|

시장보고서

상품코드

2061475

로봇용 액추에이터 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Robotics actuators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

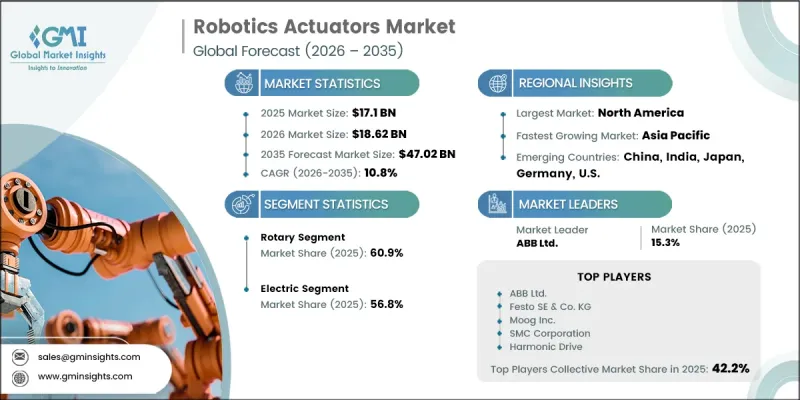

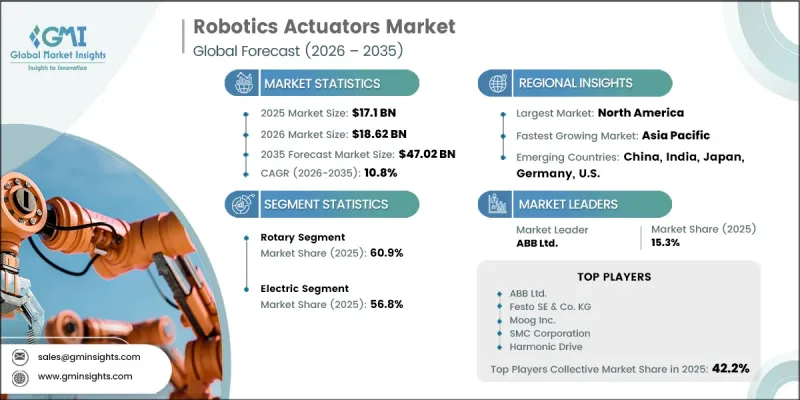

세계의 로봇용 액추에이터 시장은 2025년에 171억 달러로 평가되며, 2035년까지 CAGR 10.8%로 성장하며, 470억 2,000만 달러에 달할 것으로 추정되고 있습니다.

로봇용 액추에이터 시장은 산업 자동화 도입 가속화, 협동 로봇 시스템 도입 확대, 지능형 액추에이터 기술의 지속적인 발전, 의료·물류·제조 분야에서의 로봇 기술 도입 확대에 힘입어 강력한 성장세를 보이고 있습니다. 액추에이터는 제어된 움직임, 위치 결정 정밀도, 정확한 동작 수행을 가능하게 함으로써 로봇 시스템 내에서 중요한 구성 요소로 기능합니다. 조직이 효율성, 생산성, 운영의 일관성을 지속적으로 우선시함에 따라 첨단 로봇 동작 기술에 대한 수요는 계속해서 증가하고 있습니다. 자동화된 생산 시설, 디지털 제조 생태계, 연결된 산업 운영으로의 전환이 진행되고 있는 것은 액추에이터 제조업체에게 큰 성장 기회를 창출하고 있습니다. 또한 복잡한 작업을 정밀하게 수행할 수 있는 반응성이 뛰어난 로봇 시스템에 대한 수요가 증가함에 따라 시장 수요가 확대되고 있습니다. 지속적인 기술 혁신과 차세대 로봇 인프라에 대한 투자 확대가 맞물리면서, 예측 기간 중 전 세계 로봇용 액추에이터 시장 전체가 지속적인 성장을 이어갈 것으로 전망됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 171억 달러 |

| 예측액 | 470억 2,000만 달러 |

| CAGR | 10.8% |

로봇용 액추에이터 시장은 생산성 향상, 운영 성능 개선, 인력 의존도 감소를 추구하는 여러 산업 부문에서 자동화 기술이 급속히 도입됨에 따라 성장하고 있습니다. 정밀도, 재현성, 신뢰성이 필수적인 요건이 되는 현대의 제조 환경에서, 첨단 로봇 시스템은 없어서는 안 될 존재가 되었습니다. 스마트 팩토리와 디지털로 연결된 생산 시설의 지속적인 발전은 로봇용 액추에이터의 채택 확대를 위한 유리한 환경을 조성하고 있습니다. 또한 협업 로봇 시스템과 첨단 휴머노이드 로봇의 도입 확대는 다양한 최종 용도 산업 분야에서 새로운 성장 기회를 창출하고 있습니다. 기업이 점점 더 고도화되는 운영 요건에 대응할 수 있는 지능형 자동화 플랫폼에 대한 투자를 지속함에 따라 고성능 액추에이터 기술에 대한 수요는 계속해서 견고할 것으로 예상됩니다. 인더스트리 4.0 제조 모델로의 전환은 산업 활동 전반에 걸쳐 첨단 로봇 모션 제어 시스템의 통합을 더욱 가속화하고 있습니다.

2025년에는 로터리 액추에이터 부문이 시장 점유율의 60.9%를 차지했습니다. 이러한 확고한 시장 입지는 회전 운동과 높은 토크 성능이 필요한 로봇 시스템 전반에 걸쳐 광범위하게 채택됨으로써 지원되고 있습니다. 로터리 액추에이터는 정밀한 각도 운동, 작동 내구성, 향상된 작동 효율을 제공할 수 있으며, 자동화 제조 공정에서 널리 사용되고 있습니다. 제조업체들이 자동화를 더욱 확대하고 생산을 최적화하기 위해 노력함에 따라 로봇 모션 제어 애플리케이션에서 그 중요성은 계속해서 커지고 있습니다. 산업용 로봇과 자동 생산 시스템의 활용이 확대됨에 따라 향후 수년간 이 부문의 성장은 더욱 가속화될 것으로 예상됩니다.

2025년 기준으로, 전동 액추에이터 부문은 56.8%의 시장 점유율을 차지했습니다. 전동 액추에이터는 뛰어난 동작 정밀도, 높은 에너지 효율, 디지털 제어 아키텍처와의 원활한 호환성 덕분에 모든 로봇 플랫폼에서 선호되는 솔루션으로 자리 잡고 있습니다. 이러한 액추에이터는 부드러운 작동 성능, 유지보수 요구 사항의 감소, 자동화 환경 내에서의 높은 적응성 등 큰 장점을 갖추고 있습니다. 첨단 제조 시설 및 커넥티드 생산 시스템과의 호환성은 여전히 이러한 기술의 광범위한 도입을 지원하고 있습니다. 산업 부문 전반에 걸친 로봇 기술 도입 확대에 힘입어, 예측 기간 중 전동 액추에이터 솔루션에 대한 수요가 더욱 가속화될 것으로 예상됩니다.

2025년, 북미의 로봇용 액추에이터 시장은 32.1%의 점유율을 차지했습니다. 해당 지역에서는 자동화에 대한 투자 확대, 첨단 제조 역량, 산업 전반에 걸친 로봇 기술 도입 확대에 힘입어 앞으로도 꾸준한 시장 성장이 예상됩니다. 확립된 산업 인프라와 스마트 제조 구상의 지속적인 도입이 시장 확대를 위한 유리한 여건을 조성하고 있습니다. 조직들이 효율성, 생산성, 운영상의 유연성 향상에 주력하는 가운데, 첨단 로봇 모션 제어 시스템에 대한 수요는 계속해서 견고한 양상을 보이고 있습니다. 자동화된 생산 환경과 차세대 로봇 기술에 대한 지속적인 투자를 통해, 예측 기간 중 북미가 로봇용 액추에이터의 주요 시장으로서의 입지를 더욱 공고히 할 것으로 예상됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 추정·예측 : 구동 방식별, 2022-2035년

제6장 시장 추정·예측 : 모션 유형별, 2022-2035년

제7장 시장 추정·예측 : 로봇 유형별, 2022-2035년

제8장 시장 추정·예측 : 최종사용자 산업별, 2022-2035년

제9장 시장 추정·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.24The Global Robotics Actuators Market was valued at USD 17.1 billion in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 47.02 billion by 2035.

The robotics actuators market is witnessing strong expansion due to the accelerating adoption of industrial automation, increasing deployment of collaborative robotic systems, continuous advancements in intelligent actuator technologies, and rising implementation of robotics across healthcare, logistics, and manufacturing environments. Actuators serve as critical components within robotic systems by enabling controlled movement, positioning accuracy, and precise motion execution. As organizations continue to prioritize efficiency, productivity, and operational consistency, demand for advanced robotic motion technologies continues to rise. The growing transition toward automated production facilities, digital manufacturing ecosystems, and connected industrial operations is creating significant opportunities for actuator manufacturers. Furthermore, the increasing need for highly responsive robotic systems capable of performing complex tasks with precision is strengthening market demand. Continuous technological innovation, coupled with expanding investment in next-generation robotics infrastructure, is expected to support sustained growth across the global robotics actuators market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.1 Billion |

| Forecast Value | $47.02 Billion |

| CAGR | 10.8% |

The robotics actuators market is driven by the rapid implementation of automation technologies across multiple industrial sectors seeking enhanced productivity, improved operational performance, and reduced dependence on manual labor. Advanced robotic systems have become essential to modern manufacturing environments where precision, repeatability, and reliability are critical requirements. The ongoing evolution of smart factories and digitally connected production facilities is creating a favorable environment for increased adoption of robotics actuators. In addition, growing deployment of collaborative robotic systems and advanced humanoid robotics is generating new growth opportunities across a variety of end-use industries. As businesses continue investing in intelligent automation platforms capable of supporting increasingly sophisticated operational requirements, demand for high-performance actuator technologies is expected to remain strong. The shift toward Industry 4.0 manufacturing models is further accelerating the integration of advanced robotic motion control systems throughout industrial operations.

The rotary segment accounted for 60.9% share in 2025. Its strong market position is supported by widespread adoption across robotic systems requiring rotational motion and high-torque performance. Rotary actuators are extensively utilized in automated manufacturing processes due to their ability to provide precise angular movement, operational durability, and enhanced motion efficiency. Their importance within robotic motion control applications continues to increase as manufacturers pursue greater automation and production optimization. The expanding use of industrial robotics and automated production systems is expected to further strengthen growth within this segment over the coming years.

The electric segment held a share of 56.8% in 2025. Electric actuators have become a preferred solution across robotic platforms due to their superior motion accuracy, energy-efficient operation, and seamless compatibility with digital control architectures. These actuators offer significant advantages, including smooth operational performance, reduced maintenance requirements, and greater adaptability within automated environments. Their suitability for advanced manufacturing facilities and connected production systems continues to support widespread adoption. Growing implementation of robotic technologies across industrial sectors is expected to further accelerate demand for electric actuator solutions throughout the forecast period.

North America Robotics Actuators Market accounted for 32.1% share in 2025. The region continues to experience strong market growth supported by increasing automation investments, advanced manufacturing capabilities, and expanding deployment of robotic technologies across industrial applications. The presence of well-established industrial infrastructure and the ongoing adoption of smart manufacturing initiatives are creating favorable conditions for market expansion. Demand for advanced robotic motion control systems remains strong as organizations focus on improving efficiency, productivity, and operational flexibility. Continuous investments in automated production environments and next-generation robotics technologies are expected to reinforce North America's position as a leading market for robotics actuators throughout the forecast period.

Key companies operating in the Global Robotics Actuators Market include Yaskawa Electric Corporation, ABB Ltd., FANUC Corporation, Harmonic Drive Systems Inc., Nabtesco Corporation, Maxon Motor AG, Sumitomo Heavy Industries, Ltd., Parker Hannifin Corporation, Schaeffler Group, Moog Inc., Festo SE & Co. KG, Oriental Motor Co., Ltd., Technosoft SA, Actuonix Motion Devices Inc., and Firgelli Technologies Inc. Companies participating in the robotics actuators market are adopting a variety of strategic initiatives to strengthen their competitive position and expand market reach. Major industry participants are investing heavily in research and development to improve actuator performance, energy efficiency, precision control, and integration capabilities for advanced robotic systems. Strategic collaborations with robotics manufacturers, automation solution providers, and industrial technology companies are helping organizations broaden their customer base and accelerate product innovation. Companies are also focusing on expanding production capacity, enhancing supply chain resilience, and developing smart actuator technologies that support connected manufacturing environments. Additionally, acquisitions, partnerships, and regional expansion strategies are being utilized to strengthen global presence, improve market penetration, and capture emerging opportunities in rapidly growing automation sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Actuation Type trends

- 2.2.2 Motion Type trends

- 2.2.3 Robot Type trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of industrial automation and smart manufacturing systems

- 3.2.1.2 Growing demand for collaborative robots and humanoid robots

- 3.2.1.3 Technological advancements in smart and AI-enabled actuator systems

- 3.2.1.4 Expansion of healthcare robotics and surgical automation

- 3.2.1.5 Rising warehouse automation and e-commerce logistics applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs

- 3.2.2.2 Technical complexity and power efficiency limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of robotics in electric vehicle (EV) manufacturing

- 3.2.3.2 Integration with Industry 4.0 and intelligent factory ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Actuation Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Electric

- 5.2.1 Servo Motors

- 5.2.2 Stepper Motors

- 5.2.3 Linear Motors

- 5.2.4 DC Motors

- 5.3 Hydraulic

- 5.3.1 Single-Acting Hydraulic Actuators

- 5.3.2 Double-Acting Hydraulic Actuators

- 5.4 Pneumatic

- 5.4.1 Single-Acting Pneumatic Actuators

- 5.4.2 Double-Acting Pneumatic Actuators

- 5.5 Mechanical

- 5.5.1 Piezoelectric Actuators

- 5.5.2 Shape-Memory Alloy Actuators

- 5.5.3 Magnetic Actuators

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Motion Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Rotary

- 6.2.1 Single-Axis Rotary Actuators

- 6.2.2 Multi-Axis Rotary Actuators

- 6.2.3 Others

- 6.3 Linear

- 6.3.1 Electromechanical Linear Actuators

- 6.3.2 Rodless Linear Actuators

- 6.3.3 Belt-Driven Linear Actuators

- 6.3.4 Others

Chapter 7 Market Estimates and Forecast, By Robot Type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Industrial Robots

- 7.2.1 Articulated Robots

- 7.2.2 SCARA Robots

- 7.2.3 Delta Robots

- 7.2.4 Cartesian/Gantry Robots

- 7.2.5 Others

- 7.3 Collaborative Robots (Cobots)

- 7.3.1 Professional Service Robots

- 7.3.2 Personal/Domestic Service Robots

- 7.3.3 Medical & Healthcare Robots

- 7.3.4 Others

- 7.4 Humanoid Robots

- 7.4.1 Research & Development Humanoids

- 7.4.2 Commercial & Entertainment Humanoids

- 7.4.3 Others

Chapter 8 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Automotive

- 8.2.1 Assembly & Fabrication

- 8.2.2 Welding & Joining

- 8.2.3 Painting & Coating

- 8.2.4 Others

- 8.3 Packaging

- 8.3.1 Food & Beverages

- 8.3.2 Processing & Sorting

- 8.3.3 Packaging & Palletizing

- 8.3.4 Others

- 8.4 Metal & Machinery

- 8.4.1 Machining & Cutting

- 8.4.2 Casting & Forging

- 8.4.3 Others

- 8.5 Healthcare & Medical

- 8.5.1 Surgical Robotics

- 8.5.2 Rehabilitation & Prosthetics

- 8.5.3 Laboratory Automation

- 8.5.4 Others

- 8.6 Chemicals & Materials

- 8.6.1 Batch Processing

- 8.6.2 Material Handling & Mixing

- 8.6.3 Others

- 8.7 Logistics & Warehousing

- 8.7.1 Automated Guided Vehicles (AGVs)

- 8.7.2 Sorting & Distribution Systems

- 8.7.3 Pick & Place Operations

- 8.7.4 Others

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 ABB Ltd

- 10.1.2 Festo SE & Co. KG

- 10.1.3 Moog Inc.

- 10.1.4 SMC Corporation

- 10.1.5 Harmonic Drive Systems Inc.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Parker Hannifin Corporation

- 10.2.1.2 Actuonix Motion Devices Inc.

- 10.2.1.3 Firgelli Technologies Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Nabtesco Corporation

- 10.2.2.2 Yaskawa Electric Corporation

- 10.2.3 Europe

- 10.2.3.1 Schaeffler Group

- 10.2.3.2 Technosoft SA

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Technosoft SA

- 10.3.2 Oriental Motor Co, Ltd.