|

시장보고서

상품코드

2051999

수의용 PoC 진단 시장 예측(-2031년) : 제품(소모품, 기기), 기술(면역진단, 분자진단(등온 증폭, PCR, CRISPR)), 동물 유형별(반려동물, 가축, 가금류)Veterinary PoC Diagnostics Market by Product (Consumables and Instruments), Technology [Immunodiagnostics, Molecular Diagnostics (Isothermal Amplification, PCR, CRISPR)], Animal Type (Companion Animals, Livestock, Poultry) - Global Forecast to 2031 |

||||||

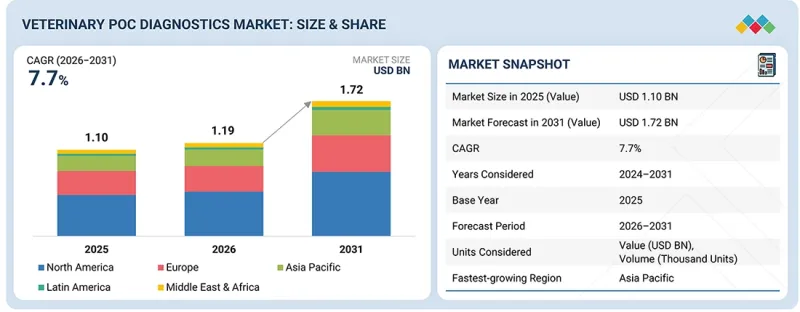

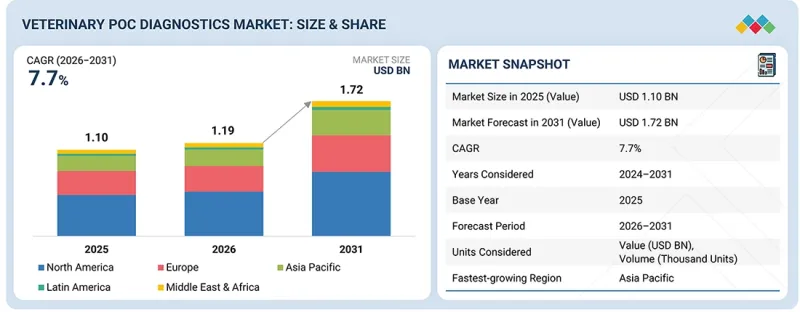

수의용 PoC 진단 시장 규모는 2026년 11억 9,000만 달러에서 2031년에는 17억 2,000만 달러로, CAGR 7.7%로 확대할 것으로 예측됩니다.

이러한 성장은 신속한 수의학 진단, 분산형 검사, 실시간 동물 헬스케어의 미래를 형성하는 몇 가지 주요 요인에 의해 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 기술, 동물 유형, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

수의학 PoC 진단 시장은 주로 반려동물 및 가축 진료 현장에서 질병 식별에 대한 관심이 높아지면서 신속한 임상적 판단의 필요성이 대두되고 있습니다. 반려동물 사육 및 가축의 집약화 추세에 따라 신속한 임상적 판단이 요구되는 가운데, 수의사 및 동물의료 서비스 제공자들은 조기 발견과 정기적인 건강 모니터링을 중요시하고 있으며, 이를 통해 질병 부담 경감 및 치료 관리의 향상을 도모하고 있습니다. 이에 따라 동물병원, 농장, 현장 수의사들은 신속한 질병 확인을 위해 신속 면역측정법, 휴대용 분자 진단 시스템, 휴대용 분석기 등 POC 장비를 점점 더 많이 채택하고 있습니다.

또 다른 주요 촉진요인은 동물 건강 예방, 바이오 보안, 인수공통전염병 및 경제적으로 중요한 질병 관리에 대한 관심의 증가입니다. 정부, 수의사협회, 동물 사육자들은 질병 발생 건수를 줄이고 식품 안전과 공중 보건을 보호하기 위해 질병 모니터링에 더욱 집중하고 있습니다. 이에 따라 신속한 질병 검출 및 치료 방침 결정을 위한 PoC 검사에 대한 수요가 증가하고 있습니다.

또한 현재 PoC 진단 시장은 아직 개발 중이지만, 진단 기술의 발전, 특히 소형화 및 휴대성이 향상된 진단 기기, 등온증폭 기술, 통합형 디지털 플랫폼의 등장으로 PoC 진단 툴의 성능과 실용성이 향상되고 있습니다. 카트리지 방식, 즉석 진단키트, 네트워크 접속형 진단기기 등의 개발로 검사시간의 대폭적인 단축, 공정의 자동화가 실현되어 PoC 진단의 보다 폭넓은 활용이 가능해질 전망입니다.

동물 유형별로는 반려동물이 예측 기간 중 더 높은 CAGR을 기록할 것으로 예상됩니다.

반려동물 부문은 전 세계 반려동물 수의 증가와 반려동물의 '인간화'가 진행되고 고급 수의학에 대한 지출이 증가함에 따라 시장에서 더 높은 성장률을 보일 것으로 예상됩니다. 반려동물 보호자들은 질병의 조기 발견과 즉각적인 치료 결정을 위해 진료소 내에서의 빠른 진단을 점점 더 많이 요구하고 있으며, 이는 동물병원의 PoC 기술 도입을 촉진하고 있습니다. 또한 예방의학에 대한 인식이 높아지고, 동물병원을 자주 방문하며, 반려동물을 위한 맞춤형 첨단 진단 솔루션이 보급되면서 이 부문의 성장이 더욱 가속화되고 있습니다.

기술별로는 면역 진단 부문이 2025년 가장 큰 시장 점유율을 차지했습니다.

2025년 면역진단 부문은 측방유동 어세이 및 ELISA 기반 키트와 같이 신속하고 간편한 검사 형태가 광범위하게 사용되면서 수의학 PoC 진단 시장을 주도할 것으로 예상됩니다. 이러한 검사는 반려동물과 가축 모두에서 감염, 기생충, 바이오마커를 검출하는 데 일반적으로 사용되며, 일상적인 수의학 진료에 필수적인 요소로 자리 잡았습니다. 빠른 결과 도출, 비용 효율성, 최소한의 시료 준비, 첨단 인프라를 필요로 하지 않는 진료소 및 현장 사용에 적합하다는 장점은 높은 도입 실적을 이끌며 면역진단을 시장의 주요 부문로 만들고 있습니다.

예측 기간 중 아시아태평양이 가장 높은 성장률을 기록할 것으로 예상됩니다.

아시아태평양은 수의용 PoC 진단 시장에서 가장 빠른 성장세를 보이고 있습니다. 주요 이유는 이 지역 신흥 국가의 가축 생산량 증가, 반려동물 사육두수 증가, 동물 건강관리에 대한 인식이 높아졌기 때문으로 분석됩니다. 많은 신흥 국가에서 반려동물 사육이 증가하고 있으며, 수의학 인프라의 확충과 질병 감시 및 통제를 위한 정부의 노력으로 진료 현장과 농장에서 휴대용 및 신속 진단 제품의 사용이 확대되고 있습니다. 전염병 및 인수공통전염병 발생률의 증가, 글로벌 및 지역내 주요 기업의 투자 확대로 인해 휴대가 간편하고 사용하기 쉬운 수의용 PoC 진단 기기가 광범위하게 도입되고 있습니다.

세계의 수의용 PoC 진단 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 수의용 POC 진단 시장 : 제품별

제10장 수의용 POC 진단 시장 : 동물 유형별

제11장 수의용 POC 진단 시장 : 기술별

제12장 수의용 POC 진단 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.06.09The veterinary PoC diagnostics market is expected to grow from USD 1.19 billion in 2026 to USD 1.72 billion by 2031, at a CAGR of 7.7%. This growth is driven by several key factors shaping the future of rapid veterinary diagnostics, decentralized testing, and real-time animal health management.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | PRODUCT, TECHNOLOGY ANIMAL TYPE, REGION |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa, |

The veterinary PoC diagnostics market is primarily driven by increasing focus on disease identification at the point of care in companion and farm animals, fueling the need for rapid clinical decision-making. The growing trend of pet ownership and livestock intensification is pushing veterinarians and animal health service providers to emphasize early detection and regular health monitoring, helping them reduce the disease burden and improve treatment management. Consequently, veterinary clinics, farms and field veterinarians are increasingly employing point-of-care instruments such as rapid immunoassays, portable molecular systems, and handheld analyzers for rapid disease identification.

Another key driver is the growing focus on animal health prevention, biosecurity and management of zoonotic and economically important diseases. Governments, veterinary associations, and animal owners are placing greater focus on disease monitoring and surveillance to reduce the number of disease outbreaks and safeguard food safety and public health. This is increasing the demand for PoC testing for rapid disease detection and treatment decision-making.

In addition, while the current PoC diagnostic market is still in development, improvements in diagnostic technology, in particular smaller and more portable diagnostic devices, isothermal amplification techniques, and integrated digital platforms, are improving the potency and viability of PoC diagnostic tools. Developments including cartridge-based approaches, ready-to-use diagnostic kits, and connected diagnostic devices will greatly reduce testing times, automate processes, and make the wider use of PoC diagnostics more feasible.

By animal type, companion animals to record higher CAGR during forecast period

The companion animals segment is expected to witness a higher growth rate in the veterinary PoC diagnostics market due to the rising global pet population and increasing humanization of pets, leading to higher spending on advanced veterinary care. Pet owners are increasingly demanding rapid, in-clinic diagnostics for early disease detection and immediate treatment decisions, driving adoption of PoC technologies in veterinary clinics. Additionally, greater awareness of preventive healthcare, frequent veterinary visits, and the availability of advanced, user-friendly diagnostic solutions tailored for companion animals are further accelerating growth in this segment.

By technology, immunodiagnostics segment accounted for largest market share in 2025

In 2025, the immunodiagnostics segment dominated the veterinary PoC diagnostics market due to its widespread use in rapid, easy-to-perform testing formats such as lateral flow assays and ELISA-based kits. These tests are commonly used to detect infectious diseases, parasites, and biomarkers across both companion and livestock animals, making them integral to routine veterinary practice. Their advantages, including quick turnaround time, cost-effectiveness, minimal sample preparation, and suitability for in-clinic and field settings without advanced infrastructure, drive high adoption volumes and make immunodiagnostics the dominant segment in the market.

Asia Pacific to witness highest growth rate during forecast period

The Asia Pacific region is growing at the fastest rate in the veterinary PoC diagnostics market. The main reason for this is due to rising livestock production, pet ownership, and awareness of animal health management in emerging countries of the region. Pet adoption is increasing in many emerging nations, coupled with the rising use of portable, rapid diagnostic products in clinical and farm settings due to expanding veterinary infrastructure and government initiatives for disease surveillance and control. The growing incidence of infectious and zoonotic diseases and an increase in investments by global and regional players are leading to the wide adoption of portable, user-friendly veterinary PoC diagnostics.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Note: C-level executives include CEOs, COOs, CTOs, and VPs.

Other designations include sales, marketing, and product managers.

Breakdown of demand-side primary interviews:

- By End User: Veterinary Hospitals & Clinics (50%), Homecare Settings (35%), Other End Users (15%)

By Designation: Veterinarians/Veterinary Practitioners (47%), Veterinary Clinics or Hospital Directors/Owners (22%), Livestock Farm Managers/Animal Health Managers (15%), and Others (16%)

- By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Note: Other end users include academic and research institutes, livestock farm owners, and animal welfare organizations.

Note: Other designations include laboratory technicians, practice managers, procurement officers, and academic researchers.

