업(전자상거래, 금융 서비스 등)별로 세분화되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

스페인의 택배, 특송, 소포(CEP) 시장 동향 및 인사이트

스페인의 전자상거래 반품률 22%가 주도하는 역물류의 급증

22%에 육박하는 반품률은 스페인을 유럽에서 가장 과제가 많은 전자상거래 환경 중 하나로 만들고 있으며, 사업자들은 양방향 물류 흐름에 대응하기 위해 허브 앤 스포크형 네트워크 재구축을 추진하는 한편, 물류 센터 내에 검수 및 재생 라인을 설치하고 있습니다. 반품의 대부분은 의류 및 신발이 차지하고 있으며, 사이즈에 대한 불확실성이나 여러 사이즈를 구매하는 경우로 인해 반품률이 30% 이상의 경우도 드물지 않습니다. C2C(개인 간) 마켓플레이스는 모든 C2C 배송에서 취급 거점 수가 두 배로 늘어남에 따라 양방향 물류에 또 다른 차원을 더하고 있습니다. 전용 역물류 역량과 재고 가시화 플랫폼에 투자하는 기업들은 기존의 비용 센터를 차별화의 원천으로 전환해 나가고 있습니다. 더 많은 브랜드가 회수 프로그램을 도입함에 따라, 스페인의 택배, 특송, 소포(CEP) 시장에서 역방향 물류 처리량은 향후 5년 동안 정방향 배송의 성장률을 상회할 것으로 예측됩니다.

AI를 활용한 동적 경로 계획 및 적재량 최적화를 통해 킬로미터당 비용을 절감

교통 상황, 기상 정보, 과거 배송 패턴을 분석하는 머신러닝 알고리즘을 통해 간선 운송 및 라스트 마일 비용을 12-18% 절감할 수 있게 되었습니다. 실시간 배송 순서 재편을 통해 바르셀로나의 혼잡한 노선에서 시간당 정차 횟수가 20% 이상 증가했으며, 플랫폼 주도의 운임 압박에도 불구하고 운송 사업자들은 이익률을 유지할 수 있게 되었습니다. 아마존의 아스투리아스 시설과 같은 자본 집약형 로봇 허브에서는 AI를 활용한 분류 작업과 무인 운반차(AGV)를 결합하여 성수기의 처리 능력을 유지하고 있습니다. 데이터 사이언스 인력에 대한 투자가 어려운 중견 서비스 제공업체들은 화이트라벨 SaaS 최적화 도구를 도입하거나 기술 기업과 제휴하는 사례가 늘어나고 있어, 스페인의 택배, 특송, 소포(CEP) 시장에서 경쟁사 간의 역량 격차가 확대되고 있습니다.

골판지, 연료, 냉매 가격의 급등으로 인해 단위 비용이 8% 이상 상승했습니다.

펄프 부족으로 골판지 가격이 15-20% 급등하고, 디젤 연료 가격이 리터당 1.20-1.60유로 사이에서 등락했으며, F가스의 단계적 감축으로 인해 냉매 비용이 상승함에 따라 2025년에는 전반적으로 이익률이 압박을 받았습니다. 운송업체는 연료 헤지를 실시하고 포장 자재에 대한 고정 가격 계약을 체결했으나, 수주의 80% 이상을 차지하는 대형 플랫폼은 가격 조정에 저항했습니다. 중소규모 통신사업자들은 가격 급등을 흡수할 여력이 제한적이었기 때문에 스페인의 택배, 특송, 소포(CEP) 시장에서 방어적 합병이 진행되었으며, AI를 활용한 효율화 방안 마련에 더욱 주력하게 되었습니다.

부문별 분석

2025년, 제조업은 스페인의 택배, 특송, 소포(CEP) 시장 점유율의 32.41%를 차지했으며, 이는 카탈루냐주와 나바라주에서 자동차 및 기계의 꾸준한 생산에 힘입은 결과였습니다. 제조업과 관련된 스페인의 택배, 특송, 소포(CEP) 시장은 여전히 견조한 모습을 보이고 있지만, 산업 생산 주기에 연동되어 한 자릿수 중반대의 완만한 성장에 그치고 있습니다.

C2C 재판매를 포함한 전자상거래 소포 시장은 패션, 전자기기, 가정용품 분야의 온라인 침투 심화에 힘입어 2031년까지 연평균 성장률(CAGR) 4.00%를 기록하며 성장할 것으로 전망됩니다. 제조업체들은 예비 부품 조달에 B2B 전자상거래 포털을 점점 더 많이 도입하고 있으며, 이를 통해 예측 가능한 소량 출하를 촉진하고 있습니다. 한편, 패션 소매업체들은 30% 이상의 반품률에 대응하기 위해 역물류 허브를 활용하고 있습니다. 금융 서비스는 수익성이 높은 서류 배송을 뒷받침하고 있으며, GDP 규제가 강화됨에 따라 의료 분야의 발송업체들은 프리미엄 특급 배송 서비스를 이용하고 있습니다. 최종 사용자의 다양화로 인해 특정 부문 고유의 변동성이 완화되면서, 스페인의 택배, 특송, 소포(CEP) 시장에서 여러 업종을 아우르는 네트워크를 운영할 수 있는 사업자가 유리한 입지를 점하고 있습니다.

2025년, 국내 소포 시장은 스페인의 택배, 특송, 소포(CEP) 시장 규모의 63.92%를 차지했으나, 도시권 시장이 서비스 포화 상태에 이르면서 성장 둔화에 직면해 있습니다. 국제 물류 시장은 EU 부가가치세(VAT)의 조화와 150유로 미만 화물에 대한 통관 절차의 번거로움을 줄여주는 IOSS 규정의 뒷받침을 받아, 2031년까지 연평균 성장률(CAGR) 3.80%를 나타낼 것으로 전망됩니다.

국경을 넘는 성장은 스페인·프랑스·독일 간 운송 경로에 집중되어 있으며, 수소 트럭 실증 실험과 연간 1만 1,500회의 트럭 운행을 줄이는 철도·도로 복합 운송 서비스에 의해 뒷받침되고 있습니다. 또한, 스페인의 수출업체들은 문화적 친화성과 시차적 이점을 활용하여 UPS의 Estafeta 네트워크를 통해 라틴아메리카로의 수출을 확대되고 있습니다. 국제 거래 구조의 다양화에 따라, 각 운송사는 통관 업무 역량을 강화하는 한편, 스페인의 택배, 특송, 소포(CEP) 시장 전반에 걸쳐 다중 통화 및 다국어를 지원하는 고객 포털에 대한 투자를 서둘러야 하는 상황에 놓여 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the spain courier, express, and parcel market size was valued at USD 4.39 billion in 2025 and estimated to grow from USD 4.58 billion in 2026 to reach USD 5.48 billion by 2031, at a 3.67% CAGR during the forecast period (2026-2031).

Spain's double-digit e-commerce penetration, a persistently high 22% return rate, and growing demand for cold-chain services keep parcel volumes on an upward trajectory. This report is Segmented by Destination (Domestic, International), by Speed of Delivery (Express, Non-Express), by Model (Business-To-Business, and More), by Shipment Weight (Heavy Weight, Light Weight, Medium Weight), by Mode of Transport (Air, Road, Others), and by End User Industry (E-Commerce, Financial Services, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Courier, Express, And Parcel (CEP) Market Trends and Insights

Surge in Reverse Logistics Driven by Spain's 22% E-Commerce Return Rate

Return rates near 22% make Spain one of Europe's most challenging e-commerce environments, prompting operators to rebuild hub-and-spoke networks for two-way flows while installing inspection and refurbishment lines inside depots. Fashion and footwear account for the bulk of returns and often exceed 30% due to size uncertainty and bracketing purchases. Peer-to-peer marketplaces add another layer of bidirectional traffic as every C2C shipment doubles touchpoints. Operators that invest in dedicated reverse logistics capacity and inventory-visibility platforms increasingly turn a traditional cost center into a source of differentiation. As more brands introduce take-back schemes, reverse flow volumes inside the Spain courier, express, and parcel market are projected to outpace forward shipment growth over the next five years.

AI-Powered Dynamic Route Planning and Load Balancing Cutting Cost per Kilometer

Machine-learning algorithms that ingest traffic, weather, and historical delivery patterns now trim 12-18% off line-haul and last-mile costs. Real-time re-sequencing raises stops per hour by more than 20% on dense Barcelona routes, allowing carriers to protect margins despite platform-driven rate pressure. Capital-intensive robotics hubs such as Amazon's Asturias facility combine AI sortation with automated guided vehicles to sustain peak-season throughput. Mid-tier providers unable to fund data-science talent increasingly adopt white-label SaaS optimization tools or partner with technology firms, widening the capability gap among competitors in the Spain courier, express, and parcel market.

Inflation Spikes in Corrugate, Fuel, and Refrigerants Adding More Than 8% to Unit Costs

Corrugate surged 15-20% on pulp shortages, diesel prices swung between EUR 1.20-1.60 per liter, and F-gas phase-downs inflated refrigerant costs, collectively compressing margins in 2025. Carriers hedged fuel and signed fixed-rate packaging contracts, yet high-volume platforms controlling over 80% of orders resisted price adjustments. Smaller providers found limited headroom to absorb spikes, prompting defensive mergers and stronger focus on AI efficiency levers inside the Spain courier, express, and parcel market.

Other drivers and restraints analyzed in the detailed report include:

- Cross-Border Grocery and Meal-Kit Boom Boosting Temperature-Controlled Parcel Demand

- EU-Funded Hydrogen Truck Pilots Lowering Long-Haul Emission Costs and Toll Exposure

- CSRD-Mandated ESG Auditing Increasing Compliance Overheads for CEP Firms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 32.41% of the Spain Courier, Express, and Parcel (CEP) market share in 2025, supported by steady automotive and machinery output in Catalonia and Navarre. The Spain courier, express, and parcel market linked to manufacturing remains resilient but posts modest mid-single-digit growth tied to industrial production cycles.

E-commerce parcels, including C2C resale, are forecast to grow 4.00% CAGR through 2031, buoyed by deepening online penetration in fashion, electronics, and homeware baskets. Manufacturers increasingly adopt B2B e-commerce portals for spare parts, driving predictable small-batch shipments, while fashion retailers leverage reverse logistics hubs to cope with returns exceeding 30%. Financial services sustain high-margin document couriers, and stricter GDP rules push healthcare senders toward premium express services. End-user diversification staves off sector-specific volatility and rewards operators able to run multi-vertical networks inside the Spain courier, express, and parcel market.

Domestic parcels represented 63.92% of the Spain Courier, Express, and Parcel (CEP) market size in 2025, yet face slowing growth as urban markets reach service saturation. International flows will register 3.80% CAGR to 2031, lifted by EU VAT harmonization and IOSS rules that cut customs friction for sub-EUR 150 shipments.

Cross-border growth clusters along Spain-France-Germany corridors supported by hydrogen truck pilots and rail-road services that eliminate 11,500 annual truck trips. Spanish exporters also tap UPS's Estafeta network to Latin America, capitalizing on cultural affinity and time-zone alignment. The widening international mix compels carriers to refine customs-brokerage capabilities and invest in multi-currency, multi-language customer portals across the Spain courier, express, and parcel market.

List of Companies Covered in this Report:

- Correos Express

- DHL Group

- FedEx

- GEODIS

- La Poste Group (including SEUR)

- Logista

- MRW

- Paack

- Szendex

- International Distribution Services plc

- Amazon, Inc.

- CTT Express

- Envialia

- TIPSA

- Stuart Delivery

- Sending Transporte Urgente

- Rangel Logistics

- Zeleris

- ID Logistics

- United Parcel Service of America, Inc. (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Surge in Reverse Logistics Driven by Spain's 22 % E-Commerce Return Rate

- 4.15.2 AI-Powered Dynamic Route-Planning and Load-Balancing Cutting Cost Per Kilometer

- 4.15.3 Cross-Border Grocery and Meal-Kit Boom Boosting Temperature-Controlled Parcel Demand

- 4.15.4 EU-Funded Hydrogen Truck Pilots Lowering Long-Haul Emission Costs and Toll Exposure

- 4.15.5 Stricter EU GDP Pharma Rules Expanding Cold-Chain Express Volumes

- 4.15.6 Rapid Rise of C2C Resale Platforms (Wallapop, Vinted) Multiplying Micro-Parcel Flows

- 4.16 Market Restraints

- 4.16.1 Inflation Spikes in Corrugate, Fuel, and Refrigerants Adding More Than 8 % to Unit Costs

- 4.16.2 CSRD-Mandated ESG Auditing Increasing Compliance Overheads for CEP Firms

- 4.16.3 Escalating Cyber-Attacks on Tracking APIs Causing SLA Penalties and Brand Damage

- 4.16.4 Saturation of Urban Pick-Up/Locker Points Limiting Further Last-Mile Density Gains

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 By Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 By Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 By Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 By Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 By End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Correos Express

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 GEODIS

- 6.4.5 La Poste Group (including SEUR)

- 6.4.6 Logista

- 6.4.7 MRW

- 6.4.8 Paack

- 6.4.9 Szendex

- 6.4.10 International Distribution Services plc

- 6.4.11 Amazon, Inc.

- 6.4.12 CTT Express

- 6.4.13 Envialia

- 6.4.14 TIPSA

- 6.4.15 Stuart Delivery

- 6.4.16 Sending Transporte Urgente

- 6.4.17 Rangel Logistics

- 6.4.18 Zeleris

- 6.4.19 ID Logistics

- 6.4.20 United Parcel Service of America, Inc. (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment