|

시장보고서

상품코드

2073483

전자전 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Electronic Warfare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

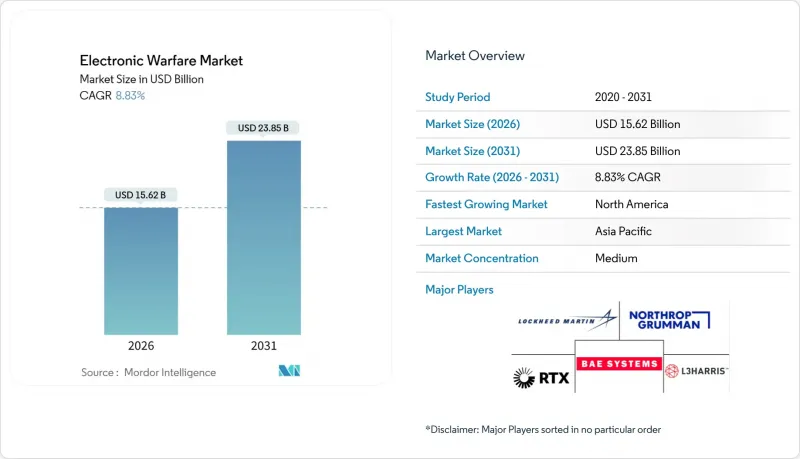

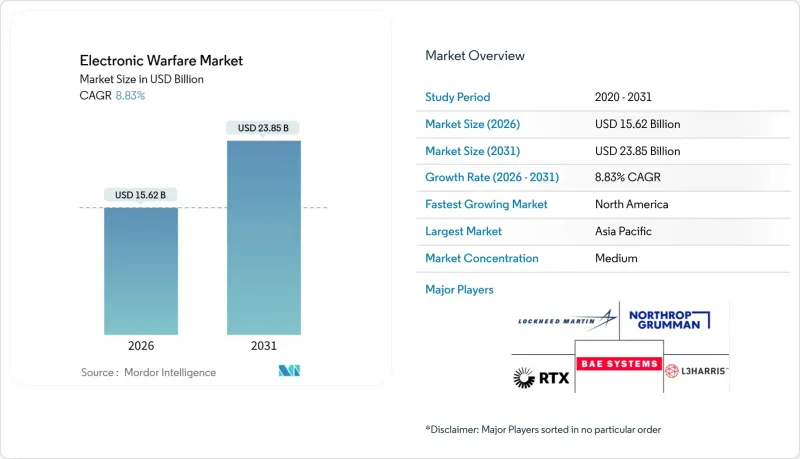

Mordor Intelligence에 의하면, 전자전 시장 규모는 2026년에 156억 2,000만 달러에 달하고, 2031년까지 238억 5,000만 달러에 이를 것으로 예측되며, CAGR은 8.83%를 나타낼 것으로 전망됩니다.

본 보고서는 기능별(전자 공격, 전자 방어, 전자 지원), 플랫폼별(항공, 해상, 지상, 우주), 장비별(재머 시스템, 레이더 경보 수신기, 기타), 최종 사용자별(공군, 해군, 육군), 도입 형태별(OEM 및 개조 설치/업그레이드), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 전자전 시장 동향 및 인사이트

고조되는 지정학적 긴장과 국방력의 현대화

우크라이나 전장에서 러시아가 자행한 전파 교란으로 인해, 나토(NATO) 회원국 군은 대체 교란기나 특정 주파수 대역에 내성이 있는 무전기를 서둘러 주문해야만 했으며, 이에 따라 조달 주기가 지속적인 능력 도입으로 재조정되었습니다. 2024년에 수여된 미 육군의 1억 달러 규모의 “Terrestrial Layer System"계약은 전자 지원, 공격, 사이버 작전 기능을 단일 섀시에 통합한 휴대용 키트에 대한 수요를 상징하는 것입니다. 2025년 일본의 방위 전략에서는 중국 국방부가 전개하는 고주파 호핑식 레이더 시스템에 대응하기 위한 F-35A의 전자전 대응 능력 업그레이드에 사상 최대 규모의 예산을 우선 배정했습니다. 만안 국가들은 주요 항로 주변의 혼잡한 전자기 환경을 감시하기 위해 공중 조기경보기 함대를 확대되고 있습니다. 이러한 움직임에 따라 스펙트럼 지배력은 항공·해상 우위와 동등한 중요성을 띠게 되었으며, 전자전 시장의 장기적인 성장을 뒷받침할 투자 기반이 확고해졌습니다.

전자전 페이로드를 필요로 하는 무인 플랫폼의 급증

임시로 제작된 무기를 장착한 상용 쿼드콥터가 수십억 달러 규모의 주력함을 위협하게 되자, 해군은 대 UAS(무인항공기 시스템) 장비를 임무용 키트가 아닌 표준 장비로 함정에 탑재할 수밖에 없게 되었습니다. 록히드 마틴의 “산크텀"와 엘비트의 “리드론"는 RF 감지, 프로토콜 분석, 표적 집중 재밍 기능을 지휘관이 몇 분 만에 전개할 수 있는 휴대용 패키지에 통합하고 있습니다. 공격용 드론 무리에도 기만 신호를 송신하는 소형 GaN 증폭기가 탑재되어 있어, 적은 비용으로 적의 방어 시스템을 포화 상태로 몰아넣고 있습니다. 무인 시스템의 양방향적 보급에 힘입어, 국방 예산 전체가 정체된 상황에서도 두 자릿수의 수주 대수가 유지되고 있으며, 전자전 시장 내 대UAS 부문의 성장세가 지속되고 있습니다.

높은 프로그램 비용과 긴 개발 주기

미국 해군의 “차세대 재머(Next Generation Jammer)"가 초기 운용 능력에 도달하기까지 11년이 걸린 것은 탑재 센서에 지장을 주지 않으면서 고출력 송신기를 통합하기 위해 대규모 비행 검사가 필요했기 때문입니다. 2025년 이탈리아가 3억 달러에 EA-37B 항공기 2대를 발주한 사실은 동적 무기를 탑재하지 않는 전용 전파 교란 플랫폼이 자본 집약적이라는 점을 여실히 보여주고 있습니다. 이러한 고가의 가격은 각국의 국방부가 단계적인 업그레이드를 추진하도록 이끌며, 항공기를 처음부터 설계하는 주계약업체보다 모듈식 개조를 담당하는 공급업체를 우선시하는 경향을 보입니다. 또한, 도급업체는 계약이 확정되기 전에 기밀로 분류된 위협 파형을 평가하기 위한 안전한 시험장을 마련하기 위해 자금을 조달해야 하며, 이로 인해 전자전 시장 전체에서 대차대조표상의 위험이 증가하고 이익률이 하락하고 있습니다.

부문별 분석

2025년에도 모든 플랫폼에는 여전히 자체 방어용 수신기 및 디스펜서가 필요하기 때문에 전자 방어 부문은 전자전 시장에서 35.37%의 점유율을 유지했습니다. 그러나, 적의 방공망을 뚫기 위한 일회용 드론에 고출력 송신기를 탑재하는 ‘스탠드 간섭"라는 개념에 힘입어, 전자공격 부문의 전자전 시장은 2031년까지 연평균 성장률(CAGR) 9.16%로 가장 빠르게 확대될 것으로 전망됩니다. L3Harris가 5억 8,700만 달러에 수주한 ‘차세대 저대역 전파 교란기(Next Generation Jammer Low-Band)" 프로젝트는 공격 및 지원 기능을 융합한 광대역 포드에 대한 수요를 부각시키고 있으며, 내부 능력 구분이 점차 모호해지고 있습니다.

2세대 방어 시스템은 현재 적외선 센서와 RF 센서를 융합하고 있지만, 성능의 점진적인 향상 폭은 줄어들고 있어 이 성숙한 부문의 수익 성장 속도는 둔화되고 있습니다. 소형화된 SDR(소프트웨어 정의 무선) 덕분에 그룹 2 드론에 위치 파악용 페이로드를 탑재할 수 있게 되었고, 전술 지휘관을 위한 저비용 대안이 등장함에 따라 전자 지원에 대한 수요가 증가하고 있습니다. 인지 알고리즘의 통합을 통해 단일 개구부가 위협 감지에서 교란 모드로 밀리초 단위로 자동 전환될 수 있게 되어, SWaP(크기·무게·전력 소비)를 줄이는 동시에 전자전 시장에서 부문 간 채택을 가속화하는 매력적인 가치 제안을 제공합니다.

항공 시스템은 2025년 매출의 35.21%를 차지하며, F-35, EA-18G 및 구형 전투기의 지속적인 업그레이드 주기를 반영했습니다. 한편, 위성 군집이 고가치 표적이자 지속적인 방해 노드 역할을 동시에 수행하고 있기 때문에 우주 플랫폼용 전자전 시장은 연평균 성장률(CAGR) 9.37%로 성장할 것으로 전망됩니다. 미국 우주군은 궤도 상의 우주 쓰레기에 관한 규약을 위반하지 않으면서 적의 통신을 차단할 수 있는 페이로드에 대한 연구에 자금을 지원하고 있으며, 향후 10년 동안 새로운 계약이 잇따를 것으로 전망됩니다.

해양 플랫폼은 안정적인 조선 예산의 혜택을 받고 있습니다. 노스롭 그루먼사의 SEWIP 블록 3는 미 해군의 수상 전투함에 탑재된 아날로그 방식의 SLQ-32를 AESA 어레이로 대체하는 것으로, USS 핑키호 등 아레이 버크급 구축함에 탑재가 시작되었습니다. 육상 부대에서는 드론 떼나 GPS 방해에 대응하기 위해 이동식 전파 교란기의 현대화를 추진하고 있습니다. 플랫폼의 다양화는 위험을 분산시키고, 공급업체가 자원을 재분배할 수 있게 하며, 전자전 시장의 안정적이고 장기적인 성장을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 매출의 40.46%를 차지했으며, 연평균 성장률(CAGR) 9.42%를 나타낼 것으로 예측되는데, 이는 모든 지역 중 가장 높은 성장률입니다. 미국 국방부의 2025 회계연도 예산 8,420억 달러 중, 실시간 주파수 대역 관리 도구가 필요한 ‘통합 전영역 지휘통제(JADC2)" 이니셔티브에 막대한 자금이 배정되었습니다. 캐나다의 F-35 도입 계획에는 전투기 현대화에 첨단 전자전 능력이 포함되어 있는 반면, 멕시코는 마약 단속 작전을 위해 항공기 탑재형 신호정보(SIGINT) 시스템에 투자하고 있습니다.

유럽에서는 각국이 개별적으로 추진해 오던 노력에서 공동 역량 개발로 초점을 옮겨가고 있습니다. 영국과 독일이 자금을 지원하는 유로파이터의 전자전형은 2030년까지 사브의 ‘알렉시스(Arexis)"스위트와 노스롭 그루먼의 AARGM 미사일을 통합함으로써, NATO에 전용 SEAD(적 방공망 제압) 전력을 추가하게 됩니다. 이탈리아, 일본, 영국이 주도하는 “세계 전투 항공 프로그램(GCAP)"에서는 통합 센싱 및 비살상 효과 부문에서 레오나르도사와 ELT 그룹을 공동 주계약자로 지정하고, 프로그램 시작 초기부터 인지형 전자전을 포함시켰습니다. 프랑스의 라팔 F5 표준형은 전파 교란 능력을 강화하기 위해 탈레스사의 “SPECTRA"스위트를 업그레이드하여, 적의 방공망이 촘촘히 펼쳐진 환경에서도 해당 플랫폼의 경쟁력을 유지하고 있습니다.

중국이 첨단 방공 시스템을 배치함에 따라 아시아태평양 수요가 가속화되고 있습니다. 인도의 DRDO는 테자스 전투기 및 구축함용 항공기 탑재형 및 함재형 시스템을 완성해 나가는 동시에, 이스라엘산 하드웨어와의 격차를 좁혀가고 있습니다. 일본의 2025년도 예산은 사상 최대 규모를 기록했으며, F-35의 전자전 능력 향상과 위성 교란을 완화하기 위한 대우주 시스템에 자금이 배정되었습니다. 한국의 KF-21 전투기와 세종급 구축함 프로그램에는 수입 의존도를 낮추기 위한 국산 전자전 시스템이 탑재되어 있습니다. 호주는 AUKUS 협정을 활용하여 BAE Systems와의 협력을 통해 잠수함용 전자전 및 신호정보 수집 능력 개발을 추진하고 있습니다. 중동 고객들의 관심사는 각기 다릅니다. 이스라엘은 공격적인 전파 방해에 중점을 두고 있는 반면, 걸프 연안 국가들은 전자 지원 및 드론 방어에 투자하고 있습니다. 남미와 아프리카는 여전히 도입 초기 단계에 있으며, 브라질과 남아프리카공화국은 제한적인 틈새 시장 구매에 그치고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the electronic warfare market size reached USD 15.62 billion in 2026 and is forecasted to reach USD 23.85 billion by 2031, advancing at an 8.83% CAGR.

This report is Segmented by Capability (Electronic Attack, Electronic Protection, and Electronic Support), Platform (Air, Sea, Land, and Space), Equipment (Jammer Systems, Radar Warning Receivers, and More), End-User (Air Force, Navy, and Army), Fit (OEM and Retrofit/Upgrades), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Electronic Warfare Market Trends and Insights

Escalating Geopolitical Tensions and Defense Modernization

Russia's battlefield jamming in Ukraine compelled NATO armies to rush orders for stand-in jammers and spectrum-resilient radios, resetting procurement cycles toward continuous capability insertion. The US Army's USD 100 million Terrestrial Layer System contract, awarded in 2024, typifies demand for man-portable kits that integrate electronic support, attack, and cyber effects on a single chassis. Japan's defense strategy in 2025 prioritizes record budget allocations toward F-35A electronic countermeasure upgrades aimed at addressing advanced frequency-hopping radar systems deployed by the Chinese Ministry of Defense. The Gulf states are expanding airborne early warning fleets to surveil congested EM environments along critical shipping lanes. These moves elevate spectrum dominance to parity with air and maritime superiority, cementing an investment baseline that supports long-run growth of the electronic warfare market.

Surge in Unmanned Platforms Requiring EW Payloads

Commercial quadcopters armed with improvised munitions now threaten multi-billion-dollar capital ships, forcing navies to install shipboard counter-UAS suites as standard fit rather than mission kits. Lockheed Martin's Sanctum and Elbit's ReDrone integrate RF detection, protocol analysis, and targeted jamming in man-portable packages that commanders can deploy in minutes. Offensive drone swarms are also being equipped with miniature GaN amplifiers that broadcast deceptive signals, saturating enemy defenses at a fraction of the cost. The bidirectional proliferation of unmanned systems is driving double-digit unit orders even as broader defense budgets flatten, sustaining momentum for counter-UAS segments of the electronic warfare market.

High Program Cost and Long Development Cycles

The US Navy's Next Generation Jammer took 11 years to reach initial operational capability because integrating high-power transmitters without disrupting on-board sensors required extensive flight testing. Italy's USD 300 million order for two EA-37B aircraft in 2025 underscores the capital-intensive nature of purpose-built jamming platforms that carry no kinetic weapons. These headline prices push ministries toward incremental upgrades that favor modular retrofit vendors over prime contractors dependent on clean-sheet aircraft. Contractors must also finance secure test ranges to evaluate classified threat waveforms before contracts are guaranteed, elevating balance-sheet risk and diluting margins across the electronic warfare market.

Other drivers and restraints analyzed in the detailed report include:

- Evolution of Radar and Communication Threats

- COTS GaN Enabling Low-SWaP EW on Small Drones

- Spectrum Management and Regulatory Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronic protection retained a 35.37% share in the electronic warfare market during 2025, as every platform still requires self-defense receivers and dispensers. However, the electronic warfare market for electronic attack is projected to expand fastest at a 9.16% CAGR through 2031, driven by stand-in jamming concepts that embed high-power transmitters on expendable drones that penetrate enemy air defenses. L3Harris's USD 587 million Next Generation Jammer Low-Band award underscores demand for wideband pods that merge attack with support, blurring internal capability lines.

Second-generation protection suites now fuse infrared and RF sensors, but incremental performance gains are shrinking, slowing revenue velocity for this mature segment. Electronic support is climbing as miniaturized SDRs enable geolocation payloads on Group 2 drones, creating low-cost options for tactical commanders. Integration of cognitive algorithms enables a single aperture to auto-switch from threat detection to jamming within milliseconds, reducing SWaP and providing a compelling value proposition that accelerates cross-segment adoption in the electronic warfare market.

Air systems delivered 35.21% of 2025 revenue, reflecting sustained upgrade cycles for F-35, EA-18G, and legacy fighters. Yet the electronic warfare market for space platforms is forecasted to grow at a 9.37% CAGR, as satellite constellations have become both high-value targets and persistent jamming nodes. The US Space Force is financing studies on payloads that can deny adversary communications without violating orbital debris protocols, adding a fresh stream of contracts through the decade.

Sea platforms benefit from steady shipbuilding budgets: Northrop Grumman's SEWIP Block 3 replaces analog SLQ-32s with AESA arrays on US surface combatants, with installations starting on Arleigh Burke-class destroyers like the USS Pinckney. Land fleets are refreshing mobile jammers as armies confront drone swarms and GPS denial. Platform diversification spreads risk and enables suppliers to reallocate resources, reinforcing stable, long-term growth in the electronic warfare market.

Complete Report Scope:

- By Capability

- Electronic Attack

- Electronic Protection

- Electronic Support

- By Platform

- Air

- Sea

- Land

- Space

- By Equipment

- Jammer Systems

- Radar Warning Receivers

- Directed Energy Weapons

- Counter-UAS EW Suites

- Other Equipments

- By End-User

- Air Force

- Navy

- Army

- By Fit

- OEM

- Retrofit/Upgrades

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 40.46% of 2025 revenue and is expected to grow at a 9.42% CAGR, the fastest among all regions. The US DoD's USD 842 billion FY 2025 budget allocates significant funding to Joint All-Domain Command and Control (JADC2) initiatives that require real-time spectrum management tools. Canada's F-35 procurement embeds advanced EW into its fighter recapitalization, while Mexico invests in airborne SIGINT for counter-narcotics operations.

Europe is pivoting from fragmented national efforts to pooled capability development. The Eurofighter Electronic Attack variant, financed by the UK and Germany, will integrate Saab's Arexis suite and Northrop Grumman's AARGM missiles by 2030, adding a dedicated SEAD asset to NATO. Italy, Japan, and the UK's Global Combat Air Programme (GCAP) has named Leonardo and ELT Group as co-primes for integrated sensing and non-kinetic effects, embedding cognitive EW from program inception. France's Rafale F5 standard upgrades Thales's SPECTRA suite for enhanced jamming, keeping the platform competitive in denied environments.

Asia-Pacific demand is accelerating as China fields advanced air-defense complexes. India's DRDO is maturing airborne and shipborne suites for Tejas and destroyers while bridging gaps with Israeli hardware. Japan's FY 2025 record budget funds F-35 EW upgrades and counter-space systems to mitigate satellite jamming. South Korea's KF-21 fighter and Sejong-class destroyer programs include indigenous EW to reduce reliance on imports. Australia leverages the AUKUS pact to develop submarine EW and signals intelligence with BAE Systems integration. Middle Eastern customers split focus: Israel emphasizes offensive jamming, whereas Gulf states invest in electronic support and counter-drone defenses. South America and Africa remain early-stage adopters, with Brazil and South Africa making limited niche purchases.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- L3Harris Technologies, Inc.

- BAE Systems plc

- Saab AB

- Thales Group

- Leonardo S.p.A.

- Israel Aerospace Industries Ltd.

- Elbit Systems Ltd.

- HENSOLDT AG

- ASELSAN A.S.

- General Dynamics Corporation

- Rohde & Schwarz GmbH & Co. KG

- Mercury Systems, Inc.

- Bharat Electronics Limited

- Indra Sistemas S.A.

- CACI International Inc.

- Textron Systems Corporation (Textron Inc.)

- Tata Advanced Systems Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating geopolitical tensions and defence modernization

- 4.2.2 Surge in unmanned platforms requiring EW payloads

- 4.2.3 Evolution of radar/comm threats necessitating advanced EW

- 4.2.4 COTS GaN enabling low-SWaP EW on small drones

- 4.2.5 AI/ML-driven cognitive EW for adaptive jamming

- 4.2.6 Orbital opportunities from satellite mega-constellations

- 4.3 Market Restraints

- 4.3.1 High program cost and long development cycles

- 4.3.2 Spectrum management and regulatory hurdles

- 4.3.3 Cyber-enabled spoofing vulnerability of EW suites

- 4.3.4 Tightening export controls on advanced semiconductors

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Capability

- 5.1.1 Electronic Attack

- 5.1.2 Electronic Protection

- 5.1.3 Electronic Support

- 5.2 By Platform

- 5.2.1 Air

- 5.2.2 Sea

- 5.2.3 Land

- 5.2.4 Space

- 5.3 By Equipment

- 5.3.1 Jammer Systems

- 5.3.2 Radar Warning Receivers

- 5.3.3 Directed Energy Weapons

- 5.3.4 Counter-UAS EW Suites

- 5.3.5 Other Equipments

- 5.4 By End-User

- 5.4.1 Air Force

- 5.4.2 Navy

- 5.4.3 Army

- 5.5 By Fit

- 5.5.1 OEM

- 5.5.2 Retrofit/Upgrades

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lockheed Martin Corporation

- 6.4.2 Northrop Grumman Corporation

- 6.4.3 RTX Corporation

- 6.4.4 L3Harris Technologies, Inc.

- 6.4.5 BAE Systems plc

- 6.4.6 Saab AB

- 6.4.7 Thales Group

- 6.4.8 Leonardo S.p.A.

- 6.4.9 Israel Aerospace Industries Ltd.

- 6.4.10 Elbit Systems Ltd.

- 6.4.11 HENSOLDT AG

- 6.4.12 ASELSAN A.S.

- 6.4.13 General Dynamics Corporation

- 6.4.14 Rohde & Schwarz GmbH & Co. KG

- 6.4.15 Mercury Systems, Inc.

- 6.4.16 Bharat Electronics Limited

- 6.4.17 Indra Sistemas S.A.

- 6.4.18 CACI International Inc.

- 6.4.19 Textron Systems Corporation (Textron Inc.)

- 6.4.20 Tata Advanced Systems Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment