|

시장보고서

상품코드

2072630

연포장용 디지털 인쇄 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Digital Printing For Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

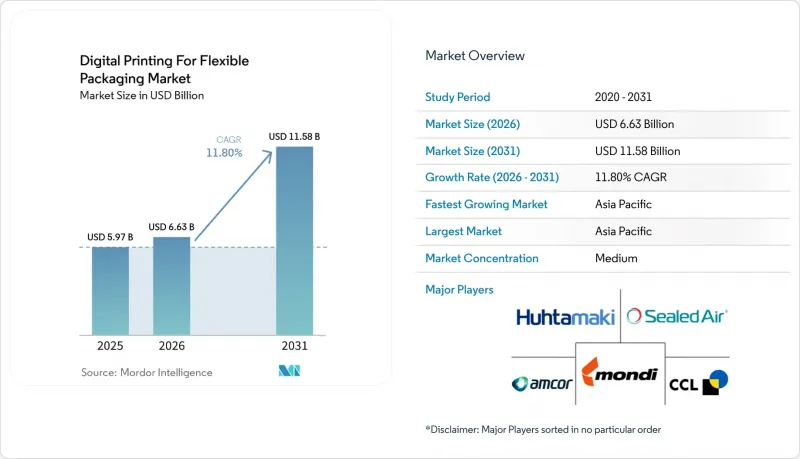

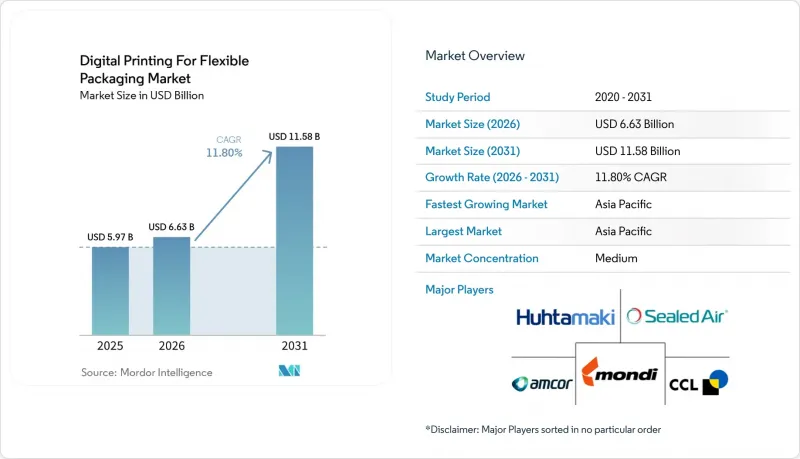

Mordor Intelligence에 의하면, 연포장용 디지털 인쇄 시장 규모는 2025년에 59억 7,000만 달러로 평가되었고, 2026년에 66억 3,000만 달러로 추정되고, 2031년까지 115억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 11.80%로 성장할 전망입니다.

본 보고서는 인쇄 기술별(전자사진, UV 잉크젯, 수성 잉크젯 등), 포장 유형별(파우치, 스틱팩, 소포장 등), 잉크 유형별(UV 경화형 잉크 등), 소재 유형별(종이 및 종이계 라미네이트 등), 최종 사용자 산업별(식품, 음료 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 연포장용 디지털 인쇄 동향 및 인사이트

소량 SKU 증가가 연포장 제품의 대량 생산 경제성을 견인하고 있습니다.

SKU 증가는 단순한 브랜딩 활동의 범위를 넘어, 현재는 연포장용 디지털 인쇄 시장의 생산 계획, 설비 활용 및 컨버터의 투자에 영향을 미치고 있습니다. FTA FORUM INFOFLEX 2026에서 Siegwerk, GEW, Flint Group의 연사들은 각 브랜드 기업들이 소량 주문을 하는 한편, 디자인부터 매장 진열에 이르기까지의 실행 속도를 높여줄 것을 요구하고 있다고 밝혔습니다. 이로 인해 기존의 그라비아 인쇄에서 판 교체 시의 경제성이 저하되고 있습니다. 디지털 시스템에서는 작업 간에 물리적인 인쇄판 교체가 필요 없기 때문에 컨버터는 10,000-1만 5,000 단위의 로트 수 범위에서 경쟁력을 유지하기가 쉬워집니다. 이 범위에서는 아날로그 설비로는 효율적으로 대응하기가 점점 어려워지고 있습니다. 이러한 변화로 인해 과잉 재고의 위험이 줄어들고, 구식 디자인으로 인한 손실도 감소합니다. 또한, 연포장용 디지털 인쇄 시장에서 조달 팀이 공급업체를 비교할 때 총비용의 전체적인 상황을 보다 명확하게 파악할 수 있게 됩니다. 발주 패턴도 수요의 방향성을 바꾸고 있습니다. 각 브랜드사는 디지털 기능을 단순한 선택적 서비스로 취급하기보다는 공급 요건으로 요구하는 경향이 강해지고 있기 때문입니다. 그 결과, 컨버터의 투자 회수 기간은 하드웨어 자체만큼이나 고객의 문의나 수주 구성의 질에 따라 좌우되게 되었습니다.

전자상거래 물류가 지역의 배송 형태를 재편하고 있습니다.

전자상거래는 수량뿐만 아니라, 연포장용 디지털 인쇄 시장이 대응해야 하는 패키지 유형, 라벨 변경, 지역별 포맷에도 변화를 가져오고 있습니다. 중국에서는 택배 관련 국가 포장 기준에 따라 대규모 온라인 판매업체 전반에 걸쳐 신속한 디자인 업데이트의 필요성이 높아지고 있으며, 이는 실린더를 빈번하게 교체하는 것보다 디지털 생산에 더 적합합니다. 인도에서는 퀵 커머스 방식의 식료품 판매 모델이 경량 파우치 및 소포장에 대한 지속적인 수요를 견인하고 있으며, 이를 위해서는 지역 언어 지원, 현지 맞춤형 프로모션, 짧은 재고 보충 주기가 요구됩니다. 이 점은 중요합니다. 왜냐하면 온라인 수요는 단일한 대규모 주문 흐름으로 발생하는 것이 아니라, 지역별, 계절별 또는 캠페인 중심의 수많은 SKU로 나뉘어 있으며, 컨버터는 이를 동시에 관리해야 하기 때문입니다. 유럽의 브랜드 소유주들도 공통된 제품 구조를 각국의 언어 및 표시 방식의 차이에 맞추는 과정에서 유사한 과제에 직면하고 있으며, 이것이 연포장 분야에서 디지털 인쇄의 보급을 촉진하고 있습니다. 따라서 디지털의 민첩성은 단순한 인쇄 비용 절감 수단에 그치지 않고, 공급망을 관리하는 도구로서도 기능합니다.

막대한 설비 투자가 장기적인 경제성에 대한 투자 회수 위험을 초래하고 있습니다.

자본 비용은 연포장용 디지털 인쇄 시장에서 여전히 가장 뚜렷한 단기적 장벽으로 남아 있습니다. 특히, 현장에서 아직 사용할 수 있는 아날로그 설비를 보유하고 있는 컨버터의 경우 더욱 그렇습니다. 다양한 기판에 대응할 수 있는 생산용 인쇄기는 일반적으로 100만 달러 이상의 비용이 소요되며, 워크플로우 통합으로 인해 안정적인 생산량을 달성하기까지의 총 투자액은 더욱 증가합니다. 투자 회수 전망은 수주 잔고에 충분한 소·중량 주문이 있는지 여부에 달려 있지만, 많은 컨버터 업체들은 고객과의 계약이 기존의 장기 생산을 전제로 체결되어 있기 때문에 그러한 수주 구성을 보장할 수 없습니다. 이에 대해 Flint Group 디지털 제이콘은 'Ecolyne' 구독 모델을 도입했습니다. 이 모델은 2025년 하반기 아시아태평양에서 처음 출시된 후, 2026년에 전 세계로 확대되었습니다. 이 모델은 막대한 설비 투자를 지속적인 운영 비용으로 간주하고, 컨버터의 규모를 단계적으로 확대할 수 있도록 함으로써 초기 도입의 장벽을 낮추고 있습니다. 그럼에도 불구하고, 많은 구매자들은 생산 구성, 고객 수요, 가동률이 양호한 상태를 유지할 수 있다는 명확한 증거를 여전히 요구하고 있기 때문에 설비 투자 문제가 연포장용 디지털 인쇄 시장의 도입을 가로막는 걸림돌로 남아 있습니다.

부문별 분석

2025년, UV 잉크젯은 연포장용 디지털 인쇄 시장에서 30.88%의 점유율을 차지했습니다. 이는 풍부한 도입 실적, 다양한 기판에 대한 대응 능력, 그리고 탄탄한 서비스 지원을 반영한 것입니다. 이 제품의 강점은 다양한 유연 필름에 대응할 수 있을 뿐만 아니라, 기존 컨버터의 워크플로우에 적합하며, 일부 경쟁 공정에 비해 불필요한 준비 공정이 적다는 점에 있습니다. 전자사진 방식에 비해 UV 잉크젯은 PE 및 PP 필름의 용도에 더 적합합니다. 이러한 용도에서는 생산 팀이 더 간편한 기판 취급과 확실한 접착력을 원하고 있습니다. 변환기 제조업체는 생산 규모를 확대할 때 인증 기간 단축, 작업자 재교육, 공급망의 복잡성 완화를 가능하게 하는 시스템을 선호하는 경향이 있으므로, 이러한 운영상의 호환성은 중요합니다. 연포장용 디지털 인쇄 시장에서 이러한 실용적인 요인들이 새로운 기술이 확산되는 상황 속에서도 UV 잉크젯이 주요 수익원으로 남아 있는 한 가지 이유가 되고 있습니다.

수성 잉크젯도 종이 기반 용도 분야에서 발전하고 있으며, SCREEN Europe사의 'Truepress PAC 520P'는 현재 이탈리아의 Sacchital사에서 분당 80m의 속도로 본격적인 상업 생산이 이루어지고 있습니다. 이 시스템은 플레이트나 금형이 필요하지 않으며, 식품 안전 기준을 준수하는 수성 잉크가 사용됩니다. 하이브리드 인쇄기는 2031년까지 연평균 성장률(CAGR) 14.38%를 기록하며 성장할 것으로 예상되며, 이 시장에서 가장 빠르게 성장하고 있는 기술 분야로 꼽히고 있습니다. 2025년 Gallus Five의 출시는 각 컨버터 업체들이 산업 수준의 처리 능력을 유지하면서도 다양한 작업 흐름에 대응할 수 있는 디지털 시스템의 유연성을 겸비한 시스템을 원하고 있음을 보여줍니다. 하이브리드 시스템은 순수 디지털 설비만으로는 수익성을 확보하기 어려운 중량 생산에 대한 디지털 대응 범위를 확대하기 위해, 단순히 구형 디지털 기기를 교체하는 데 그치지 않고 수주 가능한 프로젝트의 폭을 넓혀줍니다. 그 대가로, 변환기 제조업체들은 이처럼 고속이긴 하지만 자본 집약도가 높은 대안을 채택하기 전에, 소량에서 중량에 이르는 수요가 지속될 것이라는 확신을 더욱 굳게 가져야 하는 것이 일반적입니다.

2025년, 파우치는 37.04%의 시장 점유율을 차지했으며, 이 부문에서 가장 큰 포맷으로 자리매김했고, 식품, 음료, 개인 위생 용품, 가정용품 등 각 용도 분야에서 핵심적인 역할을 수행하고 있는 것으로 확인되었습니다. 이 리드는 차단 성능, 매장 내 시각적 효과, 소비자의 편의성, 그리고 잦은 디자인 변경에 대응할 수 있는 능력 간의 균형이 잘 잡혀 있음을 반영하고 있습니다. 스탠드업 파우치는 특히 디지털 인쇄의 이점을 크게 누리고 있습니다. 브랜드는 소량 아날로그 인쇄를 비현실적으로 만드는 실린더 비용을 부담하지 않고도, 단일 캠페인에서 여러 가지 디자인 변형을 선보일 수 있기 때문입니다. 랩이나 롤 스톡은 여전히 광범위한 산업 분야에서 활용되고 있으며, 특히 장기간에 걸친 식품 용도의 경우 아날로그 생산 방식과의 연계가 여전히 더 밀접한 상태입니다. 그렇긴 하지만, 프로모션용 오버랩이나 한정판 캠페인에서는 단위 비용보다 출시 속도가 더 중요시되는 경우가 많기 때문에 디지털 인쇄의 활용이 확대되고 있습니다.

스틱팩과 향주머니 시장은 2031년까지 연평균 성장률(CAGR) 12.74%를 기록하며 성장할 것으로 예상되며, 이는 모든 포장 형태 중 가장 높은 성장 속도입니다. 이러한 성장은 1회분 단위의 영양 보충제, 편의성을 중시한 퍼스널케어 제품, 그리고 컴팩트한 형태와 빈번한 아트워크 변경이 필요한 전자상거래 주문 처리 모델과 발을 맞추고 있습니다. 또한, 일부 일반의약품이 봉지 형태로 전환되고 있는 점과, 추적성 및 환자 정보를 위해 단위별 가변 데이터가 필요하다는 점 때문에 의약품 분야 수요도 확대되고 있습니다. 도미노 프린텍 인디아는 일련번호 부여 수요와 포장 형식의 유연성이 정확히 교차하는 이러한 요구에 부응하기 위해, CPHI 및 PMEC 2025에서 최대 250 m/min의 속도를 자랑하는 가변 데이터 인쇄 시스템 'K300'을 발표했습니다. 봉투나 그 밖의 포장 형태도 여전히 중요하지만, 범용 제품이나 대량 포장 용도에 대한 의존도가 높기 때문에 이러한 분야에서는 기존의 대량 인쇄가 여전히 경제적으로 유리한 위치를 차지하고 있습니다.

지역별 분석

아시아태평양은 2025년 연포장용 디지털 인쇄 시장 규모의 35.95%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 13.06%로 확대될 것으로 전망됩니다. 이 지역은 최대의 생산량 기반과 가장 빠른 성장률을 모두 갖추고 있으며, 이러한 드문 조합은 포장 수요가 전자상거래 규모, 소비재(FMCG), 그리고 지역별 제품 다양성과 얼마나 밀접하게 연관되어 있는지를 보여줍니다. 중국은 여전히 중심적인 위치를 차지하고 있습니다. 이는 온라인 소매 활동의 활성화, 패키지의 빈번한 업데이트, 그리고 표준화에 대한 필요성으로 인해 소량 디지털 인쇄가 자연스럽게 요구되고 있기 때문입니다. 인도 역시 의약품의 시리얼화, 퀵 커머스를 통한 식료품 판매 확대, 그리고 식품 접촉 재료에 대한 규제 강화로 인해 컨버터들이 더욱 신속하고 연포장 형태를 요구하게 되면서 주요 성장 거점으로 부상하고 있습니다. BOBST사는 상하이에서 개최된 'Chinaplas 2026'에서 중국 컨버터 기업과 공동으로 디지털이자 지속 가능한 연포장 솔루션을 전시하며, 이러한 수요가 해당 지역에 중요함을 강조했습니다.

2026년 시점에서 북미와 유럽은 연포장용 디지털 인쇄 시장에서 가장 성숙한 기술 기반을 갖추고 있었으나, 본 자료에서는 각 시장의 지역별 점유율은 별도로 제시되지 않았습니다. 북미에서는 ePac사가 2026년 3월 피닉스에 새로운 시설을 개설하고, 애틀랜타, 필라델피아, 밴쿠버에서도 생산 능력을 확대하고 있어, 디지털 연포장 시장이 고립된 지역적 확장이 아닌 보다 광범위한 네트워크 구축으로 전환되고 있음을 보여주고 있습니다. 유럽에서는 PPWR 2025/40 및 독일의 인쇄 잉크 규정이 잉크와 기판의 인증 기준 선정에 영향을 미치고 있어, 보다 엄격한 규정 준수 조건 하에서 발전하고 있습니다. 또한, ePac의 셰필드 거점에 EMEA 지역 최초로 HP Indigo 200K가 도입된 것은 지역적 규모 확대가 시범 단계에 그치는 것이 아니라 보다 상업적인 단계로 접어들고 있음을 보여줍니다.

남미, 중동 및 아프리카 및 기타 소규모 시장에서는 2025년 시점에서도 도입이 초기 단계에 머물러 있었으며, 그 진전은 현재의 디지털 설비 도입 상황보다는 패키지의 현대화나 현지 브랜드 개발에 크게 좌우되었습니다. 브라질은 남미 시장에서 가장 큰 성장 기회를 주도하고 있습니다. 이는 브랜드 식품 및 음료에 대한 수요가 증가함에 따라, 기존의 대량 생산 시스템으로는 대응하기 어려운 고품질의 그래픽, SKU의 다양화, 그리고 단기간 내의 제품 출시가 요구되고 있기 때문입니다. 아랍에미리트(UAE)와 사우디아라비아에서는 현지화된 신제품 출시 및 소량 생산에 적합한, 보다 고급스러운 식품 및 퍼스널케어 제품 포장 프로그램이 추진되고 있습니다. 남아프리카, 나이지리아, 이집트에는 추가적인 성장 여지가 있으며, 연포장용 디지털 인쇄 시장이 현재의 주요 지역을 넘어 확대됨에 따라 이들 국가의 성장 속도는 컨버터의 투자, 원자재의 확보 가능성, 그리고 전자상거래 인프라에 좌우될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the digital printing for flexible packaging market size is projected to be USD 5.97 billion in 2025, USD 6.63 billion in 2026, and reach USD 11.58 billion by 2031, growing at a CAGR of 11.80% from 2026 to 2031.

This report is Segmented by Printing Technology (Electrophotography, UV Inkjet, Water-Based Inkjet, and More), Packaging Type (Pouches, Stick Packs and Sachets, and More), Ink Type (UV-Curable Inks, and More), Material Type (Paper and Paper-Based Laminates, and More), End-User Industry (Food, Beverages, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Printing For Flexible Packaging Market Trends and Insights

Short-Run SKU Proliferation Drives Volume Economics in Flexible Packs

SKU growth has moved beyond branding activity and now affects production planning, asset use, and converter investment in the digital printing for flexible packaging market. At FTA FORUM INFOFLEX 2026, speakers from Siegwerk, GEW, and Flint Group said brands were placing smaller orders while also asking for faster design-to-shelf execution, which weakens the economics of conventional gravure changeovers. Digital systems avoid physical print forms between jobs, helping converters stay competitive in the run-length range of 10,000 to 15,000 units, which has become harder for analog assets to serve efficiently. That same shift lowers overstock risk, reduces write-offs from obsolete designs, and gives procurement teams a clearer total-cost picture when they compare suppliers in the digital printing for flexible packaging market. The ordering pattern is also changing the direction of demand, as brands are increasingly requiring digital capability as a supply requirement rather than treating it as an optional service. As a result, converter payback periods are being influenced as much by customer pull and order mix quality as by the hardware itself.

E-Commerce Logistics Reshape Regional Pack Formats

E-commerce is changing not only volume but also the number of pack versions, labeling changes, and regional formats that the digital printing for flexible packaging market must support. In China, national packaging standards for express shipments have heightened the need for rapid design updates across a large online seller base, which aligns better with digital production than repeated cylinder changes. In India, quick-commerce grocery models are driving repeat demand for lightweight pouches and sachets that require regional language support, local promotions, and short refill cycles. This matters because online demand does not flow as a single, large order stream; instead, it breaks into many geography-specific, seasonal, and campaign-led SKUs that one converter has to manage simultaneously. European brand owners face a similar issue when aligning common product structures with country-level language and labeling differences, which supports wider adoption of digital printing for flexible packaging. Digital agility, therefore, acts as a supply chain control tool, not only as a print cost tool.

High Capital Expenditure Creates Payback Risk Against Long-Run Economics

Capital cost remains the clearest short-term barrier in the digital printing for flexible packaging market, especially for converters that still have usable analog assets on the floor. Production-grade presses that can run across a broad substrate range commonly cost more than USD 1 million, and workflow integration further increases the total commitment before stable output is achieved. The payback profile depends on having enough short- and medium-run orders in the order book, and many converters cannot guarantee that mix when their customer contracts were built around longer, conventional production. Flint Group Digital Xeikon has responded with its Ecolyne subscription model, which was launched globally in 2026 after its initial Asia-Pacific introduction in late 2025. The model lowers the upfront entry point by treating a large capital commitment as a recurring operating cost and allowing converters to scale more gradually. Even so, the capex question continues to slow adoption in the digital printing for flexible packaging market because many buyers still need clear proof that run mix, customer demand, and utilization will remain favorable.

Other drivers and restraints analyzed in the detailed report include:

- Brand Demand for Variable Data and Mass Customization Accelerates Converter Migration

- Hybrid Digital Presses Resolve the Changeover-Speed Trade-Off at Scale

- Specialty Ink and Film Substrate Price Volatility Compresses Converter Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UV inkjet held 30.88% of the digital printing market share for flexible packaging in 2025, reflecting a mature installed base, broad substrate qualification, and well-developed service support. Its strength has come from how it handles a wide range of flexible films while also fitting existing converter workflows, with fewer extra preparation steps than some competing processes. Compared with electrophotography, UV inkjet is better aligned with PE and PP film applications, where production teams want simpler substrate handling and dependable adhesion. That operational familiarity matters because converters tend to favor systems that reduce qualification time, operator retraining, and supply chain complexity when they scale output. In the digital printing for flexible packaging market, those practical factors have helped UV inkjet remain the main revenue anchor even as newer technologies expand.

Water-based inkjet is also advancing in paper-based applications, and SCREEN Europe's Truepress PAC 520P is now in full commercial production at Sacchital in Italy at 80 m/min, using food-safety-compliant water-based inks without plates or tooling. Hybrid presses are projected to grow at a 14.38% CAGR through 2031, which makes them the fastest moving technology category in this market. The Gallus Five launch in 2025 showed how converters are looking for systems that preserve industrial throughput while also adding digital flexibility for mixed job streams. Hybrid systems extend digital reach into medium-run work that pure digital assets often struggle to serve profitably, so they widen the usable order mix rather than simply replacing older digital units. The tradeoff is that converters usually need stronger confidence in sustained short-to-medium run demand before they commit to this faster but more capital-intensive option.

Pouches held a 37.04% share in 2025, making them the largest format in the segment and confirming their central role across food, beverage, personal care, and household applications. Their lead reflects the balance they offer between barrier performance, shelf impact, consumer convenience, and the ability to support frequent design changes. Stand-up pouches have especially benefited from digital printing, as brands can carry multiple design variants in a single campaign without absorbing the cylinder costs that make small analog runs unattractive. Wraps and rollstock still serve a broad industrial base and remain more closely linked to analog production, particularly in long-run food applications. Even so, promotional overwraps and limited-edition campaigns are drawing more digital activity because launch speed often matters more than unit cost in those programs.

Stick packs and sachets are projected to grow at a 12.74% CAGR through 2031, which gives them the strongest pace among packaging formats. Their growth aligns with single-serve nutrition, convenience-led personal care, and e-commerce fulfillment models that require compact formats and frequent artwork changes. Pharmaceutical demand is also expanding as some over-the-counter products shift to sachet-based delivery and require unit-level variable data for traceability and patient information. Domino Printech India launched the K300 variable data printing system at CPHI and PMEC 2025 for this exact intersection of serialization demand and packaging format flexibility, with speeds up to 250 m/min. Bags and other packaging types remain relevant, but their heavier exposure to commodity and bulk applications means conventional long-run print still holds a stronger economic position there.

Complete Report Scope:

- By Printing Technology

- Electrophotography

- UV Inkjet

- Water-based Inkjet

- Hybrid Presses

- Other Printing Technologies

- By Packaging Type

- Pouches

- Stick Packs and Sachets

- Wraps and Rollstock

- Bags

- Labels

- Other Packaging Types

- By Ink Type

- UV-curable Inks

- Water-based Inks

- Solvent-based Inks

- Electron-beam (EB) Inks

- By Material Type

- Plastic Films (PET, PE, PP)

- Paper and Paper-based Laminates

- Aluminum Foil

- Compostable Films

- Other Material Types

- By End user Industry

- Food

- Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Household

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Thailand

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific accounted for 35.95% share of the digital printing for flexible packaging market size in 2025 and is projected to expand at a 13.06% CAGR through 2031. The region combines the strongest volume base with the fastest growth, an uncommon combination that shows how closely packaging demand is tied to e-commerce scale, fast-moving consumer goods, and regional product variation. China remains central because online retail activity, fast pack updates, and standardization needs create a natural case for short-run digital output. India is also becoming a major growth center as pharmaceutical serialization, quick-commerce grocery expansion, and food-contact oversight push converters toward faster, more flexible packaging formats. BOBST underscored the regional importance of this demand by showcasing digital and sustainable flexible packaging solutions alongside Chinese converters at Chinaplas 2026 in Shanghai.

North America and Europe formed the most mature technology base for the digital printing for flexible packaging market in 2026, even though the input did not provide separate regional shares for each market. In North America, ePac opened a new facility in Phoenix in March 2026 and added capacity in Atlanta, Philadelphia, and Vancouver, showing that digital flexible packaging is moving into broader network deployment rather than isolated local expansion. Europe is advancing under tighter compliance conditions because PPWR 2025/40 and the German Printing Ink Ordinance are both influencing ink and substrate qualification choices. The first HP Indigo 200K installation in EMEA at ePac's Sheffield site also showed that regional scaling is moving into a more commercial stage rather than staying in pilot mode.

South America, the Middle East and Africa, and other smaller markets remained at earlier adoption stages in 2025, and their progress depended more on packaging modernization and local brand development than on current installed digital depth. Brazil leads the South American opportunity because growing branded food and beverage demand favors better graphics, more SKU variety, and shorter launch cycles than long-run conventional systems handle well. The United Arab Emirates and Saudi Arabia are supporting more premium food and personal care packaging programs, which fit localized launches and shorter production runs. South Africa, Nigeria, and Egypt offer a longer runway, and their pace will depend on converter investment, substrate availability, and e-commerce infrastructure as the digital printing for flexible packaging market expands beyond its current core regions.

- HP Inc.

- Xeikon N.V.

- Canon Solutions America, Inc.

- EFI Electronics For Imaging, Inc.

- Durst Group AG

- Heidelberger Druckmaschinen AG

- Landa Digital Printing Ltd.

- Domino Printing Sciences plc

- Eastman Kodak Company

- CCL Industries Inc.

- Amcor plc

- Mondi plc

- Huhtamaki Oyj

- Sealed Air Corporation

- ePac Holdings, LLC

- Bobst Group SA

- Konica Minolta, Inc.

- SCREEN Graphic Solutions Co., Ltd.

- Fujifilm Holdings Corporation

- Agfa-Gevaert N.V.

- Flint Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Short-Run SKU Proliferation in Flexible Packs

- 4.2.2 E-Commerce-Driven Regionalized Packaging Demand

- 4.2.3 Brand Demand for Variable Data and Mass Customization

- 4.2.4 Hybrid Digital Presses Reducing Changeover Waste and Lead Times

- 4.2.5 Low-Migration and Food-Safe Ink Adoption in Regulated Packs

- 4.2.6 Direct-To-Converter Digital Printing for Micro-Fulfillment and Personalized Medicine

- 4.3 Market Restraints

- 4.3.1 High Capex and Payback Risk Versus Conventional Long-Run Printing

- 4.3.2 Specialty Ink and Film Substrate Price Volatility

- 4.3.3 Limited Food-Contact and Recyclability Qualification for Some Digital Ink Systems

- 4.3.4 Cybersecurity and Workflow Downtime Risks in Connected Print Lines

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Electrophotography

- 5.1.2 UV Inkjet

- 5.1.3 Water-based Inkjet

- 5.1.4 Hybrid Presses

- 5.1.5 Other Printing Technologies

- 5.2 By Packaging Type

- 5.2.1 Pouches

- 5.2.2 Stick Packs and Sachets

- 5.2.3 Wraps and Rollstock

- 5.2.4 Bags

- 5.2.5 Labels

- 5.2.6 Other Packaging Types

- 5.3 By Ink Type

- 5.3.1 UV-curable Inks

- 5.3.2 Water-based Inks

- 5.3.3 Solvent-based Inks

- 5.3.4 Electron-beam (EB) Inks

- 5.4 By Material Type

- 5.4.1 Plastic Films (PET, PE, PP)

- 5.4.2 Paper and Paper-based Laminates

- 5.4.3 Aluminum Foil

- 5.4.4 Compostable Films

- 5.4.5 Other Material Types

- 5.5 By End user Industry

- 5.5.1 Food

- 5.5.2 Beverages

- 5.5.3 Pharmaceuticals

- 5.5.4 Personal Care and Cosmetics

- 5.5.5 Household

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Thailand

- 5.6.4.7 Indonesia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Xeikon N.V.

- 6.4.3 Canon Solutions America, Inc.

- 6.4.4 EFI Electronics For Imaging, Inc.

- 6.4.5 Durst Group AG

- 6.4.6 Heidelberger Druckmaschinen AG

- 6.4.7 Landa Digital Printing Ltd.

- 6.4.8 Domino Printing Sciences plc

- 6.4.9 Eastman Kodak Company

- 6.4.10 CCL Industries Inc.

- 6.4.11 Amcor plc

- 6.4.12 Mondi plc

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Sealed Air Corporation

- 6.4.15 ePac Holdings, LLC

- 6.4.16 Bobst Group SA

- 6.4.17 Konica Minolta, Inc.

- 6.4.18 SCREEN Graphic Solutions Co., Ltd.

- 6.4.19 Fujifilm Holdings Corporation

- 6.4.20 Agfa-Gevaert N.V.

- 6.4.21 Flint Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment