|

시장보고서

상품코드

2083326

원료의약품(API) CDMO 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Active Pharmaceutical Ingredient CDMO Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

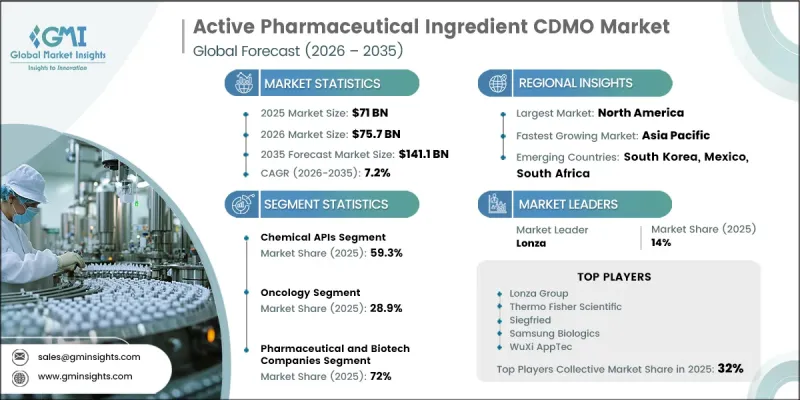

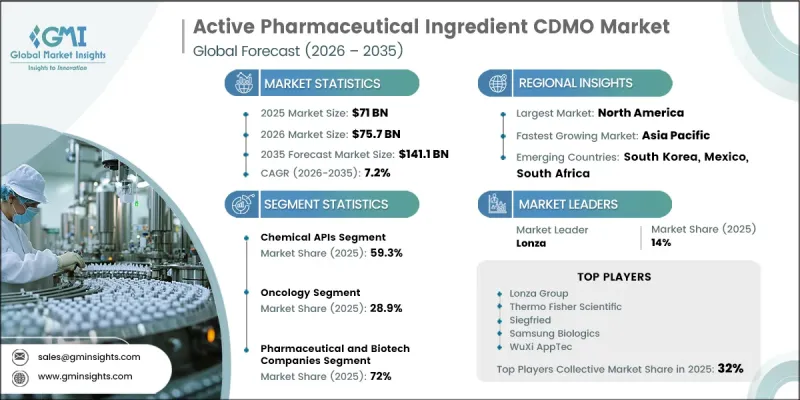

세계의 원료의약품(API) CDMO 시장은 2025년에 710억 달러로 평가되었고, CAGR 7.2%로 성장하여 2035년까지 1,411억 달러에 달할 것으로 추정되고 있습니다.

이러한 확대는 제약 밸류체인의 구조적 재편에 의해 주도되고 있습니다. 연구개발비 증가, 의약품 파이프라인의 복잡화, 자본 효율 최적화를 위한 지속적인 압박으로 인해 혁신 기업들은 수탁 개발·제조 기관(CDMO)에 대한 의존도를 높이고 있습니다. 동시에, 만성 질환 및 감염병으로 인한 전 세계적 부담이 커짐에 따라, 광범위한 치료 분야에서 원료의약품에 대한 수요가 지속적으로 증가하고 있습니다. 의약품 모달리티, 특히 생물학적 제제, 펩타이드, 올리고뉴클레오티드, 항체-약물 복합체(ADC)의 급속한 발전으로 인해, 고도의 합성 능력과 고도로 전문화된 제조 노하우에 대한 수요가 높아지고 있습니다. 현재 규제 당국의 승인 건수에서 상당한 비중을 차지하는 중소 바이오기술 기업들은 대개 사내 생산 인프라가 부족하기 때문에 외부와의 제조 제휴가 필수적입니다. 업계 전반에 걸쳐 규제 당국의 요구 사항이 더욱 엄격해지고 파이프라인의 복잡성이 계속 증가하는 가운데, 제약사들은 유연한 외부 위탁 생산 네트워크로의 전환을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 710억 달러 |

| 예측액 | 1,411억 달러 |

| CAGR | 7.2% |

2025년, 화학 계열 API 부문은 59.3%의 점유율을 차지했습니다. 이러한 우위는 심혈관 질환, 대사성 질환, 감염증, 만성 질환 치료제 등 처방되는 치료법의 대부분을 여전히 뒷받침하고 있는 저분자 치료제에 대한 전 세계적인 의존도가 지속되고 있다는 점에 기인합니다.

2025년, 제약 및 바이오기술 부문은 72%의 점유율을 차지하며, API CDMO 시장의 주요 최종 사용자 그룹으로서의 입지를 확고히 했습니다. 여기에는 사내 역량을 유지하면서 생산을 선택적으로 외부에 위탁하는 대형 다국적 제약 기업은 물론, 임상 및 상업적 생산 요건을 충족하기 위해 거의 전적으로 외부 제조 파트너에 의존하고 있는 신생 생명공학 기업도 포함됩니다.

북미의 원료의약품(API) CDMO 시장은 활발한 의약품 승인 환경과 제조 활동의 광범위한 외주화에 힘입어 2025년에는 41.2%의 시장 점유율을 차지했습니다. 승인된 의약품의 압도적 다수가 외부에서 제조된 원료의약품(API)에 의존하고 있으며, 이는 제약 생태계가 수탁 제조에 크게 의존하고 있음을 반영합니다. 확립된 GMP 및 품질 준수 기준에 기반한 규제 체계는 경험이 풍부하고 검사 대응 체계가 잘 갖춰진 CDMO 제공업체에 유리한, 고도로 구조화된 사업 환경을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022년-2035년

제6장 시장 추산 및 예측 : 적응증별, 2022년-2035년

제7장 시장 추산 및 예측 : 약물별, 2022년-2035년

제8장 시장 추산 및 예측 : 워크플로우별, 2022년-2035년

제9장 시장 추산 및 예측 : 용도별, 2022년-2035년

제10장 시장 추산 및 예측 : 최종 용도별, 2022년-2035년

제11장 시장 추산 및 예측 : 지역별, 2022년-2035년

제12장 기업 개요

LSHThe Global Active Pharmaceutical Ingredient CDMO Market was valued at USD 71 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 141.1 billion by 2035.

The expansion is shaped by a structural reconfiguration of the pharmaceutical value chain, where rising R&D expenditure, increasingly complex drug pipelines, and sustained pressure to optimize capital efficiency are pushing innovators to rely more heavily on contract development and manufacturing organizations. At the same time, the increasing global burden of chronic and infectious diseases continues to expand demand for active pharmaceutical ingredients across a wide range of therapies. The rapid evolution of drug modalities, particularly biologics, peptides, oligonucleotides, and antibody-drug conjugates, has intensified the need for advanced synthesis capabilities and highly specialized manufacturing expertise. Smaller biotechnology firms, which now represent a significant portion of regulatory approvals, typically lack in-house production infrastructure, making external manufacturing partnerships essential. Across the industry, pharmaceutical companies are increasingly shifting toward flexible, outsourced manufacturing networks as regulatory expectations tighten and pipeline complexity continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $71 Billion |

| Forecast Value | $141.1 Billion |

| CAGR | 7.2% |

The chemical-based APIs segment held a 59.3% share in 2025. This dominance is supported by the continued global reliance on small-molecule therapeutics, which remain the foundation of most prescribed treatments, including cardiovascular, metabolic, infectious, and chronic disease medications.

The pharmaceutical and biotechnology segment held a 72% share in 2025, positioning them as the primary end-user group in the API CDMO landscape. This includes large multinational pharmaceutical organizations that selectively outsource production while maintaining internal capabilities, as well as emerging biotech firms that depend almost entirely on external manufacturing partners to support clinical and commercial production requirements.

North America Active Pharmaceutical Ingredient CDMO Market held a 41.2% share in 2025, supported by a highly active drug approval environment and widespread outsourcing of manufacturing activities. A significant majority of approved medicines rely on externally manufactured APIs, reflecting the strong dependence of the pharmaceutical ecosystem on contract manufacturing. Regulatory frameworks under established GMP and quality compliance standards reinforce a highly structured operating environment that favors experienced and inspection-ready CDMO providers.

Major players operating in the global active pharmaceutical ingredient CDMO industry include WuXi AppTec, Thermo Fisher Scientific, Lonza AG, Dr. Reddy's Laboratories, Catalent, Inc., Piramal Pharma Solutions, Recipharm AB, Cambrex Corporation, Siegfried Holding AG, Teva API (TAPI), Boehringer Ingelheim, Aurobindo Pharma, Divi's Laboratories, Ajinomoto Biopharma Services, and CordenPharma International. The Active Pharmaceutical Ingredient CDMO Market is being shaped by several strategic priorities adopted by leading companies to strengthen competitive positioning. Firms are heavily investing in expanding high-potency API and complex molecule manufacturing capacity to align with evolving drug pipelines. Many players are strengthening geographic footprints through facility expansions and acquisitions across North America, Europe, and Asia to ensure supply chain resilience and proximity to key clients. Long-term supply agreements with pharmaceutical innovators are increasingly used to secure predictable revenue streams and deepen client relationships. Companies are also prioritizing digital manufacturing technologies, process automation, and continuous manufacturing systems to improve efficiency and regulatory compliance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Indication trends

- 2.1.4 Drug trends

- 2.1.5 Workflow trends

- 2.1.6 Application trends

- 2.1.7 End use trends

- 2.1.8 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic disease

- 3.2.1.2 Rising R&D activities in the pharmaceutical industry

- 3.2.1.3 Rising demand for generic drugs

- 3.2.1.4 Rising adoption of outsourcing services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory compliance

- 3.2.2.2 Pricing pressure and margin constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of high-potency and complex API manufacturing

- 3.2.3.2 Long-term strategic outsourcing partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing trend analysis (Driven by primary research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Investment & funding analysis (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Chemical APIs

- 5.3 Biological APIs

- 5.4 High Potent APIs

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Cardiovascular diseases

- 6.4 Diabetes

- 6.5 Hormonal disorders

- 6.6 Infectious diseases

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By Drug, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Branded

- 7.3 Generic

Chapter 8 Market Estimates and Forecast, By Workflow, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Clinical

- 8.3 Commercial

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Human application

- 9.3 Veterinary application

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Pharmaceutical and biotechnology companies

- 10.3 Academic and research institutes

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 France

- 11.3.3 UK

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Lonza Group

- 12.2 Thermo Fisher Scientific

- 12.3 Catalent

- 12.4 Recipharm

- 12.5 Cambrex

- 12.6 CordenPharma International

- 12.7 Siegfried

- 12.8 Boehringer Ingelheim

- 12.9 Ajinomoto Biopharma Services

- 12.10 Teva API (TAPI)

- 12.11 Piramal Pharma Solutions

- 12.12 WuXi AppTec

- 12.13 Divi’s Laboratories

- 12.14 Aurobindo Pharma

- 12.15 Dr. Reddy’s Laboratories