|

시장보고서

상품코드

1804839

압력 센서 시장 : 감지 방법별, 유형별, 압력 범위별 - 예측(-2030년)Pressure Sensor Market by Sensing Method, Type, Range PSI - Global Forecast to 2030 |

||||||

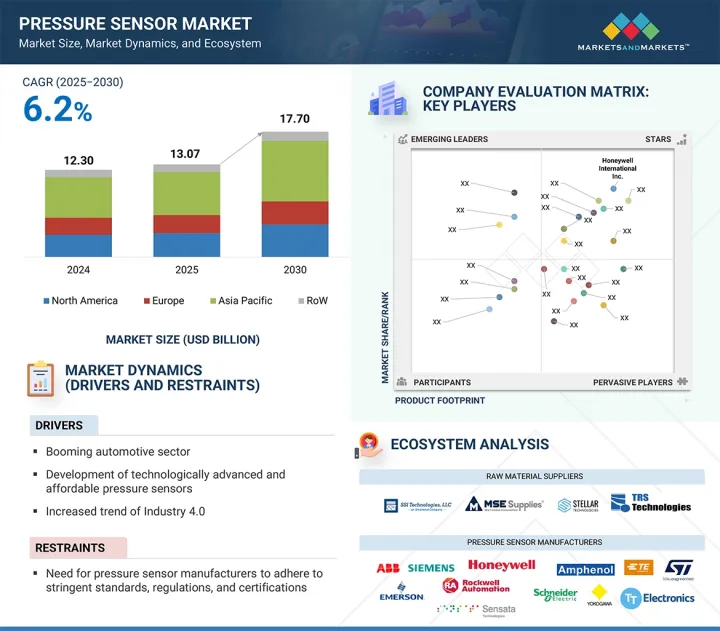

세계의 압력 센서 시장 규모는 2025년 130억 7,000만 달러에서 2030년까지 177억 달러에 이를 것으로 예측되며, 2025-2030년에 CAGR로 6.2%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 접속성, 감지 방법, 감지 유형, 압력 범위, 최종 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

산업계 전반에 걸쳐 예지보전 전략의 채택이 증가하고 있으며, 특히 산업용 IoT 기술의 통합을 통해 압력 센서 시장에 큰 성장 기회를 창출하고 있습니다. 예지보전은 실시간 상태 모니터링에 의존하며, 압력 센서는 기계 및 시스템의 압력 변동을 추적하여 잠재적인 이상을 감지하여 비용이 많이 드는 고장으로 이어지기 전에 감지하는 데 중요합니다. 제조, 석유 및 가스, 유틸리티, 운송 등의 산업에서 예지보전은 계획되지 않은 다운타임을 최소화하고 장비의 수명을 연장하며 운영비용을 절감하기 위해 도입되고 있습니다. IoT 지원 네트워크에 내장된 압력 센서는 지속적인 데이터 스트림을 제공하고 고급 분석 플랫폼을 통해 분석하여 장비의 상태와 유지보수 필요성을 정확하게 예측할 수 있습니다. 이를 통해 기업은 사후 대응형에서 사전 대응형 유지보수 계획으로 전환하여 생산성과 자산의 신뢰성을 향상시킬 수 있습니다.

또한, 클라우드 기반 분석 플랫폼과 안전한 데이터 통신 프로토콜의 등장으로 데이터의 무결성을 보장하면서 예지보전 프로그램 배포를 간소화할 수 있습니다. 조직이 효율성, 비용 관리, 업무 탄력성을 우선시하는 가운데, 예지보전 용도를 위한 스마트 센서(압력 센서)에 대한 수요가 급증할 것으로 예측됩니다. 이러한 추세는 고정밀, 고내구성, IoT 지원 솔루션을 개발하는 센서 제조업체의 기술 혁신을 촉진하여 압력 센서 시장을 더욱 촉진할 것입니다.

"피에조 저항 검출 방식 부문이 2025-2030년 압력 센서 시장에서 높은 CAGR을 나타낼 것으로 예측됩니다. "

피에조 저항 검출 방법 부문은 정확성, 안정성, 비용 효율성에서 우위를 입증하여 2025-2030년 압력 센서 시장에서 높은 CAGR을 나타낼 것으로 예측됩니다. 피에조 저항식 압력 센서는 기계적 변형에 의한 반도체 재료의 저항 변화를 감지하여 작동하며, 고감도의 선형적인 출력 신호를 구현합니다. MEMS 제조 기술과의 호환성을 통해 소형화가 가능하여 의료, 자동차, 소비자 가전 분야에서 사용되는 소형 휴대용 기기에 통합하기에 적합합니다. 자동차 산업에서 피에조 저항식 센서는 다양한 환경 조건에서 높은 내구성과 정확성으로 인해 매니폴드 절대 압력(MAP), 연료, 타이어 압력 모니터링 시스템(TPMS)에 널리 사용되고 있습니다. 의료기기, 특히 카테터 및 주입 펌프와 같은 침습적 응용 분야에서 피에조 저항 센서는 소형 및 고정밀도의 장점으로 인해 선호되고 있습니다. 또한, 실리콘 기반 센서 기술의 발전과 제조 기술의 향상으로 센서의 성능을 향상시키면서 생산 비용을 절감하고 있습니다. 산업계가 보다 신뢰할 수 있고, 에너지 효율적이며, 용도에 특화된 센싱 솔루션을 찾고 있는 가운데, 피에조 저항식 압력 센서는 이용 사례에 관계없이 적응성이 뛰어나다는 장점 때문에 많은 사랑을 받고 있습니다. 이러한 요인들이 종합적으로 예측 기간 동안 피에조 저항 검출 방법 부문의 높은 성장 잠재력에 기여하고 있습니다.

"절대압력 센서 부문이 2025-2030년 압력 센서 시장에서 큰 비중을 차지할 가능성이 높습니다. "

절대압력 센서 부문은 진공에 대한 정확한 압력 측정이 필요한 모든 응용 분야에서 폭넓게 활용될 수 있어 2025-2030년에도 강력한 시장 지위를 유지할 것으로 예측됩니다. 이 센서는 항공우주, 기상학, 산업용 진공 시스템, 자동차 엔진 진단 등 작은 압력 변화도 성능에 영향을 미칠 수 있는 환경에서 필수적인 센서입니다. 자동차 부문에서 절대압 센서는 연료 분사 및 배기가스 제어 최적화에 필수적인 엔진 부하를 계산하는 데 사용되는 매니폴드 절대압(MAP) 센서의 주요 구성 요소입니다. 또한, 이러한 센서는 자동차 및 항공 시스템의 온도 조절기 및 기압 모니터링에도 사용됩니다. 고진동 및 극한의 온도 환경에서 높은 신뢰성으로 특히 항공우주 및 중공업 용도에 적합합니다. 또한, 드론, 기상 모니터링 기기, 휴대용 전자기기 등 스마트 기기 및 커넥티드 기기에 대한 수요가 증가함에 따라 작고 견고하며 정확한 절대 압력 센서의 필요성이 더욱 커지고 있습니다. 대기압 변화에 영향을 받지 않고 안정적인 측정값을 제공할 수 있는 절대압 센서는 밀폐형 시스템 모니터링에도 적합합니다. 이러한 특성과 MEMS 기술 및 소형화의 발전으로 절대압 센서 시장 기여도는 지속적이고 큰 폭으로 증가하고 있습니다.

세계의 압력 센서(Pressure Sensor) 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 지견

- 압력 센서 시장 기업에 있어서 매력적인 기회

- 북미 압력 센서 시장 : 최종 용도별, 국가별

- 압력 센서 시장 : 최종 용도별

- 압력 센서 시장 : 국가별

제5장 시장 개요

- 서론

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 공급망 분석

- 생태계 분석

- 투자 및 자금조달 시나리오

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 가격 결정 분석

- 주요 기업이 제공하는 절대 압력 센서 가격대(2024년)

- 압력 센서 평균 판매 가격 동향 : 용도별(2021년-2024년)

- 압력 센서 평균 판매 가격 동향 : 지역별(2021년-2024년)

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 사례 연구 분석

- ALTHEN SENSORS & CONTROLS, 소형 압력 센서로 네덜란드 DELFT HYPERLOOP 프로젝트를 강화

- SURREY SENSORS LTD, HONEYWELL 압력 센서를 도입하여 UAV와 항공우주 시험 정밀도를 향상

- 대형 농업기계 제조업체가 기계 제어에 WIKA 레벨 센서를 채택

- 압력 트랜스듀서 모니터링에 의해 EMPTEEZY는 긴급 탱크 샤워기에서 일관된 물 흐름 보장

- 의료기기 기업이 중환자 혈압 모니터링에 압력 센서를 채택

- 무역 분석

- 수입 시나리오(HS코드 902620)

- 수출 시나리오(HS코드 902620)

- 관세 및 규제 상황

- 관세 분석

- 규제기관, 정부기관, 기타 조직

- 기준/규제

- 특허 분석

- 주요 컨퍼런스 및 이벤트(2025년-2026년)

- 압력 센서 시장에 대한 AI/생성형 AI의 영향

- 압력 센서 시장에 대한 2025년 미국 관세의 영향

- 서론

- 주요 관세율

- 가격 영향 분석

- 국가/지역에 대한 영향

- 최종 용도에 대한 영향

제6장 다양한 매체에 대응하는 압력 센서

- 서론

- 공기압 센서

- 기압 센서

- 가스 압력 센서

- 수압 센서

- 액체 압력 센서

- 공기압 및 유압 압력 센서

- 부식성 액체 및 가스 압력 센서

제7장 압력 센서 관련 기술

- 서론

- 미세가공 기술

- MEMS

- CMOS

- AI센서 기술

- 머신러닝(ML)

- 자연언어처리(NLP)

- 상황인식 컴퓨팅

- 컴퓨터 비전

제8장 압력 센서 시장 : 접속성별

- 서론

- 유선

- 무선

제9장 압력 센서 시장 : 감지 방법별

- 서론

- 피에조 저항

- 정전용량

- 공진 고체

- 전자

- 광학

- 기타 감지 방법

제10장 압력 센서 시장 : 센서 유형별

- 서론

- 절대압 센서

- 게이지압 센서

- 차압 센서

- 밀폐형 압력 센서

- 진공 압력 센서

제11장 압력 센서 시장 : 압력 범위별

- 서론

- 100PSI 미만

- 101-1,000PSI

- 1,000PSI 이상

제12장 압력 센서 시장 : 최종 용도별

- 서론

- 자동차

- 의료

- 제조

- 유틸리티

- 항공

- 석유 및 가스

- 해사

- 소비자 디바이스

- 기타 용도

제13장 압력 센서 시장 : 지역별

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 기타 지역

- 기타 지역 거시경제 전망

- 중동

- 아프리카

- 남미

제14장 경쟁 구도

- 개요

- 주요 전략/강점(2021년-2025년)

- 시장 점유율 분석(2024년)

- 매출 분석(2020년-2024년)

- 기업 평가와 재무 지표

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제15장 기업 개요

- 주요 기업

- HONEYWELL INTERNATIONAL INC.

- TE CONNECTIVITY

- SENSATA TECHNOLOGIES, INC.

- EMERSON ELECTRIC CO.

- AMPHENOL CORPORATION

- ABB

- TT ELECTRONICS

- ROCKWELL AUTOMATION

- SCHNEIDER ELECTRIC

- SIEMENS

- STMICROELECTRONICS

- INFINEON TECHNOLOGIES AG

- NXP SEMICONDUCTORS

- YOKOGAWA ELECTRIC CORPORATION

- ENDRESS+HAUSER GROUP SERVICES AG

- 기타 기업

- BOSCH SENSORTEC GMBH

- IFM ELECTRONIC GMBH

- JUMO GMBH & CO. KG

- KITA SENSOR TECH. CO., LTD.

- NIDEC CORPORATION

- PHOENIX SENSORS

- MICRO SENSOR CO., LTD

- BD|SENSORS GMBH

- KISTLER GROUP

- OMEGA ENGINEERING INC.

제16장 부록

LSH 25.09.11The pressure sensor market is projected to grow from USD 13.07 billion in 2025 to USD 17.70 billion by 2030, at a CAGR of 6.2% between 2025 and 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By connectivity, sensing method, sensing type, pressure range, end use, and region |

| Regions covered | North America, Europe, APAC, RoW |

The rising adoption of predictive maintenance strategies across industries creates significant growth opportunities for the pressure sensor market, particularly through the integration of Industrial Internet of Things (IoT) technologies. Predictive maintenance depends on real-time condition monitoring, where pressure sensors are critical in tracking pressure fluctuations within machinery and systems to detect potential anomalies before they lead to costly failures. Industries such as manufacturing, oil & gas, utilities, and transportation increasingly implement predictive maintenance to minimize unplanned downtime, extend equipment lifespan, and reduce operational costs. Pressure sensors embedded in IoT-enabled networks provide continuous data streams that, when analyzed through advanced analytics platforms, allow accurate forecasting of equipment health and maintenance needs. This enables companies to shift from reactive to proactive maintenance planning, improving productivity and asset reliability.

Moreover, the rise in cloud-based analytics platforms and secure data communication protocols simplifies the deployment of predictive maintenance programs while ensuring data integrity. As organizations continue to prioritize efficiency, cost control, and operational resilience, the demand for smart sensors-pressure sensors-tailored to predictive maintenance applications is expected to surge. This trend drives innovation among sensor manufacturers to develop high-precision, durable, and IoT-compatible solutions, further propelling the pressure sensor market.

"Piezoresistive sensing method segment is expected to record a significant CAGR in the pressure sensor market from 2025 to 2030."

The piezoresistive sensing method segment is projected to register a significant CAGR in the pressure sensor market from 2025 to 2030 due to its proven advantages in accuracy, stability, and cost-effectiveness. Piezoresistive pressure sensors operate by detecting resistance changes in semiconductor materials under mechanical strain, which allows them to deliver highly sensitive and linear output signals. Their compatibility with MEMS fabrication techniques has enabled miniaturization, making them ideal for integration into compact, portable devices used in medical, automotive, and consumer electronics sectors. In the automotive industry, piezoresistive sensors are widely used in manifold absolute pressure (MAP), fuel, and tire pressure monitoring systems (TPMS) due to their durability and precision under varying environmental conditions. In medical devices, especially in invasive applications such as catheters and infusion pumps, piezoresistive sensors are favored for their small size and high accuracy. Furthermore, advancements in silicon-based sensor technology and improvements in fabrication techniques are reducing production costs while increasing sensor performance. As industries demand more reliable, energy-efficient, and application-specific sensing solutions, piezoresistive pressure sensors are gaining traction due to their adaptability across use cases. These factors collectively contribute to the high growth potential of the piezoresistive sensing method segment during the forecast period.

"Absolute pressure sensor segment is likely to contribute a major share of the pressure sensor market from 2025 to 2030."

The absolute pressure sensor segment is expected to maintain a strong market position from 2025 to 2030, driven by its broad utility across applications that require precise measurement of pressure relative to a vacuum. These sensors are indispensable in environments where even small pressure changes can impact performance, such as aerospace, meteorology, industrial vacuum systems, and automotive engine diagnostics. In the automotive sector, absolute pressure sensors are key components in manifold absolute pressure (MAP) sensors used to calculate engine load, which is critical for optimizing fuel injection and emissions control. Additionally, these sensors are used in climate control and barometric pressure monitoring in automotive and aviation systems. Their reliability in high-vibration and extreme temperature environments makes them particularly suitable for aerospace and heavy industrial applications. Furthermore, the rise in demand for smart and connected devices, including drones, weather monitoring equipment, and portable electronics, further fuels the need for compact, robust, and accurate absolute pressure sensors. Their ability to offer consistent readings unaffected by atmospheric pressure changes also makes them a preferred choice for sealed system monitoring. These characteristics, combined with advances in MEMS technology and miniaturization, ensure a sustained and significant contribution of the absolute pressure sensor segment to the market.

"North America accounted for the largest share of the pressure sensor market in 2024."

North America held the largest share in the pressure sensor market in 2024, primarily due to its advanced industrial infrastructure, strong automotive and aerospace sectors, and the rapid adoption of smart technologies across key verticals. The US, in particular, is a global hub for innovation in sensor technology, with leading companies, such as Honeywell, Emerson Electric, and Amphenol, headquartered in the region. These firms continue to invest heavily in R&D to develop high-performance, application-specific pressure sensors. The early embrace of Industrial IoT (IIoT) and predictive maintenance strategies across manufacturing plants has significantly increased the deployment of pressure sensors for real-time equipment monitoring and operational optimization. Furthermore, the stringent regulatory frameworks, especially regarding vehicle safety and emissions standards, have driven the integration of pressure sensors into engine control units, exhaust systems, and tire pressure monitoring systems (TPMS). In the medical domain, the strong healthcare infrastructure and the growing demand for advanced diagnostic and monitoring equipment have also contributed to increased sensor adoption. Additionally, the push toward renewable energy and smart grid systems creates new applications for pressure sensors in the utility and energy sectors. These diverse and mature end-user markets reinforce North America's leading market share in 2024.

- By Company Type: Tier 1 - 26%, Tier 2 - 32%, and Tier 3 - 42%

- By Designation: C-level Executives - 40%, Managers - 30%, and Others - 30%

- By Region: North America - 34%, Europe - 25%, Asia Pacific- 30%, and RoW - 11%

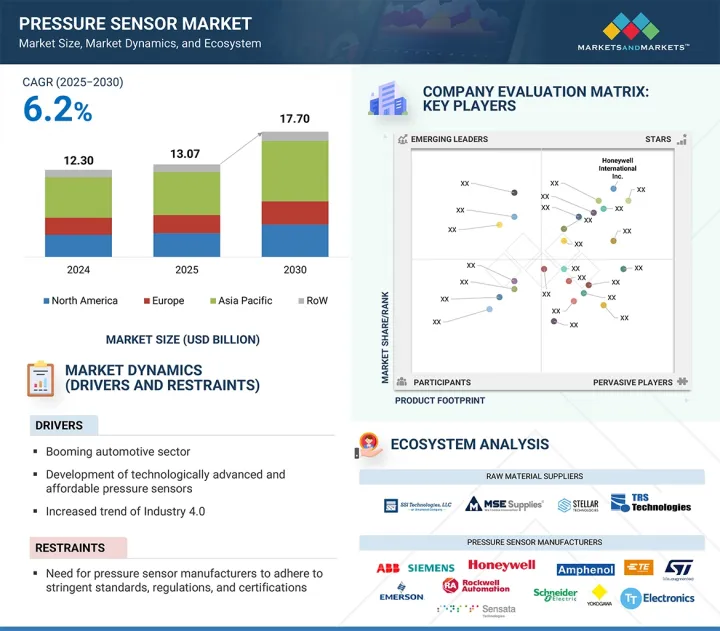

Prominent players profiled in this report include Honeywell International Inc. (US), ABB (Switzerland), Emerson Electric Co. (US), Amphenol Corporation (US), and TE Connectivity (Switzerland).

Report Coverage

The report defines, describes, and forecasts the pressure sensor market based on connectivity (wired sensors, wireless sensors), sensing method (piezoresistive, capacitive, resonant solid-state, electromagnetic, optical, other sensing methods), sensor type (absolute, gauge, differential, sealed, vacuum), pressure range (up to 100 psi, 101-1,000 psi, above 1,000 psi), end use (automotive, medical, manufacturing, utilities, aviation, oil & gas, marine, consumer devices, other end use) and region (North America, Europe, Asia Pacific, RoW). It provides detailed information regarding drivers, restraints, opportunities, and challenges influencing the market growth. It also analyzes competitive developments such as acquisitions, product launches, expansions, and actions carried out by the key players to grow in the market.

Reasons to Buy This Report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue for the overall pressure sensor market and the subsegments. The report will help stakeholders understand the competitive landscape and gain more insight to position their business better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, opportunities, and challenges.

The report will provide insights into the following points:

- Analysis of key drivers (Booming automotive sector, Development of technologically advanced and affordable pressure sensors, Increased trend of Industry 4.0, Rising demand for pressure sensors in medical device industry), restraints (Need for pressure sensor manufacturers to adhere to stringent standards, regulations, and certifications), opportunities (Rising demand for advanced pressure sensors in consumer electronics industry, Adoption of pressure sensors in IoT-enabled predictive maintenance programs, Rapid advancements in AI and ML technologies), and challenges (Shrinking profit margins of manufacturers with declining prices, increasing competition, and commoditization of technology) of the pressure sensor market

- Product development /Innovation: Detailed insights into upcoming technologies, research & development activities, and new product launches in the pressure sensor market

- Market Development: Comprehensive information about lucrative markets; the report analyses the pressure sensor market across various regions

- Market Diversification: Exhaustive information about new products launched, untapped geographies, recent developments, and investments in the pressure sensor market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and offering of leading players, including Honeywell International Inc. (US), ABB (Switzerland), Emerson Electric Co. (US), Amphenol Corporation (US), TE Connectivity (Switzerland), Sensata Technologies, Inc. (US), TT Electronics (UK), Rockwell Automation (US), Schneider Electric (France), Siemens (Germany), STMicroelectronics (Switzerland), Infineon Technologies AG (Germany), and NXP Semiconductors (Netherlands) in the pressure sensor market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 List of key secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 Breakdown of primaries

- 2.1.3.2 Key data from primary sources

- 2.1.3.3 Key industry insights

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- 2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PRESSURE SENSOR MARKET

- 4.2 PRESSURE SENSOR MARKET IN NORTH AMERICA, BY END USE AND COUNTRY

- 4.3 PRESSURE SENSOR MARKET, BY END USE

- 4.4 PRESSURE SENSOR MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Booming automotive sector

- 5.2.1.2 Rising adoption of microelectromechanical systems and miniaturization trends

- 5.2.1.3 Shift toward smart manufacturing due to Industry 4.0 evolution

- 5.2.1.4 Mounting demand for telemedicine, home healthcare, and wearable medical devices

- 5.2.2 RESTRAINTS

- 5.2.2.1 Need to adhere to stringent standards, regulations, and certifications

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Strong focus on enhancing functionality and user experience of consumer electronics

- 5.2.3.2 Rising implementation of IoT-enabled predictive maintenance programs

- 5.2.3.3 Rapid advances in AI and ML technologies

- 5.2.4 CHALLENGES

- 5.2.4.1 Shrinking profit margins with declining prices and increasing competition

- 5.2.1 DRIVERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 INVESTMENT AND FUNDING SCENARIO

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 PRICING ANALYSIS

- 5.7.1 PRICING RANGE OF ABSOLUTE PRESSURE SENSORS PROVIDED BY KEY PLAYERS, 2024

- 5.7.2 AVERAGE SELLING PRICE TREND OF PRESSURE SENSORS, BY END USE, 2021-2024

- 5.7.3 AVERAGE SELLING PRICE TREND OF PRESSURE SENSORS, BY REGION, 2021-2024

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Microelectromechanical systems (MEMS)

- 5.8.1.2 Piezoresistive sensors

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Wireless communication protocols

- 5.8.2.2 Advanced material innovations

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Internet of Things (IoT)

- 5.8.3.2 Sensor fusion

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PORTER'S FIVE FORCES ANALYSIS

- 5.9.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.9.2 BARGAINING POWER OF SUPPLIERS

- 5.9.3 BARGAINING POWER OF BUYERS

- 5.9.4 THREAT OF NEW ENTRANTS

- 5.9.5 THREAT OF SUBSTITUTES

- 5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.10.2 BUYING CRITERIA

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 ALTHEN SENSORS & CONTROLS ENHANCES DUTCH DELFT HYPERLOOP PROJECT WITH MINIATURE PRESSURE SENSORS

- 5.11.2 SURREY SENSORS LTD DEPLOYS HONEYWELL'S PRESSURE SENSORS TO ELEVATE PRECISION IN UAV AND AEROSPACE TESTING

- 5.11.3 MAJOR AGRICULTURAL MACHINERY COMPANY STARTS USING WIKA'S LEVEL SENSORS FOR MACHINE CONTROL

- 5.11.4 PRESSURE TRANSDUCER MONITORING ENABLES EMPTEEZY TO ENSURE CONSISTENT WATER FLOW IN EMERGENCY TANK SHOWERS

- 5.11.5 MEDICAL DEVICE COMPANY ADOPTS PRESSURE SENSOR FOR CRITICAL CARE BLOOD PRESSURE MONITORING

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT SCENARIO (HS CODE 902620)

- 5.12.2 EXPORT SCENARIO (HS CODE 902620)

- 5.13 TARIFF AND REGULATORY LANDSCAPE

- 5.13.1 TARIFF ANALYSIS

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.3 STANDARDS/REGULATIONS

- 5.14 PATENT ANALYSIS

- 5.15 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.16 IMPACT OF AI/GEN AI ON PRESSURE SENSOR MARKET

- 5.16.1 TOP AI/GEN AI USE CASES

- 5.16.1.1 Smart tire pressure monitoring systems (TPMS)

- 5.16.1.2 Respiratory monitoring in medical devices

- 5.16.1.3 Leak detection in water and gas pipelines

- 5.16.1.4 Aerospace cabin pressure and structural integrity monitoring

- 5.16.1.5 Smart fluid management in robotics and Industry 4.0

- 5.16.1 TOP AI/GEN AI USE CASES

- 5.17 IMPACT OF 2025 US TARIFF ON PRESSURE SENSOR MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRIES/REGIONS

- 5.17.4.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON END USES

6 PRESSURE SENSORS FOR DIFFERENT MEDIA TYPES

- 6.1 INTRODUCTION

- 6.2 AIR PRESSURE SENSORS

- 6.3 BAROMETRIC (ATMOSPHERIC) PRESSURE SENSORS

- 6.4 GAS PRESSURE SENSORS

- 6.5 WATER PRESSURE SENSORS

- 6.6 LIQUID PRESSURE SENSORS

- 6.7 PNEUMATIC & HYDRAULIC PRESSURE SENSORS

- 6.8 CORROSIVE LIQUID & GAS PRESSURE SENSORS

7 TECHNOLOGIES RELATED TO PRESSURE SENSORS

- 7.1 INTRODUCTION

- 7.2 MICROFABRICATION TECHNOLOGIES

- 7.2.1 MICROELECTROMECHANICAL SYSTEMS (MEMS)

- 7.2.2 COMPLEMENTARY METAL-OXIDE-SEMICONDUCTORS (CMOS)

- 7.3 AI SENSOR TECHNOLOGIES

- 7.3.1 MACHINE LEARNING (ML)

- 7.3.2 NATURAL LANGUAGE PROCESSING (NLP)

- 7.3.3 CONTEXT-AWARE COMPUTING

- 7.3.4 COMPUTER VISION

8 PRESSURE SENSOR MARKET, BY CONNECTIVITY

- 8.1 INTRODUCTION

- 8.2 WIRED

- 8.2.1 HIGH RELIABILITY AND ROBUSTNESS IN INDUSTRIAL APPLICATIONS TO DRIVE MARKET

- 8.3 WIRELESS

- 8.3.1 EASE OF DEPLOYMENT IN HARD-TO-REACH OR DYNAMIC ENVIRONMENTS TO BOOST DEMAND

9 PRESSURE SENSOR MARKET, BY SENSING METHOD

- 9.1 INTRODUCTION

- 9.2 PIEZORESISTIVE

- 9.2.1 HIGH RELIABILITY AND ACCURACY TO CONTRIBUTE TO SEGMENTAL GROWTH

- 9.3 CAPACITIVE

- 9.3.1 RISING USE IN ENERGY-EFFICIENT AND SMART DEVICES TO FUEL SEGMENTAL GROWTH

- 9.4 RESONANT SOLID-STATE

- 9.4.1 INCREASING DEMAND IN OIL & GAS INDUSTRY FOR PRECISE PRESSURE MEASUREMENTS TO AUGMENT SEGMENTAL GROWTH

- 9.5 ELECTROMAGNETIC

- 9.5.1 HIGH SUITABILITY IN EXTREME CONDITIONS ACROSS MULTIPLE INDUSTRIES TO EXPEDITE SEGMENTAL GROWTH

- 9.6 OPTICAL

- 9.6.1 INCREASING DEPLOYMENT IN MEDICAL APPLICATIONS TO ACCELERATE SEGMENTAL GROWTH

- 9.7 OTHER SENSING METHODS

10 PRESSURE SENSOR MARKET, BY SENSOR TYPE

- 10.1 INTRODUCTION

- 10.2 ABSOLUTE PRESSURE SENSORS

- 10.2.1 INCREASING NEED TO ACHIEVE PRECISE PRESSURE MEASUREMENTS RELATIVE TO PERFECT VACUUM TO FOSTER SEGMENTAL GROWTH

- 10.3 GAUGE PRESSURE SENSORS

- 10.3.1 GROWING USE IN INDUSTRIAL AUTOMATION AND PROCESS MONITORING APPLICATIONS TO DRIVE MARKET

- 10.4 DIFFERENTIAL PRESSURE SENSORS

- 10.4.1 INCREASING FOCUS OF INDUSTRY PLAYERS ON ENHANCING ENERGY EFFICIENCY AND ACHIEVING SUSTAINABILITY TO BOOST DEMAND

- 10.5 SEALED PRESSURE SENSORS

- 10.5.1 RISING ADOPTION IN EXTREME CONDITIONS TO AUGMENT SEGMENTAL GROWTH

- 10.6 VACUUM PRESSURE SENSORS

- 10.6.1 GROWING NEED FOR HIGH ACCURACY AND STABILITY VACUUM IN CHEMICAL PROCESSING TO FUEL SEGMENTAL GROWTH

11 PRESSURE SENSOR MARKET, BY PRESSURE RANGE

- 11.1 INTRODUCTION

- 11.2 UP TO 100 PSI

- 11.2.1 RISING INTEGRATION INTO PORTABLE AND WEARABLE DEVICES TO ACCELERATE SEGMENTAL GROWTH

- 11.3 101-1,000 PSI

- 11.3.1 INCREASING NEED FOR PRECISE PRESSURE CONTROL IN INDUSTRIAL PROCESSES TO BOOST SEGMENTAL GROWTH

- 11.4 ABOVE 1,000 PSI

- 11.4.1 GROWING DEMAND IN OIL & GAS AND MANUFACTURING SECTORS TO FOSTER SEGMENTAL GROWTH

12 PRESSURE SENSOR MARKET, BY END USE

- 12.1 INTRODUCTION

- 12.2 AUTOMOTIVE

- 12.2.1 INCREASING VEHICLE SALES DUE TO GOVERNMENT TAX BREAKS TO AUGMENT SEGMENTAL GROWTH

- 12.3 MEDICAL

- 12.3.1 RAPID INNOVATION IN MEDTECH ECOSYSTEM TO BOLSTER SEGMENTAL GROWTH

- 12.4 MANUFACTURING

- 12.4.1 GROWING ADOPTION OF AUTOMATION TECHNOLOGIES AND ROBOTICS TO FUEL SEGMENTAL GROWTH

- 12.5 UTILITIES

- 12.5.1 RAPID EXPANSION OF SMART GRID INFRASTRUCTURE TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.6 AVIATION

- 12.6.1 RISING FOCUS ON ENHANCING AIRCRAFT EFFICIENCY, SAFETY, AND PASSENGER COMFORT TO FUEL SEGMENTAL GROWTH

- 12.7 OIL & GAS

- 12.7.1 HIGH SAFETY REQUIREMENTS DUE TO EXPOSURE TO DYNAMIC ENVIRONMENT TO DRIVE DEMAND

- 12.8 MARINE

- 12.8.1 INCREASING NEED TO MONITOR WATER DEPTH AND OTHER CRUCIAL PARAMETERS TO BOOST SEGMENTAL GROWTH

- 12.9 CONSUMER DEVICES

- 12.9.1 RISING INSTALLATION OF PORTABLE DEVICES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.10 OTHER END USES

13 PRESSURE SENSOR MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 Rising development of microelectronics and printed sensor technology advancements to boost market growth

- 13.2.3 CANADA

- 13.2.3.1 Thriving automotive industry to contribute to market growth

- 13.2.4 MEXICO

- 13.2.4.1 Increasing production of vehicles, oil, and gas to foster market growth

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Increasing new vehicle registration and robust manufacturing base to drive market

- 13.3.3 UK

- 13.3.3.1 High investments in electric vehicles to support decarbonization goals to fuel market growth

- 13.3.4 FRANCE

- 13.3.4.1 Mounting production of commercial vehicles to contribute to market growth

- 13.3.5 ITALY

- 13.3.5.1 Thriving automotive and healthcare sectors to drive market

- 13.3.6 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 CHINA

- 13.4.2.1 Rapid industrialization and infrastructure development to boost market growth

- 13.4.3 JAPAN

- 13.4.3.1 Expanding process industries to contribute to market growth

- 13.4.4 INDIA

- 13.4.4.1 Mounting demand for consumer goods to augment market growth

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Booming consumer electronics industry to bolster market growth

- 13.4.6 REST OF ASIA PACIFIC

- 13.5 ROW

- 13.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 13.5.2 MIDDLE EAST

- 13.5.2.1 Bahrain

- 13.5.2.1.1 Industrial automation and infrastructure modernization to accelerate market growth

- 13.5.2.2 Kuwait

- 13.5.2.2.1 Strong commitment to diversifying economy and expanding renewable energy infrastructure to drive market

- 13.5.2.3 Oman

- 13.5.2.3.1 Rising emphasis on energy efficiency, industrial safety, and water resource management to fuel market growth

- 13.5.2.4 Qatar

- 13.5.2.4.1 Burgeoning demand for high-performance sensors for monitoring and control systems to boost market growth

- 13.5.2.5 Saudi Arabia

- 13.5.2.5.1 Robust industrial base and large-scale smart infrastructure projects to contribute to market growth

- 13.5.2.6 UAE

- 13.5.2.6.1 Increasing investment in smart cities to accelerate market growth

- 13.5.2.7 Rest of Middle East

- 13.5.2.1 Bahrain

- 13.5.3 AFRICA

- 13.5.3.1 Rising need to monitor and control critical processes to drive market

- 13.5.4 SOUTH AMERICA

- 13.5.4.1 Substantial growth in automobile production to bolster market growth

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY STRENGTHS/RIGHT TO WIN, 2021-2025

- 14.3 MARKET SHARE ANALYSIS, 2024

- 14.4 REVENUE ANALYSIS, 2020-2024

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Connectivity footprint

- 14.6.5.4 Sensing method footprint

- 14.6.5.5 Sensor type footprint

- 14.6.5.6 Pressure range footprint

- 14.6.5.7 End use footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPETITIVE SCENARIO

- 14.8.1 PRODUCT LAUNCHES

- 14.8.2 DEALS

- 14.8.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 HONEYWELL INTERNATIONAL INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths/Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses/Competitive threats

- 15.1.2 TE CONNECTIVITY

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths/Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses/Competitive threats

- 15.1.3 SENSATA TECHNOLOGIES, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths/Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses/Competitive threats

- 15.1.4 EMERSON ELECTRIC CO.

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths/Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses/Competitive threats

- 15.1.5 AMPHENOL CORPORATION

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths/Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses/Competitive threats

- 15.1.6 ABB

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.6.3.3 Expansions

- 15.1.7 TT ELECTRONICS

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Expansions

- 15.1.8 ROCKWELL AUTOMATION

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.9 SCHNEIDER ELECTRIC

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.10 SIEMENS

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.11 STMICROELECTRONICS

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches

- 15.1.12 INFINEON TECHNOLOGIES AG

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches

- 15.1.12.3.2 Deals

- 15.1.12.3.3 Expansions

- 15.1.13 NXP SEMICONDUCTORS

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.14 YOKOGAWA ELECTRIC CORPORATION

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.15 ENDRESS+HAUSER GROUP SERVICES AG

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Expansions

- 15.1.1 HONEYWELL INTERNATIONAL INC.

- 15.2 OTHER PLAYERS

- 15.2.1 BOSCH SENSORTEC GMBH

- 15.2.2 IFM ELECTRONIC GMBH

- 15.2.3 JUMO GMBH & CO. KG

- 15.2.4 KITA SENSOR TECH. CO., LTD.

- 15.2.5 NIDEC CORPORATION

- 15.2.6 PHOENIX SENSORS

- 15.2.7 MICRO SENSOR CO., LTD

- 15.2.8 BD|SENSORS GMBH

- 15.2.9 KISTLER GROUP

- 15.2.10 OMEGA ENGINEERING INC.

16 APPENDIX

- 16.1 INSIGHTS FROM INDUSTRY EXPERTS

- 16.2 DISCUSSION GUIDE

- 16.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.4 CUSTOMIZATION OPTIONS

- 16.5 RELATED REPORTS

- 16.6 AUTHOR DETAILS