|

시장보고서

상품코드

2083337

수의 진단 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Veterinary Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

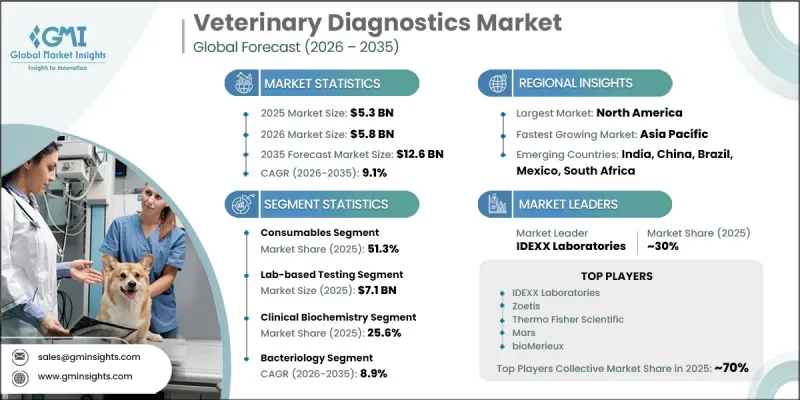

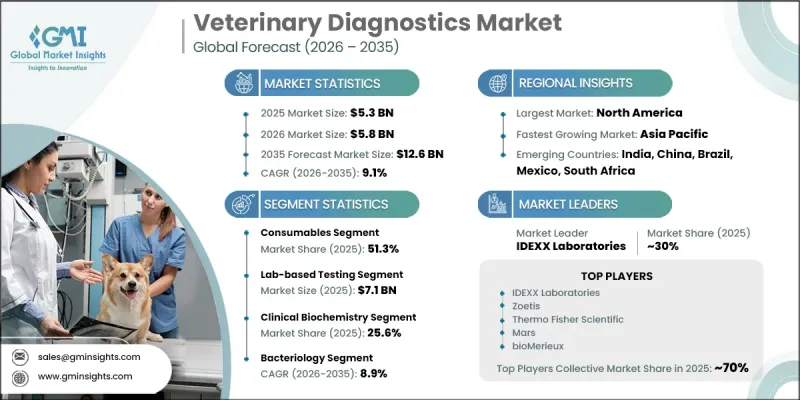

세계의 수의 진단 시장은 2025년에 53억 달러로 평가되었고, CAGR 9.1%로 성장하여 2035년까지 126억 달러에 달할 것으로 추정되고 있습니다.

시장의 확대는 반려동물과 가축 모두에서 감염병, 인수공통감염병, 만성 질환의 발생률이 높아지고 있는 데다, 예방 수의학에 대한 인식이 높아짐에 따라 주도되고 있습니다. 질병 발생 빈도가 증가하고 있는 것은 정확하고 신속한 진단 솔루션의 필요성을 계속해서 강조하고 있습니다. 최근 몇 년간 이 시장은 반려동물의 의료비 증가와 진단 기술의 지속적인 발전에 힘입어 꾸준한 성장세를 보이고 있습니다. 신종 및 국경을 초월하는 동물 질병으로 인한 부담이 커짐에 따라, 신뢰성이 높은 검사 솔루션에 대한 수요가 더욱 가속화되고 있습니다. 전 세계 반려동물 및 생산용 가축의 사육 두수 증가도 시장 전체 수요를 뒷받침하고 있습니다. 반려동물 사육 마릿수는 특히 개와 고양이의 경우 꾸준히 증가하고 있으며, 반려인들은 정기적인 건강검진과 예방 의료에 대한 투자에 더욱 적극적인 태도를 보이고 있습니다. 동시에, 분자진단, PCR법, 차세대 염기서열 분석, 바이오마커 검사 및 휴대용 현장 진단 시스템 분야의 기술 발전으로 인해 질병 검출 속도, 정확도 및 접근성이 향상되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 53억 달러 |

| 예측액 | 126억 달러 |

| CAGR | 9.1% |

소모품 부문은 2025년에 51.3%의 시장 점유율을 차지했으며, 2026-2035년 연평균 성장률(CAGR) 9.2%로 성장을 이어갈 전망입니다. 이러한 우위는 진단 워크플로우 전반에 걸쳐 필수적인 역할을 수행한다는 점과 지속적인 수익 구조에 의해 뒷받침되고 있습니다. 소모품에는 시약, 진단 키트, 분석 카트리지, 채혈 튜브, 슬라이드, 교정 도구 및 대조용 시료가 포함되며, 이들은 동물병원, 진료소, 진단실험실, 연구소 등에서 널리 사용되고 있습니다.

검사실 기반 검사 부문은 2035년까지 71억 달러에 달할 것으로 전망됩니다. 이 부문은 분자 검사, 미생물학적 분석, 면역 측정, 독성학 스크리닝 및 전문적인 병리학적 평가를 포함한 첨단 진단 절차를 지원할 수 있기 때문에 여전히 널리 선호되고 있습니다. 이러한 검사에서는 질환을 정확하게 감지하기 위해 높은 정확도와 신뢰성을 확보하기 위해, 첨단 검사실 인프라, 숙련된 전문가, 그리고 통제된 환경이 필요합니다.

2025년, 북미 수의 진단 시장은 46.5%의 점유율을 차지했습니다. 이 지역의 경쟁력은 선진적인 수의의료 인프라, 높은 반려동물 사육률, 진단 기술 도입률의 높음, 그리고 혁신적인 동물 보건 기술의 광범위한 활용에 의해 뒷받침되고 있습니다. 확립된 진단 기업의 존재, 광범위한 검사실 네트워크, 그리고 잘 갖춰진 수의학 시스템이 이 지역 시장 경쟁력과 지속적인 성장을 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022년-2035년

제6장 시장 추산 및 예측 : 모달리티별, 2022년-2035년

제7장 시장 추산 및 예측 : 기술별, 2022년-2035년

제8장 시장 추산 및 예측 : 용도별, 2022년-2035년

제9장 시장 추산 및 예측 : 동물 유형별, 2022년-2035년

제10장 시장 추산 및 예측 : 최종 용도별, 2022년-2035년

제11장 시장 추산 및 예측 : 지역별, 2022년-2035년

제12장 기업 개요

LSH 26.07.14The Global Veterinary Diagnostics Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 12.6 billion by 2035.

Market expansion is driven by the rising incidence of infectious, zoonotic, and chronic diseases across both companion and livestock animal populations, along with growing awareness of preventive veterinary healthcare. The increasing frequency of disease outbreaks continues to reinforce the need for accurate and rapid diagnostic solutions. Over recent years, the market has shown consistent growth, supported by higher expenditure on companion animal healthcare and continuous advancements in diagnostic technologies. The growing burden of emerging and transboundary animal diseases is further accelerating demand for reliable testing solutions. Rising global populations of companion animals and production livestock are also strengthening overall market demand. Pet ownership is increasing steadily, particularly for dogs and cats, while owners are showing greater willingness to invest in routine wellness screening and preventive care. At the same time, technological progress in molecular diagnostics, PCR-based methods, next-generation sequencing, biomarker assays, and portable point-of-care systems is improving the speed, precision, and accessibility of disease detection.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 9.1% |

The consumables segment accounted for a 51.3% share in 2025 and continues to grow at a CAGR of 9.2% during 2026-2035. This dominance is driven by its essential role across diagnostic workflows and its recurring revenue structure. Consumables include reagents, diagnostic kits, assay cartridges, blood collection tubes, slides, calibration tools, and control materials, which are widely used across veterinary hospitals, clinics, diagnostic laboratories, and research centers.

The lab-based testing segment is projected to reach USD 7.1 billion by 2035. This segment remains widely preferred due to its ability to support advanced diagnostic procedures, including molecular testing, microbiological analysis, immunoassays, toxicology screening, and specialized pathology evaluations. These tests require advanced laboratory infrastructure, skilled professionals, and controlled environments to ensure high accuracy and reliability in disease detection.

North America Veterinary Diagnostics Market held 46.5% share in 2025. The region's dominance is supported by advanced veterinary healthcare infrastructure, high pet ownership levels, strong diagnostic adoption rates, and widespread use of innovative animal health technologies. The presence of established diagnostic companies, extensive laboratory networks, and well-developed veterinary care systems further reinforces regional market strength and sustained growth.

