|

시장보고서

상품코드

2055593

우주 추진 시장(-2031년) : 플랫폼, 유형(고체, 액체, 전기, 하이브리드), 컴포넌트(홀 효과 스라스타, 바이오 추진제, 추진제 탱크, 로켓 엔진, 노즐, PPU), 최종사용자, 서비스, 지역별Space Propulsion Market By Platform, Type (Solid, Liquid, Electric, Hybrid), Component (Hall-Effect Thrusters, Biopropellant, Propellant Tanks, Rocket Motor, Nozzle, PPU), End User, Services and Region - Global Forecast to 2031 |

||||||

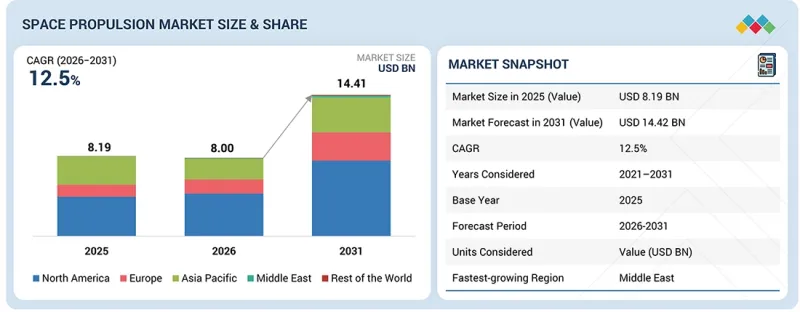

우주 추진 시장 규모는 예측 기간 중에 CAGR 12.5%로 확대되어 2026년 80억 달러에서 2031년에는 144억 1,000만 달러에 이를 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020년-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 플랫폼, 유형, 컴포넌트, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

궤도상 서비스, 스페이스 태그 임무, 우주 쓰레기 제거, 궤도 간 운송 수단의 확대에 따라, 반복적인 궤도 변경 및 유연한 임무 운영을 지원할 수 있는 추진 시스템에 대한 수요가 증가하고 있으며, 이는 시장 성장을 견인하고 있습니다.

“최종 사용자별로는 예측 기간 동안 상업 부문이 가장 큰 점유율을 차지할 것으로 예측됩니다.” '

이는 신규 위성 발사, 광대역 위성군, 지구관측 플랫폼 및 상업용 발사 활동의 상당 부분이 민간 기업에 의해 주도되고 있기 때문입니다. 또한, 이 부문은 LEO 위성군에서 교체 주기가 길어지고, 비용 효율이 높은 추진 시스템에 대한 수요가 확대되는 혜택도 누리고 있습니다.

“부품별로는 스러스터 부문이 2026년부터 2031년까지 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. '

스러스터 부문이 가장 높은 성장률을 보일 것으로 예상되는 이유는 우주선의 궤도 제어, 자세 제어, 궤도 수정 및 통제된 궤도 이탈에 스러스터가 직접적으로 필요하기 때문입니다. 위성 플랫폼의 소형화가 진행되고 임무 수행 시 기동 빈도가 높아짐에 따라, 소형 화학 추진기 및 전기 추진기에 대한 수요가 증가하고 있습니다. 또한 LEO 위성, 스페이스 태그, 달 탐사선, 궤도상 서비스선(OOSV) 증가로 인해 임무 전반에 걸쳐 다양한 추진기 구성에 대한 수요가 높아지고 있습니다.

“예측 기간 동안 중동이 가장 빠르게 성장할 지역이 될 것으로 전망됩니다.” '

이는 주로 해당 지역의 각국이 위성 통신, 지구관측, 국가 우주 계획 및 국방 우주 역량에 대한 투자를 확대하고 있기 때문입니다. 해당 지역은 주로 위성 구매자에서 벗어나, 파트너십, 현지 기관 및 국가 위성 계획을 통해 보다 견고한 국내 우주 인프라를 구축하는 방향으로 전환하고 있습니다. 이로 인해 위성, 발사 접근성, 그리고 향후 심우주 탐사에 참여하는 데 필요한 추진 시스템에 대한 새로운 수요가 발생하고 있습니다.

본 보고서에서는 전 세계 우주 추진 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류, 지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 프로파일 등을 종합적으로 다루고 있습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성 이니셔티브

제8장 고객 현황과 구매 행동

제9장 우주 추진 시장 : 컴포넌트별

제10장 우주 추진 시장 : 최종사용자별

제11장 우주 추진 시장 : 플랫폼별

제12장 우주 추진 시장 : 추진 방식별

제13장 우주 추진 시장 : 지원 서비스별

제14장 우주 추진 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

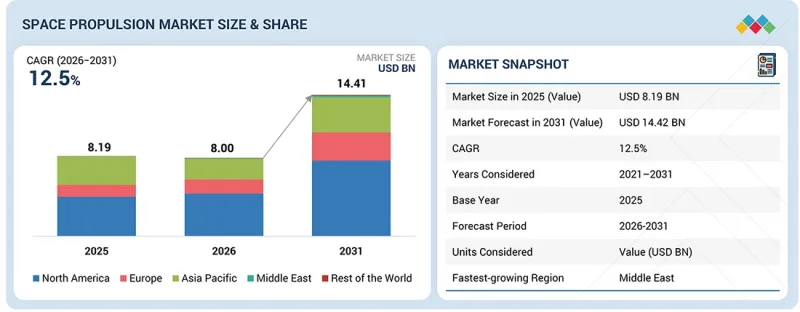

LSH 26.06.19The space propulsion market is expected to grow from USD 8.00 billion in 2026 to USD 14.41 billion in 2031, at a CAGR of 12.5% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Platform, Type, Component and Region |

| Regions covered | North America, Europe, APAC, RoW |

The market is growing as on-orbit servicing, space tug missions, debris removal, and orbital transfer vehicles are creating new demand for propulsion systems that can support repeated maneuvering and flexible mission operations.

"By end user, the commercial segment is projected to be the most dominant during the forecast period."

The commercial segment is projected to remain the leading segment during the forecast period because most new satellite launches, broadband constellations, Earth observation platforms, and commercial launch activity are driven by private companies. The segment also benefits from higher replacement cycles in LEO constellations and growing demand for cost-efficient propulsion packages.[SM1.1]

"By component, the thrusters segment is projected to grow at the highest CAGR from 2026 to 2031."

The thrusters segment is projected to grow at the fastest rate because thrusters are directly required for spacecraft maneuvering, attitude control, orbit correction, and controlled deorbiting. As satellite platforms become smaller and missions become more maneuver-intensive, demand is rising for compact chemical and electric thrusters. Growth in LEO satellites, space tugs, lunar spacecraft, and on-orbit servicing vehicles is also increasing the need for multiple thruster configurations across missions.[SM2.1]

"The Middle East is projected to be the fastest-growing region during the forecast period."

The Middle East is projected to be the fastest-growing region through 2031, mainly because countries in the region are increasing investments in satellite communication, Earth observation, national space programs, and defense-space capabilities. The region is moving from being mainly a satellite buyer to building stronger domestic space infrastructure through partnerships, local agencies, and sovereign satellite programs. This creates new demand for propulsion systems linked to satellites, launch access, and future deep space participation.[SM3.1]

The breakdown of profiles for primary participants in the space propulsion market is provided below:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: Directors - 20%, Managers - 10%, and Others - 70%

- By Region: North America - 30%, Europe - 15%, Asia Pacific - 40%, Middle East - 10%, Rest of the World - 5%

Research Coverage:

This market study covers the space propulsion market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to buy this report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall space propulsion market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market drivers (rising launch vehicle and satellite deployment activity, growing need for station keeping, orbit raising, collision avoidance, and deorbiting), restraints (high qualification, safety testing, and mission assurance cost, supply chain constraints in space-qualified propulsion components), opportunities (adoption of green and non-toxic propulsion systems, demand for advanced propulsion in cislunar, deep space, and space tug missions), challenges (platform-specific integration complexity across satellites, launch vehicles, spacecraft, landers, and rovers, environmental and licensing scrutiny linked to higher launch and re-entry activity)

- Market Penetration: Comprehensive information on space propulsion offered by the top players in the market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the space propulsion market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the space propulsion market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the space propulsion market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 HIGH-GROWTH SEGMENTS

- 2.4 DISRUPTIVE TRENDS SHAPING MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SPACE PROPULSION MARKET

- 3.2 SPACE PROPULSION MARKET, BY PLATFORM

- 3.3 SPACE PROPULSION MARKET, BY PROPULSION TYPE

- 3.4 SPACE PROPULSION MARKET, BY CHEMICAL PROPULSION

- 3.5 SPACE PROPULSION MARKET, BY NON-CHEMICAL PROPULSION

- 3.6 SPACE PROPULSION MARKET, BY COMPONENT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising launch frequency

- 4.2.1.2 Growing satellite density and orbital congestion

- 4.2.1.3 Increasing investment in lunar and deep-space missions

- 4.2.2 RESTRAINTS

- 4.2.2.1 High qualification, safety testing, and mission assurance costs

- 4.2.2.2 Supply chain constraints in space-qualified propulsion components

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Adoption of green and non-toxic propulsion systems

- 4.2.3.2 Rise of in-space servicing and orbital transfer

- 4.2.4 CHALLENGES

- 4.2.4.1 Platform-specific integration complexity

- 4.2.4.2 Environmental and licensing scrutiny

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 AFFORDABLE AND MINIATURIZED PROPULSION FOR SMALL SATELLITES

- 4.3.2 HIGH-ENDURANCE PROPULSION FOR CISLUNAR AND DEEP-SPACE MISSIONS

- 4.3.3 STANDARDIZED AND MODULAR PROPULSION ARCHITECTURES

- 4.3.4 SCALABLE PROPULSION FOR IN-SPACE SERVICING AND ORBITAL TRANSFER

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 SATELLITE MANUFACTURING AND SMALL SATELLITE ECOSYSTEM

- 4.4.2 LAUNCH VEHICLES AND SPACE TRANSPORTATION INFRASTRUCTURE

- 4.4.3 DEEP-SPACE EXPLORATION AND IN-SPACE MOBILITY SERVICES

- 4.4.4 ELECTRIC PROPULSION, ADVANCED ELECTRONICS, AND ENERGY SYSTEMS

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 ECOSYSTEM ANALYSIS

- 5.1.1 PROMINENT COMPANIES

- 5.1.2 PRIVATE AND SMALL ENTERPRISES

- 5.1.3 END USERS

- 5.2 VALUE CHAIN ANALYSIS

- 5.3 TRADE ANALYSIS

- 5.3.1 IMPORT SCENARIO (HS CODE 880260)

- 5.3.2 EXPORT SCENARIO (HS CODE 880260)

- 5.4 CASE STUDY ANALYSIS

- 5.4.1 LANDSPACE LAUNCHES METHANE-POWERED ZHUQUE-2 ROCKET

- 5.4.2 ASTROBOTIC COMPLETES ROTATING DETONATION ROCKET ENGINE TESTING

- 5.4.3 ARKADIA SPACE DEPLOYS GREEN PROPULSION SYSTEM FOR SATELLITES

- 5.5 KEY CONFERENCES AND EVENTS, 2026

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 MACROECONOMIC OUTLOOK

- 5.8.1 GDP TRENDS AND FORECAST

- 5.8.2 TRENDS IN GLOBAL SPACE INDUSTRY

- 5.8.3 TRENDS IN GLOBAL SPACE PROPULSION INDUSTRY

- 5.9 IMPACT OF 2025 US TARIFF

- 5.9.1 KEY TARIFF RATES

- 5.9.2 PRICE IMPACT ANALYSIS

- 5.9.3 IMPACT ON COUNTRY/REGION

- 5.9.3.1 US

- 5.9.3.2 Europe

- 5.9.3.3 Asia Pacific

- 5.9.4 IMPACT ON END-USE INDUSTRY

- 5.10 VOLUME DATA

- 5.11 PRICING ANALYSIS

- 5.11.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.11.2 INDICATIVE PRICING ANALYSIS, BY LAUNCH VEHICLE

- 5.12 BUSINESS MODELS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ELECTRIC PROPULSION SYSTEMS

- 6.1.2 SOLAR SAILS

- 6.1.3 ION PROPULSION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 HEAT MANAGEMENT SYSTEMS

- 6.2.2 ADVANCED PROPELLANT MANAGEMENT

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 MAGNETOPLASMADYNAMIC THRUSTERS

- 6.3.2 AUTONOMOUS PROPULSION

- 6.4 TECHNOLOGY ROADMAP

- 6.5 IMPACT OF AI/GEN AI

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 CASE STUDIES ON AI IMPLEMENTATION

- 6.5.3 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT AI/GEN AI

- 6.6 PATENT ANALYSIS

- 6.7 FUTURE APPLICATIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 GREEN PROPULSION AND LOW-TOXICITY FUEL DEVELOPMENT

- 7.2.2 ELECTRIC PROPULSION FOR FUEL EFFICIENCY

- 7.2.3 REUSABLE LAUNCH VEHICLE DEVELOPMENT

- 7.2.4 ORBITAL DEBRIS MITIGATION

- 7.2.5 LIGHTWEIGHT AND EFFICIENT ENGINE MANUFACTURING

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING EVALUATION CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

9 SPACE PROPULSION MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 THRUSTERS

- 9.2.1 COMPLEX SPACECRAFT OPERATIONS AND INCREASED ORBITAL ACTIVITIES TO DRIVE MARKET

- 9.2.2 CHEMICAL THRUSTERS

- 9.2.2.1 Cold & warm gas thrusters

- 9.2.2.2 Monopropellant thrusters

- 9.2.2.3 Bipropellant thrusters

- 9.2.3 ELECTRIC THRUSTERS

- 9.2.3.1 Ion thrusters

- 9.2.3.2 Hall-effect thrusters

- 9.2.3.3 Pulsed plasma thrusters

- 9.2.3.4 Magnetoplasmadynamic thrusters

- 9.3 PROPELLANT FEED SYSTEMS

- 9.3.1 SURGE IN LAUNCH ACTIVITY AND ADVANCEMENTS IN SPACECRAFT MISSIONS TO DRIVE MARKET

- 9.3.2 PROPELLANT TANKS

- 9.3.2.1 Monopropellant tanks

- 9.3.2.2 Bipropellant tanks

- 9.3.2.3 Oxidizer tanks

- 9.3.3 PRESSURE & FLOW REGULATORS

- 9.3.4 VALVES

- 9.3.5 TURBOPUMPS

- 9.3.6 COMBUSTION CHAMBERS

- 9.4 ROCKET MOTORS

- 9.4.1 NEED FOR PROPULSION SYSTEMS CAPABLE OF SUPPORTING VARIED MISSION REQUIREMENTS TO DRIVE MARKET

- 9.5 NOZZLES

- 9.5.1 EXPANSION OF REUSABLE LAUNCH SYSTEMS AND HIGH-PERFORMANCE SPACECRAFT PROGRAMS TO DRIVE MARKET

- 9.6 PROPULSION THERMAL CONTROL SYSTEMS

- 9.6.1 RISE OF DEEP-SPACE MISSIONS AND LONG-DURATION ORBITAL OPERATIONS TO DRIVE MARKET

- 9.7 POWER PROCESSING UNITS

- 9.7.1 FOCUS ON SPACECRAFT ENERGY EFFICIENCY AND LONG-DURATION ORBITAL MOBILITY TO DRIVE MARKET

- 9.8 OTHER COMPONENTS

10 SPACE PROPULSION MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 COMMERCIAL

- 10.2.1 GROWING COMMERCIAL SPACE ACTIVITY ACROSS COMMUNICATION AND REMOTE SENSING SERVICES TO DRIVE MARKET

- 10.2.2 SATELLITE OPERATORS & OWNERS

- 10.2.3 SPACE LAUNCH SERVICE PROVIDERS

- 10.3 GOVERNMENT & DEFENSE

- 10.3.1 CONTINUOUS FUNDING IN PROPULSION TECHNOLOGIES FOR SCIENTIFIC MISSIONS AND DEFENSE PREPAREDNESS TO DRIVE MARKET

- 10.3.2 NATIONAL SPACE AGENCIES

- 10.3.3 OTHERS

11 SPACE PROPULSION MARKET, BY PLATFORM

- 11.1 INTRODUCTION

- 11.2 SATELLITES

- 11.2.1 RISING SATELLITE CONSTELLATION DEPLOYMENTS TO DRIVE MARKET

- 11.2.2 SMALL SATELLITES (1-1,200 KG)

- 11.2.3 MEDIUM SATELLITES (1,201-2,000 KG)

- 11.2.4 LARGE SATELLITES (>2,000 KG)

- 11.3 CAPSULE & CARGO SPACECRAFT

- 11.3.1 INCREASING COLLABORATION BETWEEN GOVERNMENT SPACE AGENCIES AND PRIVATE COMPANIES TO DRIVE MARKET

- 11.3.2 CREWED SPACECRAFT

- 11.3.3 UNCREWED SPACECRAFT

- 11.4 INTERPLANETARY SPACECRAFT & PROBES

- 11.4.1 EXPANDING SCIENTIFIC EXPLORATION PROGRAMS FOCUSED ON PLANETARY STUDIES AND SPACE OBSERVATION TO DRIVE MARKET

- 11.5 LANDERS & ROVERS

- 11.5.1 GOVERNMENT'S FOCUS ON MOON AND MARS EXPLORATION PROGRAMS TO DRIVE MARKET

- 11.6 LAUNCH VEHICLES

- 11.6.1 GROWING IMPORTANCE OF SPACE ACCESS ACROSS INDUSTRIES TO DRIVE MARKET

- 11.6.2 SMALL LAUNCH VEHICLES

- 11.6.3 MEDIUM-TO-HEAVY LAUNCH VEHICLES

- 11.6.4 REUSABLE LAUNCH VEHICLES

12 SPACE PROPULSION MARKET, BY PROPULSION TYPE

- 12.1 INTRODUCTION

- 12.2 CHEMICAL

- 12.2.1 RISING CARGO TRANSPORTATION, SCIENTIFIC MISSIONS, AND DEFENSE PROGRAMS TO DRIVE MARKET

- 12.2.2 SOLID

- 12.2.3 LIQUID

- 12.2.3.1 Monopropellant

- 12.2.3.1.1 Non-green

- 12.2.3.1.2 Green

- 12.2.3.2 Bipropellant

- 12.2.3.2.1 Cryogenic

- 12.2.3.2.2 Hypergolic

- 12.2.3.1 Monopropellant

- 12.2.4 HYBRID

- 12.2.5 COLD/WARM GAS

- 12.3 NON-CHEMICAL PROPULSION

- 12.3.1 NEED FOR SUSTAINED SPACECRAFT MOVEMENT WITH IMPROVED FUEL EFFICIENCY TO DRIVE MARKET

- 12.3.2 ELECTRIC

- 12.3.2.1 Electrothermal

- 12.3.2.1.1 Argon

- 12.3.2.1.2 Hydrogen

- 12.3.2.1.3 Others

- 12.3.2.2 Electromagnetic

- 12.3.2.3 Electrostatic

- 12.3.2.3.1 Xenon

- 12.3.2.3.2 Krypton

- 12.3.2.3.3 Others

- 12.3.2.1 Electrothermal

- 12.3.3 SOLAR

- 12.3.3.1 Solar sail

- 12.3.3.2 Solar electric

- 12.3.3.3 Solar thermal

- 12.3.4 TETHER

- 12.3.5 NUCLEAR

13 SPACE PROPULSION MARKET, BY SUPPORT SERVICE

- 13.1 INTRODUCTION

- 13.2 DESIGN, ENGINEERING, OPERATION, & MAINTENANCE

- 13.3 HOT FIRING & ENVIRONMENTAL TEST EXECUTION

- 13.4 FUELING, LAUNCH, & GROUND SUPPORT

14 SPACE PROPULSION MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Public space investments and commercial launch expansion to drive market

- 14.2.2 CANADA

- 14.2.2.1 Satellite expansion and government-supported programs to drive market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 RUSSIA

- 14.3.1.1 Launch vehicle modernization and domestic space programs to drive market

- 14.3.2 FRANCE

- 14.3.2.1 Launcher innovation and high-thrust engine programs to drive market

- 14.3.3 GERMANY

- 14.3.3.1 Reusable space systems and research-led aerospace programs to drive market

- 14.3.4 UK

- 14.3.4.1 Domestic launch expansion and space transportation initiatives to drive market

- 14.3.5 ITALY

- 14.3.5.1 Reusable launcher programs and European space partnerships to drive market

- 14.3.1 RUSSIA

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Sustained government investment in launch vehicles and satellite constellations to drive market

- 14.4.2 SOUTH KOREA

- 14.4.2.1 National launch capability and private sector participation to drive market

- 14.4.3 JAPAN

- 14.4.3.1 Reusable rocket research and commercial space investment to drive market

- 14.4.4 AUSTRALIA

- 14.4.4.1 Sovereign launch infrastructure and hybrid rocket development to drive market

- 14.4.5 INDIA

- 14.4.5.1 Increasing satellite deployment and launch vehicle modernization to drive market

- 14.4.1 CHINA

- 14.5 MIDDLE EAST

- 14.5.1 GCC

- 14.5.1.1 Saudi Arabia

- 14.5.1.1.1 National space investments and satellite partnerships to drive market

- 14.5.1.2 UAE

- 14.5.1.2.1 Satellite manufacturing expansion and deep-space programs to drive market

- 14.5.1.1 Saudi Arabia

- 14.5.2 REST OF MIDDLE EAST

- 14.5.1 GCC

- 14.6 REST OF THE WORLD

- 14.6.1 LATIN AMERICA

- 14.6.1.1 Satellite programs and launch infrastructure development to drive market

- 14.6.2 AFRICA

- 14.6.2.1 Satellite deployment and national space programs to drive market

- 14.6.1 LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 15.3 MARKET SHARE ANALYSIS, 2025

- 15.4 REVENUE ANALYSIS, 2021-2025

- 15.5 BRAND/PRODUCT COMPARISON

- 15.6 COMPANY VALUATION AND FINANCIAL METRICS

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Propulsion type footprint

- 15.7.5.4 Component footprint

- 15.7.5.5 End user footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2026

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING

- 15.8.5.1 List of startups/SMEs

- 15.8.5.2 Competitive benchmarking of startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 DEALS

- 15.9.2 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 SPACEX

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.3.2 Other developments

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 NORTHROP GRUMMAN

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 L3HARRIS TECHNOLOGIES, INC.

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.3.2 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 ARIANEGROUP

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.3.2 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 SAFRAN

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.3.2 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 IHI CORPORATION

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.7 LOCKHEED MARTIN CORPORATION

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.3.2 Other developments

- 16.1.8 MOOG INC.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Other developments

- 16.1.9 THALES ALENIA SPACE

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.9.3.2 Other developments

- 16.1.10 SIERRA NEVADA CORPORATION

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Deals

- 16.1.10.3.2 Other developments

- 16.1.11 VACCO INDUSTRIES

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Other developments

- 16.1.12 BLUE ORIGIN

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.12.3.2 Other developments

- 16.1.13 EATON

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Other developments

- 16.1.14 RAFAEL ADVANCED DEFENSE SYSTEMS LTD.

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.15 OHB SE

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.15.3.2 Other developments

- 16.1.16 AIRBUS

- 16.1.16.1 Business overview

- 16.1.16.2 Products offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Deals

- 16.1.16.3.2 Other developments

- 16.1.17 AVIO

- 16.1.17.1 Business overview

- 16.1.17.2 Products offered

- 16.1.17.3 Recent developments

- 16.1.17.3.1 Deals

- 16.1.17.3.2 Other developments

- 16.1.1 SPACEX

- 16.2 OTHER PLAYERS

- 16.2.1 THRUSTME

- 16.2.2 URSA MAJOR

- 16.2.3 PHASEFOUR

- 16.2.4 EXOTRAIL

- 16.2.5 DAWN AEROSPACE

- 16.2.6 AST ADVANCED SPACE TECHNOLOGIES GMBH

- 16.2.7 STANFORD MU CORPORATION

- 16.2.8 MANASTU SPACE TECHNOLOGIES PRIVATE LIMITED

- 16.2.9 KREIOS SPACE

- 16.2.10 FIREFLY AEROSPACE

- 16.2.11 BUSEK CO. INC.

- 16.2.12 BELLATRIX AEROSPACE

- 16.2.13 BENCHMARK SPACE SYSTEMS

- 16.2.14 NAMMO

- 16.2.15 ENPULSION

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Primary sources

- 17.1.2.2 Key data from primary sources

- 17.1.2.3 Breakdown of primary interviews

- 17.1.1 SECONDARY DATA

- 17.2 FACTOR ANALYSIS

- 17.2.1 DEMAND-SIDE INDICATORS

- 17.2.2 SUPPLY-SIDE INDICATORS

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.3.1.1 Market size estimation methodology (demand side)

- 17.3.2 TOP-DOWN APPROACH

- 17.3.1 BOTTOM-UP APPROACH

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS