|

시장보고서

상품코드

2037095

데이터센터용 반도체 시장 : 프로세서별, DRAM 및 NAND별, 센서별, 연결성별, 전력별 - 세계 예측(-2029년)Data Center Semiconductor Market by Processor (GPU, TPU, Trainium, Inferentia, Biren, ASIC, CPU), DRAM & NAND, Sensor (Temperature, Humidity, Airflow), Connectivity (NIC/Ethernet Adapters, Switches, Interconnects), Power - Global Forecast to 2029 |

||||||

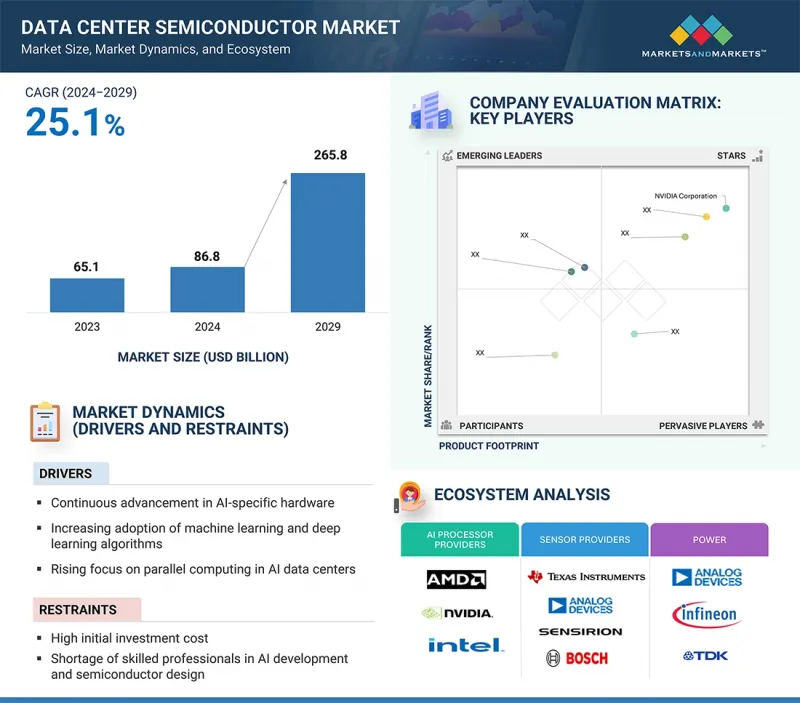

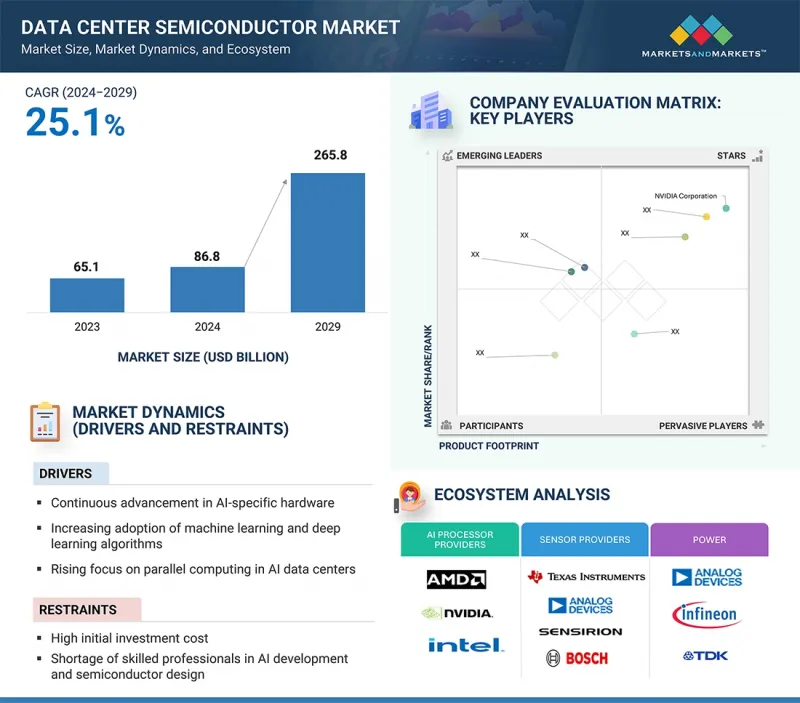

세계의 데이터센터용 반도체 시장 규모는 2024년 868억 달러에서 2029년까지 2,658억 달러에 달할 것으로 예측되며, 이 기간의 CAGR은 25.1%를 기록할 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2029년 |

| 기준 연도 | 2023년 |

| 예측 기간 | 2024-2029년 |

| 단위 | 10억 달러 |

| 부문 | 프로세서, 연결성, 전력, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

기업들은 콘텐츠 제작, 고객 서비스 자동화, 신약 개발, 개인화 마케팅 등을 위해 생성형 AI를 빠르게 도입하고 있습니다. 이러한 광범위한 채택으로 인해 고부하 워크로드를 처리할 수 있는 고성능 AI 서버에 대한 수요가 크게 증가하고 있습니다.

"파워스테이지 부문이 2029년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

파워스테이지 부문은 2029년 데이터센터용 반도체 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이는 주로 데이터센터 내 모든 핵심 구성요소의 효율적인 전력 변환 및 공급에 필수적인 구성요소이기 때문입니다. 현대의 AI 기반 워크로드, 특히 GPU와 커스텀 액셀러레이터를 활용하는 워크로드는 저전압의 초고전류를 필요로 하기 때문에 전력 공급 네트워크에 큰 부하를 가하고 있습니다. MOSFET 및 게이트 드라이버와 같은 요소를 통합한 파워 스테이지가 손실과 발열을 최소화하면서 이 전력을 효율적으로 변환하고 조정하는 데 필수적입니다. 서버 아키텍처의 전력 밀도가 높아짐에 따라 각 CPU, GPU, 메모리 모듈, 네트워크 칩에는 여러 개의 파워 스테이지가 필요하며, 서버당 탑재되는 파워 스테이지의 수가 많아지고 있습니다. 또한, 하이퍼스케일 데이터센터의 48V 배전 시스템으로의 업계 전반의 전환으로 인해 더 높은 입력 전압을 수용하고 정확한 출력을 제공할 수 있는 고급 고효율 파워 스테이지에 대한 수요가 증가하고 있습니다. 또한, 전력 비용의 상승과 지속가능성 목표에 따라 에너지 효율이 최우선 과제로 떠오르고 있습니다. 파워 스테이지는 변환 효율과 열 성능에 직접적인 영향을 미치기 때문에 데이터센터 사업자에게 매우 중요한 투자 분야가 되었습니다. 광범위한 배포, 높은 부가가치, 신뢰할 수 있고 효율적이며 확장 가능한 AI 인프라를 구현하는 데 필수적인 역할로 인해 시장 점유율의 대부분을 차지하고 있습니다.

"멀티채널 ADC/DAC가 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다."

멀티채널 ADC/DAC 부문은 점점 더 복잡해지고 전력 밀도가 높아지는 AI 인프라에서 실시간 모니터링 및 실시간 제어에 대한 요구가 증가함에 따라 데이터센터용 반도체 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다. 데이터센터가 HPC 및 AI 워크로드를 지원하기 위해 규모를 확장함에 따라 CPU, GPU, 메모리, 전력 공급 시스템 전반에 걸쳐 전압, 전류, 온도, 기류 등 여러 아날로그 신호를 동시에 모니터링해야 할 필요성이 증가하고 있습니다. 멀티채널 ADC는 다수의 아날로그 입력을 시스템 분석에 사용되는 디지털 데이터로 효율적으로 변환하고, DAC는 전력 및 열 관리 시스템을 세밀하게 제어할 수 있게 해줍니다. 지능형 소프트웨어 정의 데이터센터와 자율 최적화로의 전환은 이러한 컨버터가 폐쇄 루프 제어 시스템에서 필수적이기 때문에 그 채택을 더욱 가속화하고 있습니다. 또한, 48V 시스템 및 분산형 전력 관리와 같은 고급 전력 아키텍처의 보급에 따라 정확도와 응답성을 향상시키기 위해 높은 채널 수의 데이터 수집이 요구되고 있습니다. 단일 채널 솔루션에 비해 멀티채널 ADC/DAC는 높은 집적도, 기판 공간 절감, 시스템 비용 절감 등의 이점을 가지고 있어 그 매력이 더욱 커지고 있습니다. 예지보전을 가능하게 하고, 에너지 효율과 시스템 신뢰성을 높이는 역할로 인해 이러한 장치는 가장 빠른 성장이 예상됩니다.

세계의 데이터센터용 반도체 시장에 대해 조사 분석했으며, 주요 촉진요인, 저해요인, 과제, 기회, 2029년까지의 예측 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 시장 역학

제2장 시장 전망

제3장 부록

KSM 26.05.29The data center semiconductor market is expected to grow from USD 86.8 billion in 2024 to USD 265.8 billion by 2029, reflecting a 25.1% CAGR over the period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Processor, Connectivity, Power and Region |

| Regions covered | North America, Europe, APAC, RoW |

Enterprises are increasingly deploying generative AI for applications such as content creation, customer service automation, drug discovery, and personalized marketing. This widespread adoption is significantly increasing demand for high-performance AI servers capable of handling intensive workloads.

"Power stage segment will hold largest market share in 2029."

The power stage segment is projected to hold the largest share of the data center semiconductor market by 2029, primarily because it is fundamental to efficient power conversion and delivery across every critical component within a data center. Modern AI-driven workloads-especially those powered by GPUs and custom accelerators-require extremely high current at low voltages, placing significant demands on power delivery networks. Power stages, which integrate key elements such as MOSFETs and gate drivers, are essential for converting and regulating this power efficiently while minimizing losses and heat generation. As server architectures become more power-dense, each CPU, GPU, memory module, and networking chip requires multiple power stages, leading to high unit volumes per server. Additionally, the industry-wide shift toward 48V power distribution systems in hyperscale data centers is increasing the need for advanced, high-efficiency power stages capable of handling higher input voltages and delivering precise output. Furthermore, energy efficiency has become a top priority due to rising electricity costs and sustainability goals. Power stages directly influence conversion efficiency and thermal performance, making them a critical investment area for data center operators. Their widespread deployment, high value contribution, and essential role in enabling reliable, efficient, and scalable AI infrastructure collectively drive their dominant market share.

"Multi-channel ADC/DAC is estimated to record the highest CAGR during the forecast period."

The multi-channel ADC/DAC segment is expected to post the highest CAGR in the data center semiconductor market, driven by the growing need for precise, real-time monitoring and control in increasingly complex, power-dense AI infrastructure. As data centers scale to support high-performance computing and AI workloads, there is a growing need to monitor multiple analog signals simultaneously-such as voltage, current, temperature, and airflow-across CPUs, GPUs, memory, and power delivery systems. Multi-channel ADCs efficiently convert numerous analog inputs into digital data for system analytics, while DACs enable fine-grained control of power and thermal management systems. The transition toward intelligent, software-defined data centers and autonomous optimization further accelerates adoption, as these converters are critical to closed-loop control systems. Additionally, the proliferation of advanced power architectures-such as 48V systems and distributed power management-requires high-channel-count data acquisition to improve accuracy and responsiveness. Compared with single-channel solutions, multi-channel ADC/DACs offer higher integration, reduced board space, and lower system cost, making them increasingly attractive. Their role in enabling predictive maintenance, energy efficiency, and system reliability positions them for the fastest growth.

Extensive primary interviews were conducted with key industry experts in the data center semiconductor market to determine and verify the market size for segments and subsegments identified through secondary research. The breakdown of primary participants for the report is provided below:

The study contains insights from various industry experts, including component suppliers, Tier 1 companies, and OEMs. The breakdown of the primary participants is as follows:

- By Company Type: Tier 1-50%, Tier 2-20%, and Tier 3-30%

- By Designation: C-level-20%, Directors-30%, and Others-50%

- By Region: North America-40%, Europe-20%, Asia Pacific-30%, and RoW-10%

Research Coverage:

This research report categorizes the data center semiconductor market by processor type, DRAM & NAND, sensors, power, connectivity, and other analog devices. It describes the major drivers, restraints, challenges, and opportunities in the data center semiconductor market and forecasts the market through 2029.

Key Benefits of Buying the Report

The report will provide market leaders and new entrants with the closest approximations of the overall data center semiconductor market and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to position their businesses more effectively and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (continuous advancement in AI-specific hardware), restraints (high initial investment costs), opportunities (planned investments in data centers by cloud service providers), and challenges (supply chain disruptions).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the data center semiconductor market

- Market Development: Comprehensive information about lucrative markets

- Competitive Assessment: In-depth assessment of market share and growth strategies

TABLE OF CONTENTS

1 MARKET DYNAMICS

- 1.1 ANALYSIS OF KEY DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 1.1.1 MARKET DYNAMICS - DRIVERS

- 1.1.1.1 In-house development of AI-specific hardware by hyperscalers such as TPU (Google), Trainium (AWS), Inferencia (AWS), and Maia 100 (Meta)

- 1.1.1.2 High demand for dedicated AI processors with surging need for parallel computing in hyperspectral data centers

- 1.1.2 MARKET DYNAMICS - RESTRAINTS

- 1.1.2.1 Extended lead time for enterprise customers due to demand-supply imbalance for GPUs

- 1.1.3 MARKET DYNAMICS - OPPORTUNITIES

- 1.1.3.1 Accelerating AI-optimized data center expansion by hyperscalers

- 1.1.4 MARKET DYNAMICS - CHALLENGES

- 1.1.4.1 NVIDIA's dominance in data center GPUs creating ecosystem dependence

- 1.1.1 MARKET DYNAMICS - DRIVERS

- 1.2 DATA CENTER ECOSYSTEM

- 1.2.1 CPU SERVER COST STRUCTURE/BILL OF MATERIAL (BOM)

- 1.2.2 SERVERS WITH NVIDIA A100 GPUS COST ~15X MORE THAN STANDARD CPU SERVERS

- 1.2.3 SERVERS WITH NVIDIA H100 GPUS COST ~32X MORE THAN CPU SERVERS AND ~2X MORE THAN A100-BASED SYSTEMS

- 1.2.4 AI SERVER ADOPTION AND MARKET GROWTH OUTLOOK

- 1.2.4.1 30% of data center servers to be equipped with AI semiconductors by 2029

- 1.3 DATA PROTECTION-, LOCALIZATION-, AND AI-RELATED NORMS

- 1.3.1 DATA PROTECTION AND LOCALIZATION NORMS DRIVING DATA CENTER INVESTMENT IN EMERGING COUNTRIES

- 1.3.2 ARTIFICIAL INTELLIGENCE (AI) REGULATORY LANDSCAPE

- 1.3.2.1 Global regulatory efforts to address AI-related risks

- 1.3.2.1.1 Global overview of AI regulatory frameworks and policy drivers

- 1.3.2.1 Global regulatory efforts to address AI-related risks

- 1.4 UPCOMING DATA CENTER DEPLOYMENTS BY HYPERSCALERS

- 1.4.1 CLOUD SERVICE PROVIDER-LED DATA CENTER EXPANSION IN FUTURE, BY REGION

- 1.5 GENERATIVE AI: EMERGING OPPORTUNITY FOR HYPERSCALERS

- 1.5.1 GENERATIVE AI: TRANSFORMATIVE OPPORTUNITY FOR HYPERSCALERS

- 1.5.2 RAPID UPGRADES OF HARDWARE BY HYPERSCALERS TO SUPPORT GENERATIVE AI

- 1.5.2.1 Strategic investments in AI infrastructure fueling generative AI ecosystem

- 1.5.3 HYPERSCALERS GROWTH IN GENERATIVE AI

- 1.5.3.1 Generative AI expansion fueling AI infrastructure development in data centers

- 1.6 CAPITAL EXPENDITURE AND GROWTH OUTLOOK FOR CLOUD SERVICE PROVIDERS (2020-2029)

- 1.6.1 CSP INVESTMENTS IN IT AND DATA CENTER INFRASTRUCTURE DRIVEN BY AI GROWTH

- 1.7 GPU POWER RATING

- 1.7.1 DATA CENTER GPU INNOVATIONS WITH HIGHER TDP TO POWER ADVANCED AI COMPUTING

- 1.8 DATA CENTER POWER CONSUMPTION

- 1.8.1 DATA CENTER POWER CONSUMPTION TO INCREASE ~10X IN NEXT FIVE YEARS

- 1.9 AI SEMICONDUCTOR MARKET, 2023-2029

- 1.9.1 AI SEMICONDUCTOR MARKET, BY PROCESSOR, 2023-2029

- 1.9.2 AI SEMICONDUCTOR MARKET, BY SENSOR, 2023-2029

- 1.9.3 AI SEMICONDUCTOR MARKET, BY CONNECTIVITY, 2023-2029

- 1.9.4 AI SEMICONDUCTOR MARKET, BY POWER, 2023-2029

- 1.9.5 AI SEMICONDUCTOR MARKET, BY OTHER ANALOG, 2023-2029

2 MARKET POTENTIAL

- 2.1 CLOUD DATA CENTER SEMICONDUCTOR MARKET, 2023-2029

- 2.2 CLOUD DATA CENTER SEMICONDUCTOR MARKET, BY PRODUCT, 2023-2029

- 2.2.1 CLOUD DATA CENTER: AI SEMICONDUCTOR MARKET, BY PROCESSOR TYPE, 2023-2029

- 2.2.2 CLOUD DATA CENTER: AI SEMICONDUCTOR MARKET, BY DRAM & NAND, 2023-2029

- 2.2.3 CLOUD DATA CENTER: AI SEMICONDUCTOR MARKET, BY CONNECTIVITY DEVICE, 2023-2029

- 2.2.4 CLOUD DATA CENTER: AI SEMICONDUCTOR MARKET, BY POWER COMPONENT, 2023-2029

- 2.2.5 CLOUD DATA CENTER: AI SEMICONDUCTOR MARKET, BY OTHER ANALOG COMPONENT, 2023-2029

- 2.3 REVENUE SHARE OF CLOUD SERVICE PROVIDERS, BY INDUSTRY, 2023

- 2.3.1 CLOUD SERVICE PROVIDERS: INDUSTRY REVENUE DISTRIBUTION, 2023

- 2.4 PROCUREMENT OF SERVERS BY CLOUD SERVICE PROVIDERS (IN VOLUME) FROM 2020 TO 2029

- 2.4.1 MICROSOFT WAS LARGEST AI SERVER BUYER IN 2023 WITH ~22% OF SHARE IN 2023

- 2.5 COMPETITIVE LANDSCAPE

- 2.5.1 COMPANY-WISE SHARE ANALYSIS: DATA CENTER EDGE PROCESSOR MARKET, 2023 VS. 2024

- 2.5.2 IMPLICATION FOR ANALOG DEVICES IN CLOUD DATA CENTER MARKET

3 APPENDIX

- 3.1 LIST OF ABBREVIATIONS

- 3.2 MARKET DEFINITION

- 3.2.1 AI SEMICONDUCTOR TAM, 2023

- 3.3 RESEARCH METHODOLOGY

- 3.3.1 FRAMEWORK FOR PROCESSOR TAM ESTIMATION

- 3.3.1.1 Processor TAM, 2023

- 3.3.2 FRAMEWORK FOR SENSOR TAM ESTIMATION

- 3.3.2.1 Sensor TAM, 2023

- 3.3.3 FRAMEWORK FOR CONNECTIVITY DEVICE TAM ESTIMATION

- 3.3.3.1 Connectivity device TAM, 2023

- 3.3.4 FRAMEWORK FOR POWER COMPONENT TAM ESTIMATION

- 3.3.4.1 Power component TAM, 2023

- 3.3.5 FRAMEWORK FOR OTHER ANALOG COMPONENTS TAM ESTIMATION

- 3.3.5.1 Other analog components TAM, 2023

- 3.3.6 FRAMEWORK FOR DRAM & NAND TAM ESTIMATION

- 3.3.6.1 DRAM & NAND market size calculation, 2023

- 3.3.7 COMPARISON OF GENERATIVE AI CLOUD PLATFORMS

- 3.3.1 FRAMEWORK FOR PROCESSOR TAM ESTIMATION