Key industry participants include Zoetis, IDEXX Laboratories, bioMerieux, Bio-Rad Laboratories, Thermo Fisher Scientific, Neogen, QIAGEN, Virbac, Randox Laboratories, Fujifilm, Mindray Animal Medical Technology, BioNote, IDvet, INDICAL Bioscience, MEGACOR Diagnostik, Eurolyser Diagnostica, Agrolabo, Biochek, and GD Animal Health (Royal GD). Companies in the veterinary diagnostics market are strengthening their market position by focusing on continuous innovation in diagnostic technologies that improve the speed, accuracy, and reliability of test results. Many players are expanding their portfolios with advanced molecular diagnostics, multiplex testing platforms, and automated laboratory systems. Strategic collaborations with veterinary clinics, hospitals, and diagnostic laboratories are helping companies improve distribution reach and service integration. Firms are also investing heavily in research and development to introduce next-generation sequencing, biomarker-based assays, and portable diagnostic solutions. Expansion into emerging markets with growing pet populations and livestock industries is another key focus area.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy & data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation for any one approach

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Product trends

- 2.2.3 Modality trends

- 2.2.4 Technology trends

- 2.2.5 Application trends

- 2.2.6 Animal type trends

- 2.2.7 End use trends

- 2.2.8 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing trend of adopting pet animals

- 3.2.1.2 Rising prevalence of foodborne and zoonotic diseases

- 3.2.1.3 Favorable government initiatives

- 3.2.1.4 Advancements in companion diagnostics

- 3.2.1.5 Increasing adoption of pet insurance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Prohibitive cost associated with animal tests

- 3.2.2.2 Low out of pocket expenditure on veterinary care

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of point-of-care (POC) diagnostic solutions

- 3.2.3.2 Integration of AI and data analytics in diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technological and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies (Driven by Primary Research)

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historic price trend analysis

- 3.5.2 Pricing analysis, by drug type

- 3.6 Regulatory landscape (Driven by Primary Research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.10 Investment and funding landscape (Driven by Primary Research)

- 3.11 Future market trends (Driven by Primary Research)

- 3.12 Pet population statistics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments

- 5.4 Softwares

Chapter 6 Market Estimates and Forecast, By Modality, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Point-of-care testing (POC)

- 6.3 Lab-based testing

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical biochemistry

- 7.2.1 Glucose monitoring

- 7.2.2 Blood gas and electrolyte analysis

- 7.2.3 Other clinical biochemistry tests

- 7.3 Immunodiagnostics

- 7.3.1 Lateral flow assays

- 7.3.2 ELISA

- 7.3.3 Immunoassay analyzers

- 7.3.4 Other immunodiagnostic tests

- 7.4 Molecular diagnostics

- 7.4.1 PCR

- 7.4.2 Microarrays

- 7.4.3 Other molecular diagnostic tests

- 7.5 Hematology

- 7.6 Urinalysis

- 7.7 Diagnostic imaging (inclusive of AI assisted)

- 7.8 Other technologies

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Bacteriology

- 8.3 Pathology

- 8.4 Parasitology

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Companion animals

- 9.2.1 Dogs

- 9.2.2 Cats

- 9.2.3 Horses

- 9.2.4 Other companion animals

- 9.3 Farm animals

- 9.3.1 Cattle

- 9.3.2 Swine

- 9.3.3 Poultry

- 9.3.4 Other farm animals

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Diagnostic labs

- 10.4 Home care settings

- 10.5 Other end users

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Agrolabo

- 12.2 Bio-Rad Laboratories

- 12.3 bioMerieux

- 12.4 BioNote

- 12.5 Biochek

- 12.6 Eurolyser Diagnostica

- 12.7 Fujifilm

- 12.8 GD Animal Health (Royal GD)

- 12.9 IDEXX Laboratories

- 12.10 IDvet

- 12.11 INDICAL Bioscience

- 12.12 MEGACOR Diagnostik

- 12.13 Mindray Animal Medical Technology

- 12.14 Neogen

- 12.15 QIAGEN

- 12.16 Randox Laboratories

- 12.17 Thermo Fisher Scientific

- 12.18 Virbac

- 12.19 Zoetis