|

시장보고서

상품코드

2071256

전지형 크레인 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)All-Terrain Crane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

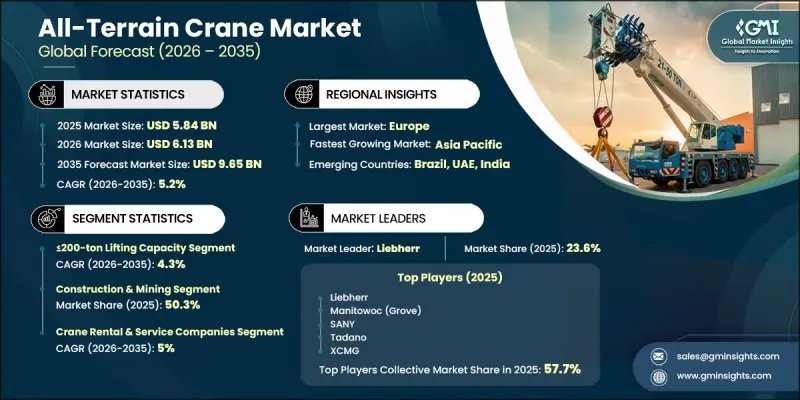

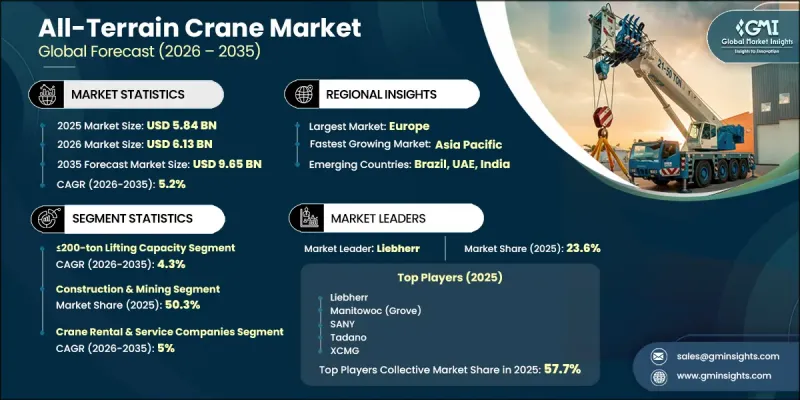

세계의 전지형 크레인 시장은 2025년에 58억 4,000만 달러 규모에 이르고, CAGR 5.2%로 성장하여 2035년까지 96억 5,000만 달러에 달할 것으로 추정되고 있습니다.

전지형 크레인 업계 전반의 성장은 인프라 개발, 재생에너지 프로젝트, 산업용 건설 및 장비 임대 서비스에 대한 투자 확대에 힘입어 계속해서 뒷받침되고 있습니다. 에너지 및 산업 분야에서 중량물 운반 솔루션에 대한 수요가 증가함에 따라, 더욱 복잡한 프로젝트 요구 사항을 충족할 수 있는 대용량 크레인 모델의 도입이 촉진되고 있습니다. 대규모 제조 시설, 가공 플랜트, 에너지 인프라 개발 및 대규모 토목 공사 프로젝트로 인해 중-대형 크레인에 대한 지속적인 수요가 발생하고 있습니다. 일부 개발도상국에서 진행되고 있는 급속한 도시화와 산업화가 시장 전망을 더욱 밝게 하고 있습니다. 또한, 전지형 크레인은 대규모 수송 지원 없이도 작업 현장 간을 효율적으로 이동할 수 있다는 점이 여전히 큰 경쟁 우위를 차지하고 있습니다. 이러한 기동성 덕분에 운용의 유연성이 향상되고, 배치 시간이 단축되며, 함대의 가동률이 높아져 비용 대비 효과가 높은 프로젝트 수행을 뒷받침하기 때문에 전지형 크레인은 전 세계의 다양한 건설 및 산업 분야에서 선호되는 선택지가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 58억 4,000만 달러 |

| 예측액 | 96억 5,000만 달러 |

| CAGR | 5.2% |

200톤 이하 적재 능력 부문은 2025년에 44억 5,240만 달러의 매출을 기록하며 시장 점유율의 76.2%를 차지했습니다. 이 용량 범위의 크레인에 대한 수요는 인프라 개발, 상업 건축, 공공시설의 유지 관리, 그리고 중규모 산업 운영 등 폭넓은 분야에서 활용도가 높기 때문에 계속해서 견조한 추세를 보이고 있습니다. 이 크레인들은 적재 능력, 기동성 및 운영 효율성 간의 균형이 뛰어나며, 다양한 프로젝트 요구 사항에 적합합니다. 교통망, 도시 개발 사업 및 산업 시설에 대한 지속적인 투자를 통해 향후 몇 년간 이 부문에 대한 수요가 유지될 것으로 예상되며, 전 세계 전지형 크레인 시장에서 이 부문의 지배적 지위가 더욱 공고해질 것으로 전망됩니다.

2025년, 건설 및 광업 부문 시장 규모는 29억 3,900만 달러에 달했으며, 시장 점유율의 50.3%를 차지했습니다. 이러한 성장은 대규모 인프라 프로젝트, 자원 채굴 시설 및 대규모 토목 공사에 대한 지속적인 투자에 힘입어 이루어지고 있습니다. 이러한 용도에서는 가혹한 작업 환경에서도 높은 적재 정밀도, 뛰어난 기동성, 그리고 신뢰성 높은 성능을 발휘할 수 있는 장비가 요구됩니다. 이 부문에서 제품의 차별화는 첨단 리프팅 기술, 운영 효율성 향상, 안정성 시스템 강화, 디지털 모니터링 기능, 그리고 최적화된 하중 관리 기능에 점점 더 중점을 두고 있습니다. 프로젝트의 복잡성이 계속 증가하는 가운데, 기술적으로 고도로 발전된 전지형 크레인에 대한 수요는 계속해서 견조할 것으로 예측됩니다.

북미의 전지형 크레인 시장은 2025년에 16억 4,200만 달러 규모를 기록하고, 2035년까지 24억 1,200만 달러에 달할 것으로 예상되며, 2026년부터 2035년에 걸쳐 연평균 성장률(CAGR) 3.9%로 확대될 것으로 전망됩니다. 시장의 확대는 교통 인프라, 에너지 프로젝트, 산업 시설 및 상업 건축 활동에 대한 지속적인 투자를 바탕으로 이루어지고 있습니다. 다양한 프로젝트의 요구에 대응할 수 있는 범용성이 높은 리프팅 장비에 대한 수요가 증가함에 따라, 향후 10년 동안 해당 지역 전체에서 전지형 크레인에 대한 수요가 견조한 추세를 보일 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 적재 능력별, 2022년-2035년

제6장 시장 추산 및 예측 : 추진력별, 2022년-2035년

제7장 시장 추산 및 예측 : 용도별, 2022년-2035년

제8장 시장 추산 및 예측 : 최종사용자별, 2022년-2035년

제9장 시장 추산 및 예측 : 지역별, 2022년-2035년

제10장 기업 개요

LSH 26.07.02The Global All-Terrain Crane Market was valued at USD 5.84 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 9.65 billion by 2035.

Growth across the all-terrain crane industry continues to be supported by expanding investments in infrastructure development, renewable energy projects, industrial construction, and equipment rental services. Increasing demand for heavy lifting solutions in the energy and industrial sectors is encouraging the adoption of higher-capacity crane models capable of handling more complex project requirements. Large-scale manufacturing facilities, processing plants, energy infrastructure developments, and heavy civil engineering projects are generating sustained demand for cranes within the mid- to high-capacity range. Rapid urbanization and industrialization across several developing economies are further strengthening market prospects. In addition, the ability of all-terrain cranes to travel efficiently between job sites without requiring extensive transportation support remains a major competitive advantage. This mobility enhances operational flexibility, reduces deployment times, improves fleet utilization rates, and supports cost-effective project execution, making all-terrain cranes a preferred choice across a wide range of construction and industrial applications worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.84 Billion |

| Forecast Value | $9.65 Billion |

| CAGR | 5.2% |

The <=200-ton lifting capacity segment generated USD 4,452.4 million in 2025 and accounted for 76.2% share. Demand for cranes within this capacity range remains strong due to their versatility across infrastructure development, commercial construction, utility maintenance, and medium-scale industrial operations. These cranes offer an effective balance between lifting performance, mobility, and operational efficiency, making them well-suited for a broad range of project requirements. Continued investment in transportation networks, urban development initiatives, and industrial facilities is expected to sustain demand for this segment over the coming years, reinforcing its dominant position within the global all-terrain crane market.

The construction and mining segment accounted for USD 2,939 million in 2025, representing 50.3% share. Growth is driven by ongoing investments in large-scale infrastructure projects, resource extraction facilities, and heavy civil engineering developments. These applications require equipment capable of delivering high lifting precision, strong maneuverability, and reliable performance across challenging operating environments. Product differentiation within the segment is increasingly centered on advanced lifting technologies, improved operational efficiency, enhanced stability systems, digital monitoring capabilities, and optimized load management features. As project complexity continues to increase, demand for technologically advanced all-terrain cranes is expected to remain strong.

North America All-Terrain Crane Market generated USD 1,642 million in 2025 and is forecast to reach USD 2,412 million by 2035, expanding at a CAGR of 3.9% during 2026-2035. Market expansion is supported by continued investments in transportation infrastructure, energy projects, industrial facilities, and commercial construction activities. Growing requirements for versatile lifting equipment capable of supporting diverse project needs are expected to maintain steady demand for all-terrain cranes throughout the region over the next decade.

Key participants operating in the global all-terrain crane market include Liebherr, Manitowoc (Grove), XCMG, Tadano, SANY, Zoomlion, and Terex. Companies operating within the all-terrain crane industry are implementing a variety of strategies to strengthen their market position and expand their global footprint. Leading manufacturers are investing heavily in product innovation, focusing on higher lifting capacities, improved fuel efficiency, advanced telematics, and enhanced safety technologies to meet evolving customer requirements. Strategic partnerships with rental companies, construction contractors, and industrial project developers are helping firms broaden their customer base and improve market penetration. Companies are also expanding service networks, strengthening aftermarket support, and investing in digital fleet management solutions to enhance customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Lifting Capacity

- 2.2.2 Propulsion

- 2.2.3 Application

- 2.2.4 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Infrastructure Construction

- 3.2.1.2 Growth of Renewable Energy Installations

- 3.2.1.3 Industrial and Petrochemical Project Development

- 3.2.1.4 Operational Flexibility and Mobility Advantages

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Equipment Acquisition and Maintenance Costs

- 3.2.2.2 Shortage of Skilled Crane Operators

- 3.2.2.3 Economic and Construction Industry Cyclicality

- 3.2.3 Market opportunities

- 3.2.3.1 Hybrid and Electric Propulsion Adoption

- 3.2.3.2 High-Capacity Wind Energy Crane Demand

- 3.2.3.3 Rental Fleet Expansion in Emerging Markets

- 3.2.3.4 Digital Lift Planning and Telematics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technologies

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 OSHA Crane & Derrick Standards

- 3.6.1.2 ASME B30.5 - Mobile & Locomotive Cranes

- 3.6.1.3 NCCCO Crane Operator Certification

- 3.6.1.4 CSA Z150 - Safety Code on Mobile Cranes

- 3.6.2 Europe

- 3.6.2.1 EU Machinery Directive 2006/42/EC

- 3.6.2.2 EU Stage V Emission Regulation (EU 2016/1628) - Non-Road Mobile Machinery

- 3.6.2.3 EN 13000 - Mobile Cranes Safety Standard

- 3.6.2.4 LOLER - Lifting Operations & Lifting Equipment Regulations

- 3.6.3 Asia-Pacific

- 3.6.3.1 GB/T 14560 - Mobile Crane Safety Standard (China)

- 3.6.3.2 CCMA Crane Type Certification (China)

- 3.6.3.3 JCMA Safety Standards (Japan)

- 3.6.3.4 DGFASLI Crane Safety Regulations (India)

- 3.6.3.5 AS 2550.5 - Cranes Safety in Use (Australia)

- 3.6.4 Latin America

- 3.6.4.1 NR-11 / NR-12 - Lifting & Machinery Safety Regulations (Brazil)

- 3.6.4.2 NOM-009-STPS - Work at Height & Lifting Equipment (Mexico)

- 3.6.5 Middle East & Africa

- 3.6.5.1 OSHAD SF CoP 33 - Lifting Operations (UAE)

- 3.6.5.2 Saudi Aramco SAES - Lifting Equipment Standards (Saudi Arabia)

- 3.6.5.3 SANS 10142 / DMR - Lifting Machinery Regulations (South Africa)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Trade Data Analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Cost breakdown analysis

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 Automated design optimization

- 3.12.3 Supply chain AI for demand forecasting

- 3.12.4 GenAI use cases & adoption roadmap by segment

- 3.12.5 Risks, Limitations & Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Lifting Capacity, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 ≤200 Tons

- 5.3 200-500 Tons

- 5.4 >500 Tons

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 ICE (Internal Combustion Engine)

- 6.3 Hybrid / Electric

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Construction & Mining

- 7.3 Utility

- 7.4 Manufacturing

- 7.5 Transport/Shipping

- 7.6 Oil & Gas/Energy

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End-User, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Infrastructure Contractors

- 8.3 Industrial & Manufacturing Facilities

- 8.4 Energy & Utilities Companies

- 8.5 Crane Rental & Service Companies

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.2.9 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.3.9 Thailand

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

- 9.5.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Konecranes

- 10.1.2 Liebherr

- 10.1.3 Manitowoc (Grove)

- 10.1.4 Palfinger

- 10.1.5 SANY

- 10.1.6 Sarens

- 10.1.7 Tadano

- 10.1.8 Terex

- 10.1.9 XCMG

- 10.1.10 Zoomlion

- 10.2 Regional Players

- 10.2.1 ALL Family of Companies

- 10.2.2 HSC Cranes

- 10.2.3 KATO Works

- 10.2.4 Kobelco Cranes

- 10.2.5 Link-Belt Cranes

- 10.2.6 Maxim Crane Works

- 10.2.7 Spierings Mobile Cranes

- 10.3 Emerging Players / Disruptors

- 10.3.1 Altrad Sparrows

- 10.3.2 Manitex International

- 10.3.3 Sennebogen