|

시장보고서

상품코드

2033992

조영제 시장 : 유형별, 제형별, 검사법별, 투여 경로별, 적응증별, 용도별, 최종사용자별, 지역별 - 세계 예측(-2031년)Contrast Media Market By Type, Form, Modality, Route of Administration, Indication & Region - Global Forecast to 2031 |

||||||

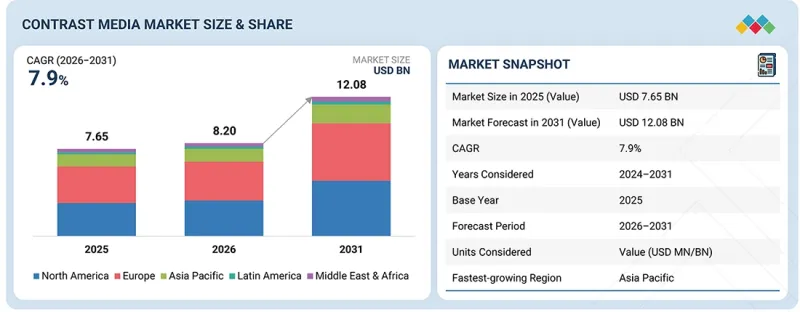

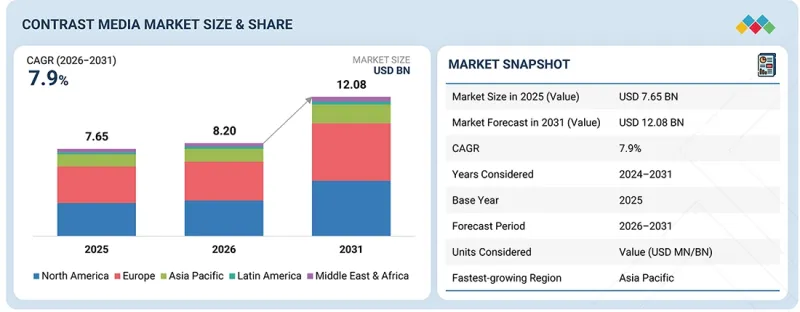

세계의 조영제 시장 규모는 2025년 76억 5,000만 달러에서 2031년까지 120억 8,000만 달러에 달할 것으로 예측되며, 2026년부터 2031년까지 CAGR은 7.9%를 기록할 전망입니다.

조영제 시장은 주로 조영제 제형의 혁신과 표적 지향성 및 활성화 가능한 조영제 개발에 의해 주도되고 있으며, 이는 영상 진단의 정확성을 높이고 정밀한 진단에 대한 수요 증가에 부응하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 제형별, 검사법별, 투여 경로별, 적응증별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

또한, 정부의 의료 이니셔티브에 대한 투자와 영상 진단 서비스 확대 및 프레임워크 협정 체결과 같은 의료 이니셔티브에 대한 투자는 첨단 영상 진단 옵션에 대한 접근성을 높이고 있습니다. 또한, 암, 심혈관질환 등 만성질환의 유병률 증가에 따라 조기 발견, 경과 관찰, 치료 계획 수립을 위해 조영제 영상 검사가 요구되고 있습니다.

"2026년에는 심혈관질환 부문이 시장에서 가장 큰 점유율을 차지했습니다."

적응증별로 조영제 시장은 심혈관계 질환, 암, 소화기 질환, 근골격계 질환, 신경계 질환, 신장질환으로 구분됩니다. 심혈관질환 부문은 관상동맥 조영술, CT 혈관조영술, 심장 카테터 삽입술과 같은 진단 및 중재 시술의 수가 많기 때문에 2026년 가장 큰 시장 점유율을 차지했습니다. 전 세계적으로 심장질환의 유병률이 증가함에 따라 정확한 진단과 치료 계획 수립을 위한 조영제 영상 진단이 표준적인 방법으로 자리 잡았습니다. 또한, 심장 수술 중 혈관의 실시간 시각화에 대한 긴급한 요구가 조영제에 대한 안정적인 수요를 뒷받침하고 있습니다. 또한 순환기학 분야의 첨단 영상 진단 기술의 도입도 이 부문이 우위를 유지하는 주요 요인으로 작용하고 있습니다.

"예측 기간 동안 중재적 심장학 분야가 가장 높은 CAGR을 기록할 것으로 예상됩니다."

용도별로 조영제 시장은 방사선과, 중재적 방사선학, 중재적 심장학으로 구분됩니다. 중재적 심장학 부문은 혈관성형술, 스텐트 삽입술, 카테터를 이용한 중재적 치료 등 최소침습적 심장 치료의 급속한 성장에 힘입어 2026년부터 2031년까지 가장 높은 CAGR을 기록할 것으로 예상됩니다. 관상동맥질환과 생활습관병으로 인한 심장질환이 증가함에 따라 시술 건수가 증가하고 있습니다. 또한, 카테터 검사실과 영상 유도 기술의 발달로 심장 중재시 조영제 사용이 확대되고 있습니다. 또한, 환자의 조기 회복과 단기 입원에 대한 선호도가 높아진 것도 이 부문에 더욱 힘을 실어주고 있습니다.

"아시아태평양 시장은 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다."

중국, 인도, 일본 등의 국가에서 의료 인프라의 급속한 발전은 아시아태평양의 조영제 시장의 성장을 주도하고 있습니다. 의료비 상승과 첨단 영상 진단 시스템의 보급으로 조영제를 이용한 검사에 대한 접근성이 향상되고 있습니다. 또한, 만성질환의 유병률 증가와 의료관광의 확대로 인해 지역 전체에서 영상 진단 건수가 증가하고 있습니다. 또한, 병원 현대화 및 조기 진단에 대한 정부의 강력한 지원으로 시장 확대 속도가 빨라지고 있습니다.

조영제 시장의 주요 기업은 Bracco Imaging S.p.A.(이탈리아), Bayer AG(독일), Guerbet(미국), Lantheus Medical Imaging(미국), GE HealthCare(미국), Unijules Life Sciences Ltd.(인도), J.B. Chemicals & Pharmaceuticals Limited(인도), Sanochemia Pharmazeutika GmbH(독일), Taejoon Pharm(한국), Jodas Expoim(인도), iMax Diagnostic Imaging Limited(아일랜드), YZJ Group(중국), Beijing Beilu Pharmaceutical(중국), 및 Livealth Biopharma Pvt. Ltd.(인도) 등이 있습니다.

조사 범위

이 보고서는 조영제 시장을 유형, 적응증, 양식, 투여 경로, 용도, 최종사용자 및 지역별로 분류하여 조사하고 있습니다. 또한, 시장 성장에 영향을 미치는 요인을 다루고, 시장의 다양한 기회와 과제를 분석하는 한편, 시장 리더들의 경쟁 상황에 대한 세부 정보를 제공합니다. 또한, 본 보고서에서는 트렌드에 기반한 마이크로 마켓을 분석합니다. 5개 주요 지역(및 해당 지역 내 각 국가)의 시장 부문별 수익을 예측하고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 전체 조영제 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 시장 리더와 신규 진입자에게 도움을 줄 것입니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 더 깊은 인사이트를 얻고, 자신의 비즈니스를 적절히 포지셔닝하고, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것입니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 촉진요인, 억제요인, 도전 과제 및 기회에 대한 인사이트를 제공하는 데 도움이 될 것입니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인 분석(조영제를 이용한 스캔 횟수 증가, 조영제 제형의 발전, 정밀 진단을 위한 표적형 및 활성화형 조영제 개발 확대, 진단 영상 진단 확대를 지원하는 정부 투자 및 NHS 프레임워크 협약), 제약요인(부작용 위험, 영상 진단 절차의 높은 비용, 조영제 순환, 시간 및 안정성 제한, 가돌리늄 기반 조영제의 환경 내 잔류성) 시간 및 안정성 제한, 가돌리늄계 조영제의 환경 내 잔류성), 기회(중재적 방사선 및 영상 유도하 시술의 성장, 마이크로버블 및 초음파 조영제 개발, 소아 복부 영상 진단에서 조영초음파(CEUS)의 소아 복부 영상 진단 적용), 도전과제(소아 복부 영상 진단에서 조영초음파(CEUS)의 적용) 방사선과 인력 부족, 공급망 취약성, 신규 및 멀티모달 조영제의 복잡한 규제 승인 절차 등) 등 조영제 시장 성장에 영향을 미치는 요인들

- 제품 개발 및 혁신 : 조영제 시장의 미래 기술, 연구 개발 활동, 신제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 조영제 시장을 분석합니다.

- 시장 다각화 : 조영제 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보

- 경쟁사 분석 : Bracco Imaging S.p.A.(이탈리아), Bayer AG(독일), Guerbet(미국), GE Healthcare(미국) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 기술, 특허, AI 도입에 의한 전략적 파괴

제8장 조영제 시장(유형별)

제9장 조영제 시장(제형별)

제10장 조영제 시장(검사법별)

제11장 조영제 시장(투여 경로별)

제12장 조영제 시장(적응증별)

제13장 조영제 시장(용도별)

제14장 조영제 시장(최종사용자별)

제15장 조영제 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.05.27The global contrast media market is projected to reach USD 12.08 billion by 2031 from USD 7.65 billion in 2025, at a CAGR of 7.9% from 2026 to 2031. The contrast media market is mainly driven by innovation in contrast agent formulations and the development of targeted and activatable contrast agents, which enhance the accuracy of imaging studies and meet the increasing demand for precise diagnostics.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Form, Indication, Modality, Route of Administration, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East, and Africa |

Additionally, government investments in healthcare initiatives, such as expanding diagnostic imaging services and establishing framework agreements, support access to advanced imaging options. Moreover, the rising prevalence of chronic diseases like cancer and cardiovascular conditions necessitates contrast imaging studies for early detection, monitoring, and treatment planning.

"The cardiovascular disease segment held the largest share of the market in 2026."

By indication, the contrast media market is segmented into cardiovascular disease, cancer, gastrointestinal disorders, musculoskeletal disorders, neurological disorders, and nephrological disorders. The cardiovascular disease segment held the largest market share in 2026, driven by the high volume of diagnostic and interventional procedures such as coronary angiography, CT angiography, and cardiac catheterization. The increasing prevalence of heart disorders worldwide has made contrast-enhanced imaging a standard practice for accurate diagnosis and treatment planning. Additionally, the urgent need for real-time visualization of vessels during cardiac surgery has sustained a steady demand for contrast agents. Furthermore, the introduction of advanced imaging technology in cardiology is a key driver of this segment's dominance.

"The interventional cardiology segment is projected to register the highest CAGR during the forecast period."

By application, the contrast media market is segmented into radiology, interventional radiology, and interventional cardiology. The interventional cardiology segment is expected to have the highest CAGR from 2026 to 2031, driven by the rapid growth of minimally invasive cardiac procedures, including angioplasty, stent placement, and catheter-based interventions. The number of procedures is increasing because of a rise in coronary artery disease and lifestyle-related cardiac disorders. Additionally, the development of catheterization labs and imaging-guided technologies has led to greater use of contrast agents in cardiac interventions. Furthermore, the segment is being further supported by patients' increasing preference for quick recovery and shorter hospital stays.

"The market in the Asia Pacific region is expected to witness the highest growth during the forecast period."

The rapid development of healthcare infrastructure in nations such as China, India, and Japan is driving growth in the contrast media market in the Asia Pacific region. Access to contrast-enhanced procedures is becoming better due to rising healthcare costs and the growing use of sophisticated diagnostic imaging systems. Imaging volumes are also being driven throughout the region by the rising prevalence of chronic illnesses and the growth of medical tourism. Additionally, the market is expanding faster due to the government's strong support for hospital modernization and early diagnosis.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-48%, Tier 2-36%, and Tier 3- 16%

- By Designation: C-level-10%, Director-level-14%, and Others-76%

- By Region: North America-40%, Europe-32%, Asia Pacific-20%, Latin America-5%, and the Middle East & Africa-3%

The prominent players in the contrast media market are Bracco Imaging S.p.A. (Italy), Bayer AG (Germany), Guerbet (US), Lantheus Medical Imaging (US), GE HealthCare (US), Unijules Life Sciences Ltd. (India), J.B. Chemicals & Pharmaceuticals Limited (India), Sanochemia Pharmazeutika GmbH (Germany), Taejoon Pharm Co., Ltd. (South Korea), Jodas Expoim (India), iMax Diagnostic Imaging Limited (Ireland), YZJ Group (China), Beijing Beilu Pharmaceutical Co., Ltd. (China), and Livealth Biopharma Pvt. Ltd. (India) among others.

Research Coverage

This report studies the contrast media market based on type, indication, modality, route of administration, application, end user, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets by growth trends. It forecasts market segment revenue across five main regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue for the overall contrast media market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides insights into key drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (Rising number of contrast- mediated scan, Advancements in contrast agent formulations, increasing development of targeted and activatable contrast agents for precision diagnostics and Government Investment and NHS Framework Agreements Supporting Diagnostic Imaging Expansion), restraints (Risk of Adverse Reactions, High Cost of Imaging Procedures, Limited circulation time and stability of contrast agents, environmental persistence of gadolinium-based contrast agents), opportunities (Growth of Interventional Radiology and Image-Guided Procedures, Development of Microbubble and Ultrasound Contrast Agents, Expansion of Contrast-Enhancced Ultrasound (CEUS) Applications in Pediatric Abdominal Imaging), and challenges (Workforce Shortages in Radiology, Supply Chain Vulnerabilities, Complex Regulatory Approval Pathways for Novel and Multimodal Contrast Agents) influencing the growth of the contrast media market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the contrast media market

- Market Development: Comprehensive information about lucrative markets-the report analyses the contrast media market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the contrast media market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Bracco Imaging S.p.A. (Italy), Bayer AG (Germany), Guerbet (US), GE HealthCare (US), and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED AND REGIONS CONSIDERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN CONTRAST MEDIA MARKET

- 2.4 HIGH GROWTH SEGMENTS

3 PREMIUM INSIGHTS

- 3.1 CONTRAST MEDIA MARKET OVERVIEW

- 3.2 CONTRAST MEDIA MARKET, BY REGION

- 3.3 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY COUNTRY AND END USER

- 3.4 GEOGRAPHIC SNAPSHOT OF CONTRAST MEDIA MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Advancements in contrast agent formulations

- 4.2.1.2 Precision Diagnostics Enabled by Targeted and Activatable Contrast Agents

- 4.2.1.3 Government Investments and Healthcare Procurement Initiatives

- 4.2.1.4 Rising number of contrast-mediated scans

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited Circulation Time and Stability of Certain Contrast Agents

- 4.2.2.2 Environmental persistence of gadolinium-based contrast agents

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of Multimodal Imaging Technologies

- 4.2.3.2 Expansion of Contrast-enhanced ultrasound (CEUS) applications in pediatric imaging

- 4.2.3.3 Increasing demand for low-dose, high-relaxivity contrast agents for neonates and infants

- 4.2.4 CHALLENGES

- 4.2.4.1 Safety and toxicity concerns associated with gadolinium and nanoparticle-based contrast agents

- 4.2.4.2 Complex regulatory approval pathways for novel and multimodal contrast agents

- 4.2.4.3 Complexity in scalable synthesis and standardization of nanoparticle-based contrast agents

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 HEALTHCARE EXPENDITURE AND INFRASTRUCTURE OUTLOOK

- 5.2.2.1 Macroeconomic outlook for NORTH AMERICA

- 5.2.3 MACROECONOMIC OUTLOOK FOR EUROPE

- 5.2.4 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 5.2.5 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 5.2.6 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.2 AVERAGE SELLING PRICE OF CONTRAST MEDIA PRODUCTS, BY KEY PLAYER

- 5.5.3 AVERAGE SELLING PRICE TREND OF CONTRAST MEDIA PRODUCTS, BY KEY PLAYER, 2024

- 5.6 TRADE DATA ANALYSIS

- 5.6.1 IMPORT DATA (HS CODE 300630)

- 5.6.2 EXPORT DATA (HS CODE 300630)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY 1: MACROCYCLIC CONTRAST AGENTS FOR IMPROVED MRI SAFETY

- 5.10.2 CASE STUDY 2: IODINATED CONTRAST MEDIA OPTIMIZATION IN CT IMAGING

- 5.10.3 CASE STUDY 3: LOW-DOSE MRI CONTRAST AGENT FOR PEDIATRIC MRI IMAGING

- 5.11 IMPACT OF 2025 US TARIFF- CONTRAST MEDIA MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.5 IMPACT ON END USERS

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 6.1.1 BUYING CRITERIA

- 6.1.2 DECISION-MAKING PROCESS

- 6.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.3 UNMET NEEDS FROM END USERS

- 6.3.1 UNMET NEEDS FROM END USERS

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, AND AI ADOPTION

- 7.1 KEY TECHNOLOGIES

- 7.1.1 CONTRAST-ENHANCED ULTRASOUND (CEUS) ADVANCEMENTS

- 7.1.1.1 Targeted and molecular contrast agents

- 7.1.1.2 Advanced gadolinium-based agents and hyperpolarized techniques

- 7.1.2 COMPLEMENTARY TECHNOLOGIES

- 7.1.2.1 Automated contrast injector systems

- 7.1.1 CONTRAST-ENHANCED ULTRASOUND (CEUS) ADVANCEMENTS

- 7.2 PATENT ANALYSIS

- 7.2.1 CONTRAST MEDIA MARKET: LIST OF PATENTS

- 7.3 FUTURE APPLICATIONS

- 7.4 IMPACT OF AI/GEN AI ON CONTRAST MEDIA MARKET

- 7.4.1 TOP USE CASES AND MARKET POTENTIAL

- 7.4.2 BEST PRACTICES IN CONTRAST MEDIA.

- 7.4.3 CASE STUDIES OF AI IMPLEMENTATION IN CONTRAST MEDIA MARKET

- 7.4.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.4.5 CLIENT READINESS TO ADOPT GENERATIVE AI IN CONTRAST MEDIA MARKET

- 7.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

8 CONTRAST MEDIA MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 IODINATED CONTRAST MEDIA

- 8.2.1 RISING ADOPTION OF CT IMAGING INCREASES DEMAND

- 8.3 GADOLINIUM-BASED CONTRAST MEDIA

- 8.3.1 SAFETY CONCERNS ASSOCIATED WITH GADOLINIUM-BASED CONTRAST AGENTS RESTRAIN MARKET GROWTH

- 8.4 MICROBUBBLE CONTRAST MEDIA

- 8.4.1 GROWING PHYSICIAN PREFERENCE FOR CONTRAST-ENHANCED ULTRASOUND DRIVES ADOPTION

- 8.5 BARIUM-BASED CONTRAST MEDIA

- 8.5.1 ADVERSE EFFECTS ASSOCIATED WITH BARIUM SULFATE CONTRAST MEDIA LIMIT CLINICAL USAGE

9 CONTRAST MEDIA MARKET, BY FORM

- 9.1 INTRODUCTION

- 9.2 LIQUID

- 9.2.1 CONVENIENCE OF USE IN HOSPITALS AND DIAGNOSTIC CENTERS TO DRIVE MARKET GROWTH

- 9.3 POWDER

- 9.3.1 CONVENIENT HANDLING, STORAGE, AND TRANSPORTATION DRIVES INCREASED ADOPTION

- 9.4 OTHER FORMS

10 CONTRAST MEDIA MARKET, BY MODALITY

- 10.1 INTRODUCTION

- 10.2 X-RAY

- 10.2.1 DEVELOPMENT OF SAFER, LOW-CONCENTRATION CONTRAST AGENTS FOR X-RAY - KEY OPPORTUNITY

- 10.3 CT

- 10.3.1 INCREASING NUMBER OF CT EXAMINATIONS TO PROPEL MARKET

- 10.4 MRI

- 10.4.1 INCREASING FOCUS ON NEXT-GENERATION GADOLINIUM-BASED CONTRAST AGENTS TO ENHANCE SAFETY AND IMAGING PERFORMANCE

- 10.5 ULTRASOUND

- 10.5.1 FLEXIBLE AND LOW-COST DIAGNOSTIC IMAGING MODALITY - KEY FACTORS DRIVING MARKET GROWTH

11 CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION

- 11.1 INTRODUCTION

- 11.2 INTRAVASCULAR ROUTE

- 11.2.1 INCREASING CLINICAL RELIANCE FOR ENHANCED DIAGNOSTIC IMAGING AND TREATMENT OUTCOMES TO DRIVE SEGMENT

- 11.2.1.1 Intravenous (IV) route

- 11.2.1.2 Intra-arterial (IA) route

- 11.2.1 INCREASING CLINICAL RELIANCE FOR ENHANCED DIAGNOSTIC IMAGING AND TREATMENT OUTCOMES TO DRIVE SEGMENT

- 11.3 ORAL ROUTE

- 11.3.1 ENHANCING GASTROINTESTINAL VISUALIZATION WITH ORAL CONTRAST AGENTS IN DIAGNOSTIC IMAGING

- 11.4 RECTAL ROUTE

- 11.4.1 RISING DEMAND FOR ACCURATE POST-SURGICAL COMPLICATION DETECTION TO DRIVE ADOPTION

- 11.5 OTHER ROUTES

12 CONTRAST MEDIA MARKET, BY INDICATION

- 12.1 INTRODUCTION

- 12.2 CARDIOVASCULAR DISEASE

- 12.2.1 HIGH BURDEN OF CVD TO DRIVE MARKET

- 12.3 CANCER

- 12.3.1 ADVANCED ONCOLOGIC DIAGNOSTICS THROUGH CONTRAST-ENHANCED ULTRASOUND IMAGING TO BOOST SEGMENT

- 12.4 GASTROINTESTINAL DISORDERS

- 12.4.1 EXPANDING ROLE OF CEUS IN PEDIATRIC GASTROINTESTINAL DISORDERS AND NEONATAL IMAGING TO PROPEL GROWTH

- 12.5 MUSCULOSKELETAL DISORDERS

- 12.5.1 RISING INCIDENCE OF WORK-RELATED MUSCULOSKELETAL DISORDERS TO SUPPORT MARKET GROWTH

- 12.6 NEUROLOGICAL DISORDERS

- 12.6.1 INCREASING BURDEN OF NEUROLOGICAL DISORDERS DRIVES DEMAND

- 12.7 NEPHROLOGICAL DISORDERS

- 12.7.1 RISING PREVALENCE OF END-STAGE RENAL DISEASE TO DRIVE DEMAND

13 CONTRAST MEDIA MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 RADIOLOGY

- 13.2.1 GROWING NUMBER OF DIAGNOSTIC PROCEDURES TO DRIVE MARKET

- 13.3 INTERVENTIONAL RADIOLOGY

- 13.3.1 RISING ADOPTION OF MINIMALLY INVASIVE INTERVENTIONS TO DRIVE MARKET

- 13.4 INTERVENTIONAL CARDIOLOGY

- 13.4.1 RISING INCIDENCE OF CARDIAC DISEASES TO DRIVE MARKET

14 CONTRAST MEDIA MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 HOSPITALS, CLINICS, AND AMBULATORY SURGERY CENTERS

- 14.2.1 INCREASING ADOPTION OF DIAGNOSTIC IMAGING MODALITIES TO DRIVE MARKET

- 14.3 DIAGNOSTIC IMAGING CENTERS

- 14.3.1 INCREASING NUMBER OF PRIVATE IMAGING CENTERS TO PROPEL MARKET

15 CONTRAST MEDIA MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Rising incidence of chronic diseases to drive market

- 15.2.2 CANADA

- 15.2.2.1 Growth influenced by supply expansion and increasing market competition

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Presence of well-established players to support market growth

- 15.3.2 FRANCE

- 15.3.2.1 Growth supported by high imaging utilization and expanding clinical applications

- 15.3.3 UK

- 15.3.3.1 Innovation in next-generation MRI contrast agents to drive growth

- 15.3.4 ITALY

- 15.3.4.1 Growth driven by innovation in ultrasound contrast agents and product expansion

- 15.3.5 SPAIN

- 15.3.5.1 Shift toward safer and cost-efficient low-osmolar contrast agents in CT imaging to boost market

- 15.3.6 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Strong domestic capabilities and strategic supply chain position drive market growth

- 15.4.2 JAPAN

- 15.4.2.1 Advanced imaging infrastructure and strategic industry expansion to drive demand

- 15.4.3 INDIA

- 15.4.3.1 Expanding domestic manufacturing and increasing imaging demand to propel market growth

- 15.4.4 AUSTRALIA

- 15.4.5 SOUTH KOREA

- 15.4.5.1 AI-driven imaging optimization and rising early-onset cancer burden reshaping demand

- 15.4.6 REST OF ASIA PACIFIC

- 15.4.7 LATIN AMERICA

- 15.4.7.1 Cost-sensitive procurement and rising CT imaging volumes drive contrast media utilization

- 15.4.8 BRAZIL

- 15.4.8.1 Rising disease burden drives demand amid safety and access challenges

- 15.4.9 MEXICO

- 15.4.9.1 Rising CKD burden, low healthcare spending, and environmental concerns influence contrast media utilization

- 15.4.10 REST OF LATIN AMERICA

- 15.4.10.1 Fragmented access, import dependence, and public-private imbalance shaping contrast media utilization

- 15.4.11 MIDDLE EAST & AFRICA

- 15.4.11.1 High burden of chronic diseases to drive market

- 15.4.12 GCC COUNTRIES

- 15.4.12.1 Increasing government investments in healthcare sector and growing pharmaceuticals industry to drive market

- 15.4.13 REST OF MIDDLE EAST & AFRICA

- 15.4.13.1 Import dependence and unbalanced imaging access driving selective contrast media utilization

- 15.4.1 CHINA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 16.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN CONTRAST MEDIA MARKET

- 16.3 REVENUE ANALYSIS OF KEY PLAYERS IN CONTRAST MEDIA MARKET 2021-2025

- 16.4 MARKET SHARE ANALYSIS, 2024

- 16.4.1 MARKET RANKING OF KEY PLAYERS, 2024

- 16.5 COMPANY VALUATION & FINANCIAL METRICS

- 16.5.1 FINANCIAL METRICS

- 16.5.2 COMPANY VALUATION

- 16.6 BRAND/PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 PERVASIVE PLAYERS

- 16.7.3 EMERGING LEADERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Product type footprint

- 16.7.5.4 MODALITY FOOTPRINT

- 16.7.5.5 ROUTE OF ADMINISTRATION FOOTPRINT

- 16.7.5.6 INDICATION FOOTPRINT

- 16.7.5.7 END USER FOOTPRINT

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2025

- 16.8.5.1 CONTRAST MEDIA MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES & APPROVALS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 GE HEALTHCARE

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses & competitive threats

- 17.1.2 BRACCO IMAGING

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 BAYER AG

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 GUERBET

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product approvals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses & competitive threats

- 17.1.5 LANTHEUS HOLDINGS, INC.

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses & competitive threats

- 17.1.6 UNIJULES LIFE SCIENCES LTD.

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.7 J.B. CHEMICALS & PHARMACEUTICALS LIMITED

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.8 SANOCHEMIA PHARMAZEUTIKA

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.9 TAEJOON PHARM CO., LTD.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.10 JODAS EXPOIM

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.11 IMAX DIAGNOSTIC IMAGING LIMITED

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Pipeline products

- 17.1.12 YANGTZE RIVER PHARMACEUTICAL GROUP

- 17.1.12.1 Business overview

- 17.1.12.2 Pipeline products

- 17.1.13 LIVEALTH

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.14 BEIJING BEILU PHARMACEUTICAL CO., LTD.

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.1 GE HEALTHCARE

- 17.2 OTHER PLAYERS

- 17.2.1 ARCO LIFESCIENCES (I) PVT. LTD.

- 17.2.2 STANEX DRUGS & CHEMICALS PVT. LTD.

- 17.2.3 ONKO ILAC SAN. VE TIC. A.S.

- 17.2.4 FRESENIUS KABI

- 17.2.5 BIEM ILAC SAN. VE

- 17.2.6 ADVACARE PHARMA

- 17.2.7 FUJIFILM WAKO PURE CHEMICAL CORPORATION

- 17.2.8 UNISPIRE BIOPHARMA PRIVATE LIMITED

- 17.2.9 TRIVITRON HEALTHCARE

- 17.2.10 NANOPET PHARMA GMBH

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.2 RESEARCH DESIGN

- 18.2.1 SECONDARY RESEARCH

- 18.2.1.1 Objectives of secondary research

- 18.2.1.2 Key data from secondary sources

- 18.2.2 PRIMARY RESEARCH

- 18.2.2.1 Objectives of primary research

- 18.2.2.2 Key industry insights

- 18.2.1 SECONDARY RESEARCH

- 18.3 MARKET SIZE ESTIMATION METHODOLOGY

- 18.3.1 BOTTOM-UP APPROACH

- 18.3.1.1 Approach 1: Company revenue estimation approach

- 18.3.1.2 Approach 4: Primary interviews

- 18.3.2 TOP-DOWN APPROACH

- 18.3.1 BOTTOM-UP APPROACH

- 18.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.5 MARKET SHARE ASSESSMENT

- 18.6 RESEARCH ASSUMPTIONS

- 18.7 RESEARCH LIMITATIONS

- 18.8 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS