|

시장보고서

상품코드

2083257

전자전 시스템 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Electronic Warfare Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

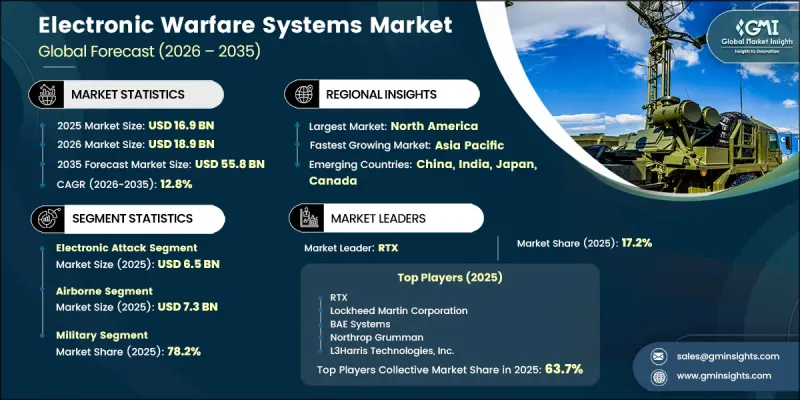

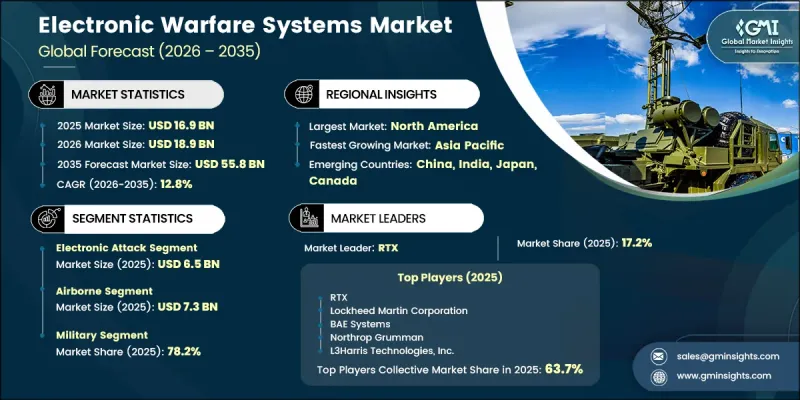

세계의 전자전 시스템 시장은 2025년에 169억 달러로 평가되었고, CAGR 12.8%로 성장하여 2035년까지 558억 달러에 달할 것으로 추정되고 있습니다.

전자전 시스템 시장은 현대 국방 전략에서 전자기 스펙트럼의 통제와 지배가 점점 더 중요시됨에 따라 강력한 성장세를 보이고 있습니다. 각국 정부와 국방 기관은 치열한 경쟁이 벌어지는 환경에서 작전 효과를 높이기 위해 전자 공격, 전자 방어 및 전자 지원 능력에 대한 투자를 대폭 늘리고 있습니다. 스펙트럼 우위 확보를 위한 노력이 점점 더 중요시되는 가운데, 동맹국들의 전체 방위 네트워크에서 차세대 전자전 기술 도입이 가속화되고 있습니다. 진행 중인 군사 현대화 프로그램과 전 세계가 다영역 작전으로 전환하고 있는 점도 시장 성장을 더욱 뒷받침하고 있습니다. 각 군은 상황 인식, 통신의 내결함성 및 임무의 효율성을 높이기 위해 육·공·해·우주·사이버 등 각 분야에 걸쳐 전자전 능력의 통합을 점점 더 추진하고 있습니다. 무인 시스템, 자율형 플랫폼, 전자 교란 기술 등 고도화된 위협에 노출되는 경우가 늘어나고 있는 점도 수요를 더욱 부추기고 있습니다. 또한, 인공지능(AI)과 머신러닝의 통합을 통해 복잡한 전자기 환경에서 위협을 자동으로 감지, 분류 및 대응할 수 있는 인지형 전자전 시스템이 구현되면서 시장 구조를 변화시키고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 169억 달러 |

| 예측 금액 | 558억 달러 |

| CAGR | 12.8% |

2025년, 전자 공격 부문 시장 규모는 65억 달러에 달했습니다. 이 부문의 성장은 교란 시스템, 전자 대항 조치, 대방사선 기술, 그리고 적의 방공 능력 억제를 위한 조치의 도입 확대에 힘입어 이루어지고 있습니다. 전자 공격 솔루션은 레이더 시스템, 통신 네트워크, 항법 신호 및 지휘통제 인프라를 교란하기 위해 널리 활용되고 있습니다. 공군, 해군, 육군 등 각 분야에서 원격 교란 기술 및 플랫폼 기반 전자전 시스템의 도입이 확대되고 있는 것이 이 부문의 성장을 더욱 뒷받침하고 있습니다.

2025년, 군사 부문은 78.2%의 점유율을 차지했습니다. 이러한 압도적인 시장 점유율은 국방 예산 증가, 지정학적 긴장의 고조, 그리고 현대 전투 시나리오에서 주파수 대역에 대한 지배력을 확보하려는 요구 증가에 힘입은 것입니다. 각국 군은 첨단 레이더 시스템, 드론, 미사일, 통신 네트워크 등에서 비롯되는 진화하는 위협에 대응하기 위해 전자 공격, 전자 방어 및 전자 지원 시스템에 대한 투자를 확대되고 있습니다. 전자전은 모든 작전 영역에서 정보 수집, 표적 지정, 상황 인식, 방공·미사일 방어 및 부대 방어에 있어 지극히 중요한 역할을 수행하고 있습니다.

북미 전자전 시스템 시장은 견조한 국방 지출과 대규모 현대화 계획에 힘입어 2025년에는 43.2%의 시장 점유율을 기록했습니다. 이 지역에서는 보다 광범위한 군사 능력 향상의 일환으로, 스펙트럼 지배 기술의 발전을 계속해서 우선시하고 있습니다. 전자 공격, 방어, 지원 시스템의 개선을 위한 지속적인 투자를 통해 작전 준비 태세가 한층 강화되었으며, 방위 플랫폼 전반에 걸친 기술적 우위가 확고해졌습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 플랫폼별, 2022년-2035년

제7장 시장 추산 및 예측 : 최종사용자별, 2022년-2035년

제8장 시장 추산 및 예측 : 지역별, 2022년-2035년

제9장 기업 개요

LSH 26.07.14The Global Electronic Warfare Systems Market was valued at USD 16.9 billion in 2025 and is estimated to grow at a CAGR of 12.8% to reach USD 55.8 billion by 2035.

The electronic warfare systems market is experiencing strong expansion as modern defense strategies increasingly prioritize control and dominance of the electromagnetic spectrum. Governments and defense organizations are significantly increasing investments in electronic attack, electronic protection, and electronic support capabilities to enhance operational effectiveness in highly contested environments. The growing emphasis on spectrum superiority initiatives is accelerating procurement of next-generation electronic warfare technologies across allied defense networks. Ongoing military modernization programs and the global transition toward multi-domain operations are further supporting market growth. Armed forces are increasingly integrating electronic warfare capabilities across land, air, naval, space, and cyber domains to improve situational awareness, communication resilience, and mission effectiveness. Rising exposure to advanced threats such as unmanned systems, autonomous platforms, and electronic disruption techniques is further strengthening demand. The integration of artificial intelligence and machine learning is also reshaping the market by enabling cognitive electronic warfare systems capable of automated threat detection, classification, and response in complex electromagnetic environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.9 Billion |

| Forecast Value | $55.8 Billion |

| CAGR | 12.8% |

The electronic attack segment accounted for USD 6.5 billion in 2025. This segment's growth is driven by the rising deployment of jamming systems, electronic countermeasures, anti-radiation technologies, and suppression of enemy air defense capabilities. Electronic attack solutions are widely used to disrupt radar systems, communication networks, navigation signals, and command and control infrastructure. Increasing adoption of stand-off jamming technologies and platform-based electronic warfare systems across airborne, naval, and ground applications continues to strengthen segment expansion.

The military segment held a 78.2% share in 2025. This dominance is supported by rising defense budgets, increased geopolitical tensions, and the growing need for spectrum dominance in modern combat scenarios. Defense forces are expanding investments in electronic attack, electronic protection, and electronic support systems to counter evolving threats from advanced radar systems, drones, missiles, and communication networks. Electronic warfare plays a critical role in intelligence gathering, targeting, situational awareness, air and missile defense, and force protection across all operational domains.

North America Electronic Warfare Systems Market accounted for 43.2% share in 2025, owing to strong defense spending and large-scale modernization initiatives. The region continues to prioritize advancements in spectrum dominance technologies as part of broader military capability upgrades. Continuous investment in improving electronic attack, protection, and support systems is further enhancing operational readiness and reinforcing technological superiority across defense platforms.

Major companies operating in the global electronic warfare systems market include Northrop Grumman, L3Harris Technologies, Lockheed Martin Corporation, BAE Systems, RTX, Thales, Leonardo S.p.A., SAAB, Elbit Systems Ltd., Hensoldt AG, Indra Sistemas, S.A., Rheinmetall AG, Kongsberg Defence & Aerospace, ASELSAN A.S., Bharat Electronics Limited, China Electronics Technology Group Corporation, EDGE Group PJSC, Hanwha Systems Co., Ltd., IAI (Israel Aerospace Industries), and Mitsubishi Electric Corporation. Companies operating in the electronic warfare systems market are strengthening their competitive position through continuous investment in advanced signal processing technologies, artificial intelligence integration, and next-generation spectrum management solutions. Market participants are focusing on enhancing system interoperability across multi-domain defense platforms, enabling seamless coordination between air, land, naval, space, and cyber operations. Strategic partnerships with defense agencies and government organizations are supporting the development of advanced electronic warfare capabilities tailored to evolving threat environments. Companies are also investing in modular and scalable system architectures to improve deployment flexibility across multiple platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Platform trends

- 2.2.3 End-user trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising defense investments in electromagnetic spectrum dominance

- 3.2.1.2 Military modernization and multi-domain warfare programs

- 3.2.1.3 Growing demand for counter-drone and anti-UAS capabilities

- 3.2.1.4 Increasing NATO and allied interoperability initiatives

- 3.2.1.5 Adoption of AI-enabled and next-generation EW technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and procurement costs

- 3.2.2.2 Rapidly evolving threat environment

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of AI-enabled cognitive electronic warfare systems

- 3.2.3.2 Growing deployment of counter-drone and autonomous defense solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Electronic Attack

- 5.2.1 Radar jammers

- 5.2.2 Communication jammers

- 5.2.3 GNSS jammers

- 5.2.4 Directed energy weapons

- 5.2.5 Anti-radiation missiles

- 5.2.6 Decoy systems

- 5.2.7 Others

- 5.3 Electronic Protection

- 5.3.1 Self-protection suites

- 5.3.2 Infrared countermeasure systems (DIRCM)

- 5.3.3 Radar absorbing materials & stealth coatings

- 5.3.4 Frequency hopping & spread spectrum modules

- 5.3.5 Others

- 5.4 Electronic Support

- 5.4.1 Radar warning receivers (RWR)

- 5.4.2 Missile approach warning systems (MAWS)

- 5.4.3 Electronic intelligence (ELINT) receivers

- 5.4.4 Communication intelligence (COMINT) receivers

- 5.4.5 Direction finding systems & signal analysers

- 5.4.6 Electronic surveillance

- 5.4.7 Others

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Airborne

- 6.3 Naval

- 6.4 Ground

- 6.5 Space

Chapter 7 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Military

- 7.3 Homeland Security

- 7.4 Commercial

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 RTX

- 9.1.2 BAE Systems

- 9.1.3 Northrop Grumman

- 9.1.4 L3Harris Technologies, Inc.

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Lockheed Martin Corporation

- 9.2.2 Asia Pacific

- 9.2.2.1 China Electronics Technology Group Corporation

- 9.2.2.2 Bharat Electronics Limited

- 9.2.2.3 Hanwha Systems Co., Ltd.

- 9.2.2.4 Mitsubishi Electric Corporation

- 9.2.3 Europe

- 9.2.3.1 Thales

- 9.2.3.2 Leonardo S.p.A.

- 9.2.3.3 Rheinmetall AG

- 9.2.3.4 Kongsberg Defence & Aerospace

- 9.2.3.5 SAAB

- 9.2.3.6 Indra Sistemas, S.A.

- 9.2.3.7 Hensoldt AG

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 EDGE Group PJSC

- 9.3.2 Elbit Systems Ltd.

- 9.3.3 IAI

- 9.3.4 ASELSAN A.S.