|

시장보고서

상품코드

2021044

식품 병원체 검사 시장 예측(-2031년) : 병원체 유형별, 피검사 식품별, 기술별, 최종사용자별, 지역별Food Pathogen Testing Market by Pathogen Type, Food Tested (Meat & Poultry, Fish & Seafood, Processed Food, Fruits & Vegetables, Dairy Products, Cereals & Grains, Other Food Products), Technology, End User, Region - Global Forecast To 2031 |

||||||

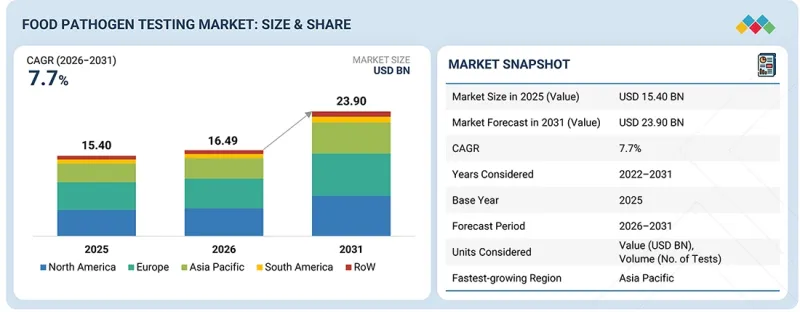

세계의 식품 병원체 검사 시장 규모는 2026년 164억 9,000만 달러에서 2031년까지 239억 달러에 달할 것으로 예측되며, CAGR로 7.7%의 확대가 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 100만 달러, 검사 건수 |

| 부문 | 병원체 유형, 기술, 피검사 식품, 최종사용자, 서비스 프로바이더, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

식중독 발생 건수의 증가와 전 세계 식품 공급망에 대한 규제 강화로 인해 시장은 꾸준히 확대되고 있습니다. 식품 제조업체와 가공업체는 제품 안전성 보장, 오염 위험 감소, 엄격한 안전 기준 준수라는 세 가지 주요 목표에 초점을 맞추고 있습니다.

검사 서비스 제공업체는 신속한 분자 수준 병원체 검출 검사를 수행할 수 있는 능력을 확장하고 있으며, 이를 통해 병원체 검출 결과를 보다 신속하게 얻을 수 있습니다. 병원체 검사는 제품 회수를 줄이고, 소비자의 안전을 보장하며, 신뢰할 수 있는 공급망 관리를 구축하는 데 있으며, 긍정적인 결과를 보여주고 있습니다. 기업은 진화하는 산업 요구사항을 충족하기 위해 첨단 진단 기술, 자동화, 고처리량 검사 솔루션에 투자하고 있습니다.

조직의 성장 과정에는 여러 가지 문제가 있으며, 이는 성장 둔화로 이어지고 있습니다. 첨단 검사 기술 및 검사실 인프라에 대한 투자는 조직에 높은 운영 비용을 초래하고 있습니다. 지역마다 다른 검사 규정과 개발도상국에서 나타나는 검사상의 제한으로 인해 검사에 제약이 발생하고 있습니다. 그러나 이러한 요소들에도 불구하고 시장에는 큰 기회가 존재합니다. 식품 무역의 확대, 인스턴트 식품의 소비 증가, 식품 안전에 대한 인식이 높아짐에 따라 식품에 대한 수요가 증가하고 있습니다. 조직은 탐지 속도 향상, 규정 준수 유지, 식품 안전 시스템 개발이라는 세 가지 큰 목표를 위해 지속적으로 노력하고 있습니다.

"기술별로는 신속 검사 부문이 예측 기간 중 식품 병원체 검사 시장에서 가장 빠르게 성장할 것으로 예상됩니다. "

현재 식품 병원체 검사 시장에서는 신속 검사법의 채택률이 빠르게 증가하고 있습니다. 이 신기술은 기존 배양 방법보다 짧은 시간 내에 병원균을 식별할 수 있으므로 보다 빠른 결과를 제공하여 제품 검사 및 시장 출시 과정을 가속화할 수 있습니다. 이 솔루션은 대량의 제품을 취급하는 식품 공급망에서 시간 제약이 심한 요구사항에 필수적입니다.

신속검사법은 PCR과 면역측정법을 이용하여 다양한 병원체를 동시에 검출하면서 정확한 결과를 제공합니다. 이 시스템은 실시간 모니터링이 가능하며, 조직이 제품 검사를 통해 더 높은 식품 안전 기준을 유지할 수 있도록 도와줍니다. 식품 공급망이 복잡해짐에 따라 검사 시장에서는 더 나은 검사 방법이 요구되고 있습니다.

기존의 검사 방식은 인증 검사에서 여전히 그 가치를 유지하고 있습니다. 현재 스크리닝 프로세스에는 신속 검사가 선호되고 있습니다. 이는 신속성과 업무 효율성뿐만 아니라 유연한 검사 능력을 제공하기 위함입니다. 신속 검사는 즉각적인 결과를 제공하고, 현행 식품 안전 기준을 충족하면서 업무 중단을 최소화하므로 사용자는 보다 신속하게 업무를 완료할 수 있습니다.

"병원체 유형별로는 살모넬라균 부문이 식품 병원체 검사 시장에서 가장 큰 비중을 차지할 것으로 예상됩니다. "

살모넬라균은 다양한 식품에 존재하므로 전 세계에서 살모넬라균에 대한 검사가 활발히 이루어지고 있습니다. 이 병원체는 육류 제품에서 가장 많이 발견되지만, 닭고기, 계란, 가공식품에도 나타나기 때문에 정기 검사와 공식 검사 모두에서 필수적입니다. 살모넬라균은 식중독 및 규제 요건과 관련이 있으므로 식품 제조업체와 검사 기관은 살모넬라균 검출을 우선순위로 삼고 있습니다. 이 병원체는 유통망 전체에 존재하므로 검사기관에서는 지속적인 검사 업무가 이루어지고 있습니다. 다른 병원균이 주목받기 시작했으나, 살모넬라균은 여전히 식품안전검사 프로그램에서 필수적인 존재로 남아 있습니다. 살모넬라 검사가 그 존재를 유지하는 이유는 광범위한 존재, 엄격한 규제, 국제 시장에서의 식품 안전 보장에 대한 역할 등 세 가지 이유에서 비롯됩니다.

세계의 식품 병원체 검사 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 식품 병원체 검사 시장 : 병원체 유형별

제10장 식품 병원체 검사 시장 : 피검사 식품별

제11장 식품 병원체 검사 시장 : 기술별

제12장 식품 병원체 검사 시장 : 최종사용자별

제13장 식품 병원체 검사 시장 : 서비스 프로바이더별

제14장 식품 병원체 검사 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 인접 시장과 관련 시장

제19장 부록

KSA 26.05.13The global food pathogen testing market is expected to grow from USD 16.49 billion in 2026 to USD 23.90 billion by 2031 at a CAGR of 7.7%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (No. of tests) |

| Segments | By Pathogen Type, Technology, Food Tested, End User, Service Provider, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

The market is expanding steadily because foodborne illness cases are increasing, and global food supply chains face stricter regulatory enforcement. Food manufacturers and processors are focusing on three main objectives, which include product safety assurance, contamination risk reduction, and adherence to strict safety standards.

Testing service providers are expanding their abilities to perform rapid and molecular pathogen detection tests, which will lead to quicker pathogen detection results. Pathogen testing shows positive results because it reduces product recalls while making consumers safer and building dependable supply chain operations. Companies are investing in advanced diagnostics, automation, and high-throughput testing solutions to meet evolving industry requirements.

The organizational growth process faces multiple challenges, which result in slower development. Advanced testing technologies and laboratory infrastructure expenses create high operational costs for organizations. The combination of different testing rules that exist in various regions, together with the testing limitations found in developing countries, creates testing restrictions. The market presents strong opportunities that exist despite these elements. The demand for food products increases because food trade expands and people eat more ready-to-eat meals and learn about food safety. The organization continues to work on three main objectives, which include speed detection improvement, compliance maintenance and food safety system development.

"By technology, the rapid testing segment is expected to be the fastest growing during the forecast period in the food pathogen testing market."

The food pathogen testing market currently experiences high adoption rates of rapid testing methods. The new technologies provide faster results because they identify pathogens in less time than standard culture techniques do, which results in faster product testing and product launch processes. The time-critical requirements of food supply chains that handle large quantities of products need this solution.

The testing method of rapid testing uses PCR and immunoassays to deliver precise results while enabling the detection of various pathogens at once. The system enables real-time observation, which helps organizations test their products to maintain higher food safety standards. The testing market requires better testing methods because food supply chains are becoming more complex.

The conventional testing approaches maintain their value for authentication testing. The screening process now prefers rapid testing because it provides both speed and operational efficiency, together with flexible testing capacity. Users can complete their tasks more rapidly with rapid testing because it provides them with immediate results and creates fewer operational interruptions while meeting current food safety standards.

"By pathogen type, the Salmonella segment is expected to account for a significant share in the food pathogen testing market."

The testing of Salmonella remains active throughout the world because this pathogen exists in many different types of food. The pathogen shows its most common presence in meat products, but also appears in poultry and eggs, and processed food items, which makes it essential for both scheduled tests and official inspections. Food producers and testing laboratories prioritize Salmonella detection because the bacterium connects to foodborne illnesses and regulatory requirements. The testing facilities maintain continuous testing operations because the pathogen exists throughout the entire distribution network. Salmonella remains essential for food safety testing programs even as other pathogens start to gain recognition. Salmonella testing maintains its existence because of three reasons, which include its widespread existence, extensive regulations and its role in safeguarding food safety for international markets.

"By food type, the meat & poultry segment is expected to account for a significant share in the food pathogen testing market."

Meat and poultry products need to undergo thorough testing because these food items present a great danger of contamination from dangerous pathogens, which include Salmonella and Campylobacter. The products require complete safety evaluations, which need to examine every step from slaughtering through processing until distribution to fulfill food safety requirements. Food producers and processors prioritize testing in this segment due to the high risk of cross-contamination and the potential impact of outbreaks on public health and brand reputation. The regulatory authorities require all meat and poultry products to undergo strict monitoring, which includes zero-tolerance policies that prohibit specific pathogens. The segment maintains high testing needs because of the large-scale product consumption, the requirements for export testing and the need to perform regular quality assessments. The testing process for meat and poultry products needs testing because contamination risks, together with supply chain monitoring and strict regulations, require operational testing to ensure food safety.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the food pathogen testing market.

- By Company Type: Tier 1 - 30%, Tier 2 - 25%, and Tier 3 - 45%

- By Designation: CXOs - 25%, Managers - 35%, Others - 40%

- By Region: North America - 20%, Europe - 30%, Asia Pacific - 35%, South America - 10%, and Rest of the World - 5%

Prominent companies in the market include SGS S.A. (Switzerland), Eurofins Scientific (Luxembourg), UL LLC (US), Intertek Group Plc. (UK), ALS (Australia), TUV SUD (Germany), Merieux Nutrisciences (US), Tentamus (Germany), Certified Group (US), Microbac Laboratories, Inc. (Pennsylvania), AsureQuality (New Zealand), Hill Laboratories (New Zealand), EMSL Analytical, Inc. (US), Symbio Laboratories (Australia), Element Materials Technology (UK), and others.

Research Coverage

This research report categorizes the food pathogen testing market by Pathogen (Salmonella, Campylobacter, E. coli, Listeria, Other Pathogen Types), Food Tested (Meat & Poultry, Fish & Seafood, Processed Food, Fruits & Vegetables, Dairy Products, Cereals & Grains, Other Food Products), Technology (Traditional, Rapid), End User, Service Provider, and Region (North America, Europe, Asia Pacific, South America, and Rest of the World).

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the food pathogen testing industry. A thorough analysis of the key industry players has been done to provide insights into their business, services, key strategies, contracts, partnerships, agreements, service launches, mergers & acquisitions, and recent developments associated with the food pathogen testing market. This report provides a competitive analysis of emerging startups in the food pathogen testing market ecosystem. Furthermore, the study covers industry-specific trends, including technology analysis, ecosystem & market mapping, and patent & regulatory landscape, among others.

Reasons to Buy This Report

The report provides market leaders/new entrants with information on the closest approximations of revenue numbers for the overall food pathogen testing market and its subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Growing awareness and cases of foodborne illnesses increases demand for food pathogen testing), restraints (High cost of advanced testing technologies such as rapid & molecular testing methods like PCR), opportunities (Expansion & adoption or rapid and molecular testing methods), and challenges (Complexity in detecting multiple pathogens across diverse food matrices) influencing the growth of the food pathogen testing market

- Service Development/Innovation: Detailed insights into research & development activities and service launches in the food pathogen testing market

- Market Development: Comprehensive information about lucrative markets-analysis of food pathogen testing across varied regions

- Market Diversification: Exhaustive information about new product sources, untapped geographies, recent developments, and investments in the food pathogen testing market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, service offerings, brand/service comparison, and service footprints of leading players such as SGS S.A. (Switzerland), Eurofins Scientific (Luxembourg), UL LLC (US), Intertek Group Plc. (UK), ALS (Australia), TUV SUD (Germany), Merieux Nutrisciences (US), Tentamus (Germany), Certified Group (US), Microbac Laboratories, Inc. (Pennsylvania), AsureQuality (New Zealand), Hill Laboratories (New Zealand), EMSL Analytical, Inc. (US), Symbio Laboratories (Australia), Element Materials Technology (UK), and other players in the food pathogen testing market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.5.1 CURRENCY UNIT

- 1.5.2 VOLUME UNIT

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN FOOD PATHOGEN TESTING MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FOOD PATHOGEN TESTING MARKET

- 3.2 FOOD PATHOGEN TESTING MARKET, BY TECHNOLOGY AND REGION

- 3.3 FOOD PATHOGEN TESTING MARKET, BY TECHNOLOGY

- 3.4 FOOD PATHOGEN TESTING MARKET, BY FOOD TESTED

- 3.5 FOOD PATHOGEN TESTING MARKET, BY RAPID TECHNOLOGY

- 3.6 FOOD PATHOGEN TESTING MARKET, BY PATHOGEN TYPE

- 3.7 FOOD PATHOGEN TESTING MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Regulatory tightening and preventive controls

- 4.2.1.2 Expansion of genomic surveillance and traceability

- 4.2.1.3 Faster testing and automation needs

- 4.2.1.4 Increasing demand for convenience and packaged food products

- 4.2.1.5 Rising food recalls due to non-compliant food products

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital and recurring costs

- 4.2.2.2 Workforce and technical capacity gaps

- 4.2.2.3 Complex validation and multi-jurisdictional compliance

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of rapid and molecular testing technologies

- 4.2.3.2 Growth of food exports and international trade compliance

- 4.2.4 CHALLENGES

- 4.2.4.1 Detection complexity across diverse food matrices

- 4.2.4.2 Data integration and traceability system limitations

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN FOOD PATHOGEN TESTING MARKET

- 4.3.1.1 Rapid on-site confirmatory testing

- 4.3.1.2 Cost-effective validated solutions for emerging markets

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Decentralized and on-site testing ecosystems

- 4.3.2.2 Integrated testing, traceability, compliance platforms

- 4.3.1 UNMET NEEDS IN FOOD PATHOGEN TESTING MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 RISING GLOBAL POPULATION AND INCREASING FOOD DEMAND

- 5.2.2 COST PRESSURES & INFLATION

- 5.2.3 RISING PUBLIC HEALTH EXPENDITURE AND FOOD SAFETY INVESTMENTS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 UPSTREAM (INPUT PROVIDERS)

- 5.3.2 SAMPLE COLLECTION & TRANSPORTATION

- 5.3.3 TESTING LABORATORIES (CORE STAGE)

- 5.3.4 DATA MANAGEMENT & REPORTING

- 5.3.5 END USERS

- 5.3.6 SUPPORTING ECOSYSTEM

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY PATHOGEN TYPE

- 5.5.2 AVERAGE SELLING PRICE, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 902720)

- 5.6.2 EXPORT SCENARIO (HS CODE 902720)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.11 IMPACT OF 2025 US TARIFFS - FOOD PATHOGEN TESTING MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGY ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 PCR-BASED MOLECULAR DIAGNOSTICS

- 6.1.2 MICROARRAY-BASED DETECTION PLATFORMS

- 6.1.3 RAPID ON-SITE DETECTION SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED MICROBIAL DETECTION SYSTEMS

- 6.2.2 CHROMATOGRAPHY-BASED TESTING SOLUTIONS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BIOSENSOR-BASED DETECTION TECHNOLOGIES

- 6.3.2 AI-ENABLED FOOD SAFETY MONITORING PLATFORMS

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 LIST OF MAJOR PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE FOOD SAFETY TESTING

- 6.6.2 ON-SITE & MOBILE TESTING SERVICES

- 6.6.3 END-TO-END DIGITAL TESTING & TRACEABILITY PLATFORMS

- 6.6.4 INTEGRATED ENVIRONMENTAL MONITORING SERVICES

- 6.6.5 HIGH-THROUGHPUT & RAPID TESTING SERVICE MODELS

- 6.7 IMPACT OF AI/GEN AI ON FOOD PATHOGEN TESTING SERVICE INDUSTRY

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN FOOD PATHOGEN TESTING SERVICES INDUSTRY

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN FOOD PATHOGEN TESTING MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.7.5 READINESS TO ADOPT GENERATIVE AI IN FOOD PATHOGEN TESTING MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 CLEAR LABS: AUTOMATED NGS-BASED PATHOGEN DETECTION FOR FOOD SAFETY

- 6.8.2 NEMIS TECHNOLOGIES: ON-SITE RAPID PATHOGEN DETECTION FOR FOOD PROCESSING FACILITIES

- 6.8.3 PATHOGENDX: MICROARRAY-BASED MULTI-PATHOGEN DETECTION TECHNOLOGY

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 North America

- 7.1.1.1.1 US

- 7.1.1.1.2 Canada

- 7.1.1.1.3 Mexico

- 7.1.1.2 Europe

- 7.1.1.2.1 European Union

- 7.1.1.2.2 Germany

- 7.1.1.2.3 UK

- 7.1.1.2.4 France

- 7.1.1.2.5 Italy

- 7.1.1.2.6 Poland

- 7.1.1.3 Asia Pacific

- 7.1.1.3.1 China

- 7.1.1.3.2 Japan

- 7.1.1.3.3 India

- 7.1.1.3.4 Australia and New Zealand

- 7.1.1.4 South America

- 7.1.1.4.1 Brazil

- 7.1.1.4.2 Argentina

- 7.1.1.5 RoW

- 7.1.1.5.1 South Africa

- 7.1.1.1 North America

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.4 DOCUMENTATION REQUIREMENTS

- 7.1.5 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.1.5.1 Stricter validation requirements for microbiological testing methods

- 7.1.5.2 Expansion of rapid testing approval pathways

- 7.1.5.3 Mandatory digital traceability in food safety testing workflows

- 7.1.5.4 Strengthening of environmental monitoring and hygiene testing regulations

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 GREEN LABORATORY OPERATIONS AND ENERGY OPTIMIZATION

- 7.2.2 SUSTAINABLE SAMPLE MANAGEMENT AND WASTE REDUCTION

- 7.2.3 DIGITALIZATION AND PAPERLESS REPORTING SYSTEMS

- 7.2.4 OPTIMIZED LOGISTICS AND DECENTRALIZED TESTING MODELS

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.3.1 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY TECHNOLOGY

9 FOOD PATHOGEN TESTING MARKET, BY PATHOGEN TYPE

- 9.1 INTRODUCTION

- 9.2 SALMONELLA

- 9.2.1 HIGH-INCIDENCE, TRADE-DRIVEN PATHOGEN DOMINATING GLOBAL TESTING VOLUMES

- 9.3 LISTERIA

- 9.3.1 LOW-PREVALENCE, HIGH-FATALITY PATHOGEN DRIVING PREMIUM PREVENTIVE TESTING

- 9.4 ESCHERICHIA COLI (E. COLI)

- 9.4.1 OUTBREAK-PRONE PATHOGEN LINKED TO FRESH FOOD SUPPLY CHAIN RISK

- 9.5 CAMPYLOBACTER

- 9.5.1 MOST PREVALENT YET UNDERDIAGNOSED PATHOGEN WITH EVOLVING TESTING COMPLEXITY

- 9.6 OTHER PATHOGEN TYPES

10 FOOD PATHOGEN TESTING MARKET, BY FOOD TESTED

- 10.1 INTRODUCTION

- 10.2 MEAT & POULTRY

- 10.2.1 RISING GLOBAL MEAT AND POULTRY CONSUMPTION TO SPUR DEMAND

- 10.3 FISH & SEAFOOD

- 10.3.1 GROWING RISK OF CONTAMINATION OF FISH AND SEAFOOD DUE TO SUPPLY CHAIN COMPLEXITIES TO DRIVE MARKET

- 10.4 DAIRY PRODUCTS

- 10.4.1 MOUNTING CASES OF LISTERIOSIS AND OTHER PATHOGEN-RELATED ILLNESSES IN DAIRY PRODUCTS TO STIMULATE MARKET DEMAND

- 10.5 PROCESSED FOOD

- 10.5.1 PROCESSED FOODS' SUSCEPTIBILITY TO PATHOGEN CONTAMINATION TO DRIVE DEMAND FOR SAFETY TESTING

- 10.6 FRUIT & VEGETABLES

- 10.6.1 MULTIPLE OUTBREAKS ASSOCIATED WITH PATHOGENS IN FRUITS AND VEGETABLES TO FUEL MARKET GROWTH

- 10.7 CEREALS & GRAINS

- 10.7.1 GROWING RISK OF CROSS-CONTAMINATION DUE TO WIDE APPLICATION OF CEREALS AND GRAINS IN FOOD INDUSTRY TO BOOST MARKET

- 10.8 OTHER FOOD PRODUCTS

11 FOOD PATHOGEN TESTING MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 TRADITIONAL

- 11.2.1 REGULATORY GOLD STANDARD USED TO ENSURE CONFIRMATORY ACCURACY AND SURVEILLANCE INTEGRITY

- 11.3 RAPID

- 11.3.1 ACCELERATED DETECTION ENABLING HIGH-THROUGHPUT AND REAL-TIME FOOD SAFETY DECISIONS TO DRIVE DEMAND

- 11.3.2 CONVENIENCE-BASED

- 11.3.3 HYBRIDIZATION-BASED

- 11.3.4 IMMUNOASSAY

- 11.3.5 OTHER MOLECULAR TESTS

12 FOOD PATHOGEN TESTING MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 FOOD MANUFACTURERS

- 12.2.1 REGULATORY COMPLIANCE AND HIGH CONTAMINATION RISK TO DRIVE LARGEST SHARE OF PATHOGEN TESTING SERVICE DEMAND

- 12.3 DISTRIBUTORS/SUPPLIERS (ONLINE & OFFLINE)

- 12.3.1 GLOBALIZED SUPPLY CHAINS AND TRANSIT-RELATED CONTAMINATION RISKS TO ACCELERATE TESTING SERVICE ADOPTION

- 12.4 RETAILERS & FOOD SERVICE CHAINS

- 12.4.1 FINAL-STAGE CONTAMINATION RISKS AND SUPPLIER COMPLIANCE REQUIREMENTS TO FUEL DEMAND FOR PATHOGEN TESTING SERVICES

- 12.5 GOVERNMENT, PUBLIC HEALTH AGENCIES, & REGULATORY AUTHORITIES

- 12.5.1 SURVEILLANCE PROGRAMS AND REGULATORY ENFORCEMENT TO SHAPE STANDARDIZED TESTING SERVICE DEMAND

- 12.6 FOOD CO-PACKERS

- 12.6.1 PRIVATE-LABEL GROWTH AND MULTI-SOURCE PROCUREMENT TO INCREASE RELIANCE ON PATHOGEN TESTING SERVICES

13 FOOD PATHOGEN TESTING MARKET, BY SERVICE PROVIDER

- 13.1 INTRODUCTION

- 13.2 INDEPENDENT THIRD-PARTY TESTING LABORATORIES

- 13.2.1 ACCREDITED, HIGH-VOLUME TESTING BACKBONE DRIVEN BY REGULATORY AND TRADE COMPLIANCE

- 13.3 CONTRACT RESEARCH ORGANIZATIONS (CROS)

- 13.3.1 SPECIALIZED VALIDATION AND RESEARCH PARTNERS ENABLING ADVANCED TESTING SOLUTIONS

- 13.4 OTHER PROVIDERS

14 FOOD PATHOGEN TESTING, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Strong regulatory framework along with implementing comprehensive food safety testing protocols to support dominant service market share

- 14.2.2 CANADA

- 14.2.2.1 Proactive measures by government aimed at reducing foodborne pathogen risks, mainly within meat and poultry industry, to fuel service adoption

- 14.2.3 MEXICO

- 14.2.3.1 Export compliance and improving regulatory systems accelerating demand for testing services

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Rise in foodborne illnesses and stringent compliance requirements to support consistent testing demand

- 14.3.2 FRANCE

- 14.3.2.1 Robust scrutiny in dairy and meat sectors and strict safety regulations to fuel pathogen testing demand

- 14.3.3 UK

- 14.3.3.1 R&D initiatives, retail-driven quality standards and high disease burden driving routine testing services

- 14.3.4 ITALY

- 14.3.4.1 High tourism and fresh food consumption to increase testing service requirements

- 14.3.5 SPAIN

- 14.3.5.1 Incidents of foodborne illnesses and quality-focused production to drive service adoption

- 14.3.6 POLAND

- 14.3.6.1 Domestic consumption and exports of dairy to drive compliance-based testing demand

- 14.3.7 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Large-scale food production and tightening regulations to accelerate testing adoption

- 14.4.2 INDIA

- 14.4.2.1 Expanding regulatory framework and informal supply chains to drive necessity for testing

- 14.4.3 JAPAN

- 14.4.3.1 Advanced food safety systems and strict standards to ensure consistent testing services

- 14.4.4 AUSTRALIA & NEW ZEALAND

- 14.4.4.1 Stringent monitoring of food commodities at consumer and industry levels to drive high-quality testing services

- 14.4.5 SOUTHEAST ASIA

- 14.4.5.1 Export markets with responsibility to address regional food safety concerns to increase demand for testing services

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Large food processing industry to drive high-volume pathogen testing demand

- 14.5.2 ARGENTINA

- 14.5.2.1 Evolving consumer attitudes and government's concern to support compliance-driven testing services

- 14.5.3 REST OF SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.6 REST OF THE WORLD

- 14.6.1 MIDDLE EAST

- 14.6.1.1 Increase in food imports and strengthening regulatory safety measures to boost testing service needs

- 14.6.2 AFRICA

- 14.6.2.1 High disease burden and evolving infrastructure to drive long-term testing demand

- 14.6.1 MIDDLE EAST

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS, 2023-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.5.1 COMPANY VALUATION

- 15.5.2 EV/EBITDA

- 15.6 BRAND COMPARISON ANALYSIS

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Pathogen type footprint

- 15.7.5.4 Food tested footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2025

- 15.8.5.1 Detailed list of key startups/SMEs

- 15.8.5.2 Competitive benchmarking of key startups/SMEs

- 15.9 COMPETITIVE SCENARIO AND TRENDS

- 15.9.1 SERVICE LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 SGS SOCIETE GENERALE DE SURVEILLANCE SA

- 16.1.1.1 Business overview

- 16.1.1.2 Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.3.2 Expansions

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 EUROFINS SCIENTIFIC

- 16.1.2.1 Business overview

- 16.1.2.2 Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Service launches

- 16.1.2.3.2 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 UL LLC

- 16.1.3.1 Business overview

- 16.1.3.2 Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 INTERTEK GROUP PLC.

- 16.1.4.1 Business overview

- 16.1.4.2 Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 ALS

- 16.1.5.1 Business overview

- 16.1.5.2 Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 TUV SUD

- 16.1.6.1 Business overview

- 16.1.6.2 Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Expansions

- 16.1.6.4 MnM view

- 16.1.7 MERIEUX NUTRISCIENCES CORPORATION

- 16.1.7.1 Business overview

- 16.1.7.2 Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.3.2 Expansions

- 16.1.7.4 MnM view

- 16.1.8 TENTAMUS

- 16.1.8.1 Business overview

- 16.1.8.2 Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.8.4 MnM view

- 16.1.9 CERTIFIED LABORATORIES

- 16.1.9.1 Business overview

- 16.1.9.2 Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Service launches

- 16.1.9.3.2 Deals

- 16.1.9.3.3 Expansions

- 16.1.9.4 MnM view

- 16.1.10 MICROBAC LABORATORIES, INC.

- 16.1.10.1 Business overview

- 16.1.10.2 Services offered

- 16.1.10.3 Recent developments

- 16.1.10.4 MnM view

- 16.1.11 ASUREQUALITY

- 16.1.11.1 Business overview

- 16.1.11.2 Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.11.4 MnM view

- 16.1.12 HILL LABORATORIES

- 16.1.12.1 Business overview

- 16.1.12.2 Services offered

- 16.1.12.3 Recent developments

- 16.1.12.4 MnM view

- 16.1.13 EMSL ANALYTICAL, INC.

- 16.1.13.1 Business overview

- 16.1.13.2 Services offered

- 16.1.13.3 Recent developments

- 16.1.13.4 MnM view

- 16.1.14 SYMBIO LABS

- 16.1.14.1 Business overview

- 16.1.14.2 Services offered

- 16.1.14.3 Recent developments

- 16.1.14.4 MnM view

- 16.1.15 ELEMENT MATERIALS TECHNOLOGY

- 16.1.15.1 Business overview

- 16.1.15.2 Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.15.3.2 Expansions

- 16.1.15.3.3 Other developments

- 16.1.1 SGS SOCIETE GENERALE DE SURVEILLANCE SA

- 16.2 STARTUPS/SMES

- 16.2.1 TWIN ARBOR LABS

- 16.2.1.1 Business overview

- 16.2.1.2 Services offered

- 16.2.1.3 Recent developments

- 16.2.1.4 MnM view

- 16.2.2 Q LABORATORIES

- 16.2.2.1 Business overview

- 16.2.2.2 Services offered

- 16.2.2.3 Recent developments

- 16.2.2.4 MnM view

- 16.2.3 DAILY LABORATORIES

- 16.2.3.1 Business overview

- 16.2.3.2 Services offered

- 16.2.3.3 Recent developments

- 16.2.3.4 MnM view

- 16.2.4 FARE LABS

- 16.2.4.1 Business overview

- 16.2.4.2 Services offered

- 16.2.4.3 Recent developments

- 16.2.4.4 MnM view

- 16.2.5 IEH INC.

- 16.2.5.1 Business overview

- 16.2.5.2 Services offered

- 16.2.5.3 Recent developments

- 16.2.5.3.1 Deals

- 16.2.5.3.2 Expansions

- 16.2.5.4 MnM view

- 16.2.6 PRIMUSLABS

- 16.2.7 DAANE LABS

- 16.2.8 PT SEAFOOD INSPECTION LABORATORY

- 16.2.9 AGROLABS

- 16.2.10 EUREKA ANALYTICAL PRIVATE LIMITED

- 16.2.1 TWIN ARBOR LABS

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Breakdown of primary profiles

- 17.1.2.3 Key insights from industry experts

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH (BASED ON TYPE, BY REGION)

- 17.2.2 TOP-DOWN APPROACH (BASED ON GLOBAL MARKET)

- 17.2.3 SUPPLY SIDE

- 17.2.4 DEMAND SIDE

- 17.3 DATA TRIANGULATION

- 17.4 RESEARCH ASSUMPTIONS

- 17.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

18 ADJACENT AND RELATED MARKETS

- 18.1 INTRODUCTION

- 18.2 RESEARCH LIMITATIONS

- 18.3 FOOD SAFETY TESTING MARKET

- 18.3.1 MARKET DEFINITION

- 18.3.2 MARKET OVERVIEW

- 18.4 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET

- 18.4.1 MARKET DEFINITION

- 18.4.2 MARKET OVERVIEW

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS