|

시장보고서

상품코드

2045725

복합 사이클 가스 터빈 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Combined Cycle Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

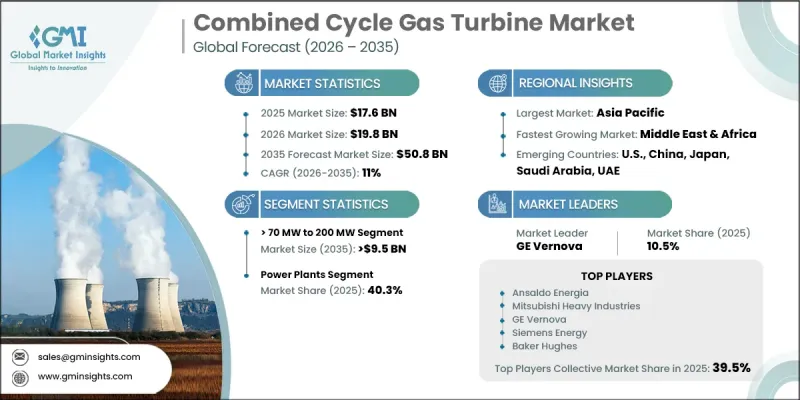

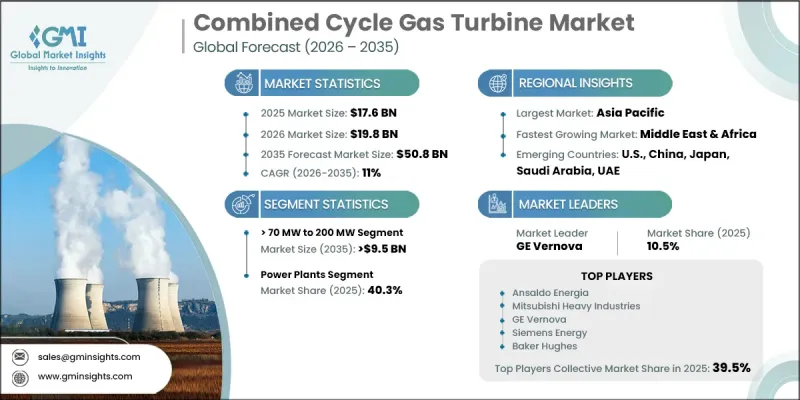

세계의 복합 사이클 가스 터빈 시장은 2025년에 176억 달러로 평가되었고 CAGR 11%로 성장하여 2035년까지 508억 달러에 이를 것으로 추정되고 있습니다.

이 시장의 성장은 더 깨끗하고 효율적인 발전 시스템으로의 전환에 의해 뒷받침되고 있습니다. 이산화탄소 배출, 대기오염, 기후 변화에 대한 우려가 높아짐에 따라 전력회사와 정부는 고도의 저배출 기술을 도입해야 하는 상황에 직면해 있습니다. 재생에너지 통합, 전력망 현대화, 고효율 에너지 시스템에 대한 투자가 시장 확대를 더욱 촉진하고 있습니다. 복합 사이클 가스 터빈 시스템은 높은 출력 성능을 발휘하면서도 연료 효율을 향상시키고 환경에 미치는 영향을 줄일 수 있어 점점 더 선호되고 있습니다. 이 시스템은 폐열을 회수하고 추가 발전을 하는 2단계 공정을 통해 천연가스를 전력으로 변환하는 것으로 널리 알려져 있으며, 기존 화력 발전 시스템에 비해 전체 효율이 크게 향상되었습니다. 전 세계 에너지 수요가 증가하는 가운데, 이 기술은 기존 에너지원과 재생에너지원을 연결하는 신뢰할 수 있는 가교로 주목받고 있으며, 지역에 관계없이 송전망의 안정성과 유연한 전력 공급 요건을 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 176억 달러 |

| 예측 시장 규모 | 508억 달러 |

| CAGR | 11% |

70-200MW 부문은 2035년까지 95억 달러에 달할 것으로 예측됩니다. 이 부문은 빠른 부하 응답과 빠른 운전 시작에 매우 적합하다는 장점이 있어 피크 시 전력 수요 관리와 송전망의 안정성 유지에 매우 효과적입니다. 안정적인 전력 공급이 필수적인 대규모 유틸리티 프로젝트, 해양 에너지 시설, 해양 사업, 항공 관련 분야에서 도입이 확대되고 있습니다. 에너지 집약적인 다양한 분야에서 이러한 중대형 시스템 도입이 확대되면서 이 부문의 성장이 가속화되고 있습니다.

2025년 기준, 발전 응용 분야는 40.3%의 점유율을 차지했습니다. 이 부문의 성장은 전 세계 전력 소비 증가, 저탄소 에너지 시스템으로의 전환, 노후화된 석탄 화력 발전 인프라의 단계적 폐지 등에 의해 주도되고 있습니다. 기존 화력발전소에 비해 복합화력 발전소는 높은 효율, 낮은 배출량, 빠른 출력 상승 능력, 연료의 유연성 향상 등 장점을 가지고 있습니다. 피크 수요를 지원하고 송전망 안정화를 위한 유연성 가스발전에 대한 수요 증가는 간헐적 재생에너지의 보급 확대로 인해 더욱 증폭되고 있습니다.

2025년 미국 복합 사이클 가스 터빈 시장은 72%의 점유율을 차지하며 25억 달러 시장 규모를 기록했습니다. 시장 확대는 신뢰할 수 있는 재생에너지 발전에 대한 강력한 수요와 저렴한 천연가스의 광범위한 공급에 의해 뒷받침되고 있습니다. 복합 사이클 가스 터빈 시스템은 운영상의 유연성과 높은 효율성으로 인해 풍력, 태양광 등 재생에너지원의 변동성을 조정하기 위해 점점 더 많이 도입되고 있습니다. 배출량 감축에 대한 규제 당국의 강력한 집중, 에너지 안보의 우선순위, 전력 인프라의 지속적인 현대화는 이 나라 시장 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 규모와 예측 : 용량별, 2022-2035년

제6장 시장 규모와 예측 : 용도별, 2022-2035년

제7장 시장 규모와 예측 : 지역별, 2022-2035년

제8장 기업 개요

JHS 26.06.11The Global Combined Cycle Gas Turbine Market was valued at USD 17.6 billion in 2025 and is estimated to grow at a CAGR of 11% to reach USD 50.8 billion by 2035.

The market growth is supported by the global shift toward cleaner and more efficient power generation systems. Increasing concerns over carbon emissions, air pollution, and climate change are pushing utilities and governments to adopt advanced low-emission technologies. Investments in renewable integration, grid modernization, and high-efficiency energy systems are further strengthening market expansion. Combined cycle gas turbine systems are increasingly preferred due to their ability to deliver high power output with improved fuel efficiency and reduced environmental impact. These systems are widely recognized for converting natural gas into electricity through a dual-stage process that captures waste heat to generate additional power, significantly improving overall efficiency compared to traditional thermal systems. As global energy demand rises, the technology is gaining traction as a reliable bridge between conventional and renewable energy sources, supporting grid stability and flexible power supply requirements across regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.6 Billion |

| Forecast Value | $50.8 Billion |

| CAGR | 11% |

The > 70 MW to 200 MW segment is projected to reach USD 9.5 billion by 2035. This segment benefits from its strong suitability for rapid load response and fast operational start-up, making it highly effective for managing peak electricity demand and maintaining grid stability. Its adoption is expanding across large-scale utility projects, offshore energy facilities, maritime operations, and aviation-related applications, where reliable and efficient power output is essential. The increasing deployment of these medium-to-large capacity systems across diverse energy-intensive sectors continues to accelerate segment growth.

The power generation application segment accounted for a 40.3% share in 2025. Growth in this segment is being driven by rising global electricity consumption, the transition toward low-carbon energy systems, and the phased retirement of aging coal-based power infrastructure. Compared to conventional thermal plants, combined cycle gas turbine facilities offer higher efficiency, lower emissions, faster ramp-up capabilities, and improved fuel flexibility. The rising need for flexible gas-based generation to support peak demand and stabilize grids is further amplified by the growing penetration of intermittent renewable energy sources.

U.S. Combined Cycle Gas Turbine Market held a 72% share in 2025, generating USD 2.5 billion. Market expansion is supported by strong demand for reliable electricity generation and the widespread availability of affordable natural gas. Combined cycle gas turbine systems are increasingly deployed to balance fluctuations from renewable energy sources such as wind and solar, due to their operational flexibility and high efficiency. Strong regulatory focus on emission reduction, energy security priorities, and continued modernization of power infrastructure are further reinforcing market growth in the country.

Major players operating in the Global Combined Cycle Gas Turbine Industry include GE Vernova, Siemens Energy, Mitsubishi Heavy Industries, Baker Hughes, Ansaldo Energia, Kawasaki Heavy Industries, Doosan Enerbility, Bharat Heavy Electricals Limited (BHEL), Rolls Royce, Shanghai Electric, Capstone Green Energy Holdings, Harbin Electric Corporation, Solar Turbines Incorporated, Wartsila, Ethos Energy Group, Everllence, MAPNA Group, Flex Energy Solutions, VERICOR, and Zorya-Mashproekt. Companies in the combined cycle gas turbine market are focusing on advancing turbine efficiency through next-generation design improvements that maximize output while minimizing fuel consumption. Many players are strengthening their position by investing heavily in digitalization, predictive maintenance, and real-time monitoring systems to enhance operational reliability. Strategic partnerships with utilities and independent power producers are being used to secure long-term service agreements and project pipelines. Manufacturers are also expanding R&D efforts to support hydrogen-ready and low-carbon turbine solutions aligned with global decarbonization goals. Cost optimization strategies, including modular plant designs and standardized components, are helping reduce installation and maintenance expenses.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Capacity trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of combined cycle gas turbines

- 3.8 Growth in untapped markets & applications

- 3.9 Digitalization & IoT integration

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.11.1 By region (Driven by Primary Research)

- 3.11.2 By capacity (Driven by Primary Research)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 50 kW

- 5.3 > 50 kW to 500 kW

- 5.4 > 500 kW to 1 MW

- 5.5 > 1 MW to 30 MW

- 5.6 > 30 MW to 70 MW

- 5.7 > 70 MW to 200 MW

- 5.8 > 200 MW

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Power plants

- 6.3 Oil & gas

- 6.4 Process plants

- 6.5 Aviation

- 6.6 Marine

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Mexico

- 7.4 Europe

- 7.4.1 UK

- 7.4.2 France

- 7.4.3 Germany

- 7.4.4 Russia

- 7.4.5 Italy

- 7.4.6 Netherlands

- 7.4.7 Finland

- 7.4.8 Denmark

- 7.4.9 Poland

- 7.4.10 Sweden

- 7.5 Asia Pacific

- 7.5.1 China

- 7.5.2 Australia

- 7.5.3 Japan

- 7.5.4 South Korea

- 7.5.5 Indonesia

- 7.5.6 Thailand

- 7.5.7 Malaysia

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 Qatar

- 7.6.4 Kuwait

- 7.6.5 Oman

- 7.6.6 Egypt

- 7.6.7 Turkey

- 7.6.8 Bahrain

- 7.6.9 Iraq

- 7.6.10 South Africa

- 7.6.11 Nigeria

- 7.6.12 Algeria

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Argentina

- 7.7.3 Chile

Chapter 8 Company Profiles

- 8.1 Ansaldo Energia

- 8.2 Baker Hughes

- 8.3 Bharat Heavy Electricals Limited (BHEL)

- 8.4 Capstone Green Energy Holdings

- 8.5 Doosan Enerbility

- 8.6 Ethos Energy Group

- 8.7 Everllence

- 8.8 Flex Energy Solutions

- 8.9 GE Vernova

- 8.10 Harbin Electric Corporation

- 8.11 Kawasaki Heavy Industries

- 8.12 MAPNA Group

- 8.13 Mitsubishi Heavy Industries

- 8.14 Rolls Royce

- 8.15 Shanghai Electric

- 8.16 Siemens Energy

- 8.17 Solar Turbines Incorporated

- 8.18 VERICOR

- 8.19 Wartsila

- 8.20 Zorya-Mashproekt