|

시장보고서

상품코드

2061327

군용기 현대화 및 레트로피트 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Military Aircraft Modernization and Retrofit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

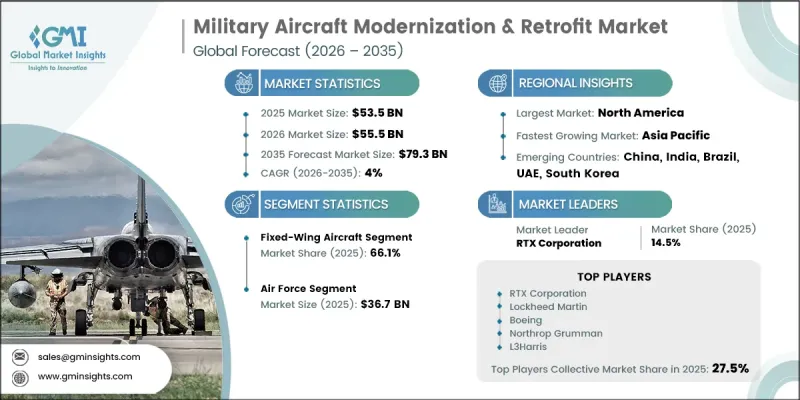

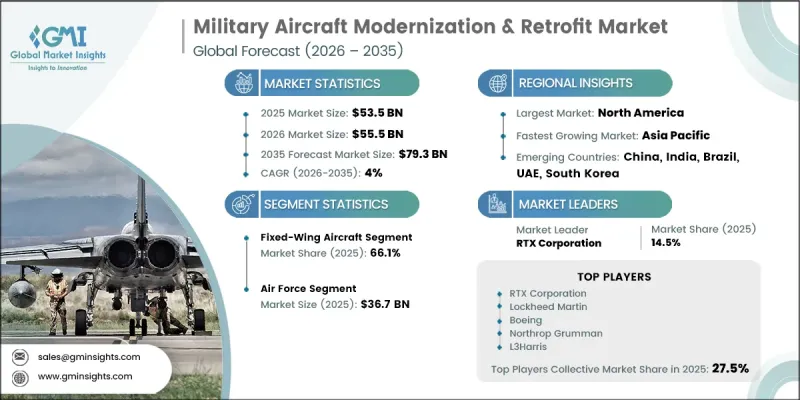

세계의 군용기 현대화·레트로피트 시장은 2025년에 535억 달러로 평가되고 CAGR 4%로 성장하며, 2035년까지 793억 달러에 달할 것으로 추정되고 있습니다.

방위 기관들이 항공기의 전면적인 교체보다는 기체군의 유지, 작전 준비 태세 및 능력 향상을 우선시하는 가운데, 군용기 개조 및 현대화 산업은 계속해서 성장세를 보이고 있습니다. 선진국 및 신흥 국가의 군사비 증가는 첨단 항공기 기술, 디지털 임무 시스템, 그리고 항공기 수명 연장 계획에 대한 투자를 촉진하고 있습니다. 네트워크 중심의 전술 능력과 다영역 전투 작전의 확대 도입 역시 통합 항공전자 장비, 통신 시스템 및 감시 기술에 대한 수요를 가속화하고 있습니다. 또한 군 운용 당국은 효율성, 적응성 및 임무 수행 능력을 향상시키는 현대화 프로그램을 통해 노후화된 항공기 기단의 운용 수명을 연장하는 데 점점 더 주력하고 있습니다. 플랫폼별 운영 요건에 맞춰 설계된 맞춤형 업그레이드 패키지에 대한 수요 역시 장기적인 시장 확대에 더욱 기여하고 있습니다. 항공전자 아키텍처, 임무 통합 및 항공기 연결성 분야의 지속적인 기술 발전은 예측 기간 중 군용기 현대화 및 개조 시장의 성장 전망을 강화할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 535억 달러 |

| 예측액 | 793억 달러 |

| CAGR | 4% |

군용기 현대화 및 개량 시장의 성장은 주로 기존 기체의 유지보수 및 업그레이드에 투입되는 국방비 증가에 힘입어 이루어지고 있습니다. 많은 정부는 신규 항공기 조달에 따른 취득 비용을 억제하면서도 운용 능력을 향상시키기 위해, 조달 우선순위를 항공기 성능 향상 프로그램으로 지속적으로 전환하고 있습니다. 또한 첨단 항공전자 장비, 항법 기술 및 임무 관리 시스템의 도입 확대도 시장 수요를 지원하고 있습니다. 국제 규제기관이 제정한 최신 항공 안전 및 통신 기준은 군용 지원 항공기 전반에 걸친 항법, 통신 및 내공성 시스템에 대한 현대화 구상을 촉진하고 있습니다. 동시에, 기존 항공기 기체의 노후화와 구형 항공전자 장비 하드웨어의 점진적인 노후화로 인해 전 세계 방위 산업 전반에 걸쳐 현대화 솔루션에 대한 지속적인 수요가 계속해서 발생하고 있습니다.

2025년에는 고정익 항공기 부문이 66.1%의 점유율을 차지했습니다. 고정익 항공기는 긴 운용 수명, 막대한 조달 비용, 그리고 정기적인 업그레이드와 통합 개선을 필요로 하는 고도로 정교한 탑재 시스템 덕분에 여전히 주요 플랫폼 범주로 자리 잡고 있습니다. 이 부문의 수요는 항공기의 성능, 운용 효율, 임무 수행 능력 및 기술적 호환성 향상에 중점을 둔 현대화 프로그램에 의해 주도되고 있습니다. 항공전자 시스템, 조종실의 디지털화, 통신 기술, 추진 시스템의 개선 및 임무 통합 능력과 관련된 업그레이드는 고정익 항공기 부문에서 계속해서 강력한 매출 기회를 창출하고 있습니다.

육군 항공 부문은 2026-2035년 연평균 성장률(CAGR) 6.8%를 기록할 것으로 전망됩니다. 이 부문의 시장 확대는 수송용, 다목적용 및 전투용 헬리콥터 기단을 대상으로 한 대규모 현대화 계획에 힘입어 이루어지고 있습니다. 방위 기관은 항공기의 신뢰성과 작전 준비 태세를 향상시키기 위해 첨단 통신 시스템, 생존성 기술, 감시 솔루션 및 통합 임무 장비에 대한 투자를 확대하고 있습니다. 회전익 항공기용으로 특별히 설계된 모듈식 항공전자 장비 패키지의 활용 가능성이 높아지고 있는 점도, 현대화 프로그램에 따른 설계의 복잡성을 줄이고 통합 비용을 절감함으로써 그 도입을 촉진하고 있습니다.

북미의 군용기 현대화·개조 시장은 2025년에 34.6%의 점유율을 차지하며, 세계 최대 지역 시장이 되었습니다. 이 지역은 풍부한 군용 항공기 보유 대수, 지속적인 국방 예산 승인, 그리고 항공기 유지 관리 프로그램에 대한 장기적인 투자를 바탕으로 확고한 입지를 유지하고 있습니다. 기체군의 운용 준비 태세, 작전 능력 향상, 그리고 장기적인 플랫폼 유지 관리에 대한 조직적인 노력이 해당 지역 전체의 시장 성장을 지속적으로 지원하고 있습니다. 또한 여러 방위 항공 부문에 걸친 지속적인 현대화 계약과 기술 통합 노력 역시 군용기 개조 및 현대화 산업 분야에서 북미의 주도적 지위를 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 항공기 유형별, 2022-2035년

제6장 시장 추산·예측 : 컴포넌트 유형별, 2022-2035년

제7장 시장 추산·예측 : 프로그램의 목적별, 2022-2035년

제8장 시장 추산·예측 : 최종사용자별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.23The Global Military Aircraft Modernization & Retrofit Market was valued at USD 53.5 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 79.3 billion by 2035.

The military aircraft retrofit and modernization industry continues to gain momentum as defense agencies prioritize fleet sustainment, operational readiness, and capability upgrades over complete aircraft replacement. Rising military expenditures across developed and emerging economies are encouraging investments in advanced onboard technologies, digital mission systems, and aircraft life-extension initiatives. The growing adoption of network-centric warfare capabilities and multidomain combat operations is also accelerating demand for integrated avionics, communication systems, and surveillance technologies. In addition, military operators are increasingly focusing on extending the operational lifespan of aging aircraft fleets through modernization programs that improve efficiency, adaptability, and mission performance. Demand for customized upgrade packages designed for platform-specific operational requirements is further contributing to long-term market expansion. Continuous technological advancements in avionics architecture, mission integration, and aircraft connectivity are expected to reinforce the growth outlook for the military aircraft modernization and retrofit market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.5 Billion |

| Forecast Value | $79.3 Billion |

| CAGR | 4% |

Growth across the military aircraft modernization & retrofit market is primarily supported by rising defense spending allocations dedicated to maintaining and upgrading existing fleets. Several governments continue to shift procurement priorities toward aircraft enhancement programs to improve operational capabilities while controlling acquisition costs associated with new aircraft procurement. Increasing adoption of advanced avionics, navigation technologies, and mission management systems is also strengthening market demand. Updated aviation safety and communication standards established by international regulatory organizations are encouraging modernization initiatives involving navigation, communication, and airworthiness systems across military support aircraft. At the same time, the aging nature of existing aircraft fleets and the gradual obsolescence of legacy avionics hardware continue to create sustained demand for modernization solutions across global defense sectors.

The fixed-wing aircraft segment accounted for 66.1% share in 2025. Fixed-wing aircraft remain the dominant platform category due to their extended operational lifespan, significant acquisition value, and highly sophisticated onboard systems requiring periodic upgrades and integration improvements. Demand within this segment is being fueled by modernization programs focused on enhancing aircraft performance, operational efficiency, mission effectiveness, and technological compatibility. Upgrades involving avionics systems, cockpit digitization, communication technologies, propulsion improvements, and mission integration capabilities continue to generate strong revenue opportunities within the fixed-wing aircraft category.

The army aviation segment is anticipated to record a CAGR of 6.8% during 2026-2035. Market expansion within this segment is being driven by large-scale modernization initiatives targeting transport, utility, and combat helicopter fleets. Defense organizations are increasingly investing in advanced communication systems, survivability technologies, monitoring solutions, and integrated mission equipment to improve aircraft reliability and operational readiness. The growing availability of modular avionics packages specifically designed for rotary-wing aircraft is also supporting adoption by reducing engineering complexity and lowering integration costs associated with modernization programs.

North America Military Aircraft Modernization & Retrofit Market captured 34.6% share in 2025, making it the leading regional market worldwide. The region maintains a strong position due to its extensive military aviation inventory, continuous defense budget approvals, and long-term investments in aircraft sustainment programs. Strong institutional focus on fleet readiness, operational capability enhancement, and long-term platform maintenance continues to support market growth across the region. Ongoing modernization contracts and technology integration initiatives across multiple defense aviation divisions are also reinforcing North America's leadership in the military aircraft retrofit and modernization industry.

Key companies operating in the Military Aircraft Modernization & Retrofit Market include Lockheed Martin Corporation, RTX Corporation (Raytheon Technologies), Northrop Grumman Corporation, BAE Systems plc, The Boeing Company, L3Harris Technologies, Inc., General Dynamics Corporation, Leonardo S.p.A, Thales Group, Safran, Israel Aerospace Industries Ltd., Elbit Systems Ltd., Honeywell International Inc., ST Engineering, and Rolls-Royce plc. Companies operating in the military aircraft modernization and retrofit market are increasingly focusing on strategic partnerships, long-term defense contracts, and advanced technology integration to strengthen their market presence. Major industry participants are investing heavily in research and development to introduce next-generation avionics, mission systems, communication technologies, and aircraft sustainment solutions. Businesses are also expanding their regional footprint through collaborations with defense agencies and local aerospace manufacturers to secure modernization contracts and improve aftermarket support capabilities. Another key strategy involves the development of modular and scalable upgrade solutions that simplify integration and reduce maintenance costs for military operators.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Aircraft type trends

- 2.2.2 Component type trends

- 2.2.3 Program objective trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising defense budget allocations for fleet sustainability and capability enhancement

- 3.2.1.2 Increasing integration of advanced avionics and mission systems

- 3.2.1.3 Expansion of multidomain warfare and network-centric operations

- 3.2.1.4 Growing focus on service life extension programs for aging aircraft fleets

- 3.2.1.5 Rising demand for platform-specific customization and mission flexibility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and complexity of retrofit and modernization programs

- 3.2.2.2 Certification and regulatory compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Emergence of next-generation aircraft programs and digital cockpit upgrades

- 3.2.3.2 Expansion of global MRO infrastructure and aftermarket service capabilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Fixed-wing aircraft

- 5.2.1 Fighter aircraft

- 5.2.2 Bomber & strike aircraft

- 5.2.3 Transport & cargo aircraft

- 5.2.4 Intelligence, surveillance & reconnaissance (ISR) aircraft

- 5.2.5 Trainer aircraft

- 5.2.6 Special mission aircraft (AEW&C, SIGINT/ELINT, maritime patrol, modified platforms)

- 5.3 Rotary-wing aircraft

- 5.3.1 Attack helicopters

- 5.3.2 Transport helicopters

- 5.3.3 Utility helicopters

- 5.3.4 Maritime & shipborne helicopters

- 5.4 Unmanned aerial vehicles (UAVs)

- 5.4.1 Combat UAVs (UCAVs)

- 5.4.2 Tactical & reconnaissance UAVs

- 5.4.3 MALE UAVs

- 5.4.4 HALE UAVs

Chapter 6 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Avionics systems

- 6.3 Communication systems

- 6.4 Radar & sensor systems

- 6.5 Electronic warfare systems

- 6.6 Weapon integration & fire control systems

- 6.7 Propulsion & engine systems

- 6.8 Airframe & structural systems

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By Program Objective, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Capability enhancement programs

- 7.3 Service life extension programs (SLEP)

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Air force

- 8.3 Naval aviation

- 8.4 Army aviation

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 RTX Corporation

- 10.1.2 Lockheed Martin

- 10.1.3 Boeing

- 10.1.4 Northrop Grumman

- 10.1.5 L3Harris

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 General Dynamics Corporation

- 10.2.1.2 Honeywell International Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 ST Engineering

- 10.2.3 Europe

- 10.2.3.1 BAE Systems plc

- 10.2.3.2 Leonardo S.p.A

- 10.2.3.3 Thales Group

- 10.2.3.4 Safran

- 10.2.3.5 Rolls-Royce plc

- 10.2.4 Middle East & Africa

- 10.2.4.1 Israel Aerospace Industries Ltd.

- 10.2.4.2 Elbit Systems Ltd.

- 10.2.1 North America