|

시장보고서

상품코드

2066436

에너지 분야 클라우드 보안 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cloud Security In Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

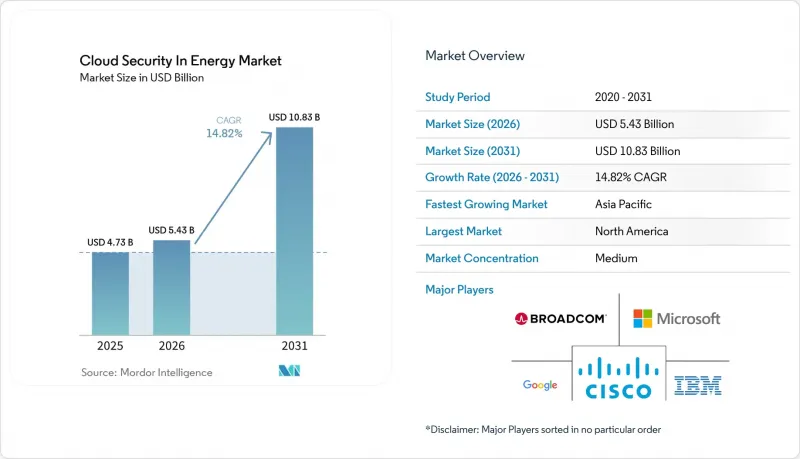

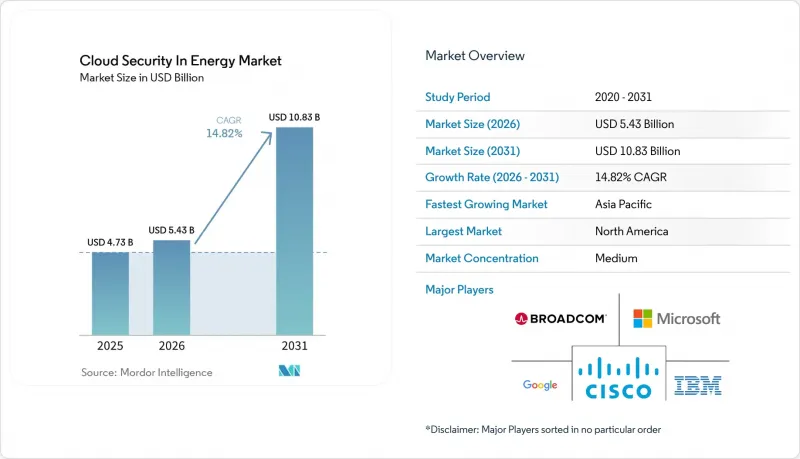

Mordor Intelligence에 의하면, 에너지 분야 클라우드 보안 시장 규모는 2025년 47억 3,000만 달러로 평가되었습니다. 2026년에는 54억 3,000만 달러로 확대되어 2031년까지 108억 3,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 14.82%로 성장할 전망입니다.

본 보고서는 솔루션 유형(ID 및 액세스 관리, 데이터 유출 방지 등), 보안 유형(용도 보안 등), 서비스 모델(Infrastructure-As-A-Service, Platform-As-A-Service, Software-As-A-Service), 배포 유형(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 에너지 분야 클라우드 보안 시장 동향 및 인사이트

사이버 위협 증가

2024년에는 랜섬웨어 및 국가가 개입한 공격이 급증하여, 북미의 공공시설 및 파이프라인을 표적으로 한 주요 사고 건수가 47건에 달했으며, 이는 전년 대비 38% 증가한 수치입니다. 공격자들은 구형 감시·제어 및 데이터 수집(SCADA) 자산과 클라우드 분석 플랫폼 간의 격차를 악용하고 있으며, 이 접점에서는 많은 엔드포인트에서 여전히 다단계 인증이 도입되지 않은 상태입니다. 사이버보안·인프라보안청(CISA) 등 기관들은 ‘Volt Typhoon’과 같이 중요 인프라 내에서 최대 5년 동안 감지되지 않은 채 지속된, 수년에 걸친 침입 사례를 보고하고 있습니다. 현재, 유틸리티자들은 운영 기술(OT)의 원격 측정 데이터를 수집하고, 이를 ID 데이터와 대조하여 물리적 손상이 발생하기 전에 비정상적인 차단기 명령을 감지할 수 있는 플랫폼을 우선적으로 도입하고 있습니다. 이러한 수요에 힘입어 보안 정보 및 이벤트 관리(SIEM) 시스템의 도입이 확대되면서, 감지부터 대응까지 걸리는 평균 소요 시간이 몇 시간에서 몇 분으로 단축되었습니다.

공급망 전반에 걸친 IoT 도입 확대

국제에너지기구(IEA)의 보고서에 따르면, 2024년 전 세계 에너지 산업 분야에서 25억 대의 연결 기기가 가동되었으며, 그 총 수는 2028년까지 40억 대를 넘어설 것으로 예측됩니다. 파이프라인, 변압기, 해상 풍력 터빈에서는 끊임없이 텔레메트리 데이터가 생성되며, 이러한 데이터는 공용 네트워크를 통해 안전하게 전송되어야 합니다. 관리되지 않는 센서 1대마다 새로운 공격 표적이 생겨납니다. 2024년 ‘Mirai’ 변종이 분산 서비스 거부(DDoS) 공격을 통해 18만 대의 에너지 관련 기기를 장악한 사례가 그 한 예입니다. 현재 사업자들은 기기 인증, 전송 중인 데이터의 암호화, 에지에서의 정책 적용을 필수 조건으로 삼고 있으며, 수백만 대에 달하는 현장 센서를 대규모로 도입하고 보호할 수 있는 클라우드 플랫폼에 자금을 투자하고 있습니다. 이러한 제어 조치는 가동 시간을 향상시키고, 현장 출장을 줄여주는 예측 유지보수 프로그램도 지원합니다.

OT 분야의 숙련된 클라우드 보안 전문가 부족

미국 에너지부에 따르면, 2024년 기준으로 미국 전력 회사의 68%가 산업용 프로토콜과 클라우드 제어 모두에 정통한 인력을 확보하지 못한 상태였습니다. 이러한 인력 부족으로 인해 매니지드 서비스 제공업체에 대한 의존도가 높아지고 있지만, 많은 외부 팀은 가동 중단 시간이 전혀 없는 환경에 필요한 운영 경험이 부족합니다. 아시아태평양도 비슷한 부족 현상에 직면해 있습니다. 인도에서만 해도 2030년까지 1만 5,000명의 OT 보안 전문가가 추가로 필요할 것으로 예측됩니다. 전력 회사는 감지 및 대응 업무를 외부에 위탁하는 비중을 늘리고 있지만, 제3자에 의한 접근은 신뢰의 사슬을 확대시키고 엄격한 계약 감시를 필요로 하기 때문에 결과적으로 단기적인 도입 속도를 제한하게 됩니다.

부문별 분석

이 부문은 가장 강력한 성장 전망을 보이고 있으며, 보안 정보 및 이벤트 관리(SIEM) 도구는 연평균 성장률(CAGR) 15.96%로 확대될 것으로 예측됩니다. 이러한 추세는 해당 부문이 독립형 방화벽에서 방화벽 로그, 감시·제어 및 데이터 수집(SCADA) 경보, 그리고 ID 신호를 통합하는 분석으로 전환되고 있음을 반영합니다. 2025년에도 ID 및 액세스 관리(IAM)는 여전히 매출 점유율의 24.78%를 차지해, 기본적인 인증 정보 관리에 대한 지속적인 수요가 부각되고 있습니다. 전력·가스 업계의 보안 정보 및 이벤트 관리(SIEM) 솔루션을 활용한 에너지 분야 클라우드 보안 시장 규모는 전력·가스 사업자들이 비정상적인 차단기 트립이나 터빈 정지 명령을 감지하는 기존 상관 분석 패키지를 도입함에 따라 2031년까지 두 배로 증가할 전망입니다. Splunk나 IBM과 같은 벤더들은 에너지 업계 특유의 규칙을 통합함으로써 사고 조사 주기를 몇 분으로 단축하고 있습니다.

데이터 유출 방지(DLP), 침입 감지 시스템(IDS) 및 암호화에 대한 보안 투자가 솔루션 스택을 보완하고 있습니다. 석유 및 가스 업스트림 부문에서는 데이터 유출 방지(DLP)를 통해 수십억 규모의 가치를 지닌 지진 탐사 모델을 보호하고, 스토리지 버킷 설정 오류로 인한 부주의한 정보 유출을 방지하고 있습니다. OT(운영 기술)에 대응하는 침입 감지 시스템(IDS)은 현재 Modbus 및 DNP3 트래픽을 검사하여 레지스터에 대한 비정상적인 쓰기 작업을 감지하고 있습니다. 엣지에서 클라우드로 이어지는 경로의 암호화는 여전히 필수적이며, 각 유틸리티체는 2024년에 확정된 포스트 양자암호화 표준을 준수하기 위해 라이브러리 업데이트를 진행하고 있습니다. 이러한 도구들은 전반적으로 인력을 증원하지 않고도 격화되는 위협의 속도에 대응할 수 있는 다층 방어 체제를 뒷받침하고 있습니다.

유틸리티자들이 모놀리식 감시 제어 및 데이터 수집(SCADA) 시스템의 인간-기계 인터페이스를 마이크로서비스로 현대화함에 따라, 용도 보안 시장은 17.28% 성장할 것으로 전망됩니다. 네트워크 보안은 2025년에도 34.68%의 점유율을 유지했지만, 보안 대책의 초점이 경계에서 애플리케이션 프로그래밍 인터페이스(API) 게이트웨이와 서비스 메시로 이동함에 따라 그 점유율은 점차 줄어들고 있습니다. 에너지 분야 클라우드 보안 시장에서 용도 보안의 점유율이 확대되고 있습니다. 이는 모든 분산형 에너지 자원 집계기가 속도 제한, 입력 데이터 정제 및 OAuth 인증이 필수인 애플리케이션 프로그래밍 인터페이스(API) 호출을 통해 연결되기 때문입니다. 오픈 웹 용도 보안 프로젝트(OWASP)는 2024년의 최대 위험 요인으로 객체 수준 인증의 결함을 꼽았으며, 이는 동적 엔드포인트 간에 전력을 배전하는 송전망 사업자에게 심각한 우려 사항이 되고 있습니다.

데이터베이스, 엔드포인트 및 이메일 제어가 이러한 발전을 보완하고 있습니다. 데이터베이스 보안은 밀리초 단위의 지연이 수익에 영향을 미치는 트레이딩 데스크를 보호하며, 토큰화와 필드 수준 암호화를 통해 기밀성이 높은 입찰 정보를 안전하게 지켜줍니다. 엔드포인트 확장형 감지 및 대응(EDR)은 데이터 유출이 발생하기 전에 현장 기술자의 비정상적인 행동을 감지합니다. 사이버보안 및 인프라 보안국(CISA)에 따르면, 이메일 게이트웨이는 2024년 정보 유출 사고의 62%를 차지한 스피어 피싱 공격을 차단했습니다. 이러한 계층들이 하나로 통합되어 모든 자산, ID 및 워크로드를 둘러싼 제로 트러스트 경계를 강화합니다.

지역별 분석

북미는 2025년에 39.72%의 점유율을 차지했습니다. 이는 북미 전력 신뢰성 공사(NERC)의 중요 인프라 보호 규정과 연방 정부의 자금 지원에 힘입은 결과입니다. 미국 에너지부는 2024년, 첨단 사이버 보안 대책을 의무화하는 조건 하에 송전망 현대화에 35억 달러를 배정했습니다. 캐나다도 이와 유사한 지침을 발표했으며, 멕시코에서는 시장 자유화에 따라 도입 초기부터 제로 트러스트를 채택한 신규 프로젝트가 추진되었습니다. 이 지역의 전력 사업자들은 감사 기준을 충족하기 위해 보안 정보 이벤트 관리(SIEM) 및 ID·접근 관리(IAM) 솔루션에 크게 의존하고 있으며, 하이퍼스케일 데이터센터의 존재가 이러한 기술의 도입을 가속화하고 있습니다. 성숙도가 높음에도 불구하고, 해당 지역은 여전히 랜섬웨어에 대한 취약성을 안고 있으며, 이로 인해 높은 투자 수준이 지속되고 있습니다.

아시아태평양은 16.32%의 성장률이 예상되며, 지역별로는 가장 빠른 성장세를 보일 것으로 전망됩니다. 2030년까지 재생에너지 1,200기가와트를 달성하겠다는 중국의 계획이 클라우드의 대대적인 도입을 뒷받침하고 있으며, 그 대표적인 사례가 11억 명의 고객을 보유한 국가전망이 2024년에 진행한 도입입니다. 인도의 ‘스마트 그리드 미션’과 일본의 회복탄력성 전략은 On-Premise의 주권성과 버스트 용량을 결합한 하이브리드 클라우드에 대한 수요를 촉진하고 있습니다. 호주에서는 시장에 진출하는 모든 기업에 다단계 인증과 암호화 통신을 의무화하고 있으며, 이로 인해 보안 예산이 더욱 증가하고 있습니다. 그러나 기술 인력 부족이 걸림돌이 되어, 공공 서비스 제공업체들은 매니지드 서비스로의 전환을 피할 수 없게 되었습니다.

기타 지역은 유럽, 남미, 중동 및 아프리카로 구성되어 있습니다. 유럽에서는 NIS2 및 사이버 복원력법에 따라 가장 엄격한 규정 준수 체제가 시행되고 있으며, 이에 따라 유틸리티자들은 지속적인 모니터링 체계를 도입해야 하는 상황에 놓여 있습니다. 독일의 에너지 전환(Energiewende)에 따라 200만 건 이상의 분산형 에너지 자원이 창출되었으며, 이를 안전하게 시스템에 통합해야 할 필요가 대두되고 있습니다. 브라질의 2024년 결의안에 따르면, 연례 침투 테스트 실시와 보안 정보 이벤트 관리(SIEM) 시스템 도입이 의무화되어 있습니다. 중동에서는 사우디아라비아의 NEOM과 같은 메가 프로젝트에서 설계 단계부터 클라우드 네이티브 운영 기술의 보안이 규정되어 있습니다. 아프리카 각국에서는 제어 기능을 탑재한 태양광 발전 미니 그리드를 구축하고 있으며, 이를 통해 기존의 기술적 부채를 피하고 클라우드 우선 아키텍처로 나아가는 직접적인 길을 열어가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the cloud security in energy market size is expected to increase from USD 4.73 billion in 2025 to USD 5.43 billion in 2026 and reach USD 10.83 billion by 2031, growing at a CAGR of 14.82% over 2026-2031.

This report is Segmented by Solution Type (Identity and Access Management, Data Loss Prevention, and More), Security Type (Application Security, and More), Service Model (Infrastructure-As-A-Service, Platform-As-A-Service, and Software-As-A-Service), Deployment Type (Public Cloud, Private Cloud, and Hybrid Cloud), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Cloud Security In Energy Market Trends and Insights

Increasing Number of Cyber Threats

Ransomware and state-sponsored campaigns surged in 2024, with 47 major incidents targeting North American utilities and pipelines, a 38% jump from the prior year. Attackers exploit gaps between legacy supervisory control and data acquisition assets and cloud analytics platforms, a seam where multi-factor authentication is still absent on many endpoints. Agencies such as the Cybersecurity and Infrastructure Security Agency have documented multi-year intrusions, like Volt Typhoon, that remained undetected in critical infrastructure for up to five years. Utilities now prioritize platforms that ingest operational technology telemetry, correlate it with identity data, and spot anomalous breaker commands before physical damage occurs. This demand is driving the adoption of Security Information and Event Management, reducing the mean time to detect and respond from hours to minutes.

Increasing Adoption of IoT Across the Supply Chain

The International Energy Agency reported 2.5 billion connected devices in global energy operations as of 2024, and the total is expected to exceed 4 billion by 2028. Pipelines, transformers, and offshore turbines generate constant telemetry that must be transmitted securely over public networks. Each unmanaged sensor introduces a new attack surface, as illustrated by the 2024 Mirai variant, which co-opted 180,000 energy devices in a distributed denial-of-service attack. Operators now insist on device attestation, encrypted data-in-transit, and policy enforcement at the edge, channeling funds toward cloud platforms capable of onboarding and securing millions of field sensors at scale. These controls also support predictive maintenance programs that boost uptime and reduce truck rolls.

Shortage of Skilled Cloud Security Professionals in Operational Technology

In 2024, 68% of U.S. electric utilities lacked personnel fluent in both industrial protocols and cloud controls, according to the Department of Energy. The talent gap necessitates a heavier reliance on managed service providers, yet many external teams lack the operational experience necessary for zero-downtime environments. Asia Pacific faces similar deficits: India alone needs 15,000 additional operational technology security specialists by 2030. Utilities increasingly outsource detection and response, but third-party access expands the chain of trust and mandates rigorous contract oversight, ultimately constraining near-term adoption velocity.

Other drivers and restraints analyzed in the detailed report include:

- Rising Integration of Smart Grid and Distributed Energy Resources

- Growing Regulatory Mandates for Zero-Trust Architectures in Critical Infrastructure

- Sovereign Cloud Compliance and Data Residency Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment generated the strongest growth outlook, with Security Information and Event Management tools forecast to expand at a 15.96% CAGR. This pace reflects the sector's shift from standalone firewalls to analytics that integrate firewall logs, supervisory control and data acquisition alarms, and identity signals. Identity and Access Management still held 24.78% revenue share in 2025, underscoring the continuing need for foundational credential controls. The cloud security in energy market size for Security Information and Event Management solutions is set to double by 2031 as utilities adopt pre-built correlation packs that flag unauthorized breaker trips or turbine shutdown commands. Vendors such as Splunk and IBM integrate energy-specific rules, compressing incident investigation cycles to minutes.

Security spending on Data Loss Prevention, Intrusion Detection Systems, and Encryption rounds out the solution stack. In upstream oil and gas, Data Loss Prevention protects seismic models valued at billions, preventing inadvertent exposure via misconfigured storage buckets. Operational technology-aware Intrusion Detection Systems now inspect Modbus and DNP3 traffic for abnormal register writes. Encryption remains mandatory for edge-to-cloud pathways: utilities are refreshing libraries to align with post-quantum standards finalized in 2024. Collectively, these tools underpin a defense-in-depth posture that can handle the heightened threat tempo without increasing headcount.

Application Security is projected to grow at 17.28% as utilities modernize monolithic supervisory control and data acquisition human-machine interfaces into microservices. While Network Security retained a 34.68% share in 2025, its share is being diluted as enforcement shifts from the perimeter to application programming interface (API) gateways and service meshes. The cloud security in energy sector market share for Application Security is widening because every distributed energy resource aggregator connects through application programming interface (API) calls that must be rate-limited, input-sanitized, and OAuth-authenticated. The Open Web Application Security Project ranked broken object-level authorization as the top risk for 2024, an acute concern for grid operators that dispatch power across dynamic endpoints.

Database, Endpoint, and Email controls complement this progression. Database Security protects trading desks where millisecond latency drives profit; tokenization and field-level encryption defend sensitive bids. Extended detection and response on endpoints detects anomalous field engineer behavior before data exfiltration occurs. Email gateways block spear-phishing campaigns, which, according to the Cybersecurity and Infrastructure Security Agency, accounted for 62% of breaches in 2024. Together, these layers tighten the zero-trust perimeter around every asset, identity, and workload.

Geography Analysis

North America held a 39.72% share in 2025, propelled by the North American Electric Reliability Corporation's Critical Infrastructure Protection regulations and federal funding. The U.S. Department of Energy allocated USD 3.5 billion in 2024 for grid modernization, stipulating advanced cybersecurity controls. Canada followed with a similar mandate, and Mexico's market liberalization led to greenfield deployments that adopted zero-trust from day one. Utilities in the region heavily rely on Security Information and Event Management (SIEM) and Identity and Access Management (IAM) solutions to meet audit benchmarks, and the presence of hyperscale data centers accelerates the adoption of these technologies. Despite its maturity, the region remains vulnerable to ransomware, which continues to drive high investment levels.

Asia Pacific is forecast to grow at 16.32%, the fastest regional pace. China's plan to achieve 1,200 gigawatts of renewable energy by 2030 drives massive cloud adoption, exemplified by State Grid's 2024 deployment, which covers 1.1 billion customers. India's Smart Grid Mission and Japan's resilience agenda are bolstering demand for hybrid cloud, which combines on-premises sovereignty with burst capacity. Australia mandates multi-factor authentication and encrypted links for all market participants, further lifting security budgets. Skills shortages, however, pose a brake, pushing utilities toward managed services.

Europe, South America, the Middle East, and Africa form the remainder. Europe enforces the toughest compliance regime under the NIS2 and the Cyber Resilience Act, prompting utilities to adopt continuous monitoring. Germany's Energiewende created over 2 million distributed energy resources, demanding secure onboarding. Brazil's 2024 resolution requires annual penetration tests and the deployment of Security Information and Event Management (SIEM). In the Middle East, megaprojects such as NEOM in Saudi Arabia specify cloud-native operational technology security from the blueprint stage. African nations are deploying solar mini-grids with embedded controls, thereby bypassing legacy technical debt and opening direct paths to cloud-first architectures.

- Amazon Web Services Inc.

- Microsoft Corporation

- IBM Corporation

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- McAfee Corp.

- Broadcom Inc.

- Google LLC

- Dell Technologies Inc.

- Zscaler Inc.

- Tenable Holdings Inc.

- Qualys Inc.

- Rapid7 Inc.

- Netskope Inc.

- CrowdStrike Holdings Inc.

- Okta Inc.

- Imperva Inc.

- Darktrace plc

- Nozomi Networks Inc.

- Dragos Inc.

- Claroty Ltd.

- Schneider Electric SE

- Siemens AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of IoT Across the Supply Chain

- 4.2.2 Increasing Number of Cyber Threats

- 4.2.3 Rising Integration of Smart Grid and Distributed Energy Resources

- 4.2.4 Growing Regulatory Mandates for Zero-Trust Architectures in Critical Infrastructure

- 4.2.5 Emergence of Cloud-Native Operational Technology Security Platforms Specific to Energy

- 4.2.6 Declining Costs of Edge-to-Cloud Secure Connectivity Solutions Enabled by 5G Private Networks

- 4.3 Market Restraints

- 4.3.1 Integration with Existing Architecture

- 4.3.2 Shortage of Skilled Cloud Security Professionals in Operational Technology

- 4.3.3 Sovereign Cloud Compliance and Data Residency Constraints

- 4.3.4 High Perceived Cost of Continuous Cloud Security Posture Management

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers or Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Identity and Access Management

- 5.1.2 Data Loss Prevention

- 5.1.3 IDS or IPS

- 5.1.4 Security Information and Event Management

- 5.1.5 Encryption

- 5.1.6 Other Solution Type

- 5.2 By Security Type

- 5.2.1 Application Security

- 5.2.2 Database Security

- 5.2.3 Endpoint Security

- 5.2.4 Network Security

- 5.2.5 Web and Email Security

- 5.2.6 Other Security Type

- 5.3 By Service Model

- 5.3.1 Infrastructure-as-a-Service

- 5.3.2 Platform-as-a-Service

- 5.3.3 Software-as-a-Service

- 5.4 By Deployment Type

- 5.4.1 Public Cloud

- 5.4.2 Private Cloud

- 5.4.3 Hybrid Cloud

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank or Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 IBM Corporation

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Palo Alto Networks Inc.

- 6.4.6 Fortinet Inc.

- 6.4.7 Check Point Software Technologies Ltd.

- 6.4.8 Trend Micro Incorporated

- 6.4.9 McAfee Corp.

- 6.4.10 Broadcom Inc.

- 6.4.11 Google LLC

- 6.4.12 Dell Technologies Inc.

- 6.4.13 Zscaler Inc.

- 6.4.14 Tenable Holdings Inc.

- 6.4.15 Qualys Inc.

- 6.4.16 Rapid7 Inc.

- 6.4.17 Netskope Inc.

- 6.4.18 CrowdStrike Holdings Inc.

- 6.4.19 Okta Inc.

- 6.4.20 Imperva Inc.

- 6.4.21 Darktrace plc

- 6.4.22 Nozomi Networks Inc.

- 6.4.23 Dragos Inc.

- 6.4.24 Claroty Ltd.

- 6.4.25 Schneider Electric SE

- 6.4.26 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment