|

시장보고서

상품코드

1915211

ADAS 시뮬레이션 시장 : 시뮬레이션 유형별, 차종별, 제공별, 방법별, 자율성 레벨별, 용도별, 최종사용자별, 지역별 - 세계 예측(-2032년)ADAS Simulation Market by Method (On-Premises, Cloud-Based), Offering (Software, Services), Simulation Type (MIL, DIL, SIL, HIL), Vehicle Type (Passenger Cars, Commercial Vehicles), LoA, Application, End-users & Region - Global Forecast to 2032 |

||||||

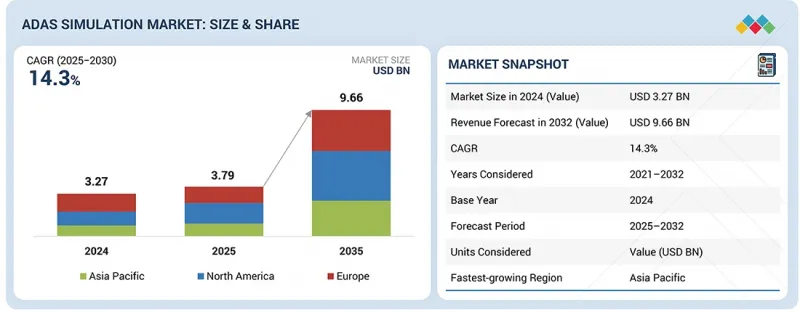

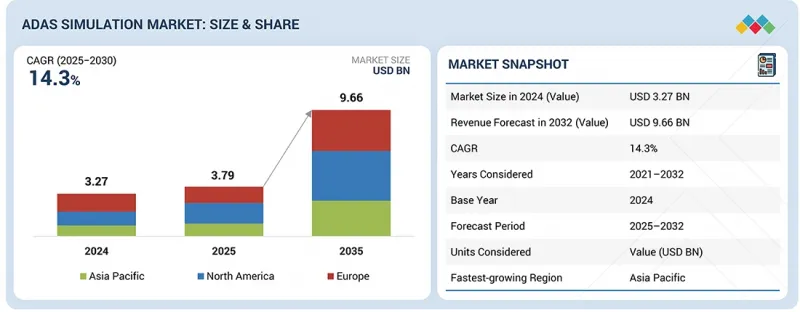

ADAS 시뮬레이션 시장 규모는 2025년 37억 9,000만 달러에서 CAGR 14.3%로 성장하여 2032년까지 약 96억 6,000만 달러에 달할 것으로 예측됩니다. 이러한 성장의 대부분은 자동차 산업의 급속한 변화에 기인합니다. 자동차 제조업체들은 모든 시스템을 실제 도로에서 테스트하는 것보다 안전하고 신속하며 비용 효율적이기 때문에 시뮬레이션에 의존하고 있습니다. 엔지니어들은 차량이 실험실을 떠나기 전에 센서, 카메라, 차량용 컴퓨터가 다양한 도로 상황과 기상 조건에 어떻게 반응하는지 연구할 수 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 대상 단위 | 가치(100만/10억 달러) |

| 부문 | 시뮬레이션 유형별, 차종별, 제공별, 방법별, 자율성 레벨별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 아시아태평양, 유럽, 북미 |

주요 공급업체들은 이러한 설정을 HIL, SIL, 클라우드 툴과 연동하여 어댑티브 크루즈, 브레이크, 차선유지 시스템의 조기 개선이 가능하도록 하고 있습니다. 3D 모델과 AI 생성 주행 장면의 활용으로 가상 테스트의 리얼리티가 크게 향상되었습니다. 안전 규제 강화, 생산주기 단축, 전기자동차의 급속한 보급에 따라 시뮬레이션은 조용히 차량 설계의 일상 업무의 일부가 되어 완전 자율주행을 실현하기 위한 중요한 단계가 되고 있습니다.

시뮬레이션 유형별로는 MiL(Model in the Loop) 부문이 예측 기간 동안 ADAS 시뮬레이션 시장을 주도할 것으로 예상됩니다. 이는 개발 사이클의 초기 단계에서 제어 알고리즘을 평가하고, 다운스트림 공정의 통합 리스크를 줄여야 할 필요성이 높아졌기 때문입니다. 자동차 제조업체들이 하드웨어가 준비될 때까지 기다리지 않고 제어 알고리즘을 조기에 테스트하려고 하는 가운데, 이 방법의 가치는 점점 더 커지고 있습니다. 이를 통해 공정 후반부의 고비용 설계 변경을 피할 수 있습니다. 엔지니어는 물리적 구성요소를 구축하기 전에 지각, 계획 및 제어 모델이 어떻게 상호 작용하는지 테스트 할 수 있습니다. 도요타, 현대, BMW, 포드 등의 자동차 제조사들은 현재 초기 설계 단계에서 센서 융합과 의사결정 로직을 조정하기 위해 MIL 환경을 활용하고 있습니다. 이러한 테스트를 가상 환경에서 실행함으로써 완전한 프로토타입 없이도 다양한 도로 상황, 날씨, 교통 상황에서의 시스템 거동을 확인할 수 있습니다. 자동차가 소프트웨어 중심이 되고 잦은 무선 업데이트에 의존하게 되면서 조기 테스트는 필수적인 단계로 바뀌었습니다. 지멘스, 앤시스, dSPACE와 같은 시뮬레이션 기업들은 더 나은 모델 라이브러리와 SIL(Software in the Loop) 및 HIL(Hardware in the Loop)과의 원활한 연계를 통해 툴을 강화하고, 제조업체가 더 빠르게 검증하고 개발 리스크를 줄일 수 있도록 지원하고 있습니다. 개발 리스크를 줄일 수 있도록 지원하고 있습니다.

자율주행 수준별로는 레벨 4와 레벨 5 부문이 예측 기간 동안 ADAS 시뮬레이션 시장에서 가장 높은 성장세를 보일 것으로 예상됩니다. 이러한 성장은 인간의 개입 없이 안전하게 작동해야 하는 고도로 복잡한 완전 자동화 시스템에 기인합니다. 자동차 제조업체와 기술 개발자들은 실제 도로에서 재현할 수 없거나 위험한 수백만 가지의 주행 상황을 테스트하기 위해 고도의 시뮬레이션을 활용하고 있습니다. 웨이모, 크루즈, 바이두 아폴로, 현대모비스 등의 기업들과 지멘스, 앤시스, dSPACE, AVL 등 시뮬레이션 분야의 선도 기업들은 센서 융합, 경로 계획, AI 기반 인지 시스템 검증을 위한 대규모 가상 환경을 구축하고 있습니다. 구축하고 있습니다. 이 플랫폼을 통해 엔지니어들은 통제된 디지털 환경에서 차량이 극한의 기상 조건, 센서 고장, 예측할 수 없는 교통 상황에 어떻게 대응하는지를 연구할 수 있습니다. 규제 당국의 안전 기준이 강화되고 업계가 소프트웨어 정의 모빌리티로 전환함에 따라, 시뮬레이션은 완전 자율주행차의 신뢰성을 검증하고 실세계 도입을 가속화하기 위해 점점 더 필수적인 요소가 되고 있습니다.

차량 유형별로는 상용차 부문이 예측 기간 동안 승용차 부문보다 높은 성장률을 보일 것으로 예상됩니다. 이러한 변화는 보다 안전하고 효율적인 차량군을 필요로 하는 물류 및 운송 기업들이 주도하고 있습니다. 트럭과 버스는 승용차보다 장거리 주행, 중량물 운송, 엄격한 안전 목표에 직면하기 때문에 시뮬레이션은 실제 테스트 비용과 위험 없이 시스템을 테스트할 수 있는 실용적인 수단이 되고 있습니다. Volvo Trucks, Daimler, Scania, Tata Motors, BYD 등의 제조사들은 이미 자율주행, 충돌방지, 주차 및 도킹 지원 시스템 개발에 이러한 툴을 활용하고 있습니다. 가상 테스트를 통해 엔지니어는 실제 도로에 차량을 투입하기 전에 교통 체증, 급커브, 날씨 변화 등 다양한 상황에서의 차량 거동을 확인할 수 있습니다. E-Commerce의 확대와 교통 안전 규제가 강화됨에 따라 많은 기업들이 디지털 테스트 플랫폼으로 전환하고 있습니다. 또한, 지멘스, 앤시스, dSPACE와 같은 시뮬레이션 분야의 선도 기업들은 대형 차량 및 AI 기반 운전 로직에 대응할 수 있도록 시스템을 업데이트하여 차량군의 자동화를 가속화할 수 있도록 지원하고 있습니다.

ADAS 시뮬레이션 시장은 Siemens(독일), Ansys, Inc.(미국), NVIDIA Corporation(미국), dSPACE(독일), AVL(오스트리아) 등 주요 기업들이 주도하고 있습니다. 이들 기업은 ADAS 시뮬레이션 시장에서의 입지를 강화하기 위해 포트폴리오를 확장하고 있습니다.

주요 시장 진입업체에 대한 상세한 경쟁 분석, 기업 프로파일, 제품 및 사업 제공에 대한 주요 관찰 사항, 최근 동향, 주요 시장 전략 등을 조사했습니다.

본 보고서 구매의 주요 이점:

- 이 보고서는 ADAS 시뮬레이션 시장과 그 하위 부문의 수익 규모에 대한 가장 정확한 추정치를 시장 리더와 신규 진입자에게 제공합니다.

- 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립하는 데 필요한 인사이트를 얻을 수 있도록 돕습니다.

- 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제, 기회에 대한 정보를 제공합니다.

- 본 보고서는 방법, 최종사용자, 애플리케이션, 시뮬레이션 유형, 시뮬레이션 유형, 자율성 수준, 차량 유형, 제공 내용, 지역별 ADAS 시뮬레이션 시장의 다양한 동향에 대한 정보를 시장 선도업체와 신규 진입업체에 제공합니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 시장 역학의 영향 분석

- 미충족 수요와 공백

- 상호 접속된 시장과 분야 횡단적인 기회

- 상호 접속된 시장

- 크로스 부문 기회

- 티어1/2/3 진출 기업의 전략적 활동

제5장 업계 동향

- 거시경제 지표

- 생태계 분석

- 공급망 분석

- 고객 비즈니스에 영향을 미치는 동향과 혼란

- 투자와 자금 조달 시나리오

- 주요 회의와 이벤트

- 사례 연구 분석

- 주요 ADAS 시뮬레이션 시장 센터

- 주요 자동차 제조업체별 ADAS의 제공

- 향후 모델과 ADAS 기능

- 향후 ADAS 소프트웨어와 시뮬레이션 개발

- 안전하고 확장가능한 자동화를 위한 ADAS 테스트

- 향후 성장에 대한 베팅

- 시뮬레이션 플랫폼의 비용 효율과 ROI 모델

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

- 주요 기술

- 보완적 기술

- 인접 기술

- 기술 로드맵

- 특허 분석

- AI/생성형 AI의 영향

제7장 고객 상황과 구매 행동

- 의사결정 프로세스

- 구매자 이해관계자와 구입 평가 기준

- 채용 장벽과 내부 과제

제8장 지속가능성과 규제 상황

- 지역 규제와 컴플라이언스

- 규제기관, 정부기관, 기타 조직

- 업계 표준

- 지속가능성에 대한 대처

- 탄소의 영향과 에코 애플리케이션

- 지속가능성에 대한 영향과 규제 정책의 대처

- 인증, 라벨, 환경기준

제9장 ADAS 시뮬레이션 시장(시뮬레이션 유형별)

- 모델 인 더 루프

- 소프트웨어 인 더 루프

- 하드웨어 인 더 루프

- 드라이버 인 더 루프

- 주요 인사이트

제10장 ADAS 시뮬레이션 시장(차종별)

- 승용차

- 상용차

- 주요 인사이트

제11장 ADAS 시뮬레이션 시장(제공별)

- 소프트웨어

- 서비스

- 주요 인사이트

제12장 ADAS 시뮬레이션 시장(방법별)

- 온프레미스

- 클라우드 기반

- 주요 인사이트

제13장 ADAS 시뮬레이션 시장(자율성 레벨별)

- 레벨 1

- 레벨2/2 이상

- 레벨 3

- 레벨4/5

- 주요 인사이트

제14장 ADAS 시뮬레이션 시장(용도별)

- 자동 긴급 제동

- 어댑티브 크루즈 컨트롤

- 차선 이탈 경보와 차선 유지 보조

- 교통 표지 인식

- 사각지대감지

- 주차 보조

- 자동 주차 어시스트

- 기타

- 주요 인사이트

제15장 ADAS 시뮬레이션 시장(최종사용자별)

- OEM

- 티어1/2 부품 제조업체

- 테크놀러지 프로바이더/소프트웨어 개발자

- 주요 인사이트

제16장 ADAS 시뮬레이션 시장(지역별)

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 유럽

- 프랑스

- 이탈리아

- 독일

- 스페인

- 영국

- 북미

- 미국

- 캐나다

제17장 경쟁 구도

- 개요

- 주요 진출 기업의 전략/강점, 2022-2025년

- 시장 점유율 분석, 2025년

- 매출 분석, 2020-2024년

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 진출 기업, 2025년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2025년

- 경쟁 시나리오

제18장 기업 개요

- 주요 진출 기업

- SIEMENS

- ANSYS, INC.

- NVIDIA CORPORATION

- DSPACE

- AVL

- APPLIED INTUITION, INC.

- IPG AUTOMOTIVE GMBH

- MATHWORKS, INC.

- HEXAGON AB

- VECTOR INFORMATIK GMBH

- KEYSIGHT TECHNOLOGIES

- DASSAULT SYSTEMES

- COGNATA

- 기타 기업

- RFPRO

- FORETELLIX

- ELEKTROBIT

- ETAS

- VI-GRADE GMBH

- AVSIMULATION

- ANTEMOTION

- PARALLEL DOMAIN

- REAL-TIME TECHNOLOGIES

- AIMOTIVE

- ANYVERSE SL

- DORLECO

제19장 조사 방법

제20장 부록

KSM 26.02.05The ADAS simulation market is projected to reach around USD 9.66 billion by 2032, growing from USD 3.79 billion in 2025 at a CAGR of 14.3%. Much of this growth stems from the rapid pace of change in the auto industry. Carmakers are relying on simulation because it's safer, faster, and cheaper than testing every system on real roads. Engineers can study how sensors, cameras, and onboard computers react to different road and weather conditions before a car ever leaves the lab.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Method, Simulation Type, Level of Autonomy, Vehicle Type, Offering, Application, and End User |

| Regions covered | Asia Pacific, Europe, North America |

Major suppliers are linking these setups with HIL, SIL, and cloud tools, enabling the refinement of adaptive cruise, braking, and lane-keeping systems early on. The use of 3D models and AI-generated driving scenes is making virtual testing feel far more realistic. With stricter safety rules, shorter production cycles, and the rapid rise of electric cars, simulation has quietly become a daily part of vehicle design and a major step toward full autonomy.

"The model-in-the-Loop (MiL) segment is projected to lead the ADAS simulation market over the forecast period."

By simulation type, the model-in-the-Loop (MiL) segment is projected to lead the ADAS simulation market over the forecast period, driven by the growing need to evaluate control algorithms early in the development cycle and reduce downstream integration risks. The approach is becoming increasingly valuable as carmakers strive to test control algorithms early, rather than waiting until the hardware is ready. Doing this helps avoid expensive redesigns later in the process. Engineers can test how perception, planning, and control models interact before any physical components are built. Automakers, such as Toyota, Hyundai, BMW, and Ford, are now using MIL setups to adjust sensor fusion and decision-making logic during the first design stages. Running these tests virtually also lets teams see how systems behave in different road, weather, or traffic conditions without needing full prototypes. As cars become software-driven and depend on frequent over-the-air updates, early testing has turned into a must-have step. Simulation firms like Siemens, Ansys, and dSPACE are upgrading their tools with better model libraries and smoother links to SIL and HIL, helping manufacturers validate faster and lower development risk.

"The level 4 & 5 segment is projected to witness the highest growth in the ADAS simulation market over the forecast period."

By level of autonomy, the level 4 & 5 segment is projected to experience the highest growth in the ADAS simulation market over the forecast period. This growth comes due to a highly complex system of fully automated systems that must operate safely without human input. Automakers and tech developers are using advanced simulation to test millions of driving situations that would be impossible or unsafe to recreate on real roads. Companies like Waymo, Cruise, Baidu Apollo, and Hyundai Mobis, along with simulation leaders such as Siemens, Ansys, dSPACE, and AVL, are building large-scale virtual environments to validate sensor fusion, path planning, and AI-based perception systems. This platform helps engineers to study how vehicles respond to extreme weather, sensor faults, or unpredictable traffic in a controlled digital setup. With regulators tightening safety rules and the industry moving toward software-defined mobility, simulation is becoming increasingly essential for verifying the reliability of fully autonomous vehicles and accelerating their deployment in the real world.

"The commercial vehicles segment is projected to achieve higher growth than the passenger cars segment during the forecast period."

By vehicle type, the commercial vehicles segment is projected to register higher growth than the passenger cars segment during the forecast period. The shift is being led by logistics and transport firms that need safer, more efficient fleets. Trucks and buses face longer routes, heavier loads, and more challenging safety targets than cars; thus, simulation has become a practical way to test systems without the cost and risk of real-world trials. Manufacturers such as Volvo Trucks, Daimler, Scania, Tata Motors, and BYD are already utilizing these tools to develop automated driving, collision avoidance, and parking or docking assistance systems. By running virtual tests, engineers can check how vehicles behave in heavy traffic, tight turns, or changing weather before sending them on actual roads. With e-commerce expanding and transport safety rules tightening, many companies are shifting to digital testing platforms. Additionally, simulation leaders like Siemens, Ansys, and dSPACE are updating their systems to handle large vehicles and AI-based driving logic, helping fleets move faster toward automation.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: MNCs - 70 %, Tier-1 Companies- 20%, and Startups - 10%

- By Designation: C-level - 45%, Director-Level - 30%, and Others - 25%

- By Region: Asia Pacific - 35%, North America - 40%, and Europe - 25%

The ADAS simulation market is dominated by major players, including Siemens (Germany), Ansys, Inc. (US), NVIDIA Corporation (US), dSPACE (Germany), AVL (Austria), and more. These companies are expanding their portfolios to strengthen their position in the ADAS Simulation market.

Research Coverage:

The report covers the ADAS simulation market by method (on-premises simulation, cloud-based simulation), simulation type (model-in-the-loop, software-in-the-loop, hardware-in-the-loop, driver-in-the-loop), level of autonomy (level 1, level 2/2+, level 3, level 4 & 5 ), vehicle type (passenger cars, commercial vehicles), offering (software, services), application (autonomous emergency braking, adaptive cruise control, lane departure warning (LDW) & lane keeping assist (LKA), traffic sign recognition (TSR), blind spot detection (BSD), parking assistance, automated parking assist, others), end user (OEMs, tier 1/tier 2 component manufacturers, technology providers/software developers), and region. The report also covers the competitive landscape and company profiles of the significant ADAS simulation market players.

The study includes an in-depth competitive analysis of the key market players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the ADAS Simulation market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

- The report will help market leaders/new entrants with information on various trends in the ADAS simulation market based on method, end user, application, simulation type, level of autonomy, vehicle type, offering, and region.

The report provides insight into the following points:

- Analysis of key drivers (Shift from hardware-based validation to virtual development, growing system complexity and calibration, increasing ADAS adoption for higher vehicle automation, rising government safety mandates), restraints (Mismatch between simulation conditions and real-world environments, human behavioral variability, system failure complexity), opportunities (Advancements in autonomous vehicle technology, unlocking strategic control and deep customization through in-house ADAS simulation development, leveraging digital twins to accelerate ADAS validation and reduce cycles), and challenges (Integrating real-world and synthetic data at scale, regulatory & homologation acceptance of simulation)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the ADAS simulation market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about products & services, untapped geographies, recent developments, and investments in the ADAS simulation market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players like Siemens (Germany), Ansys, Inc. (US), NVIDIA Corporation (US), dSPACE (Germany), AVL (Austria), among others, in the ADAS simulation market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ADAS SIMULATION MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ADAS SIMULATION MARKET

- 3.2 ADAS SIMULATION MARKET, BY VEHICLE TYPE

- 3.3 ADAS SIMULATION MARKET, BY METHOD

- 3.4 ADAS SIMULATION MARKET, BY OFFERING

- 3.5 ADAS SIMULATION MARKET, BY LEVEL OF AUTONOMY

- 3.6 ADAS SIMULATION MARKET, BY SIMULATION TYPE

- 3.7 ADAS SIMULATION MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Shift from hardware-based validation to virtual development

- 4.2.1.2 Growing system complexity and calibration demands

- 4.2.1.3 Increasing ADAS penetration

- 4.2.1.4 Rising government safety mandates

- 4.2.2 RESTRAINTS

- 4.2.2.1 Gap between simulated scenarios and real-world driving complexity

- 4.2.2.2 Human behavioral variability and system failure complexity

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Advancements in autonomous vehicle technology

- 4.2.3.2 Unlocking strategic control and deep customization through in-house ADAS simulation development

- 4.2.3.3 Integration of digital twin technology

- 4.2.4 CHALLENGES

- 4.2.4.1 Combining real-world and synthetic data at scale

- 4.2.4.2 Regulatory and homologation acceptance of simulation

- 4.2.5 IMPACT ANALYSIS OF MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL ADAS SIMULATION INDUSTRY

- 5.1.4 TRENDS IN GLOBAL AUTOMOTIVE AND TRANSPORTATION INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 ENVIRONMENT AND SCENARIO CONTENT PROVIDERS

- 5.2.2 SIMULATION PLATFORM PROVIDERS

- 5.2.3 SENSOR AND PHYSICS MODEL PROVIDERS

- 5.2.4 HARDWARE-IN-THE-LOOP/SOFTWARE-IN-THE-LOOP/MODEL-IN-THE-LOOP HARDWARE AND INTEGRATION PROVIDERS

- 5.2.5 DATA INFRASTRUCTURE AND HD MAPPING PROVIDERS

- 5.2.6 TIER-1 SYSTEM INTEGRATORS

- 5.2.7 OEMS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.5 INVESTMENT AND FUNDING SCENARIO

- 5.6 KEY CONFERENCES AND EVENTS

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 RIDEFLUX ACCELERATES LEVEL 4 AUTONOMY WITH APPLIED INTUITION'S SCALABLE SIMULATION AND DATA MANAGEMENT PLATFORM

- 5.7.2 MERCEDES-BENZ ACCELERATES LEVEL 3 ADAS CERTIFICATION WITH ANSYS OPTISLANG'S ADVANCED RELIABILITY SIMULATION FRAMEWORK

- 5.7.3 TUV SUD VALIDATES ADSCENE'S SCENARIO DATABASE TO STRENGTHEN GLOBAL-STANDARD COMPLIANCE FOR ADAS SAFETY CERTIFICATION

- 5.7.4 TOYOTA ACCELERATES ADAS SAFETY VALIDATION WITH DSPACE'S REAL-TO-VIRTUAL SCENARIO GENERATION AND VEHICLE-IN-THE-LOOP SIMULATION

- 5.7.5 AUTOMATED ADAS/AD VALIDATION ACHIEVED THROUGH INTEGRATED SCENARIO SIMULATION, RADAR EMULATION, AND PROBABILISTIC SAFETY ANALYSIS

- 5.7.6 BOSCH ACCELERATES ADAS DEVELOPMENT WITH UNREAL ENGINE-DRIVEN SOFTWARE-IN-THE-LOOP RADAR AND ACC SIMULATION

- 5.7.7 MOBILEDRIVE ACCELERATES ADAS DEVELOPMENT WITH SIEMENS' MBSE-DRIVEN DIGITAL TWIN AND SIMULATION-BASED VALIDATION FRAMEWORK

- 5.7.8 FORMEL D ENSURES SAFE AND COMPLIANT ADAS/AD DEPLOYMENT THROUGH COMPREHENSIVE SIMULATION AND REAL-WORLD TESTING SERVICES

- 5.8 MAJOR ADAS SIMULATION MARKET CENTERS

- 5.9 ADAS OFFERINGS BY KEY AUTOMAKERS

- 5.9.1 MODEL-WISE ADAS OFFERINGS

- 5.9.1.1 Tesla

- 5.9.1.2 Toyota Motor Corporation

- 5.9.1.2.1 Corolla

- 5.9.1.2.2 Camry

- 5.9.1.2.3 RAV4

- 5.9.1.3 Nissan Motor Co., Ltd.

- 5.9.1.3.1 Versa

- 5.9.1.3.2 Altima

- 5.9.1.3.3 Nissan Leaf

- 5.9.1.3.4 Nissan TITAN

- 5.9.1.4 Mercedes-Benz AG

- 5.9.1.4.1 S-Class Sedan

- 5.9.1.4.2 C-Class Sedan

- 5.9.1.4.3 E-Class Sedan

- 5.9.1.5 Audi

- 5.9.1.5.1 A3 Sedan

- 5.9.1.5.2 A6 Sedan

- 5.9.1.6 Cadillac

- 5.9.1.6.1 Cadillac XT6

- 5.9.1.6.2 Cadillac XT4

- 5.9.1 MODEL-WISE ADAS OFFERINGS

- 5.10 UPCOMING MODELS AND ADAS FEATURES

- 5.11 UPCOMING ADAS SOFTWARE AND SIMULATION DEVELOPMENTS

- 5.11.1 ADVENT OF CLOUD-NATIVE SIMULATION

- 5.11.2 ADOPTION OF VIRTUAL VALIDATION IN REGULATORY FRAMEWORKS

- 5.11.3 ADAS PENETRATION IN MASS-MARKET VEHICLES

- 5.11.4 RISE OF EDGE-BASED ON-VEHICLE SIMULATION

- 5.11.5 EVOLUTION OF HIGH-FIDELITY SENSOR SIMULATION

- 5.11.6 AI-DRIVEN SCENARIO GENERATION

- 5.12 ADAS TESTING FOR SAFE AND SCALABLE AUTOMATION

- 5.13 FUTURE GROWTH BETS

- 5.13.1 EMERGENCE OF ADAS TESTING-AS-A-SERVICE BUSINESS MODELS

- 5.13.2 LEVEL 4/5 TESTING FOR ROBO-TAXIS AND DELIVERY PODS

- 5.13.3 REGIONAL HOTSPOTS FOR ADAS SIMULATION AND TESTING

- 5.13.3.1 China's Smart City Pilots

- 5.13.3.2 US Highway Automation Tests

- 5.13.3.3 EU Safety Mandates

- 5.14 COST EFFICIENCY AND ROI MODELS IN SIMULATION PLATFORMS

- 5.14.1 LIMITATIONS OF TRADITIONAL PHYSICAL (CAPEX-HEAVY) TESTING

- 5.14.2 TRANSITION TOWARD VIRTUAL (OPEX-DRIVEN) TESTING

- 5.14.3 OPERATIONAL AND FINANCIAL BENEFITS OF OPEX MODEL

- 5.14.4 ROI MODELS FOR OEMS AND TIER-1 SUPPLIERS ADOPTING LARGE-SCALE SIMULATION PLATFORMS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 AI/ML PERCEPTION TESTING

- 6.1.2 SCENARIO-BASED TESTING

- 6.1.3 SENSOR-BASED TESTING

- 6.1.4 MULTI-SENSOR ENVIRONMENTS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 EDGE/CLOUD PLATFORMS

- 6.2.2 HIGH-BANDWIDTH DATA LOGGERS

- 6.2.3 HD AND SEMANTIC MAPS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 RADAR EMULATION

- 6.3.2 AD/ADAS TESTING FOR TELEMATICS AND V2X

- 6.3.3 AUTOMATED TESTING FOR SENSOR DATA ACQUISITION

- 6.4 TECHNOLOGY ROADMAP

- 6.4.1 SHORT-TERM (2026-2027)

- 6.4.2 MID-TERM (2028-2030)

- 6.4.3 LONG-TERM (BEYOND 2030)

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI/GEN AI

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.4.1 Sensor-simulation integration

- 6.6.4.2 Tier-1 and simulation co-development

- 6.6.4.3 OEM-software alliances

- 6.6.4.4 Compute and cloud partnerships

- 6.6.4.5 Mapping and virtual environments

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED ADAS SIMULATION

7 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 CARBON IMPACT AND ECO-APPLICATIONS

- 8.2.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 8.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

9 ADAS SIMULATION MARKET, BY SIMULATION TYPE

- 9.1 INTRODUCTION

- 9.2 MODEL-IN-THE-LOOP

- 9.2.1 HIGH FIDELITY MODEL VALIDATION TO DRIVE MARKET

- 9.3 SOFTWARE-IN-THE-LOOP

- 9.3.1 COMPLIANCE WITH FUNCTIONAL SAFETY EXPECTATIONS UNDER ISO STANDARDS TO DRIVE MARKET

- 9.4 HARDWARE-IN-THE-LOOP

- 9.4.1 ADVANCEMENTS IN MULTI-SENSOR HIL ARCHITECTURES TO DRIVE MARKET

- 9.5 DRIVER-IN-THE-LOOP

- 9.5.1 NEED FOR HUMAN-CENTRIC VALIDATION TO DRIVE MARKET

- 9.6 PRIMARY INSIGHTS

10 ADAS SIMULATION MARKET, BY VEHICLE TYPE

- 10.1 INTRODUCTION

- 10.2 PASSENGER CARS

- 10.2.1 RISE IN SOFTWARE AND SENSOR FUSION COMPLEXITY TO DRIVE MARKET

- 10.3 COMMERCIAL VEHICLES

- 10.3.1 HIGHER OPERATIONAL RISKS TO DRIVE MARKET

- 10.4 PRIMARY INSIGHTS

11 ADAS SIMULATION MARKET, BY OFFERING

- 11.1 INTRODUCTION

- 11.2 SOFTWARE

- 11.2.1 PRESSURE TO SHORTEN DEVELOPMENT CYCLES TO DRIVE MARKET

- 11.2.2 APPLICATION SOFTWARE

- 11.2.3 MIDDLEWARE

- 11.2.4 OPERATING SYSTEMS/PLATFORMS

- 11.3 SERVICES

- 11.3.1 NEED FOR CONSISTENT DATA FLOW AND INTEROPERABILITY TO DRIVE MARKET

- 11.3.2 SIMULATION PLATFORMS

- 11.3.3 VALIDATION SERVICES

- 11.3.4 SUPPORT & MAINTENANCE SERVICES

- 11.4 PRIMARY INSIGHTS

12 ADAS SIMULATION MARKET, BY METHOD

- 12.1 INTRODUCTION

- 12.2 ON-PREMISES

- 12.2.1 NEED FOR DETERMINISTIC HARDWARE VALIDATION AND DATA CONTROL TO DRIVE MARKET

- 12.3 CLOUD-BASED

- 12.3.1 EXTENSIVE USE IN LARGE-SCALE VALIDATION AND REGRESSION TESTING TO DRIVE MARKET

- 12.4 PRIMARY INSIGHTS

13 ADAS SIMULATION MARKET, BY LEVEL OF AUTONOMY

- 13.1 INTRODUCTION

- 13.2 LEVEL 1

- 13.2.1 REGULATORY COMPLIANCE FOR ENTRY-LEVEL SAFETY FEATURES TO DRIVE MARKET

- 13.3 LEVEL 2/2+

- 13.3.1 EXPANDED SAFETY VALIDATION REQUIREMENTS TO DRIVE MARKET

- 13.4 LEVEL 3

- 13.4.1 HIGH VALIDATION COMPLEXITY FOR CONDITIONAL AUTOMATION TO DRIVE MARKET

- 13.5 LEVEL 4/5

- 13.5.1 NEED TO VALIDATE LARGE-SCALE, LONG-TAIL DRIVING SCENARIOS WHILE MINIMIZING ON-ROAD TESTING RISK AND COST TO DRIVE MARKET

- 13.6 PRIMARY INSIGHTS

14 ADAS SIMULATION MARKET, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 AUTONOMOUS EMERGENCY BRAKING

- 14.3 ADAPTIVE CRUISE CONTROL

- 14.4 LANE DEPARTURE WARNING & LANE KEEPING ASSIST

- 14.5 TRAFFIC SIGN RECOGNITION

- 14.6 BLIND SPOT DETECTION

- 14.7 PARKING ASSISTANCE

- 14.8 AUTOMATED PARKING ASSIST

- 14.9 OTHERS

- 14.10 PRIMARY INSIGHTS

15 ADAS SIMULATION MARKET, BY END USER

- 15.1 INTRODUCTION

- 15.2 OEMS

- 15.3 TIER-1/2 COMPONENT MANUFACTURERS

- 15.4 TECHNOLOGY PROVIDERS/SOFTWARE DEVELOPERS

- 15.5 PRIMARY INSIGHTS

16 ADAS SIMULATION MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 ASIA PACIFIC

- 16.2.1 CHINA

- 16.2.2 INDIA

- 16.2.3 JAPAN

- 16.2.4 SOUTH KOREA

- 16.3 EUROPE

- 16.3.1 FRANCE

- 16.3.2 ITALY

- 16.3.3 GERMANY

- 16.3.4 SPAIN

- 16.3.5 UK

- 16.4 NORTH AMERICA

- 16.4.1 US

- 16.4.2 CANADA

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 17.3 MARKET SHARE ANALYSIS, 2025

- 17.4 REVENUE ANALYSIS, 2020-2024

- 17.5 COMPANY VALUATION AND FINANCIAL METRICS

- 17.6 BRAND/PRODUCT COMPARISON

- 17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT

- 17.7.5.1 Company footprint

- 17.7.5.2 Region footprint

- 17.7.5.3 Application footprint

- 17.7.5.4 Vehicle type footprint

- 17.7.5.5 Offering footprint

- 17.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.8.5 COMPETITIVE BENCHMARKING

- 17.8.5.1 List of start-ups/SMEs

- 17.8.5.2 Competitive benchmarking of start-ups/SMEs

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 17.9.2 DEALS

- 17.9.3 OTHER DEVELOPMENTS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 SIEMENS

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches/developments

- 18.1.1.3.2 Deals

- 18.1.1.3.3 Other developments

- 18.1.1.4 MnM view

- 18.1.1.4.1 Right to win

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 ANSYS, INC.

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches/developments

- 18.1.2.3.2 Deals

- 18.1.2.3.3 Other developments

- 18.1.2.4 MnM view

- 18.1.2.4.1 Right to win

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 NVIDIA CORPORATION

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Product launches/developments

- 18.1.3.3.2 Deals

- 18.1.3.3.3 Other developments

- 18.1.3.4 MnM view

- 18.1.3.4.1 Right to win

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 DSPACE

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches/developments

- 18.1.4.3.2 Deals

- 18.1.4.3.3 Other developments

- 18.1.4.4 MnM view

- 18.1.4.4.1 Right to win

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 AVL

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches/developments

- 18.1.5.3.2 Deals

- 18.1.5.3.3 Other developments

- 18.1.5.4 MnM view

- 18.1.5.4.1 Right to win

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 APPLIED INTUITION, INC.

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches/developments

- 18.1.6.3.2 Deals

- 18.1.6.3.3 Other developments

- 18.1.7 IPG AUTOMOTIVE GMBH

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Product launches/developments

- 18.1.7.3.2 Deals

- 18.1.7.3.3 Other developments

- 18.1.8 MATHWORKS, INC.

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Deals

- 18.1.9 HEXAGON AB

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches/developments

- 18.1.9.3.2 Deals

- 18.1.10 VECTOR INFORMATIK GMBH

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches/developments

- 18.1.10.3.2 Deals

- 18.1.11 KEYSIGHT TECHNOLOGIES

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Product launches/developments

- 18.1.11.3.2 Deals

- 18.1.11.3.3 Other developments

- 18.1.12 DASSAULT SYSTEMES

- 18.1.12.1 Business overview

- 18.1.12.2 Products/Solutions offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Deals

- 18.1.13 COGNATA

- 18.1.13.1 Business overview

- 18.1.13.2 Products/Solutions offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Product launches/developments

- 18.1.13.3.2 Deals

- 18.1.13.3.3 Other developments

- 18.1.1 SIEMENS

- 18.2 OTHER PLAYERS

- 18.2.1 RFPRO

- 18.2.2 FORETELLIX

- 18.2.3 ELEKTROBIT

- 18.2.4 ETAS

- 18.2.5 VI-GRADE GMBH

- 18.2.6 AVSIMULATION

- 18.2.7 ANTEMOTION

- 18.2.8 PARALLEL DOMAIN

- 18.2.9 REAL-TIME TECHNOLOGIES

- 18.2.10 AIMOTIVE

- 18.2.11 ANYVERSE SL

- 18.2.12 DORLECO

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 List of secondary sources

- 19.1.1.2 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Primary interviews: Demand and supply sides

- 19.1.2.2 Breakdown of primary interviews

- 19.1.2.3 List of primary participants

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 TOP-DOWN APPROACH

- 19.3 DATA TRIANGULATION

- 19.4 FACTOR ANALYSIS

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RESEARCH LIMITATIONS

- 19.7 RISK ASSESSMENT

20 APPENDIX

- 20.1 INSIGHTS FROM INDUSTRY EXPERTS

- 20.2 DISCUSSION GUIDE

- 20.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.4 CUSTOMIZATION OPTIONS

- 20.4.1 ADAS SIMULATION MARKET, BY LEVEL OF AUTONOMY, AT REGIONAL LEVEL (FOR REGIONS COVERED IN REPORT)

- 20.4.2 COMPANY INFORMATION

- 20.5 RELATED REPORTS

- 20.6 AUTHOR DETAILS