|

시장보고서

상품코드

2038240

클라우드 보안 시장 예측(-2031년) : 유형(CNAPP(CWPP, CSPM, CIEM, CDR, KSPM, IAC Security), CASB, 분석 및 모니터링), 도입 형태(프라이빗, 퍼블릭, 하이브리드), 산업별(의료, 소매 및 E-Commerce, 미디어 및 엔터테인먼트)Cloud Security Market by Type (CNAPP [CWPP, CSPM, CIEM, CDR, KSPM, IAC Security], CASB, Analytics and Monitoring), Deployment Mode (Private, Public, Hybrid), Vertical (Healthcare, Retail & E-commerce, Media & Entertainment) - Global Forecast to 2031 |

||||||

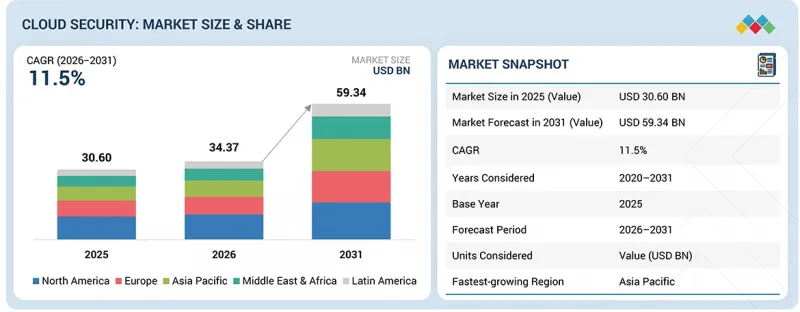

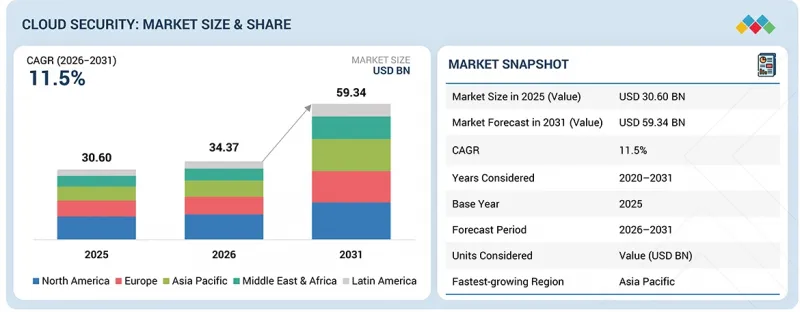

클라우드 보안 시장 규모는 2026년 343억 7,000만 달러에서 2031년에는 593억 4,000만 달러로 성장하며, CAGR은 11.5%에 달할 것으로 예측됩니다.

DevSecOps와 클라우드 네이티브 개발 기법의 확산으로 애플리케이션의 수명주기 초기 단계부터 보안이 통합되면서 지속적인 모니터링, 자동 테스트, 실시간 시정 조치를 제공하는 툴에 대한 수요가 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제공, 유형, 도입 형태, 조직 규모, 산업 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

동시에 멀티클라우드 및 하이브리드 클라우드 환경의 도입이 확대됨에 따라 일관된 가시성과 정책 적용을 보장하는 통합 보안 플랫폼에 대한 요구가 증가하고 있습니다. 이러한 요인들로 인해 동적 워크로드를 보호하고 빠르고 확장 가능한 애플리케이션 개발을 지원할 수 있는 통합 클라우드 보안 솔루션에 대한 투자가 가속화되고 있습니다.

서비스 부문은 예측 기간 중 가장 높은 성장률을 기록할 것으로 예상됩니다.

클라우드 보안 시장에서 서비스 부문은 조직이 복잡하고 다양한 멀티클라우드 환경과 끊임없이 변화하는 위협 상황을 관리하기 위해 외부 전문 지식에 대한 의존도가 높아지면서 성장세를 보이고 있습니다. 기업은 CNAPP, 제로 트러스트, AI 기반 보안 솔루션 등 고도화된 플랫폼을 도입하고 최적화하기 위해 컨설팅, 통합, 관리형 보안 서비스를 요구하고 있습니다.

팔로알토 네트웍스에 따르면 2025년에는 상당수의 대기업 고객이 프리즈마 클라우드 및 Cortex 플랫폼 도입을 가속화하기 위해 전문 서비스를 이용할 것으로 예상됩니다. IBM은 2024년, 조직이 기술 부족을 해소하고 업무 효율성을 높이기 위해 관리형 보안 서비스에 대한 수요가 증가할 것이라고 강조했습니다.

서비스는 조직이 보안 전략을 규제 요건과 비즈니스 목표에 맞게 조정하는 데 있으며, 매우 중요한 역할을 합니다. 하이브리드 및 멀티클라우드 환경이 복잡해짐에 따라 지속적인 모니터링, 사고 대응, 컴플라이언스 관리가 필요하지만, 많은 기업이 이를 아웃소싱하는 것을 선호하고 있습니다. 각 벤더들은 AI를 활용한 위협 분석, 자동화, 예방적 리스크 관리 등 서비스 제공 범위를 확장하고 있습니다. 사이버 위협이 고도화되고 조직이 숙련된 전문가 부족에 직면함에 따라 클라우드 보안 서비스에 대한 수요는 지속적으로 강세를 보일 것으로 예상되며, 이는 고급 보안 플랫폼의 장기적인 도입을 지원할 것으로 보입니다.

"도입 형태별로는 프라이빗 클라우드 부문이 2026년 가장 큰 시장 점유율을 차지할 것으로 전망"

특히 규제가 엄격한 산업에서 조직이 관리, 데이터 주권, 컴플라이언스를 우선시하는 가운데, 프라이빗 클라우드 부문은 클라우드 보안 시장에서 지속적으로 큰 비중을 차지하고 있습니다. 민감한 데이터를 다루는 기업은 엄격한 거버넌스 및 보안 관리를 보장하면서 확장성을 위해 퍼블릭 클라우드 서비스와 통합하기 위해 프라이빗 클라우드 환경에 의존하는 경우가 많습니다. 시스코에 따르면 2025년에도 많은 기업이 프라이빗 또는 하이브리드 클라우드 환경을 계속 운영할 것으로 예상되며, 이는 안전한 온프레미스 인프라의 중요성을 강조합니다. 마이크로소프트는 2024년 많은 조직이 중요한 워크로드를 프라이빗 환경에 유지하면서 퍼블릭 클라우드로 기능을 확장하고 있다고 지적했습니다.

프라이빗 클라우드를 도입하면 조직은 맞춤형 보안 정책을 구현하고, 인프라를 직접 관리하며, 규제 요건을 충족할 수 있습니다. 보안 업체들은 프라이빗 클라우드와 퍼블릭 클라우드 환경 간의 원활한 통합을 실현하고, 일관된 가시성과 위협 탐지를 보장하는 솔루션을 강화하고 있습니다. 기업이 유연성과 제어의 균형을 모색하는 가운데 하이브리드 아키텍처의 부상으로 프라이빗 클라우드 보안의 중요성이 더욱 커지고 있습니다. 규제 압력과 데이터 보호 요구사항이 계속 진화하는 가운데, 프라이빗 클라우드 환경은 기업의 클라우드 전략에서 여전히 중요한 요소로 남아 있습니다.

"산업별로는 BFSI 부문이 2026년 가장 큰 시장 점유율을 차지할 것으로 전망"

BFSI 부문은 금융 데이터의 극도로 민감한 특성과 금융 기관을 대상으로 한 사이버 공격의 빈도가 증가함에 따라 클라우드 보안 시장에서 지배적인 위치를 차지하고 있습니다. 은행과 금융 서비스 제공업체들은 디지털 뱅킹 플랫폼, 결제 시스템, 고객 데이터를 보호하기 위해 첨단 클라우드 보안 솔루션에 투자하고 있습니다.

Zscaler에 따르면 2025년에는 분산된 운영을 보호하기 위해 제로 트러스트 아키텍처를 채택하는 BFSI 고객이 기업 도입의 대부분을 차지할 것으로 예상된다고 합니다. 마이크로소프트는 2024년 금융기관이 가장 큰 타깃이 되는 분야 중 하나이며, 위협 탐지 및 컴플라이언스를 위한 통합 보안 플랫폼의 도입을 촉진하고 있다고 지적했습니다.

디지털 뱅킹, 핀테크 혁신, 실시간 결제 시스템으로의 전환은 공격 대상 영역을 확대하고 있으며, 강력한 ID 보안, 데이터 보호, 지속적인 모니터링 기능이 요구되고 있습니다. 규제 요건과 컴플라이언스 프레임워크도 안전한 클라우드 환경에 대한 투자를 촉진하고 있습니다. 각 벤더들은 부정행위 탐지, 신원 확인, 안전한 접근 관리 등 BFSI 고유의 위험에 대응하기 위한 맞춤형 솔루션을 제공하고 있습니다. 금융기관이 인프라 현대화를 추진하는 가운데, 클라우드 보안은 탄력성과 신뢰성을 확보하기 위한 중요한 우선순위가 되고 있습니다.

세계의 클라우드 보안(Cloud Security) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 소비자의 상황과 구매 행동

제9장 클라우드 보안 시장 : 제공별

제10장 클라우드 보안 시장 : 유형별

제11장 클라우드 보안 시장 : 도입 형태별

제12장 클라우드 보안 시장 : 조직 규모별

제13장 클라우드 보안 시장 : 산업별

제14장 클라우드 보안 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSA 26.06.01The cloud security market is projected to grow from USD 34.37 billion in 2026 to USD 59.34 billion by 2031, at a compound annual growth rate (CAGR) of 11.5%. The growth of DevSecOps and cloud-native development practices is embedding security earlier in the application lifecycle, driving demand for tools that provide continuous monitoring, automated testing, and real-time remediation.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, By Type, By Deployment Mode, By Organization Size, By Vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

At the same time, increasing adoption of multi-cloud and hybrid cloud environments is creating the need for unified security platforms that ensure consistent visibility and policy enforcement. These factors are accelerating investments in integrated cloud security solutions that can protect dynamic workloads and support rapid, scalable application development.

By offering, the services segment is expected to record the fastest growth rate during the forecast period.

The services segment is gaining momentum in the cloud security market as organizations increasingly rely on external expertise to manage complex, multicloud environments and evolving threat landscapes. Enterprises are seeking consulting, integration, and managed security services to deploy and optimize advanced platforms, including CNAPP, zero trust, and AI-driven security solutions. According to Palo Alto Networks, in 2025, a significant share of its large enterprise customers will engage with professional services to accelerate adoption of the Prisma Cloud and Cortex platforms. IBM highlighted in 2024 that managed security services are experiencing growing demand as organizations seek to address skill shortages and improve operational efficiency. Services play a critical role in enabling organizations to align security strategies with regulatory requirements and business objectives. The growing complexity of hybrid and multi-cloud environments requires continuous monitoring, incident response, and compliance management, which many enterprises prefer to outsource. Vendors are expanding their service offerings to include AI-driven threat analysis, automation, and proactive risk management. As cyber threats become more sophisticated and organizations face a shortage of skilled professionals, the demand for cloud security services is expected to remain strong, supporting long-term adoption of advanced security platforms.

"By deployment mode, the private cloud segment is expected to hold the largest market share in 2026. "

The private cloud segment continues to hold a significant share of the cloud security market as organizations prioritize control, data sovereignty, and compliance, especially in regulated industries. Enterprises handling sensitive data often rely on private cloud environments to ensure strict governance and security controls while integrating with public cloud services for scalability. According to Cisco, in 2025, a large proportion of enterprises will continue to operate private or hybrid cloud environments, highlighting the importance of secure on-premises infrastructure. Microsoft noted in 2024 that many organizations maintain critical workloads in private environments while extending capabilities to the public cloud. Private cloud deployments allow organizations to implement customized security policies, maintain direct oversight of infrastructure, and meet regulatory requirements. Security vendors are enhancing solutions to provide seamless integration between private and public cloud environments, ensuring consistent visibility and threat detection. The rise of hybrid architectures reinforces the relevance of private cloud security, as enterprises seek to balance flexibility with control. As regulatory pressures and data protection requirements continue to evolve, private cloud environments remain a critical component of enterprise cloud strategies.

"By vertical, the BFSI segment is projected to hold the largest market share in 2026."

The BFSI segment holds a dominant position in the cloud security market due to the highly sensitive nature of financial data and the increasing frequency of cyberattacks targeting financial institutions. Banks and financial service providers are investing in advanced cloud security solutions to protect digital banking platforms, payment systems, and customer data. According to Zscaler, in 2025, a significant portion of its enterprise deployments will be driven by BFSI customers adopting zero-trust architectures to secure distributed operations. Microsoft highlighted in 2024 that financial institutions are among the most targeted sectors, driving adoption of integrated security platforms for threat detection and compliance. The shift toward digital banking, fintech innovation, and real-time payment systems is expanding the attack surface and requiring robust identity security, data protection, and continuous monitoring capabilities. Regulatory requirements and compliance frameworks are also driving investment in secure cloud environments. Vendors are offering tailored solutions to address BFSI-specific risks, including fraud detection, identity verification, and secure access management. As financial institutions continue to modernize their infrastructure, cloud security remains a critical priority for ensuring resilience and trust.

Breakdown of Primaries

The study draws insights from a range of industry experts, including component suppliers, Tier 1 companies, and OEMs. The breakdown of the primaries is as follows:

- By Company Type: Tier 1 - 25%, Tier 2 - 30%, and Tier 3 - 45%

- By Designation: C-level - 40%, Managerial & Other Levels - 60%

- By Region: North America - 35%, Europe - 25%, Asia Pacific - 35%, Middle East and Africa - 5%, Latin America - 5%

Major vendors in the cloud security market include Microsoft (US), Palo Alto Networks (US), AWS (US), Wiz (US), Zscaler (US), Fortinet (US), Akamai (US), Cloudflare (US), IBM (US), CrowdStrike (US), SentinelOne (US), Check Point (Israel), Trend Micro (Japan), Cisco (US), Netskope (US), Qualys (US), Tenable (US), Rapid7 (US), Orca Security (US), Sysdig (US), Menlo Security (US), Aqua Security (US), SecPod (India), Plexicus (Spain), and Upwind Security (US).

The study includes an in-depth competitive analysis of the key players in the cloud security market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the cloud security market and forecasts its size based on offerings ( platforms/solutions, services), types (CNAPP, CASB, analytics & monitoring) deployment modes (private cloud, public cloud, hybrid cloud), organization sizes (large enterprises, SMEs), verticals (BFSI, government & defense, IT & telecommunications, healthcare & life sciences, retail & ecommerce, manufacturing, energy & utilities, transportation and logistics, travel & hospitality, media & entertainment, other verticals), and regions (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall cloud security market and its subsegments. This report will help stakeholders understand the competitive landscape and gain valuable insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (Increasing adoption of multicloud and hybrid cloud environments, growth of DevSecOps and cloud-native development practices, rising frequency and sophistication of cyber threats, stringent regulatory and data protection requirements), restraints (Complexity in managing multicloud security environments, high implementation and operational costs), opportunities (Expansion of cloud computing and digital transformation initiatives, growth of mobile computing and remote workforce models, increasing adoption of IoT and connected devices, shift toward zero trust and identity-first security models, adoption of AI-driven and automated cloud security solutions), and challenges (Shortage of skilled cloud security professionals, limited visibility and control across distributed cloud environments)

- Product Development/Innovation: Detailed insights on upcoming technologies, research development activities, new products, and service launches in the cloud security market

- Market Development: Comprehensive information about lucrative markets (The report analyses the cloud security market across varied regions.)

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the cloud security market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players Microsoft (US), Palo Alto Networks (US), AWS (US), Wiz (US), Zscaler (US), Fortinet (US), Akamai (US), Cloudflare (US), IBM (US), CrowdStrike (US), SentinelOne (US), Check Point (Israel), Trend Micro (Japan), Cisco (US), Netskope (US), Qualys (US), Tenable (US), and Rapid7 (US), among others, in the cloud security market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CLOUD SECURITY MARKET

- 3.2 CLOUD SECURITY MARKET, BY OFFERING

- 3.3 CLOUD SECURITY MARKET, BY SERVICE

- 3.4 CLOUD SECURITY MARKET, BY PROFESSIONAL SERVICE

- 3.5 CLOUD SECURITY MARKET, BY TYPE

- 3.6 CLOUD SECURITY MARKET, BY DEPLOYMENT MODE

- 3.7 CLOUD SECURITY MARKET, BY ORGANIZATION SIZE

- 3.8 CLOUD SECURITY MARKET, BY VERTICAL

- 3.9 CLOUD SECURITY MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing adoption of multi-cloud and hybrid cloud environments

- 4.2.1.2 Growth of DevSecOps and cloud-native development practices

- 4.2.1.3 Rising frequency and sophistication of cyber threats

- 4.2.1.4 Stringent regulatory and data protection requirements

- 4.2.2 RESTRAINTS

- 4.2.2.1 Complexity in managing multi-cloud security environments

- 4.2.2.2 High implementation and operational costs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of cloud computing and digital transformation initiatives

- 4.2.3.2 Growth of mobile computing and remote workforce models

- 4.2.3.3 Growth of mobile computing and remote workforce model

- 4.2.3.4 Increasing adoption of IoT and connected devices

- 4.2.3.5 Shift toward zero trust and identity-first security models

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of skilled cloud security professionals

- 4.2.4.2 Limited visibility and control across distributed cloud environments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 CROSS-TIER STRATEGIC PATTERNS

- 4.5.2 STRATEGIC TRENDS

- 4.5.2.1 Adoption of Zero Trust and Identity-centric Security

- 4.5.2.2 AI- and ML-driven Cloud Security

- 4.5.2.3 Growth of Cloud-native and Continuous Security

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL CYBERSECURITY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY PLATFORM/ SOLUTION, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY VENDOR (2025)

- 5.6 KEY CONFERENCES AND EVENTS IN 2026-2027

- 5.7 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 AWS ENHANCED MULTI-CLOUD SECURITY POSTURE FOR CAPITAL ONE USING CLOUD-NATIVE SECURITY SERVICES

- 5.9.2 MICROSOFT SECURED ENTERPRISE WORKLOADS FOR HEINEKEN WITH AZURE SECURITY PLATFORM

- 5.9.3 PALO ALTO NETWORKS ENABLED ZERO TRUST SECURITY FOR BMW GROUP

- 5.9.4 CROWDSTRIKE PROTECTED CLOUD WORKLOADS FOR SHOPIFY USING FALCON PLATFORM

- 5.9.5 ZSCALER ENABLED SECURE REMOTE ACCESS FOR SIEMENS WITH SASE PLATFORM

- 5.10 IMPACT OF 2025 US TARIFF - CLOUD SECURITY MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 North America

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Encryption

- 6.1.1.2 Multi-factor Authentication (MFA)

- 6.1.1.3 Role-based Access Control (RBAC)

- 6.1.1.4 Microsegmentation

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 AI/ML

- 6.1.2.2 User and Entity Behavior Analytics (UEBA)

- 6.1.2.3 Security Orchestration, Automation, and Response (SOAR)

- 6.1.2.4 Serverless Computing

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Secure Access Service Edge (SASE)

- 6.1.3.2 Edge Computing

- 6.1.3.3 Confidential Computing

- 6.1.3.4 Blockchain

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY ROADMAP

- 6.2.1 SHORT-TERM (2026-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.2.2 MID-TERM (2027-2030) SCALING, INTELLIGENCE & ECOSYSTEM EXPANSION

- 6.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS, REAL-TIME & ADAPTIVE SECURITY

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AUTONOMOUS AND AI-DRIVEN CLOUD SECURITY PLATFORMS

- 6.4.2 DATA-CENTRIC SECURITY AND PREDICTIVE RISK ANALYTICS

- 6.4.3 IDENTITY-FIRST AND ZERO TRUST SECURITY MODELS

- 6.4.4 UNIFIED SECURITY ACROSS EDGE, CLOUD, AND SERVERLESS ENVIRONMENTS

- 6.4.5 CONFIDENTIAL AND DECENTRALIZED SECURITY FRAMEWORKS

- 6.5 IMPACT OF AI/GEN AI ON CLOUD SECURITY MARKET

- 6.5.1 BEST PRACTICES IN CLOUD SECURITY MARKET

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN CLOUD SECURITY MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN CLOUD SECURITY MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 MICROSOFT: AI-DRIVEN CLOUD SECURITY TRANSFORMATION FOR GLOBAL ENTERPRISE

- 6.6.2 WIZ: CONTEXTUAL CLOUD RISK MANAGEMENT FOR GLOBAL ENTERPRISE

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CONSUMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.4.1 REVENUE POTENTIAL

- 8.4.2 COST DYNAMICS

- 8.4.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 CLOUD SECURITY MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: CLOUD SECURITY MARKET DRIVERS

- 9.2 PLATFORMS/SOLUTIONS

- 9.2.1 INCREASING ADOPTION OF CLOUD-NATIVE AND PLATFORM-BASED SECURITY SOLUTIONS TO PROTECT MULTI-CLOUD ENVIRONMENTS AND CLOUD WORKLOADS

- 9.3 SERVICES

- 9.3.1 INCREASING RELIANCE ON MANAGED AND PROFESSIONAL CLOUD SECURITY SERVICES TO ADDRESS SKILL GAPS AND COMPLEX SECURITY REQUIREMENTS

- 9.3.2 PROFESSIONAL SERVICES

- 9.3.2.1 Consulting & Advisory

- 9.3.2.2 Integration & Deployment

- 9.3.2.3 Training & education

- 9.3.2.4 Support & maintenance

- 9.3.3 MANAGED SERVICES

10 CLOUD SECURITY MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.1.1 TYPE: CLOUD SECURITY MARKET DRIVERS

- 10.2 CLOUD-NATIVE APPLICATION PROTECTION PLATFORMS (CNAPP)

- 10.2.1 INCREASING ADOPTION OF CNAPP SOLUTIONS TO SECURE CLOUD WORKLOADS, CONFIGURATIONS, AND ENTITLEMENTS ACROSS MULTI-CLOUD ENVIRONMENTS

- 10.2.2 CWPP

- 10.2.3 CSPM

- 10.2.4 CIEM

- 10.2.5 CDR

- 10.2.6 KSPM

- 10.2.7 IAC SECURITY

- 10.2.8 OTHERS (DSPM, API SECURITY INTEGRATION, SAST, SCA, ATTACK PATH ANALYSIS)

- 10.3 CLOUD ACCESS SECURITY BROKER (CASB)

- 10.3.1 INCREASING ADOPTION OF CASB SOLUTIONS TO ENABLE SECURE ACCESS TO CLOUD APPLICATIONS AND SUPPORT ZERO-TRUST ARCHITECTURES

- 10.4 ANALYTICS & MONITORING

- 10.4.1 INCREASING ADOPTION OF CLOUD-NATIVE SECURITY ANALYTICS AND MONITORING SOLUTIONS TO ENABLE REAL-TIME THREAT DETECTION AND RESPONSE

11 CLOUD SECURITY MARKET, BY DEPLOYMENT MODE

- 11.1 INTRODUCTION

- 11.1.1 DEPLOYMENT MODE: CLOUD SECURITY MARKET DRIVERS

- 11.2 PRIVATE CLOUD

- 11.2.1 INCREASING ADOPTION OF PRIVATE CLOUD SECURITY SOLUTIONS TO ENABLE GREATER CONTROL AND COMPLIANCE FOR SENSITIVE WORKLOADS

- 11.3 PUBLIC CLOUD

- 11.3.1 INCREASING ADOPTION OF PUBLIC CLOUD SECURITY SOLUTIONS TO PROTECT SCALABLE AND DYNAMIC CLOUD ENVIRONMENTS

- 11.4 HYBRID CLOUD

- 11.4.1 INCREASING ADOPTION OF HYBRID CLOUD SECURITY SOLUTIONS TO ENABLE UNIFIED SECURITY ACROSS DISTRIBUTED CLOUD ENVIRONMENTS

12 CLOUD SECURITY MARKET, BY ORGANIZATION SIZE

- 12.1 INTRODUCTION

- 12.1.1 ORGANIZATION SIZE: CLOUD SECURITY MARKET DRIVERS

- 12.2 LARGE ENTERPRISES

- 12.2.1 INCREASING ADOPTION OF ADVANCED AND INTEGRATED CLOUD SECURITY PLATFORMS TO SECURE COMPLEX MULTI-CLOUD ENVIRONMENTS

- 12.3 SMALL & MEDIUM-SIZED ENTERPRISES

- 12.3.1 INCREASING ADOPTION OF CLOUD-BASED AND MANAGED SECURITY SOLUTIONS TO ENABLE COST-EFFECTIVE PROTECTION FOR SMES

13 CLOUD SECURITY MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 VERTICAL: CLOUD SECURITY MARKET DRIVERS

- 13.2 BANKING, FINANCIAL SERVICES, AND INSURANCE (BFSI)

- 13.2.1 STRINGENT REGULATORY ENVIRONMENTS AND HIGH-VALUE DATA DRIVING ADVANCED CLOUD SECURITY ADOPTION IN BFSI

- 13.3 HEALTHCARE & LIFE SCIENCES

- 13.3.1 PROTECTION OF SENSITIVE PATIENT DATA AND SECURE DATA SHARING DRIVING CLOUD SECURITY INVESTMENTS IN HEALTHCARE

- 13.4 IT & TELECOMMUNICATIONS

- 13.4.1 CLOUD-NATIVE ARCHITECTURES AND HIGH API EXPOSURE DRIVING ADVANCED SECURITY REQUIREMENTS IN IT & TELECOM

- 13.5 GOVERNMENT & DEFENSE

- 13.5.1 NATIONAL SECURITY PRIORITIES AND CRITICAL INFRASTRUCTURE PROTECTION SHAPING CLOUD SECURITY ADOPTION IN GOVERNMENT SECTOR

- 13.6 RETAIL & E-COMMERCE

- 13.6.1 DIGITAL COMMERCE EXPANSION AND CUSTOMER DATA PROTECTION DRIVING CLOUD SECURITY DEMAND IN RETAIL

- 13.7 MANUFACTURING

- 13.7.1 CONVERGENCE OF IT, OT, AND CLOUD SYSTEMS EXPANDING ATTACK SURFACE IN MANUFACTURING ENVIRONMENTS

- 13.8 ENERGY & UTILITIES

- 13.8.1 PROTECTION OF CRITICAL INFRASTRUCTURE AND CLOUD-ENABLED GRID SYSTEMS DRIVING SECURITY INVESTMENTS

- 13.9 MEDIA & ENTERTAINMENT

- 13.9.1 CONTENT PROTECTION, DIGITAL RIGHTS MANAGEMENT, AND HIGH-VOLUME USER TRAFFIC SHAPING CLOUD SECURITY REQUIREMENTS

- 13.10 TRANSPORTATION & LOGISTICS

- 13.10.1 DIGITALIZATION OF SUPPLY CHAINS AND CONNECTED TRANSPORT SYSTEMS INTRODUCING NEW CLOUD SECURITY RISKS

- 13.11 TRAVEL & HOSPITALITY

- 13.11.1 HIGH CUSTOMER DATA EXPOSURE AND DIGITAL BOOKING ECOSYSTEMS DRIVING SECURITY PRIORITIES IN TRAVEL INDUSTRY

- 13.12 OTHER VERTICALS

14 CLOUD SECURITY MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: CLOUD SECURITY MARKET DRIVERS

- 14.2.2 US

- 14.2.2.1 Rising national security concerns, AI adoption, and federal investments driving cloud security market growth in US

- 14.2.3 CANADA

- 14.2.3.1 Strengthening cyber resilience amid geopolitical risks and data protection mandates driving cloud security adoption in Canada

- 14.3 EUROPE

- 14.3.1 EUROPE: CLOUD SECURITY MARKET DRIVERS

- 14.3.2 UK

- 14.3.2.1 Advancing national cyber resilience and secure cloud adoption through regulatory frameworks and AI-driven security investments in the UK

- 14.3.3 GERMANY

- 14.3.3.1 Data sovereignty, industrial digitalization, and critical infrastructure protection driving cloud security demand in Germany

- 14.3.4 FRANCE

- 14.3.4.1 Government-backed sovereign cloud initiatives and national cybersecurity investments accelerating cloud security adoption in France

- 14.3.5 ITALY

- 14.3.5.1 Increasing digital transformation initiatives and rising cyber threats driving cloud security demand in Italy

- 14.3.6 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: CLOUD SECURITY MARKET DRIVERS

- 14.4.2 CHINA

- 14.4.2.1 Cyber sovereignty, domestic cloud dominance, and AI-driven surveillance shaping cloud security architecture in China

- 14.4.3 JAPAN

- 14.4.3.1 Mature enterprise cloud adoption, regulatory compliance, and supply chain security concerns driving cloud security investments in Japan

- 14.4.4 INDIA

- 14.4.4.1 Explosive digital growth, hyperscaler expansion, and rising cybercrime driving cloud security market acceleration in India

- 14.4.5 AUSTRALIA

- 14.4.5.1 National cybersecurity strategies, critical infrastructure protection, and cloud-first policies driving security investments in Australia

- 14.4.6 REST OF ASIA PACIFIC

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 MIDDLE EAST & AFRICA: CLOUD SECURITY MARKET DRIVERS

- 14.5.2 GCC

- 14.5.2.1 Strong national cybersecurity strategies, sovereign cloud investments, and critical infrastructure protection accelerating cloud security demand in GCC countries

- 14.5.2.2 KSA

- 14.5.2.3 UAE

- 14.5.2.4 Rest of GCC countries

- 14.5.3 SOUTH AFRICA

- 14.5.3.1 Increasing cybercrime, financial sector digitization, and enterprise cloud adoption driving cloud security demand in South Africa

- 14.5.4 REST OF MIDDLE EAST & AFRICA

- 14.6 LATIN AMERICA

- 14.6.1 LATIN AMERICA: CLOUD SECURITY MARKET DRIVERS

- 14.6.2 BRAZIL

- 14.6.2.1 Rapid fintech growth, regulatory enforcement, and rising cyber threats driving cloud security demand in Brazil

- 14.6.3 MEXICO

- 14.6.3.1 Expanding digital economy, cross-border cloud adoption, and increasing cyber risks driving cloud security growth in Mexico

- 14.6.4 REST OF LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 15.2 REVENUE ANALYSIS, 2021-2025

- 15.3 MARKET SHARE ANALYSIS, 2025

- 15.4 BRAND COMPARISON

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.5.1 COMPANY VALUATION, 2026

- 15.5.2 FINANCIAL METRICS USING EV/EBIDTA, 2026

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.6.5.1 Company footprint

- 15.6.5.2 Offering footprint

- 15.6.5.3 Deployment mode footprint

- 15.6.5.4 Vertical footprint

- 15.6.5.5 Regional footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.7.5.1 Key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPETITIVE SCENARIO AND TRENDS

- 15.8.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 15.8.2 DEALS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 MICROSOFT

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches/developments

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 AWS

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/developments

- 16.1.2.3.2 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 PALO ALTO NETWORKS

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches/developments

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 CISCO

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches/developments

- 16.1.4.3.2 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 ZSCALER

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches/developments

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 IBM

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches/developments

- 16.1.6.3.2 Deals

- 16.1.7 CHECK POINT

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches/developments

- 16.1.7.3.2 Deals

- 16.1.8 NETSKOPE

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches/developments

- 16.1.8.3.2 Deals

- 16.1.9 AKAMAI

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches/developments

- 16.1.9.3.2 Deals

- 16.1.10 WIZ

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches/developments

- 16.1.10.3.2 Deals

- 16.1.11 FORTINET

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches/developments

- 16.1.11.3.2 Deals

- 16.1.12 CLOUDFLARE

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches/developments

- 16.1.12.3.2 Deals

- 16.1.13 CROWDSTRIKE

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Product launches/developments

- 16.1.13.3.2 Deals

- 16.1.14 SENTINELONE

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches/developments

- 16.1.14.3.2 Deals

- 16.1.15 TREND MICRO

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Product launches/developments

- 16.1.15.3.2 Deals

- 16.1.1 MICROSOFT

- 16.2 OTHER KEY PLAYERS

- 16.2.1 ORCA SECURITY

- 16.2.2 SYSDIG

- 16.2.3 QUALYS

- 16.2.4 TENABLE

- 16.2.5 RAPID7

- 16.2.6 MENLO SECURITY

- 16.2.7 AQUA SECURITY

- 16.2.8 SECPOD

- 16.2.9 PLEXICUS

- 16.2.10 UPWIND SECURITY

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakup of primary profiles

- 17.1.2.2 Key industry insights

- 17.2 DATA TRIANGULATION

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 TOP-DOWN APPROACH

- 17.3.2 BOTTOM-UP APPROACH

- 17.4 MARKET FORECAST

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 AUTHOR DETAILS