Research Coverage

The market study covers the veterinary PoC diagnostics market in various segments. It aims to estimate the market size and growth potential of this market by product, technology, animal type, and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can assist established companies and newer or smaller firms in understanding market trends, enabling them to capture a larger market share. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

- Analysis of key drivers (rising demand for rapid, on-site diagnosis and immediate clinical decision-making, increasing pet ownership and intensification of livestock production), restraints (limited sensitivity/accuracy compared to centralized laboratory testing in some cases, high cost of advanced PoC devices and limited adoption in low-income regions), opportunities (technological advancements in portable molecular diagnostics and biosensors, growing adoption in emerging markets with expanding veterinary infrastructure), and challenges (lack of standardization and regulatory variations across regions, limited skilled professionals for proper use and interpretation of PoC tests) influencing the growth of the veterinary PoC diagnostics market

- Product Development/Innovation: Detailed insights on upcoming technologies and product launches in the veterinary PoC diagnostics market

- Market Development: Comprehensive information about lucrative emerging markets by analyzing the markets for various types of PoC diagnostic products across regions

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary PoC diagnostics market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary PoC diagnostics market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN VETERINARY POC DIAGNOSTICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 VETERINARY POC DIAGNOSTICS MARKET OVERVIEW

- 3.2 VETERINARY POC DIAGNOSTICS MARKET IN ASIA PACIFIC, BY PRODUCT AND COUNTRY

- 3.3 VETERINARY POC DIAGNOSTICS MARKET: REGIONAL MIX

- 3.4 VETERINARY POC DIAGNOSTICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.5 VETERINARY POC DIAGNOSTICS MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising incidence of transboundary and endemic diseases

- 4.2.1.2 Increasing demand for animal-derived food products

- 4.2.1.3 Technological advancements in molecular diagnostics, multiplex assays, and rapid testing platforms

- 4.2.1.4 Growth in companion animal population

- 4.2.1.5 Rising demand for pet insurance and growing animal health expenditure

- 4.2.2 RESTRAINTS

- 4.2.2.1 Rising pet care costs

- 4.2.2.2 High cost of veterinary diagnostic tests

- 4.2.2.3 Limited diagnostic infrastructure in emerging economies

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of AI & ML in veterinary PoC diagnostics

- 4.2.3.2 Expansion of rapid PoC and portable on-farm diagnostic solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Rapid mutation and strain variability of viral pathogens

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN VETERINARY POC DIAGNOSTICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ANIMAL HEALTH INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING TREND OF VETERINARY POC DIAGNOSTIC PRODUCTS, BY KEY PLAYER, 2023-2025

- 5.5.1.1 Pricing trend of veterinary PoC diagnostic products, by key player, 2023-2025

- 5.5.2 PRICING TREND OF VETERINARY POC DIAGNOSTIC PRODUCTS, BY REGION, 2023-2025

- 5.5.2.1 Pricing trend of PCR kits, by region, 2023-2025

- 5.5.2.2 Pricing trend of immunodiagnostic veterinary POC products, by region, 2023-2025

- 5.5.1 PRICING TREND OF VETERINARY POC DIAGNOSTIC PRODUCTS, BY KEY PLAYER, 2023-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 TRADE DATA FOR HS CODE 3822-COMPLIANT PRODUCTS

- 5.6.1.1 Country-wise import data for HS code 3822-compliant products, 2021-2025

- 5.6.1.2 Country-wise export data for HS code 3822-compliant products, 2021-2025

- 5.6.1 TRADE DATA FOR HS CODE 3822-COMPLIANT PRODUCTS

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 USE OF AI-POWERED POULTRY DISEASE DIAGNOSTICS FOR COCCIDIOSIS & SALMONELLA DETECTION

- 5.10.2 ADOPTION OF AI-ENABLED POC DIAGNOSTIC PLATFORM FOR PARASITE DETECTION

- 5.10.3 DEVELOPMENT OF SNAP 4DX PLUS TEST FOR RAPID VECTOR-BORNE DISEASE DETECTION

- 5.11 IMPACT OF US TARIFFS ON VETERINARY POC DIAGNOSTICS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.5 IMPACT ON END USERS

- 5.11.5.1 Veterinary hospitals & clinics

- 5.11.5.2 Livestock producers & animal health networks

- 5.11.5.3 Home care settings

- 5.11.5.4 Other end users (mobile veterinary service providers, animal shelters, NGOs)

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY/EMERGING TECHNOLOGIES

- 6.1.1 CRISPR-BASED MOLECULAR DIAGNOSTICS

- 6.1.2 ISOTHERMAL AMPLIFICATION AND PAPER-BASED LAMP

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 MICROFLUIDICS & LAB-ON-A-CHIP DEVICES

- 6.2.2 BIOSENSOR-BASED DIAGNOSTIC SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 AI & MACHINE LEARNING

- 6.3.2 WEARABLE BIOSENSORS & REMOTE MONITORING DEVICES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 NEAR TERM (2025-2027)

- 6.4.2 MID TERM (2028-2030)

- 6.4.3 LONG TERM (2030+)

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR VETERINARY INFECTIOUS DISEASE DIAGNOSTICS

- 6.5.2 JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 PRECISION FLOCK-LEVEL DISEASE PREDICTION

- 6.6.2 MINI FULLY INTEGRATED ON-FARM MOLECULAR TESTING PLATFORMS

- 6.6.3 MULTIPLEX AND SYNDROMIC VETERINARY DIAGNOSTIC PANELS

- 6.6.4 SMART BIOSENSOR-ENABLED REAL-TIME HEALTH MONITORING

- 6.7 IMPACT OF AI/GENERATIVE AI ON VETERINARY POC DIAGNOSTICS MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL IN VETERINARY POC DIAGNOSTIC ECOSYSTEM

- 6.7.3 AI USE CASES

- 6.7.4 KEY COMPANIES IMPLEMENTING AI IN VETERINARY POC DIAGNOSTICS MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY ANALYSIS

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 RECYCLED AND ECO-FRIENDLY MATERIALS FOR VETERINARY POC DIAGNOSTIC PRODUCTS

- 7.2.2 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.3.1 UNMET NEEDS OF VARIOUS END USERS

- 8.4 MARKET PROFITABILITY

9 VETERINARY POC DIAGNOSTICS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 INCREASING PREVALENCE OF INFECTIOUS AND ZOONOTIC DISEASES IN ANIMALS TO BOOST DEMAND

- 9.2.2 GLOBAL VOLUME ANALYSIS OF CONSUMABLES, 2024-2031 (THOUSAND UNITS)

- 9.3 INSTRUMENTS

- 9.3.1 SURGING DEMAND FOR PORTABLE AND AUTOMATED DIAGNOSTIC SYSTEMS TO ACCELERATE MARKET GROWTH

- 9.3.2 GLOBAL VOLUME ANALYSIS OF INSTRUMENTS, 2024-2031 (THOUSAND UNITS)

10 VETERINARY POC DIAGNOSTICS MARKET, BY ANIMAL TYPE

- 10.1 INTRODUCTION

- 10.2 COMPANION ANIMALS

- 10.2.1 GROWING PET ADOPTION DUE TO RISING URBANIZATION TO FACILITATE MARKET GROWTH

- 10.2.2 DOG

- 10.2.2.1 Increasing prevalence of canine infectious diseases to support rapid adoption of veterinary care

- 10.2.3 CAT

- 10.2.3.1 Growing awareness of feline infectious diseases to fuel market growth

- 10.2.4 HORSE

- 10.2.4.1 Need to prevent vertical pathogen transmission to stimulate use of extensive PCR surveillance solutions

- 10.2.5 OTHER COMPANION ANIMALS

- 10.3 LIVESTOCK

- 10.3.1 SUSCEPTIBILITY OF LIVESTOCK TO FOOT-AND-MOUTH DISEASE, CLASSICAL SWINE FEVER, AVIAN INFLUENZA TO PROMOTE ADOPTION OF DIAGNOSTIC PRODUCTS

- 10.3.2 CATTLE

- 10.3.2.1 Increasing focus on improving milk quality, herd productivity, and biosecurity management to drive demand

- 10.3.3 PIG

- 10.3.3.1 Growing swine disease outbreaks to accelerate diagnostic utilization

- 10.3.4 POULTRY

- 10.3.4.1 Rrising concerns regarding zoonotic disease transmission to spur demand

- 10.3.5 OTHER LIVESTOCK

11 VETERINARY POC DIAGNOSTICS MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 IMMUNODIAGNOSTICS

- 11.2.1 PRESSING NEED FOR RAPID AND COST-EFFECTIVE INFECTIOUS DISEASE TESTING TO CONTRIBUTE TO MARKET GROWTH

- 11.3 MOLECULAR DIAGNOSTICS

- 11.3.1 PCR-BASED

- 11.3.1.1 Increasing use of portable and multiplex PCR platforms to propel market

- 11.3.2 ISOTHERMAL AMPLIFICATION

- 11.3.2.1 Demand for rapid and low-infrastructure molecular testing to accelerate adoption

- 11.3.3 CRISPR-BASED

- 11.3.3.1 Emerging next-generation pathogen detection technologies to create growth potential

- 11.3.1 PCR-BASED

- 11.4 OTHER TECHNOLOGIES

12 VETERINARY POC DIAGNOSTICS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 NORTH AMERICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 12.2.3 US

- 12.2.3.1 High veterinary healthcare expenditure to drive market

- 12.2.4 CANADA

- 12.2.4.1 Growing pet adoption to drive market

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 EUROPE: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 12.3.3 GERMANY

- 12.3.3.1 Rising awareness of zoonotic diseases to fuel market growth

- 12.3.4 UK

- 12.3.4.1 Increasing pet ownership to stimulate demand

- 12.3.5 FRANCE

- 12.3.5.1 Willingness of pet owners to spend on pet health to promote market growth

- 12.3.6 ITALY

- 12.3.6.1 Growing consumption of meat and dairy products to drive market

- 12.3.7 SPAIN

- 12.3.7.1 Growing demand for poultry products to fuel market growth

- 12.3.8 NETHERLANDS

- 12.3.8.1 Developments in veterinary diagnostic products to support market growth

- 12.3.9 POLAND

- 12.3.9.1 Rapid expansion of poultry production and export-oriented farming to elevate demand

- 12.3.10 SWEDEN

- 12.3.10.1 Strong veterinary healthcare infrastructure and advanced animal welfare regulations to propel market

- 12.3.11 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 ASIA PACIFIC: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 12.4.3 CHINA

- 12.4.3.1 Increasing incidence of zoonotic diseases to propel market

- 12.4.4 JAPAN

- 12.4.4.1 Increasing pet expenditure to support market growth

- 12.4.5 INDIA

- 12.4.5.1 Increasing demand for dairy products to drive market

- 12.4.6 AUSTRALIA

- 12.4.6.1 Rise in pet ownership to support market growth

- 12.4.7 SOUTH KOREA

- 12.4.7.1 Rising need for specialized veterinary services to drive market

- 12.4.8 NEW ZEALAND

- 12.4.8.1 Focus on pet insurance to aid market

- 12.4.9 THAILAND

- 12.4.9.1 Growing focus on disease surveillance to drive market

- 12.4.10 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 LATIN AMERICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 12.5.3 BRAZIL

- 12.5.3.1 Booming livestock industry to boost demand

- 12.5.4 MEXICO

- 12.5.4.1 Expanding poultry sector to support market growth

- 12.5.5 ARGENTINA

- 12.5.5.1 Expanding poultry production and increasing focus on disease monitoring to drive market

- 12.5.6 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 12.6.3 GCC COUNTRIES

- 12.6.3.1 Kingdom of Saudi Arabia (KSA)

- 12.6.3.1.1 Technology advancements in veterinary diagnostics to boost demand

- 12.6.3.2 United Arab Emirates (UAE)

- 12.6.3.2.1 Favorable government support for vet diagnostics to drive market

- 12.6.3.3 Rest of GCC Countries

- 12.6.3.1 Kingdom of Saudi Arabia (KSA)

- 12.6.4 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, JANUARY 2022-APRIL 2026

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.4.1 US MARKET SHARE ANALYSIS, 2025

- 13.4.2 EUROPE MARKET SHARE ANALYSIS, 2025

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Product footprint

- 13.5.5.4 Technology footprint

- 13.5.5.5 Animal type footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 BRAND/PRODUCT COMPARISON

- 13.8 R&D EXPENDITURE OF KEY PLAYERS

- 13.9 COMPANY VALUATION AND FINANCIAL METRICS

- 13.9.1 FINANCIAL METRICS

- 13.9.2 COMPANY VALUATION

- 13.10 COMPETITIVE SCENARIO

- 13.10.1 PRODUCT LAUNCHES/APPROVALS/ENHANCEMENTS

- 13.10.2 DEALS

- 13.10.3 EXPANSIONS

- 13.10.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 IDEXX LABORATORIES, INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches/Approvals/Enhancements

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 ZOETIS SERVICES LLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Deals

- 14.1.2.3.2 Expansions

- 14.1.2.3.3 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 THERMO FISHER SCIENTIFIC INC.

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Key strengths

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses & competitive threats

- 14.1.4 ANTECH DIAGNOSTICS, INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches/Approvals/Enhancements

- 14.1.4.3.2 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses & competitive threats

- 14.1.5 BIONOTE

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.4 Product launches/Approvals/Enhancements

- 14.1.5.4.1 Deals

- 14.1.5.5 MnM view

- 14.1.5.5.1 Key strengths

- 14.1.5.5.2 Strategic choices

- 14.1.5.5.3 Weaknesses & competitive threats

- 14.1.6 INNOVATIVE DIAGNOSTICS

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Other developments

- 14.1.7 BIOMERIEUX

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches/Approvals/Enhancements

- 14.1.8 INDICAL BIOSCIENCE GMBH

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches/Approvals/Enhancements

- 14.1.9 VIRBAC

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Deals

- 14.1.9.3.2 Expansions

- 14.1.10 MEGACOR DIAGNOSTIK GMBH

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches/Approvals/Enhancements

- 14.1.11 BIOGAL

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.12 RING BIOTECHNOLOGY CO., LTD.

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Product launches/Approvals/Enhancements

- 14.1.12.3.2 Other developments

- 14.1.13 AGROLABO S.P.A.

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.14 ENALEES

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product launches/Approvals/Enhancements

- 14.1.14.3.2 Deals

- 14.1.14.3.3 Expansions

- 14.1.14.3.4 Other developments

- 14.1.15 BIOPANDA REAGENTS LTD

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.1 IDEXX LABORATORIES, INC.

- 14.2 OTHER PLAYERS

- 14.2.1 FASSISI, GMBH

- 14.2.2 SKYER, INC.

- 14.2.3 GOLD STANDARD DIAGNOSTICS

- 14.2.4 BIO-X DIAGNOSTICS S.A.

- 14.2.5 AFFIGEN INC.

- 14.2.6 ALVEO TECHNOLOGIES

- 14.2.7 FLUXERGY INC.

- 14.2.8 WOODLEY EQUIPMENT COMPANY LTD

- 14.2.9 UBIO BIOTECHNOLOGY SYSTEMS PVT. LTD.

- 14.2.10 CORIS BIOCONCEPT

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH APPROACH

- 15.2 RESEARCH METHODOLOGY DESIGN

- 15.2.1 SECONDARY RESEARCH

- 15.2.1.1 Key data from secondary sources

- 15.2.2 PRIMARY DATA

- 15.2.2.1 Key data from primary sources

- 15.2.2.2 Key industry insights

- 15.2.1 SECONDARY RESEARCH

- 15.3 MARKET SIZE ESTIMATION

- 15.3.1 BOTTOM-UP APPROACH

- 15.4 DATA TRIANGULATION

- 15.5 MARKET SHARE ESTIMATION

- 15.6 RESEARCH ASSUMPTIONS

- 15.7 RESEARCH LIMITATIONS

- 15.7.1 METHODOLOGY-RELATED LIMITATIONS

- 15.7.2 SCOPE-RELATED LIMITATIONS

- 15.8 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.3.1 PRODUCT ANALYSIS

- 16.3.2 COMPANY INFORMATION

- 16.3.3 GEOGRAPHIC ANALYSIS

- 16.3.4 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 16.3.5 COUNTRY-LEVEL VOLUME ANALYSIS BY PRODUCT TYPE

- 16.3.6 BY PRODUCT TYPE MARKET SHARE ANALYSIS (TOP 5 PLAYERS)

- 16.3.7 ANY CONSULT/CUSTOM REQUIREMENTS AS PER CLIENT REQUESTS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS