|

시장보고서

상품코드

2083358

수의학 신속 검사 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Veterinary Rapid Tests Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

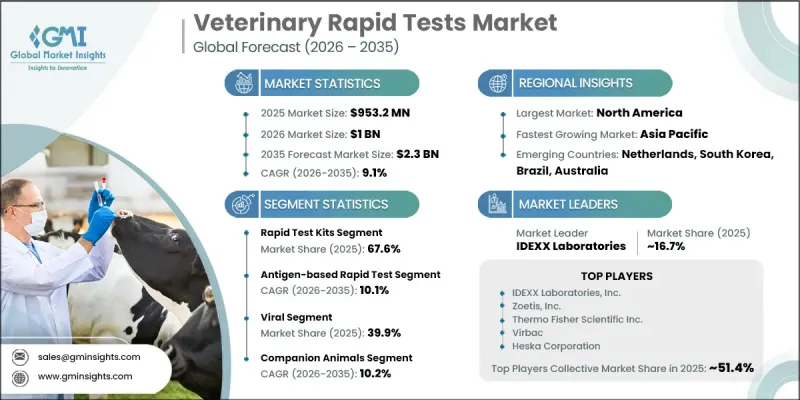

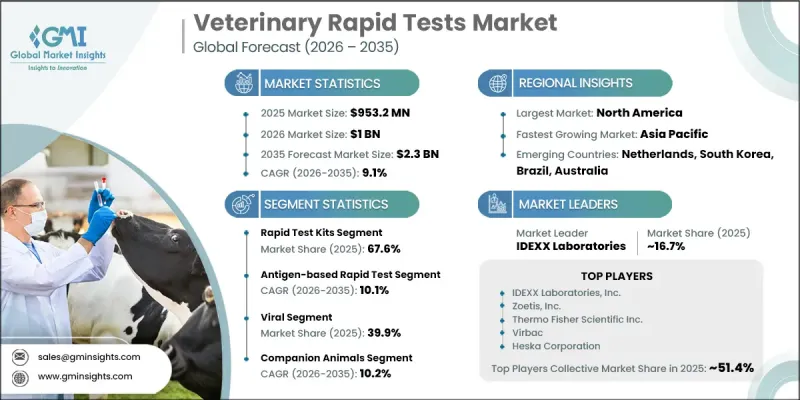

세계의 수의학 신속 검사 시장은 2025년에 9억 5,320만 달러 규모로 평가되었고, CAGR 9.1%로 성장하여 2035년까지 23억 달러에 이를 것으로 예측됩니다.

이 시장의 성장은 중앙 집중식 진단실험실에서 반려동물 진료소 및 가축 현장 작업을 포함한 모든 수의학 환경에서의 현장 진단 검사로의 지속적인 전환에 의해 주도되고 있습니다. 반려동물 사육 마릿수 증가, 동물 예방 의료에 대한 관심 고조, 그리고 신속한 진단 결과에 대한 수요 증가가 시장 확산을 더욱 뒷받침하고 있습니다. 또한, ‘원 헬스(One Health)’ 이니셔티브의 영향력이 커짐에 따라 동물과 인간을 아우르는 통합적인 질병 모니터링이 지원되고 있으며, 이는 신속 진단 도구의 중요성을 더욱 부각시키고 있습니다. 측류 분석 기술의 지속적인 비용 절감으로 인해, 개발도상국과 선진국을 막론하고 합리적인 가격으로 이용할 수 있게 되었으며 접근성도 향상되고 있습니다. 또한, 다중 검사 및 디지털 연결 솔루션의 발전으로 진단 정확도가 향상되었으며, 실시간 데이터 공유가 가능해졌습니다. 반려동물 주인과 축산 농가 사이에서 질병의 조기 발견에 대한 인식이 높아지면서 이용률이 더욱 가속화되고 있으며, 수의학 분야의 신속 진단은 동물 보건 업계 전체에서 꾸준히 성장하고 있는 분야로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 9억 5,320만 달러 |

| 예측액 | 23억 달러 |

| CAGR | 9.1% |

신속 검사 키트 부문은 2025년에 67.6%의 시장 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 9.9%로 성장할 것으로 전망됩니다. 이 부문의 경쟁력은 소모품에 대한 지속적인 수요 패턴, 다양한 동물 질병에 걸친 폭넓은 임상 적용 가능성, 그리고 반려동물과 가축의 건강 관리 모두를 대상으로 하는 제조업체들의 지속적인 혁신에 의해 뒷받침되고 있습니다. 이러한 사용 편의성, 신속한 검사 결과 확보, 그리고 현장 검사에의 적합성이 수의학 시스템 전반에 걸친 도입을 더욱 촉진하고 있습니다.

동물병원 부문은 2025년에 39.7%의 시장 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 8.6%로 성장할 것으로 전망됩니다. 이 부문이 주도적인 위치를 차지하고 있는 것은 동물 의료 서비스 제공업체의 집중도가 높고, 신속한 의사결정을 위해 병원 내 진단 검사에 대한 의존도가 높기 때문입니다. 동물병원은 동물 의료 서비스, 특히 반려동물을 위한 주요 접근 창구로 여전히 자리 잡고 있으며, 신속 검사는 즉각적인 치료 계획 수립과 질병 관리를 뒷받침하고 있습니다. 현장 진단에 대한 수요가 증가함에 따라, 수의학 서비스 제공에서 현장 진단이 차지하는 핵심적인 역할이 더욱 공고해지고 있습니다.

북미의 수의학용 신속 검사 시장은 2025년에 40.5%의 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 8.3%로 성장하여 세계 시장에서 지배적인 위치를 유지할 것으로 전망됩니다. 이 지역의 선도적 지위는 높은 반려동물 사육률, 선진적인 수의의료 인프라, 그리고 진단 기술의 적극적인 도입에 의해 뒷받침되고 있습니다. 미국은 수많은 동물병원이 존재하고, 동물의 예방 의료 및 질병 조기 발견에 대한 중요성이 부각되고 있는 것을 배경으로, 계속해서 해당 지역 수요를 견인하는 주요 요인으로 작용하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 테스트 유형별, 2022년-2035년

제7장 시장 추산 및 예측 : 용도별, 2022년-2035년

제8장 시장 추산 및 예측 : 동물 유형별, 2022년-2035년

제9장 시장 추산 및 예측 : 샘플 유형별, 2022년-2035년

제10장 시장 추산 및 예측 : 최종 용도별, 2022년-2035년

제11장 시장 추산 및 예측 : 지역별, 2022년-2035년

제12장 기업 개요

LSH 26.07.14The Global Veterinary Rapid Tests Market was valued at USD 953.2 million in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 2.3 billion by 2035.

The market growth is driven by the ongoing shift from centralized diagnostic laboratories toward point-of-care testing across veterinary care environments, including companion animal clinics and livestock field operations. Expanding pet ownership, increasing focus on preventive animal healthcare, and rising demand for fast diagnostic outcomes are further strengthening market adoption. The growing influence of One Health initiatives is also supporting integrated disease monitoring across animals and humans, reinforcing the importance of rapid diagnostic tools. Continuous cost reductions in lateral flow assay technologies are improving affordability and accessibility across developing and developed regions. In addition, advancements in multiplex testing and digital connectivity solutions are enhancing diagnostic accuracy and enabling real-time data sharing. Rising awareness among pet owners and livestock producers regarding early disease detection is further accelerating utilization rates, making veterinary rapid diagnostics a consistently expanding segment within the broader animal health industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $953.2 Million |

| Forecast Value | $2.3 Billion |

| CAGR | 9.1% |

The rapid test kits segment held 67.6% share in 2025 and is projected to grow at a CAGR of 9.9% through 2035. The dominance of this segment is supported by its recurring consumable demand model, wide clinical applicability across multiple animal diseases, and continuous innovation by manufacturers targeting both companion and livestock health applications. Their ease of use, quick turnaround time, and suitability for on-site testing further strengthen their adoption across veterinary care systems.

The veterinary clinics segment held 39.7% share in 2025 and is projected to grow at a CAGR of 8.6% through 2035. This segment leads due to the high concentration of veterinary service providers and the strong reliance on in-clinic diagnostic testing for timely decision-making. Clinics remain the primary access point for animal healthcare services, particularly for companion animals, where rapid testing supports immediate treatment planning and disease management. Increasing demand for point-of-care diagnostics continues to reinforce their central role in veterinary healthcare delivery.

North America Veterinary Rapid Tests Market accounted for 40.5% share in 2025 and is expected to grow at a CAGR of 8.3% through 2035, maintaining its dominant global position. The region's leadership is supported by high companion animal ownership rates, advanced veterinary care infrastructure, and strong adoption of diagnostic technologies. The United States remains the primary contributor to regional demand, driven by a large base of veterinary practices and increasing emphasis on preventive animal healthcare and early disease detection.

Key market participants include Zoetis, IDEXX Laboratories, Thermo Fisher Scientific, Virbac, Neogen, Heska Corporation (Mars Inc.), BioNote, MEGACOR Diagnostik, Fassisi, Swissavans, INDICAL Bioscience, VetAll Laboratories, BioChek, Agrolabo, and Shenzhen Bioeasy Biotechnology. Companies in the veterinary rapid tests market are strengthening their market position through continuous product innovation focused on improving diagnostic speed, accuracy, and ease of use. Many players are expanding their portfolios with multiplex testing solutions capable of detecting multiple pathogens in a single test. Strategic investments in digital diagnostics and connected platforms are enabling real-time data sharing and enhanced clinical decision-making. Firms are also increasing partnerships with veterinary clinics, laboratories, and distributors to improve market penetration. Expansion into emerging markets with rising pet adoption and livestock populations is another key strategy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Test type trends

- 2.2.4 Application trends

- 2.2.5 Animal type trends

- 2.2.6 Sample type trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of companion animal population

- 3.2.1.2 Increasing prevalence of zoonotic diseases in animals

- 3.2.1.3 Rising demand for rapid test diagnosis over other tests

- 3.2.1.4 Increasing pet ownership

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Limited number of infrastructures for veterinary diagnosis

- 3.2.2.2 Lack of awareness for veterinary health in underdeveloped countries

- 3.2.2.3 Increasing cost of animal healthcare

- 3.2.3 Market opportunities

- 3.2.3.1 Development of multiplex and portable rapid testing solutions

- 3.2.3.2 Expansion of veterinary diagnostics in emerging and rural markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technology

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East and Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Impact of AI and generative AI on the market

- 3.10 Future market trends (Driven by primary research)

- 3.11 Pet population statistics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Rapid test kits

- 5.3 Rapid test readers

Chapter 6 Market Estimates and Forecast, By Test Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Antigen based rapid test

- 6.3 Antibody-based rapid test

- 6.4 Mixed tests

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Viral

- 7.3 Parasitic

- 7.4 Bacterial

- 7.5 Allergies

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Companion animals

- 8.2.1 Dogs

- 8.2.2 Cats

- 8.2.3 Horses

- 8.2.4 Other companion animals

- 8.3 Livestock animals

- 8.3.1 Cattle

- 8.3.2 Swine

- 8.3.3 Poultry

- 8.3.4 Other livestock animals

Chapter 9 Market Estimates and Forecast, By Sample Type, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Blood

- 9.3 Feces

- 9.4 Serum

- 9.5 Plasma

- 9.6 Urine

- 9.7 Other sample types

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Homecare settings

- 10.3 Veterinary hospitals

- 10.4 Veterinary clinics

- 10.5 Other end users

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Zoetis

- 12.2 IDEXX Laboratories

- 12.3 Thermo Fisher Scientific

- 12.4 Virbac

- 12.5 Neogen

- 12.6 Heska Corporation (Mars Inc.)

- 12.7 BioNote

- 12.8 MEGACOR Diagnostik

- 12.9 Fassisi

- 12.10 Swissavans

- 12.11 INDICAL Bioscience

- 12.12 VetAll Laboratories

- 12.13 BioChek

- 12.14 Agrolabo

- 12.15 Shenzhen Bioeasy Biotechnology