|

시장보고서

상품코드

2071343

모듈식 포장 장비 시장 : 성장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Global Modular Packaging Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

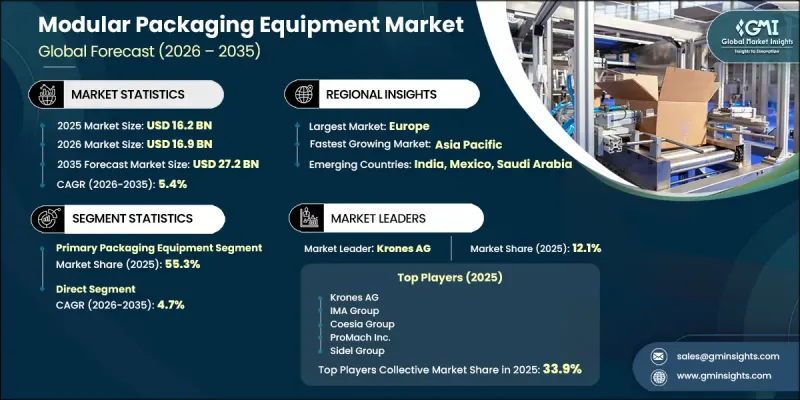

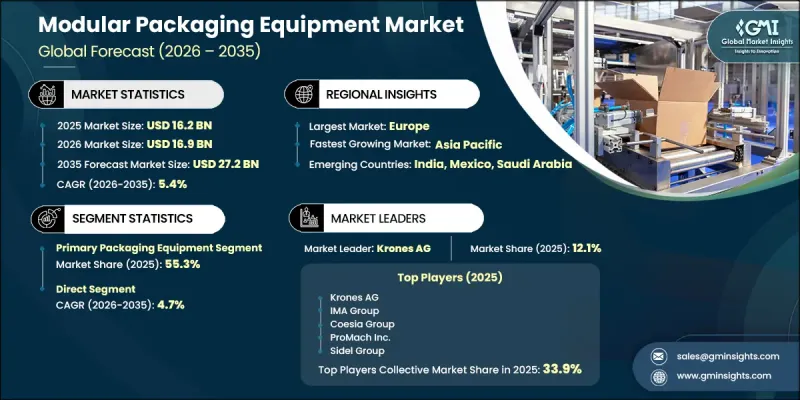

세계의 모듈식 포장 장비 시장은 2025년에 162억 달러 규모가 되어, CAGR 5.4%로 성장하여 2035년까지 272억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 신속한 전환 능력이 요구되는 제품 포트폴리오의 복잡화, 유럽의 포장 폐기물 감축 정책과 관련된 환경 규제 강화, 선진 제조 경제권에서의 지속적인 노동력 부족 등 여러 구조적 요인에 의해 형성되고 있습니다. 이러한 요인들이 복합적으로 작용함에 따라, 제조업체들이 규제 준수와 업무 효율성을 유지하면서 생산 민첩성을 높일 수 있도록 하는 모듈식 설비 설계의 도입이 가속화되고 있습니다. 특히 소비재(FMCG) 및 제약 업계에서는 수요가 활발합니다. 이러한 업계에서는 빈번한 제품 라인업 변경, 엄격한 품질 기준, 그리고 제품 수명 주기의 단축으로 인해 적응성이 뛰어난 생산 인프라가 요구되고 있습니다. 각 제조업체들은 신속한 구성 변경과 확장 가능한 생산 능력을 지원하는 시스템을 점점 더 우선시하고 있으며, 이를 통해 변화하는 시장 요구 사항에 보다 효과적으로 대응할 수 있게 되었습니다. 생산 환경이 더욱 높은 유연성과 자동화를 향해 지속적으로 진화하는 가운데, 모듈식 포장 장비는 전 세계 산업 분야에서 차세대 제조 전략의 핵심 요소로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 162억 달러 |

| 예측 금액 | 272억 달러 |

| CAGR | 5.4% |

1차 포장 장비 부문은 2025년에 55.3%의 시장 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 5%로 성장할 것으로 전망됩니다. 이 부문은 식품, 음료, 의약품 분야의 충전, 밀봉, 성형 시스템에 대한 활발한 수요 덕분에 계속해서 주도적인 위치를 유지하고 있습니다. 다양한 제품 형태에 대응할 수 있는 유연한 생산 라인에 대한 수요, 엄격한 위생 요건, 그리고 지속적으로 발전하는 재료 기준이 모듈식 1차 포장 솔루션의 도입을 촉진하고 있습니다. 의약품 제조 분야에서는 첨단 치료법이나 특수한 약물 전달 형태의 생산이 증가하고 있어, 적응성이 높고 재구성 가능한 설비 시스템에 대한 수요가 더욱 높아지고 있습니다.

직접 판매 채널은 2025년에 55.8%의 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 4.7%로 성장할 것으로 전망됩니다. 이 채널에는 맞춤형 시스템 도입, 통합 생산 라인 솔루션, 그리고 장기 서비스 계약을 통한 장비 제조업체와 최종 사용자 간의 직접적인 협력 관계가 포함됩니다. 이는 맞춤형 엔지니어링, 시스템 검증 및 지속적인 기술 지원이 필요한 복잡한 제조 설비 분야에서 여전히 선호되는 모델입니다. 또한, 직접 조달 구조를 통해 제조업체와 설비 공급업체 간의 보다 긴밀한 협력이 가능해지며, 이는 시스템 성능 최적화 및 수명 주기 관리의 개선으로 이어집니다.

북미의 모듈식 포장 장비 시장은 2025년에 28.4%의 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 4.3%로 성장할 것으로 전망됩니다. 이 지역 수요는 주로 식품 및 음료 및 제약 제조 부문에 의해 주도되고 있으며, 이러한 분야에서는 인건비 상승, 엄격한 규제 준수 요건, 그리고 유연한 생산 능력에 대한 수요 증가가 모듈식 시스템에 대한 투자를 촉진하고 있습니다. 각 제조업체들은 업무 효율 향상과 제품 교체에 따른 가동 중단 시간 감소를 도모하기 위해 자동화 및 재구성 가능한 포장 시스템의 도입을 점점 더 확대하고 있으며, 이는 해당 지역 시장 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 자동화 레벨별, 2022-2035년

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 유통 채널별, 2022-2035년

제9장 시장 추산 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

JHS 26.07.01The Global Modular Packaging Equipment Market was valued at USD 16.2 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 27.2 billion by 2035.

Growth is shaped by multiple structural forces, including the increasing complexity of product portfolios that require rapid changeover capabilities, stricter environmental regulations linked to packaging waste reduction policies in Europe, and ongoing labor shortages in advanced manufacturing economies. These combined factors are accelerating the adoption of modular equipment designs that allow manufacturers to enhance production agility while maintaining regulatory compliance and operational efficiency. Demand is particularly strong across fast-moving consumer goods and pharmaceutical manufacturing, where frequent product variation, strict quality standards, and shorter product life cycles require highly adaptable production infrastructure. Manufacturers are increasingly prioritizing systems that support rapid configuration changes and scalable production capacity, enabling them to respond more effectively to shifting market requirements. As production environments continue to evolve toward higher flexibility and automation, modular packaging equipment is becoming a core component of next-generation manufacturing strategies across global industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.2 Billion |

| Forecast Value | $27.2 Billion |

| CAGR | 5.4% |

The primary packaging equipment segment accounted for 55.3% share in 2025 and is projected to grow at a CAGR of 5% through 2035. This segment continues to lead due to strong demand for filling, sealing, and forming systems across food, beverage, and pharmaceutical applications. The need for flexible production lines capable of handling diverse product formats, strict hygiene requirements, and evolving material standards is reinforcing the adoption of modular primary packaging solutions. In pharmaceutical manufacturing, the increasing production of advanced therapies and specialized drug delivery formats is further strengthening demand for adaptable and reconfigurable equipment systems.

The direct distribution channel represented 55.8% share in 2025 and is expected to grow at a CAGR of 4.7% through 2035. This channel includes direct engagement between equipment manufacturers and end users through customized system deployment, integrated production line solutions, and long-term service agreements. It remains the preferred model for complex manufacturing installations that require tailored engineering, system validation, and ongoing technical support. Direct procurement structures also enable closer collaboration between manufacturers and equipment providers, improving system performance optimization and lifecycle management.

North America Modular Packaging Equipment Market held a 28.4% share in 2025 and is projected to grow at a CAGR of 4.3% through 2035. Demand in the region is primarily driven by food and beverage as well as pharmaceutical manufacturing sectors, where investment in modular systems is supported by increasing labor costs, strict regulatory compliance requirements, and rising demand for flexible production capabilities. Manufacturers are increasingly adopting automated and reconfigurable packaging systems to improve operational efficiency and reduce downtime associated with product changeovers, further supporting regional market growth.

Key companies operating in the Global Modular Packaging Equipment Market include Coesia Group, Syntegon Technology, Krones AG, Multivac Group, IMA Group, Schubert Group, ProMach Inc., Sidel Group, Optima Packaging Group, Ishida Co., Ltd., ULMA Packaging, Marchesini Group, Robopac / Aetna Group, Fuji Machinery Co., Ltd., TNA Solutions, Mpac Group plc, Nichrome India Pvt. Ltd., Combi Packaging Systems, Massman Companies, Truking Technology Ltd., and Cama Group. Companies operating in the modular packaging equipment market are focusing on advanced automation integration, system modularity enhancement, and digitalization of packaging operations to strengthen their competitive position. Manufacturers are investing in smart equipment technologies, predictive maintenance capabilities, and IoT-enabled production monitoring systems to improve efficiency and reduce downtime. Strategic partnerships with end-use industries are enabling the co-development of customized packaging solutions tailored to specific production requirements. Companies are also expanding global service networks and aftermarket support capabilities to enhance customer retention and lifecycle value. In addition, firms are emphasizing sustainability-driven innovation, including energy-efficient machinery designs and reduced material waste systems, to align with evolving environmental regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.2.1 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Type

- 2.2.3 Automation Level

- 2.2.4 End Use

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising SKU proliferation & demand for rapid format changeover across FMCG & pharma

- 3.2.1.2 Labor cost escalation & skilled technician shortages driving automation adoption

- 3.2.1.3 Growth of e-commerce & direct-to-consumer fulfillment requiring flexible line configurations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Standardization gaps- interoperability between multi-vendor modular components

- 3.2.2.2 Cybersecurity risks in IIoT-connected modular packaging lines

- 3.2.3 Opportunities

- 3.2.3.1 Industrialization & packaging modernization in Asia Pacific & MEA

- 3.2.3.2 Modular-as-a-service (MaaS) & equipment-as-a-service (EaaS) business model adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Standards & Compliance Requirements

- 3.4.2 Regional Regulatory Frameworks

- 3.4.3 Certification Standards

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.6.1 Current trends

- 3.6.2 Emerging trends

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS Code-8422)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen-AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Capacity & production landscape (driven by primary research)

- 3.13.1 Installed capacity by region & key producer (driven by primary research)

- 3.13.2 Capacity utilization rates & expansion pipelines(driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Primary Packaging Equipment

- 5.2.1 Filling Machines

- 5.2.2 Sealing Machines

- 5.2.3 Labeling Machines

- 5.2.4 Coding & Marking Equipment

- 5.3 Secondary Packaging Equipment

- 5.3.1 Cartoning Machines

- 5.3.2 Case Packing Systems

- 5.3.3 Shrink Wrapping Machines

- 5.3.4 Palletizing Equipment

- 5.4 Tertiary Packaging Equipment

- 5.4.1 Stretch Hooding Systems

- 5.4.2 Unitizing & Strapping Systems

Chapter 6 Market Estimates and Forecast, By Automation Level, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual modular equipment

- 6.3 Semi-automatic systems

- 6.4 Automatic systems

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food and beverage

- 7.3 Pharmaceuticals

- 7.4 Cosmetics and personal care

- 7.5 Chemical and agrochemical

- 7.6 Electronics

- 7.7 Others (automotive, etc.)

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Companies

- 10.1.1 Coesia Group

- 10.1.1.1 Business Overview

- 10.1.1.2 Financial Data

- 10.1.1.3 Product Landscape

- 10.1.1.4 Strategic Outlook

- 10.1.1.5 SWOT Analysis

- 10.1.2 IMA Group

- 10.1.3 Krones AG

- 10.1.4 Multivac Group

- 10.1.5 ProMach Inc.

- 10.1.6 Sidel Group

- 10.1.7 Syntegon Technology

- 10.1.1 Coesia Group

- 10.2 Regional Companies

- 10.2.1 Fuji Machinery Co., Ltd.

- 10.2.2 Ishida Co., Ltd.

- 10.2.3 Marchesini Group

- 10.2.4 Optima Packaging Group

- 10.2.5 Robopac / Aetna Group

- 10.2.6 Truking Technology Ltd.

- 10.2.7 ULMA Packaging

- 10.3 Emerging Companies

- 10.3.1 Cama Group

- 10.3.2 Combi Packaging Systems

- 10.3.3 Massman Companies

- 10.3.4 Mpac Group plc

- 10.3.5 Nichrome India Pvt. Ltd.

- 10.3.6 Schubert Group

- 10.3.7 TNA Solutions